🇨🇴 Colombia: Abelardo de la Espriella declared the winner.

🇵🇪 Peru: Keiko Fujimori is all but elected, the count is essentially settled.

Two more wins for the right in June.

But this isn't only about ideology. I see a broader pattern that's been taking shape for months.

🇻🇪 Venezuela: direct capture of Maduro and reassertion of control over oil flows.

🇨🇺 Cuba: intense economic and military pressure — energy blockade, explicit threats, and US naval presence off the coast.

🇲🇽 Mexico: mounting pressure on the cartels, with major leadership losses and visible signs of internal shifts and adaptation.

🇧🇷 Brazil: Lula under growing strain, the biggest strategic stake in the region.

What actually interests me isn't just the electoral results. It's what's happening underneath: the transformation of institutions, administrative chokepoints, and economic circuits.

Back in January, I was already laying the groundwork for this reading:

"The Empire no longer seeks to influence. It seeks to own."

I'll be putting out a regular state of play, country by country, a deep dive on each one to map where things actually stand.

Every comment, every counterpoint helps sharpen the reading. Tell me where I'm wrong.

The January article is pinned on my profile if you want the full version.

In conclusion: when a reserve currency depreciates, markets eventually reject paper promises and demand tangible value.

The physical gold shortage doesn’t block the transition — it simply accelerates the digitization of real assets (RWA + Bitcoin as scarce liquidity).

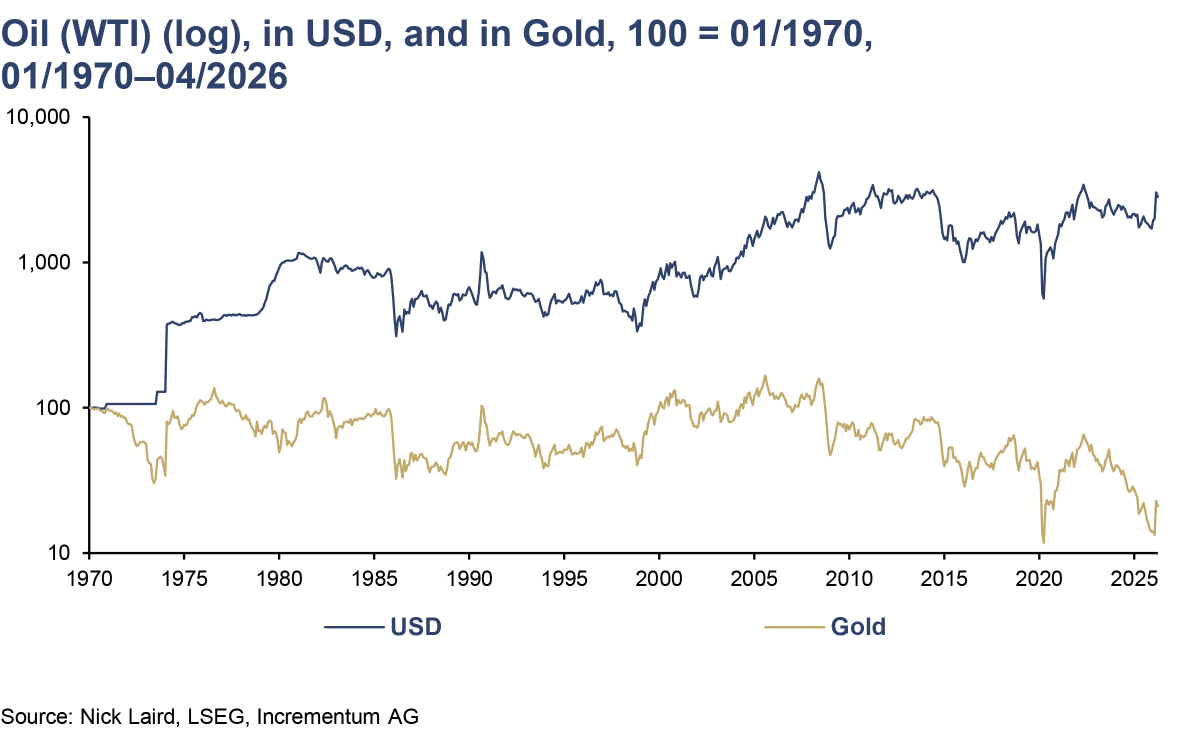

To put the original chart into 2026 context: the current Gold/Oil ratio stands at ~61 barrels per ounce (Gold ~$4,187, WTI ~$69), compared to a long-term historical average of 15-20 since 1970.

This forward-looking analysis is open.

What flaws or counter-arguments do you see in this hybrid transition scenario?

Genuinely interested in your thoughts 👇

In that scenario, real-world players (miners, exporters, industrial states) would eventually push back. To protect margins, they would demand payment in something other than a depreciating dollar.

The immediate dilemma:

Physical gold? Available global stocks are far too limited to support daily commerce.

Paper gold (futures)? Estimates suggest dozens of times more paper gold circulates than physical gold actually held in vaults. The market would no longer accept promises on quantities that don't physically exist.

Without enough physical gold and with a demonetized dollar, what options remain?

3. The general public and savers

This is the adjustment variable.

Classic savings are being eroded by inflation. In response to instability, central banks will roll out CBDCs.

Presented as stabilization tools, they will mainly introduce programmable money (with expiry dates and usage controls), structurally redefining the very concept of private savings.

Beyond the historical chart, this raises a very current issue.

Faced with the wall of public debt and liquidity pressures, many analysts expect the Fed to have little choice but to restart large-scale Quantitative Easing to prevent a breakdown in the bond market.

Whether gradual or abrupt, this internal Fed shock would accelerate dollar devaluation.

From there, a tipping point emerges: what happens when the real economy starts rejecting the dollar?

Long-term market analysis sometimes reveals uncomfortable truths.

When priced in gold, WTI oil has lost roughly 80% of its value since 1971.

For a gold mining company, selling production in dollars and then paying energy costs (which represent 25-30% of operating expenses) has meant a slow but steady destruction of purchasing power over 55 years.

This chart illustrates a mathematical reality: the systematic depreciation of fiat currencies against hard assets. 👇

Priced in gold, oil has lost roughly 80% of its value since 1971.

Energy runs 25% to 30% of a gold miner's cash costs: diesel, power, processing. A producer who sells gold and banks the proceeds in dollars is betting those dollars buy the same energy next quarter.

Since 1971, that has consistently been a losing bet.

The Artemis chart shows the whole money pyramid resting on a $30.9T base of T-bills.

In 2001 Argentina, the system didn’t break because of a technical violation of the peg. It broke when confidence collapsed and capital fled, exposing that far more dollar claims had been created than there were actual dollars to back them.

Inside today’s dollar system, what kind of shock could create a comparable loss of confidence? A major geopolitical event that undermines trust in the U.S. ability to uphold the current order?

And if the response is another round of heavy money printing, where would capital flee to this time, in a world where alternatives remain limited?

@Degenerate_DeFi What kind of metamorphosis do you actually see happening here? Is there a real risk of an Argentina 2001 style collapse for the dollar pyramid, or are we looking at something completely different?

@Degenerate_DeFi Velocity of money on steroids.

Where do you think the breaking point is? Is it the crazy speed of the system or the sheer size of the money-printing pool?

@1914ad The ultimate dilemma of Bitcoin-native stocks. Selling BTC goes against their entire thesis, but doing nothing leads to this chart. Is MicroStrategy bound to follow XXI down this path?

@MarioNawfal Exactly. Australia pioneered this dangerous playbook under the guise of 'protecting kids,' and Europe is rushing down the same path. The road to hell is paved with good intentions

@RaoulGMI Exactly. The structural trend is set. The real question now isn't if debt accelerates, but which sectors, asset classes, or specific categories will absorb the bulk of this debasement first. What’s the consensus looking like?

@AndreasSteno France has the same problem, in some ways worse. The CDI (France’s standard permanent contract) makes firing for cause so hard to make stick that companies just don’t bother, they tolerate zero output instead of fighting a system stacked against them.

This isn’t a finished argument. It’s a lens I want to check against real data. What’s still missing to make this clearer — especially solid numbers on how much of Argentina’s stablecoin use comes from households versus companies?

The question I’m trying to test: Can US financial backing today, and maybe stablecoin infrastructure later, slowly reduce the monetary power of the old Argentine elite without needing to destroy the institutions outright? And does Venezuela show what happens when that softer route isn’t on the table?

When a local elite has lost almost all legitimacy, people sometimes end up preferring to deal with an outside power rather than keep the one they hate. Is that dynamic playing out in Argentina through monetary tools instead of tanks and sanctions?

The broader approach was spelled out clearly. Treasury Secretary Bessent said in October 2025:

"We want to set the tone in Latin America. I would rather extend a swap line than be shooting at the boats carrying drugs, as we're having to, coming out of Venezuela."

One country gets the financial tool. The other gets the harder treatment.

🇻🇪 In Venezuela we’ve seen the harder version play out — military moves against Maduro and an "oil quarantine." 🇦🇷 In Argentina it’s the financial version: swap lines, direct peso purchases, and support linked to elections. Different methods, same goal of shaping outcomes in the region.