A month ago I posted this. The replies were a genre of their own: "topline shrinking," "bottomline shrinking," "game over," "priced to perfection, want to give someone an exit?"

All of it anchored on one reported year. Reported PAT is a lagging indicator and it tells you where a business was, not where it's headed. This thread was about where it's headed: the B2B oncology supplier angle, what the company is becoming, not what it printed last March.

Meanwhile the pricing backdrop flipped. Instead of the feared cuts, NPPA revised anti-cancer ceiling prices upward in June.

The overhang on onco lifted — tailwind, not headwind. 📈

Mcap then: ~₹1,500 Cr. Now: ~₹2,350 Cr. ~56% in a month.

Here's the uncomfortable part. A lot of the pushback wasn't analysis, it was ego. It's easier to type "game over" than to sit with having missed it. The market couldn't care less who sounds smartest in the replies - it pays the people who did the work.

Real skepticism is gold. Reflex rejection dressed up as skepticism is just cope.

Not a victory lap - price can pull back any day. Just read the concall before you write the obituary.

Stay not out 🏏

Disc: Invested. Not a buy/sell rec. DYOR.

The mourning lasted exactly two sessions. Indices have bounced back hard today

This is why you never make portfolio decisions from the timeline's mood 🏏

And this is why you need to build your own conviction to steer through the middle

You can borrow an idea but can never borrow conviction

Watch out for sector rotation

#MarketAnalysis

#Nifty

Bull market corrections are violent. Never forget this. They exist to shake out the faint-hearted 🌪️

Yesterday: a 2% cut on Iran headlines. This morning: microcaps +1.75%, smallcaps +1.25%, Nifty +0.6%.

Watch which names reclaim their highs first. They are telling you where the next leg starts.

#NiftySmallCap250

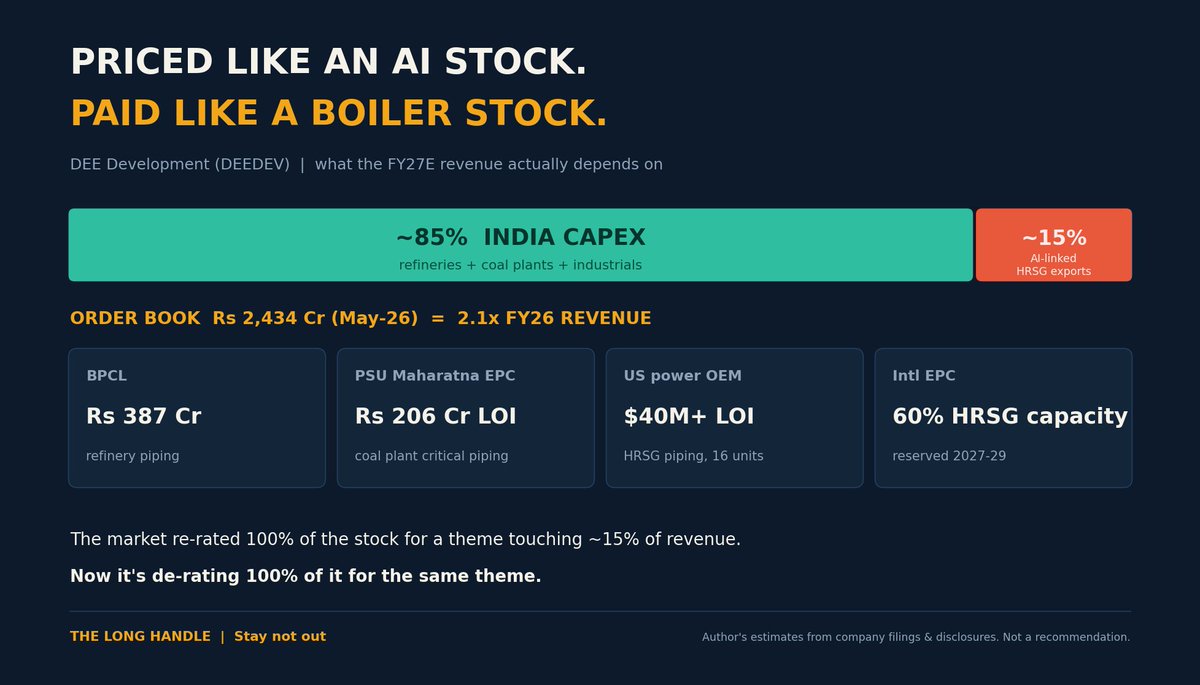

Poor #DEEDEV 😅

Got drafted into the AI trade without ever applying.

Now correcting ~14% from highs because US data centre stocks are bleeding 🩸

Here's what the basket-sellers missed 👇

The ₹2,434 Cr order book (2.1x FY26 revenue) is mostly boring, beautiful India capex:

🛢️ BPCL - ₹387 Cr refinery piping

⚡ PSU Maharatna EPC - ₹206 Cr LOI, coal plant critical piping

⚡ ₹173 Cr more power contracts + ₹58 Cr seamless

The AI-linked bit? HRSG pipe exports - a $40M LOI from a US power OEM + 60% of HRSG capacity reserved by an intl EPC from 2027.

My math: 15% of FY27E revenue.

The other 85%? Indian refineries and coal boilers that don't care what CoreWeave did this week.

The market re-rated 100% of the stock for a theme touching 15% of revenue.

Now it's de-rating 100% of it for the same theme.

What I'm watching instead: monthly order inflows (₹682 Cr in Apr+May vs ₹2,000 Cr FY27 guide) and the Q1 margin print vs 19% guidance.

A Test batsman doesn't become a bad player because the T20 side lost.

Not a reco. I hold a position.

Stay not out 🏏

Nifty Capital Market Index 🙋♂️

It is one of the only holdings which is for the 'long term'

Betting on the casino, not the gamblers 🎰 😅

What's yours, folks?

@Salman_2911 So true. Panic sells are the worst and most often market punishes by coming back up twice as hard. Sector rotations are healthy and get every industry to shine if it’s working hard. As an investor important to acknowledge and invest

#NiftySmallcap250 is barely 1% off its all-time high and the timeline is already in mourning 😅

Let's get one thing straight. A 4-5% correction can happen anytime. Bull market, bear market, doesn't matter.

Sometimes in a single day. We have to embrace this as investors.

What I'm actually watching 👇

Rotation is visible. The AI proxy basket ran hard and money is quietly stepping out 🔄

Not panic. Just profit booking it seems

Where does smart money land?

Look at companies where👇

✅ PEG under 1.5

✅ Earnings compounding 20-25%+ while nominal GDP does 10%

When rotation happens, these are the names that catch the flows 💰

Corrections shake out tourists.

Residents use the dip to churn and upgrade the portfolio 📈

Stay the course. Keep hunting.

Stay not out 🏏

Not a buy/sell rec. DYOR.

#MarketAnalysis

#Nifty

#WhatDoYouSee | Gravita India

Why would anyone pay ₹560cr for a plant running at 1/3rd capacity?

Because the old owner was in exit mode; and the buyer recycles metal for a living.

FY27 target: 18k tons. Capacity doubling 30k → 60k MTPA.

EBITDA/ton bridge of ₹45k → ₹65k as own scrap replaces bought cathode.

Plus ₹100cr on electrolysis for Grade 2 scrap - the step rivals skip.

Stay not out 🏏

Not a buy/sell rec. DYOR.

Peter Lynch ran Fidelity's Magellan Fund from 1977 to 1990.

29% CAGR for 13 straight years 📈 ₹1 lakh would've become ₹27 lakh+. One of the greatest runs in fund management history.

Now guess what the average investor in his fund made?

They LOST money. Per Fidelity's own oft-quoted study 🤯

Same fund. Same manager. Same 13 years.

How? Magellan lost money in 17% of all 12-month windows during his run. Every dip shook someone out.

Investors piled in after great years, panicked out in drawdowns 📉

Lynch did the compounding. Investors did the churning.

You yourself are your biggest enemy. Nobody bowled these investors out - they hit their own wickets

Stay not out 🏏

#KnowledgeHandle

6/ Here's where it gets interesting: write-backs. 💡

When a provided loan recovers, that provision reverses and flows BACK into profit.

FY25: ₹425 cr impairment cost.

FY26: ₹237 cr net REVERSAL.

₹270 cr recovered in FY26. Management guides ₹250-300 cr more in each of FY27 and FY28.

Private Markets PAT went ₹151 cr → ₹543 cr. That's 3.6x in one year.

4/ Then the cycle turned. IL&FS blew up in 2018, Covid followed, and restructured accounts kept slipping.

Provisions (money set aside expecting loans to go bad) peaked in FY24. RBI even barred their IPO financing arm for a few months in 2024.

The stock went nowhere for 4 years while the IB kept winning deals. 😮💨

3/ The original sin: wholesale lending. 🏗️

Unlike home loans (small tickets, thousands of borrowers), wholesale means a handful of massive loans to real estate developers and promoters. One default and the P&L bleeds.

And bleed it did.

The book peaked at ₹10,215 cr in FY24 - the same year impairments hit ₹641 cr and the segment posted a LOSS. Even FY25 ROE: just 1.7%. 🩸

2/ The company: JM Financial. A 53-year-old franchise and India's #1 investment bank in IPOs for FY26. 🏆

Quick jargon check: an investment bank is the middleman that helps companies raise money (IPOs, QIPs, M&A) and charges a fee.

No capital stuck, high ROE.

This was always JM's crown jewel.

So how did they end up in trouble?

1/ Imagine deploying 60% of your capital in a business earning 5% ROE.

For years, that was this company's reality. Wholesale lending quietly bled a franchise that was elite at everything else.

Then it dawned on them. The book had to go: ₹10,000 cr → ₹4,000 cr in 2 years. The non-core part is nearly ZERO now. 📉

Today the stock trades at ~1.1x book, with India's #1 IPO banker sitting inside it.

Mispricing or another value trap?

Let's decode the business 🧵👇

Weekly chart of Spandana Sphoorty, what do you

see 👀?

Looks like microfinance is turning. Much better players there apart from Spandana, but this could be a high risk high reward trade.

Reversals are strong in this market. But SL is a must.

Disc: Only for educational purposes. This is not investment advice.

#WhatDoYouSee

#Nuvama 🚀

1,600 then, 1,925 now.

Hard to believe this stock was available at a PE of ~20 in the middle of the March collapse triggered by the Iran-US war.

And look at it now - blue skies

Mentioned several times before: this remains the cheapest wealth management stock around, with one caveat - the promoter overhang.

Earnings are real. India's capital markets story is just getting started.

Invested. Not a recommendation.

15/ Here's the lever almost nobody's modelling. 🔓

₹702cr of EBITDA becomes only ~₹180cr of owner profit today.

But three handbrakes release in FY27:

Goodwill amortization drops ₹100cr → ₹35cr.

Finance cost keeps falling (0.2x net debt).

Tax normalizes to ~27% off an inflated quarter.

Profit can compound faster than revenue - with zero new products. 🚀

12/ Credit where it's due: the CEO refuses to hype the rocket. 🎯

On the glamorous new-molecule work, he said plainly:

"It's easy to say CDMO can work with innovators but I don't want to go into that."

Rare honesty on a results call.

So today's "CDMO" is the humble, dependable mechanic - not the moonshot. Value it as the former. 🔧