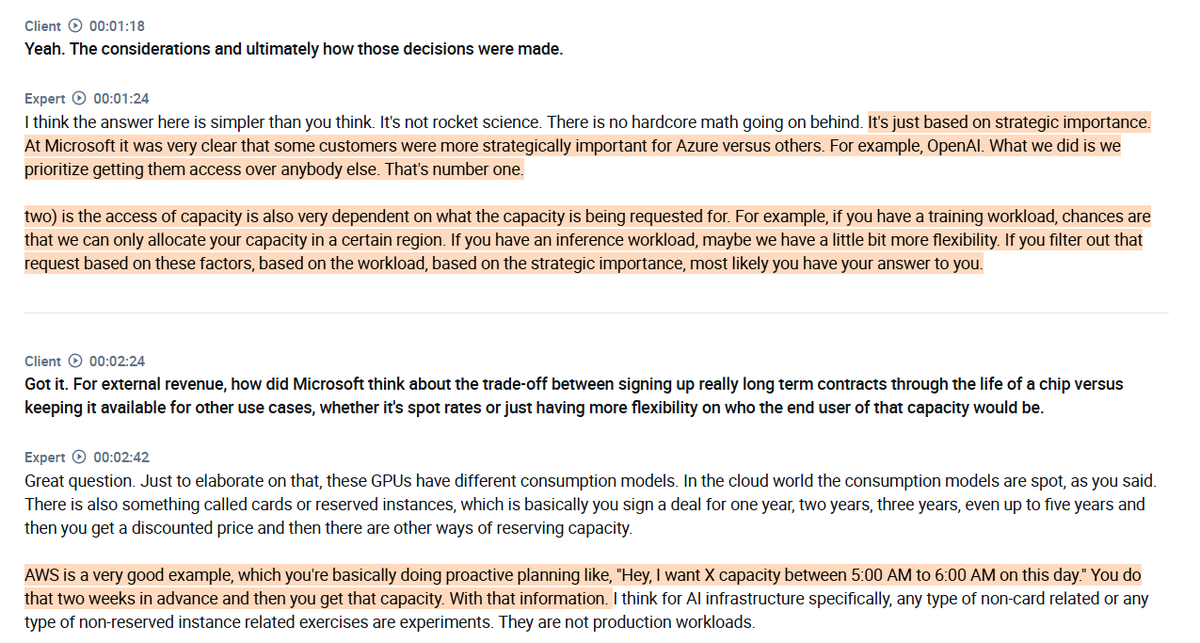

Today, the premise in the market is that semis and Anthropic will capture most of the value in the whole AI chain and that the SOTA model will always be used for the majority of economically valuable tasks.

I think that premise is wrong to some extent and might be a small shock for the market. The reason we have used the SOTA model for almost every task so far is that its capabilities have only recently become useful enough to provide value for many work tasks, especially agentic AI. At the same time, model progress is accelerating, which means that we are getting more and more capable models faster. The main reason why we won't use SOTA for every task is because it will be too expensive for most tasks. I think that in a year, we will look back and see that the premise that the SOTA model captures most of the usage and value will be wrong. Now, don't get me wrong: SOTA models will always have value and use, especially in tasks such as drug discovery and science.

So what happens to the market if SOTA models no longer capture most of the token's value?

The biggest AI labs' revenue growth rates slow down, combined with pressure on their margins as competition on non-SOTA models explodes. At the same time, the ability of AI model providers to raise new funds on the market via debt or equity also gets harder as the premise of »AI model commoditization, « at least on some layers, gets attention again. This leads to a portion of their planned future compute commitments with hyperscalers and neoclouds being released (because they can't pay for it) to other companies in the market.

In the short-term, it creates a gap where a portion of the compute that was »reserved« for the big AI model providers from data center builders gets released to other companies. That gap release of compute could further influence hyperscalers to reduce the steep growth curves of their CapEx spend, as the growth rates normalizes closer to the rates of non-AI model companies' ability to consume the tokens with smaller non-SOTA, more efficient models.

In the long term, this scenario is not bad for semis as the AI model layer leaves more of the margin to other layers, such as the data center and semis. At the same time, data center builders' business economics improve (having multiple small clients paying for compute vs 2 or 3 big buyers means the buyers have less pricing power).

In any case, the market is not prepared for this scenario, especially the gap that would happen in the short-term.

Did people really expect $META wouldn't charge a subscription for AI products and use their +3B distribution network?

$SNAP makes $5B in ad revenue and $1B in direct subs revenue (growing 87% YoY). $META can add a few $10B to its bottom line just by providing solid-value subscriptions.

Distribution is the ultimate AI bottleneck and moat, as we have AI models and services available in every app and platform.

Investors are really underestimating $META and $META AI. $META's AI app has been alongside OAI, Anthropic, and $GOOGL Gemini in terms of top downloads, since they launched Muse Spark, despite Muse Spark not being SOTA.

The reason for that is that $META has unprecedented distribution.

Now imagine what happens when $META delivers SOTA models. They have the talent, data, and compute.

It's coming...

@RihardJarc on how the hyperscalers are absolutely crushing right now.

"The core ad businesses at Meta and Google are accelerating because of AI, not in spite of it

Operating margins on cloud are expanding even as AI workloads scale

Custom ASICs are no longer a side project - they are the next big business segment

The era of “subsidized” compute is ending, and we are seeing the first hints of pricing power coming through"

https://t.co/Pf1FR5xiNV

I know the market wants to do what the market wants to do but can we just appreciate these growth numbers from some of the largest companies on earth:

- $GOOGL cloud +63% YoY

- $MSFT Azure +40% YoY

- $META revenue up 33% YoY

- $AMZN AWS +28% YoY

Amazing. Long-term investors pray for periods like this one.

I just published my Q1 alternative data report covering the cloud providers $AMZN, $GOOGL, and $MSFT:

- Data showing significant growth

- Expecting higher cloud growth than the consensus from one particular provider

- Surprising data on $MSFT Copilot

https://t.co/tvCPrKOprH

My deep dive article on $AMZN and why it is my biggest position:

1. Value of e-commerce in agentic shopping

2. Disruption of the Ad business

3. Agentic AI lead: MCP server adoption showing a strong lead for AWS vs peers

4. AWS (growth of traditional and AI compute).

5. Importance of Trainium

6. Valuation breakdown and the discount the market is giving

https://t.co/wrJQTRQSqO

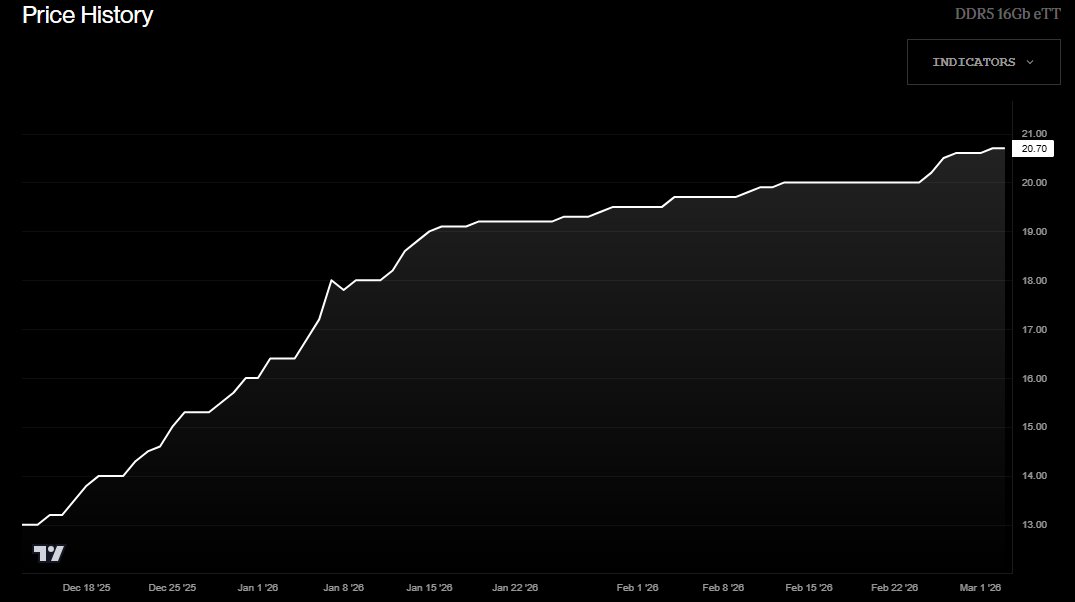

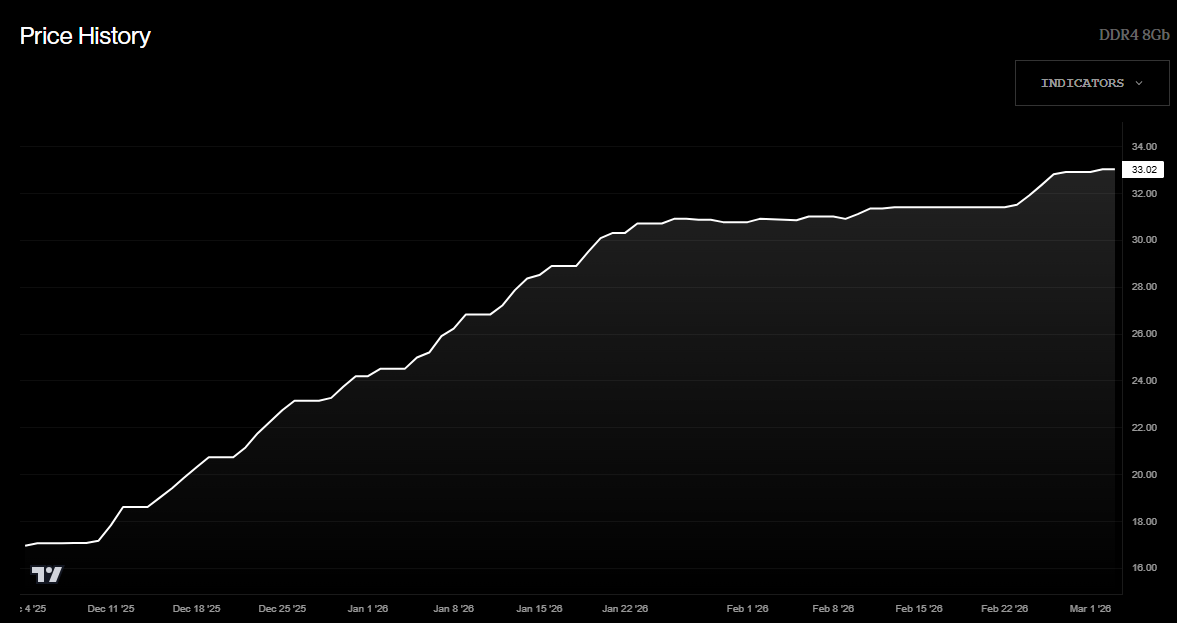

Contrary to some reporting that DRAM prices are falling, checking my alt data sources, not one shows DRAM spot prices falling; on the contrary, they again increased in the first days of March. This is DDR5 16Gb eTT and DDR4 8Gb.

While the prices won't go up forever, no fall yet, based on what I am seeing.

Samsung and SK Hynix are selling off 10% today because they have risen in the high single digits almost every day for quite some time now, and because South Korea is highly dependent on oil from the Middle East.

In a few weeks/months, some investors will again scratch their heads at the new highs these stocks will reach, because they are busy looking at the trees and missing the forest.

Both of these companies trade at 3-4x forward P/E ratios in one of the biggest memory cycles in history. They benefit in any case; $NVDA or ASIC, cloud or on-prem, or edge adoption, it doesn't matter.

And yes, if needed, South Korea will get its oil from somewhere else; they also hold approximately 208 days of oil cover, which not many countries can say.

I have owned Samsung and SK Hynix for quite some time and will continue to do so.

In general, the market, with all that is going on, especially around AI, is showing you that it is confused, and not many investors have a clear view of how this will unfold. For someone who has clarity, this is a perfect environment for catching opportunities.

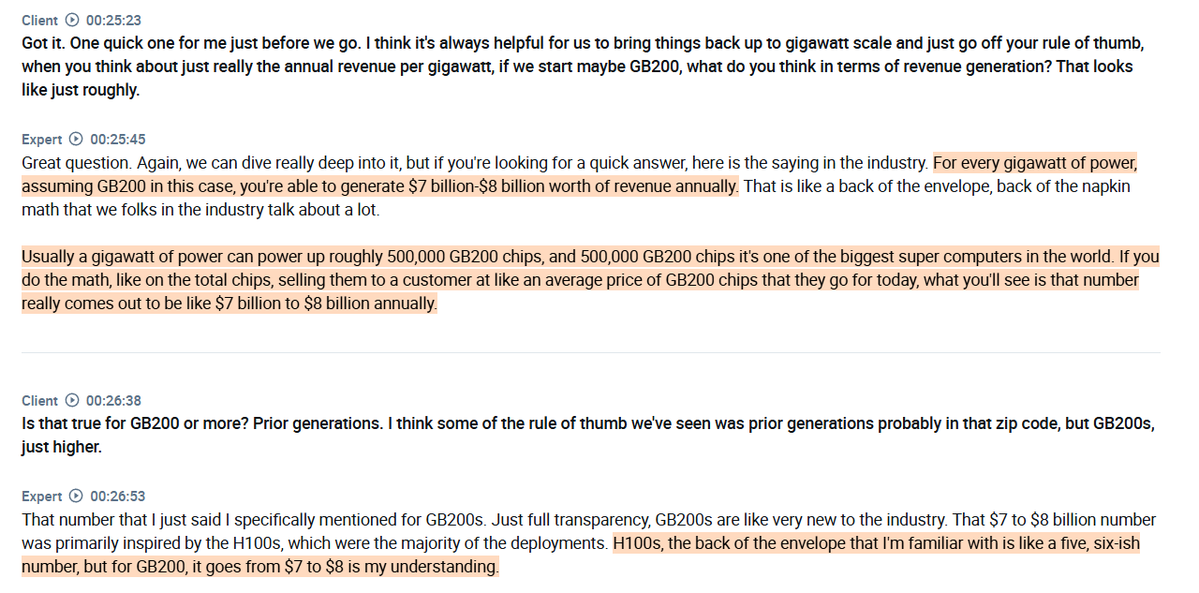

A very insightful conversation with a former $MSFT employee on cloud AI margins, GPU depreciation cycles, and the cloud economics in the AI era:

1. The expert highlights two key factors before discussing how $MSFT approaches ROIC targets in customer contracting conversations. First, GPU depreciation cycles have extended dramatically, from an initial estimate of 3 years all the way to 5, and later 8 or 9 years for certain chips. This means the original ROIC analysis has become significantly more favorable over time because the asset is lasting much longer than originally planned.

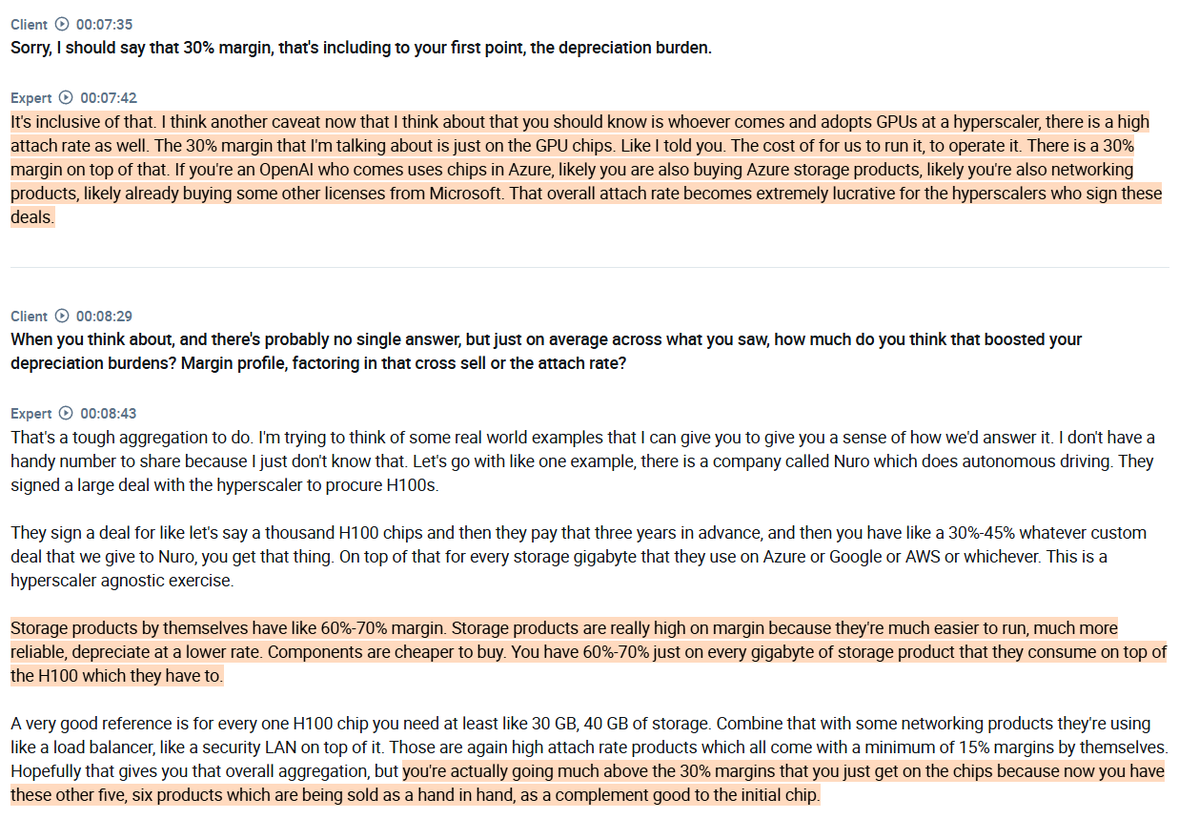

2. Second, strategic customers all operate on custom pricing deals, with those decisions made at the very top of the organization. The baseline approach is to use OpEx as the floor, with a minimum 30% margin built on top. He explains that this essentially covers the cost of capital on the original GPU investment, including depreciation.

3. The expert emphasizes that the V100 is the best real-world example of how depreciation cycles actually play out. That chip is nearly a decade old and still running at full utilization across many hyperscaler environments today, despite originally being depreciated over three years. Hyperscalers simply paid $NVDA to extend the warranty and kept generating margins from hardware that was already fully depreciated on paper.

4. Newer chips like the H100 and GB200 are a different story entirely, running at sustained high utilization around the clock, thermally constrained, and essentially impossible to repair, making replacement the only option when something fails. $NVDA has extended warranty terms for hyperscalers on H100-class systems, effectively taking on reliability risk and covering replacement costs.

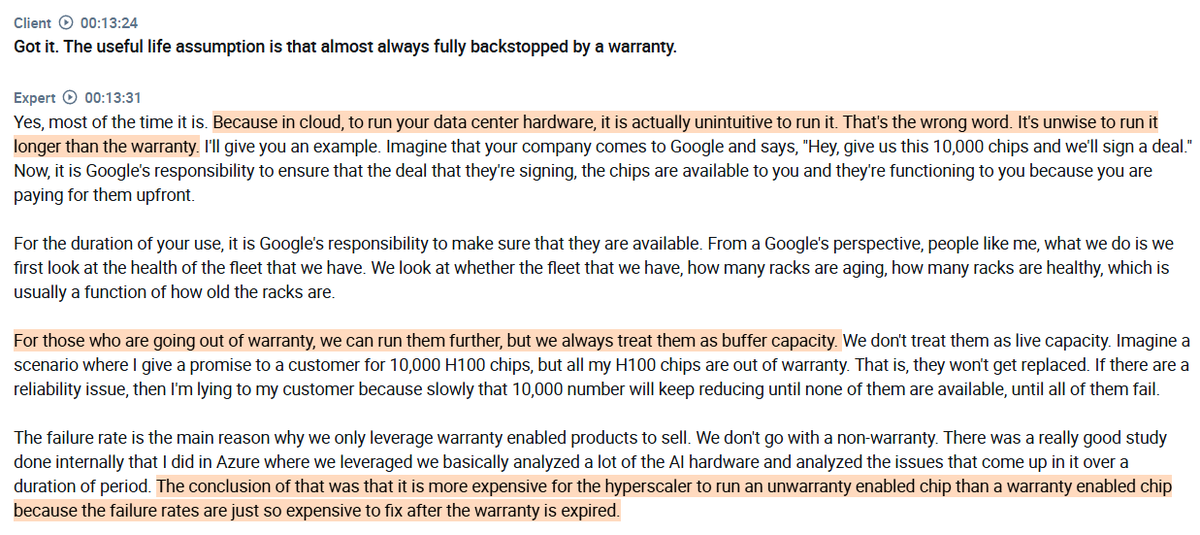

5. He is clear that running chips beyond their warranty is actually more expensive than staying within it, since failure rates without replacement coverage slowly erode customer commitments, which is why out-of-warranty chips are treated as buffer capacity rather than live capacity.

6. On the CapEx side, he estimates it costs roughly $30 to $35 billion dollars to stand up a gigawatt scale data center from scratch. Of that, around 80% goes toward IT infrastructure, primarily GPUs, CPUs, and memory, with the remaining 20% covering the physical shell and power setup. To put the GPU cost in perspective, each GB200 node costs around $60,000, with ten nodes stacked to form one rack at $600,000, and some hyperscalers go even higher. Given that everything in the supply chain remains constrained, he expects that overall CapEx figure to climb by another 5% or so from current levels.

found on @AlphaSenseInc

All of these $AMD and custom ASIC billion-dollar deals are great for $TSM and the memory providers (SK Hynix, Samsung & $MU).

Instead of just having one client ( $NVDA ) who can negotiate better terms, you now have multiple clients competing for the same supply.

$AMD and $META just announced a strategic partnership to deploy 6GW of $AMD GPUs.

Some people still don't get it when they were cheering about the $NVDA- $META partnership expansion last week, claiming that this shows that $NVDA is the only compute option.

No AI research lab wants to be exclusive to $NVDA, no one, because the risk is just too high.

Every research lab is expanding its compute stack to include $NVDA, $AMD, as well as ASICs such as TPU and Tranium. No one wants to be locked into one vendor and the $NVDA 75% tax.

The real power in the supply chain has shifted to fabs, advanced packaging, and the memory providers.

$META looks like one of the most defensible businesses in the AI age with almost zero disruption risk.

The moat is not the software its the network. TikTok is the only competitor over the last 10 years to get close to $META, but even TikTok needed a pandemic when everyone was looking for entertainment on their phones and tens of billions of dollars spent on ads (funny on $META) to build their network.

To build a distribution platform today in the AI age, this gets even more expensive as there are multiple more competitors fighting for the attention of consumers (because of things like vibe coding), pushing global ad prices up.

In addition, Traditional Search is losing organic eyeballs to AI surfaces, and AI surfaces remain questionable for ad business models, pushing even more advertisers towards $META and making ads more expensive.

Zuck has the ultimate cash machine, and he is pouring all that FCF towards building AI, which even further extends $META's moats and adds new business segments.

I just published my article on why CPUs are the new bottleneck of Agentic AI ( $AMD, $INTC, $NVDA, $TSM, $AMZN).

1. How exactly CPUs are used in agentic systems and what the demand looks like

2. Why, just for the basic enterprise usage, will we need to DOUBLE the current yearly CPU production.

3. Which companies benefit the most from this

https://t.co/HuzjrC4BrN

The gap between Wall Street and AI labs is massive right now.

The market is sweating over ROI and CapEx, while the AI community is burning every scrap of compute just to keep up with coding demands.

Meanwhile, $GOOGL's Demis Hassabis (who doesn't hype) says curing all diseases with the help of AI is "within reach" in the next decade.

On $AMZN's earnings call, Trainium was mentioned 27x times, while $NVDA was mentioned 0 times.

Also interesting comment:

»I think people know about our chips capability and our chips business, but I'm not sure folks realize how strong a chips company we've become over the last 10 years.

If you look at what we've done with Trainium, if you look at what we've done with Graviton, which is our CPU chip, which is about 40% better price performance than comparable x86 processors, 90% of the top 1,000 AWS customers are using Graviton very expansively. If you combine Trainium and Graviton, it's well over a $10 billion annualized run rate business, and it's still very early there.«

$GOOGL is a company that doesn’t do hype.

For them to go and increase CapEx from $90B to $180B is probably the most bullish thing long-term investors can see as it shows the scale of future revenue growth. I am shocked that at this stage most still don’t understand this.

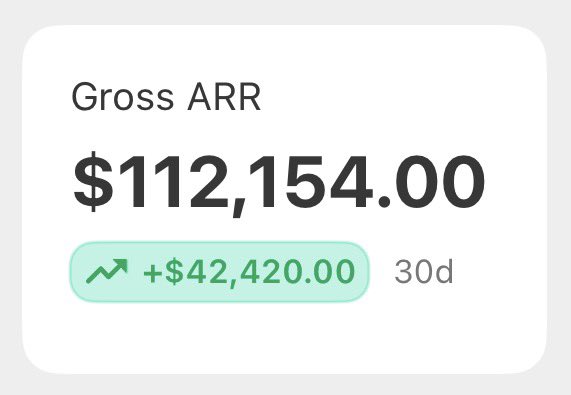

I normally don't do this, but as UncoverAlpha crossed the $100k ARR mark, I would like to thank all subscribers for their support!

UncoverAlpha has been one of the fastest-growing finance newsletters. We now have over 18k free subscribers, in addition to hundreds of paid subscribers, including more than 50 institutional investors and some of the largest global funds with over $50B in AUM.

The goal of the newsletter has always been and will continue to be to share data-driven analysis of the AI, semiconductor, and other tech sectors and companies. Technical yet understandable for the investment audience. We harness many alternative data providers to maximize value for our subscribers, and with the growth that we have achieved, we will deliver even more value in our work in the future with more data insights and better research.

One of the things I am most proud of is that, even with a paid tier that provides the most value, we still increased the value of our free tier and are growing free subscribers much faster than we did before the paid tier.

Stay tuned, as there are so many more things coming this year, all aimed at helping people with their research efforts.

Truly, thank you!

Anthropic with Claude Code is having its "ChatGPT" moment (Clawd bot, Cowork), as daily install counts in VS Code almost DOUBLE in January alone, growing way past OpenAI Codex & Gemini!

$AMZN, $GOOGL benefiting.

More details in the article:

https://t.co/6DQbux4iLW