Aletheia on $MU:

"We forecast MU’s EPS to jump 8.5x in CY27E, followed by a further 1.8x expansion in CY28E. This implies roughly 15x cumulative EPS growth and $350–400bn of FCF generation in FY26-28E."

"We now expect server DRAM ASP to jump a further 30% in C3Q26 (vs previous expectation of 10- 15%); this is likely to rise by another 10-15% in C4Q26 (same as previous expectation)"

"we now expect HBM ASP to double YoY in C2027"

"Our analysis shows that memory devices are becoming the most critical components in the AI hardware system as their combined content value are expected to cross over 70% in 2027 vs mid-40%s in 2025. For DRAM-intensive device such as Vera CPU, the SoCAAM alone contributes over 70% of BOM in 2H26; the full spec Vera CPU rack could reach a staggering $26M ASP per rack..."

Mizuho semi supply chain tracker: no delays 800VDC & strong demand $NVDA CPO switch:

"In the HVDC/800VDC investment case, the deployment schedule should be an average of 12-month lead-time from the initial system (like power rack) shipment by vendors, in our view"

"Lumentum ( $LITE ) highlighted a rising adoption rate of InP-based NPO from its clients and we also expect stronger Google TPU demand to boost $AVGO VCSEL-based NPO sales.

"micro-LED (uLED) based optical solutions that are developed and promoted by other chipmakers, such as Credo ( $CRDO ) in ALC (LED cables) and Avicena (private), to capture future scale-up (XPU to XPU) and scale-in (XPU to HBM) opportunities."

Scientists at Columbia University have edited the genes of human embryos for the first time using a technique called base editing.

They were able to change single letters in the DNA to remove mutations linked to heart disease.

This marks the first known case of altering an embryo after it was created, rather than just screening for traits.

The embryos weren’t implanted, but researchers say it’s now technically possible to create a child from genetically edited embryos.

Writers: Lucas, Oliver

Scientists used CRISPR to engineer gut-living hookworms to produce a medical antibody inside hamsters, as a proof of concept for turning parasites into living drug dispensaries for people with chronic diseases. Results are promising but needs refinement

https://t.co/aWB2I7xD6g

Exceptions should not become the rule. Labeling an entire group based on the behavior of a few is unfair and counterproductive. Like every other country, India has its share of rowdy or inconsiderate tourists—but they are the exception, not the norm. https://t.co/FDczdEdurZ

Cowen on $QCOM: 6/24 catalyst

"already has purchase orders in hand across multiple products, including custom ASICs, CPUs, and customer-specific engagements, such as its HUMAIN deal"

"Management pointed to a material revenue ramp beginning in the DecQ (F1Q27) and accelerating more meaningfully in fiscal 2027, with the potential to reach a multibillion-dollar scale."

Mizuho on Agentic AI CPU/servers: see Agentic AI driving demand higher, but memory/CPU supply potentially limit upside in 2H26E.

"believe the demand for traditional servers could come from both x86 (+ve $INTC, $AMD) and $ARM-based CPUs with ARM gaining overall share into 2027E."

"Estimate total server shipments for 2026E up 17% y/y to 14.6M units (prior: ~14.0M units) with non-AI server growth at up ~6% y/y (prior flattish y/y). Estimate AI servers growing at a 26% 2025-29E CAGR to reach 5.87M units by 2029E (prior: 5.67M units)"

"Continued Blackwell/Rubin ramps providing near-term tailwinds for $CRDO"

"We see AMD with Turin and Genoa continuing to see strong demand ahead of Venice ramps in 2H26E, while INTC continues to see Granite/Diamond Rapids supply constrained ahead of Coral Rapids in 2027E, and ARM continuing to benefit from partner ramps, ahead of upcoming AGI CPU, where demand was noted up 2x vs. launch, and potential ASIC announcement"

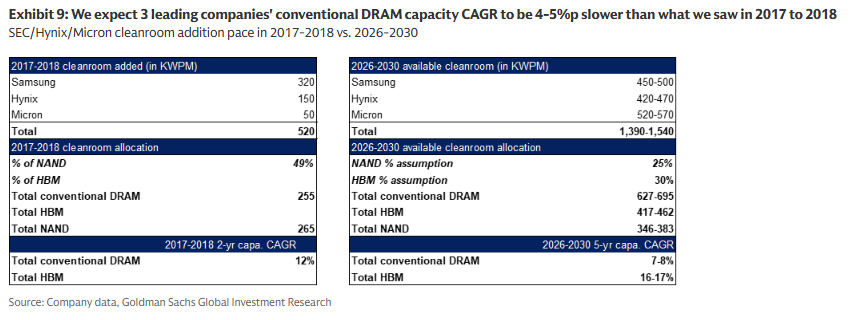

GS on memory ( $MU / $SNDK ):

"The key demand driver of both the 2017-2018 upcycle and the current upcycle is strong server demand. While the 2017-2018 upcycle was driven by cloud data center expansion, the current cycle is driven by massive AI server build out...memory demand is now closely tied to server demand where server segment comprises around 50% of DRAM demand and ~40% of NAND demand."

"given the long lead time (takes at least ~3 years to construct a fab and produce output), we expect conventional DRAM capacity addition pace by 2030 to be slower than the 2017-2018 upcycle."

"Based on our checks, LTAs are being discussed to include sizable prepayments and meaningful penalty clauses for non-compliance which could guarantee stronger binding power. Pricing is being discussed within a pre-determined range with a floor price that guarantees a high margin level on a sustainable basis."

Expect supply shortage to persist at least until 2028 and next year to be tighter than this year

"We now expect 2026E/2027E/2028E DRAM S/D to be in a larger undersupply of 5.0%/5.9%/3.9% (vs. prior expectations of 4.9%/2.5% undersupply in 2026E/2027E)"

"We now expect 2026E/2027E global DRAM demand to grow 28%/20% yoy (vs. +25%/+17% yoy previously), and introduce 2028E estimate of +19% yoy growth."

"We now expect 2026E/2027E/2028E NAND S/D to be in a larger undersupply of 4.4%/4.6%/3.0% (vs. prior expectations of 4.2%/2.1% undersupply in 2026E/2027E)"

"We now expect 2026E/2027E global NAND demand to grow 23%/20% yoy (vs. +22%/+15% yoy previously), and introduce our 2028E estimate of +19% yoy growth."

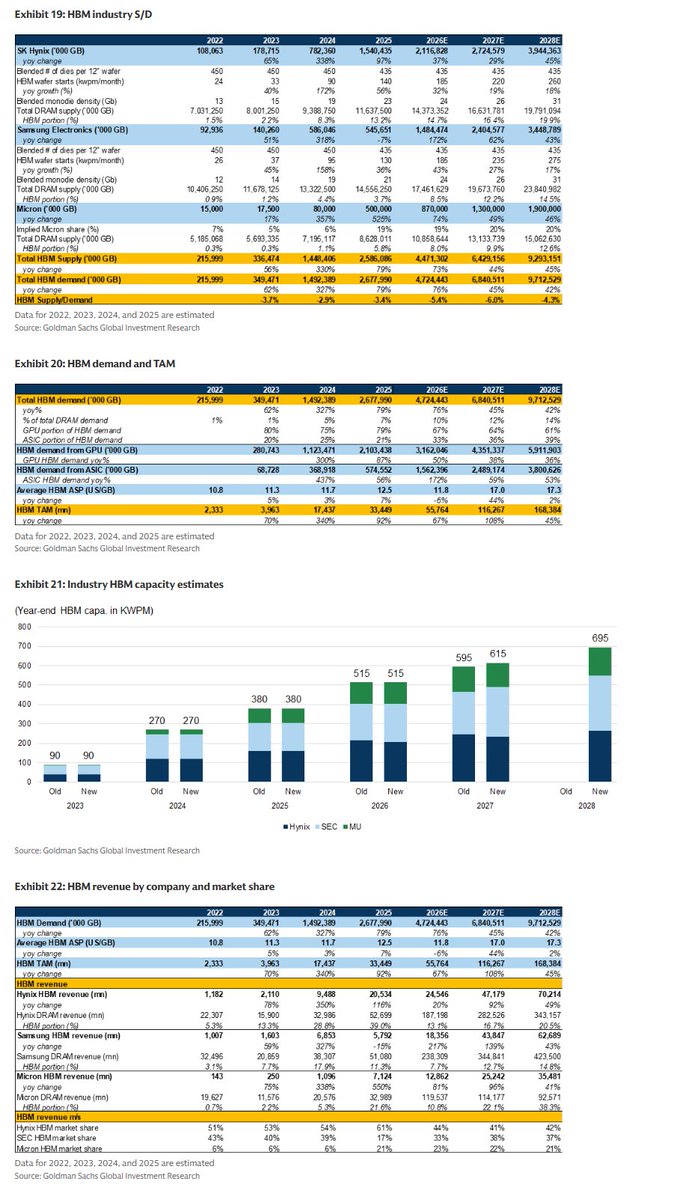

HBM: Expect a tighter 2027 S/D, and a significant ASP increase to lead to a +100%+ growth in TAM to US$116bn

We now expect 2026E/2027E/2028E HBM S/D to be in a larger undersupply of 5.4%/6.0%/4.3% (vs. prior expectations of 5.1%/4.0% undersupply in 2026E/2027E)

Significantly raise HBM ASP forecast as we expect a catch-up to conventional DRAM

Raise 2026E/2027E/2028E HBM TAM to US$56bn/US$116bn/US$168bn

Cowen TMT memory/storage takeaways:

"DRAM/NAND is becoming a big percentage of CapEx (went from 10-15% to +40%). This requires a meaningful shift in how hyperscalers operate given that they have used to quarterly pricing negotiations."

" $STX and $WDC both indicated that NAND pricing increase should not be a derivative for HDD pricing, and investors are clearly most enthusiastic about the pricing opportunity for HDDs"

"For $SNDK, management highlighted the unique structure of the LTAs it already signed. The floor gross margin is higher than what our checks for DRAM suggest (80% for SNDK vs our checks for 60% in DRAM, here)."

"SNDK already locked in 30% of its capacity next year under LTAs and the goal is to potentially increase that to 80% over time. With this level of margin structure, durability matters more than continued price increases."

Rosenblatt InP lasers checks:

According to our checks, NVIDIA, which is the driving force behind scale up CPO, asked the supply chain to increase InP laser capacity by ~20x from 2025-2030. The vendors appear to have taken a more conservative stance, agreeing to an ~12x increase ( $AAOI / $LITE etc)

Early $MRVL comments:

Cowen: Custom XPU would need to grow >2x to $7B to reach Marvell's $10B Analyst Day target.

JPM: believe Marvell’s Trainium 4 ramp (2nm) has secured additional content wins for CPO, NVLink I/O chiplets, and UALink switching chip (splitting the opportunity with $ALAB) and has commenced design activities on Microsoft’s next gen 2nm Maia program.

MS: we likely need to see continued estimate revisions, additional evidence of sustained networking share/content gains, or increasing confidence around large custom ramps to become more constructive from current levels.

Cantor: What mgmt did not discuss in detail was the Google XPU-Attach biz, so some may be disappointed here

Goldman Sachs: We believe investor expectations were elevated heading into the quarter based on peers' reports, and robust spending at key customers. From here, we believe stock performance is likely to hinge on the magnitude of Marvell's custom compute ramp in 2H and upside to its overall Datacenter business.

Wells Fargo: Bus Tour this week.

$QCOM: Digitimes reporting:

"Qualcomm has "more than one" ASIC project customer."

"It is understood that another of the four major US cloud service providers (CSPs) is currently collaborating with Qualcomm on a project."

https://t.co/eTrfmghRFr

$MU / $SNDK Mizuho pounding table, again:

DRAM demand still expected to outpace supply into 2027E, with HBM trade ratios and limited capacity adds.

We see NAND following DRAM with tightening supply in 2027E as AI demand for high-bandwidth memory capacity continues to increase with KV Cache/Prefill/Decode.

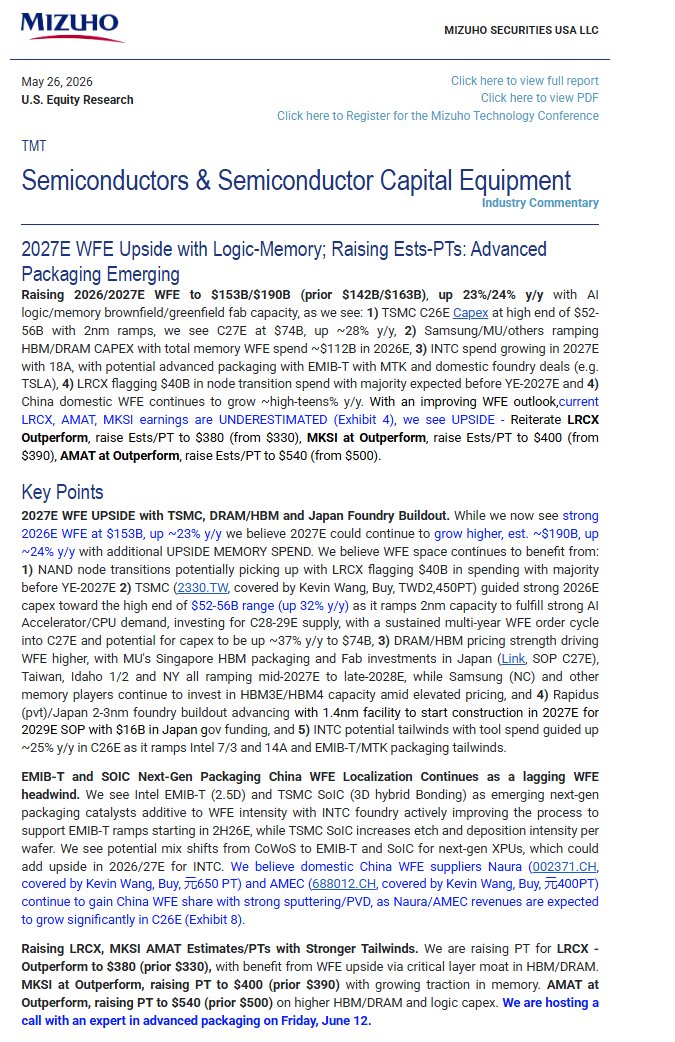

Mizuho on $INTC / $TSM & WFE:

We see potential mix shifts from CoWoS to EMIB-T and SoIC for next-gen XPUs, which could add upside in 2026/27E for INTC.

With an improving WFE outlook, current $LRCX, $AMAT, $MKSI earnings are UNDERESTIMATED

Barclay's upgrade $SNDK & revising $MU higher:

SNDK: We think this type of contract fundamentally changes the way memory players can decide and allocate business, making their environment much more secure and protected on the downside

MU: We are of the opinion that as MU signs more of these SCAs they will provide similar information to SNDK, giving details on the financial hooks and potential prepayment structures they are contracting. When these details come to light, we see it as a positive catalyst and another step forward in the sustainability of this memory cycle.