Wow, the S&P Dow Jones Indices has just officially announced that they will NOT be changing their inclusion rules to make it easier for “MegaCap” companies (such as @SpaceX) to be fast-tracked into the S&P 500.

Their reasoning:

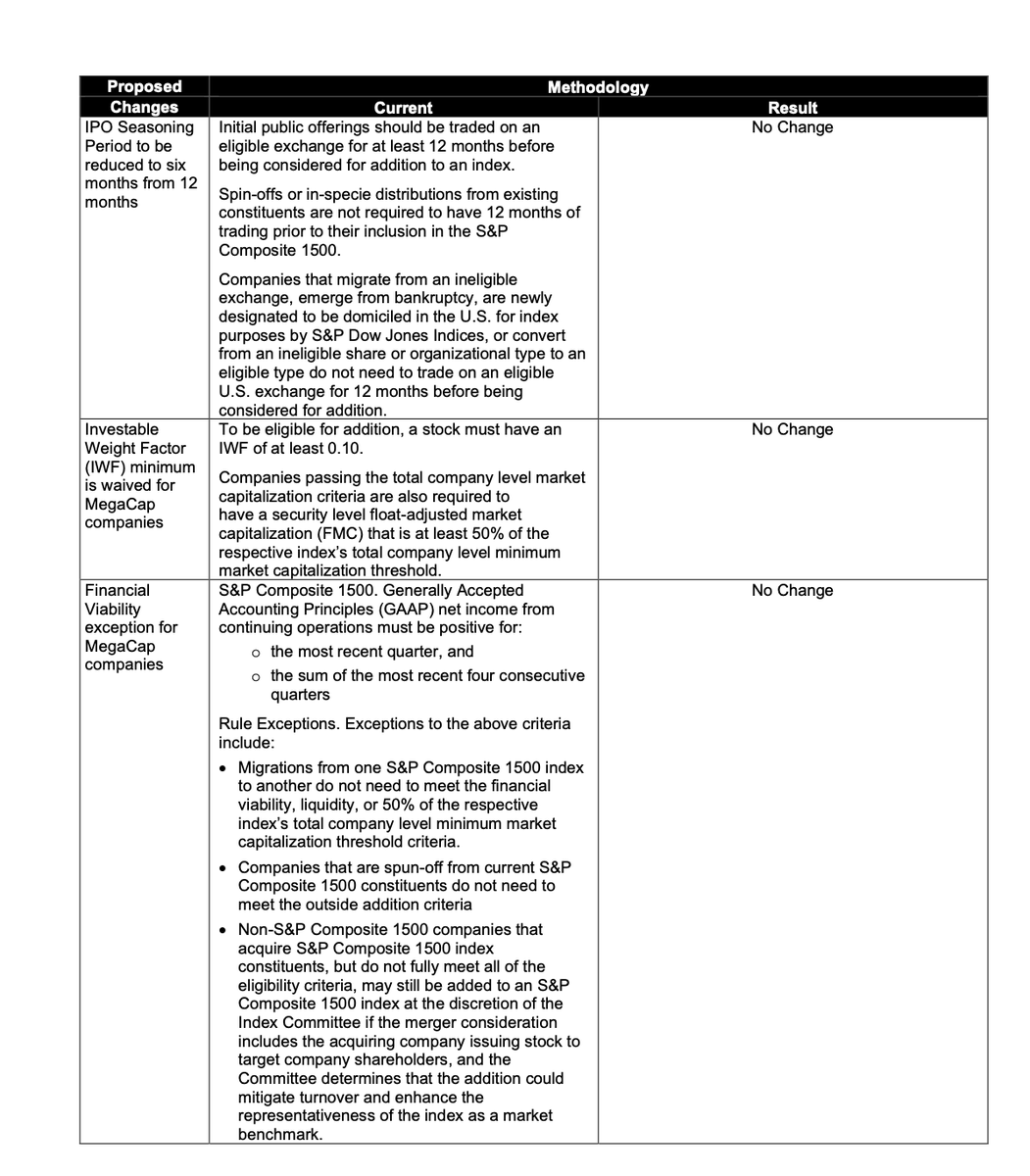

"S&P DJI determined that exceptions to the financial viability, seasoning, and IWF requirements should not be granted solely based on market capitalization. The decision not to adopt the proposed exceptions preserves core index principles by maintaining consistent application of these key requirements. Although there may be trade-offs between strict adherence to these eligibility requirements and broad representativeness, the current methodology provides substantial market coverage and sector balance. As a result, the indices can continue to meet their stated objectives while preserving their role as representative and investable benchmarks for the U.S. equity market.

No changes will be made to the eligibility criteria including financial viability screens, seasoning period, or minimum IWF, for the S&P 500, S&P MidCap 400, or S&P SmallCap 600 as a result of the S&P Dow Jones Indices consultation on the treatment of MegaCap companies. Accordingly, there will be no changes to existing methodology for this index family."

This means that the earliest @SpaceX could be eligible to be added to the S&P 500 would now be June 2027.

The requirements that will now remain in place are:

• No changes to S&P 500 eligibility rules for mega-cap companies.

• Mega-cap companies will still need to wait 12 months after their IPO before being considered for S&P 500 inclusion.

• S&P will not waive profitability requirements for mega-cap companies. The company must have positive GAAP net income in the most recent quarter, and the sum of the most recent four consecutive quarters.

• S&P will not waive minimum public float requirements for mega-cap companies. At least 10% of a company's shares must be publicly tradable ("free float").

The S&P rejected proposals that would have:

• Reduced the IPO seasoning period from 12 months to 6 months

• Waived profitability requirements

• Waived minimum public float requirements

Investor Gavin Baker on why the AI bubble might not happen and why a handful of people in their 70s are the reason:

Baker opens with a blunt warning about what's at stake:

"The last thing anyone should want is a bubble. Bubbles are terrible. They're awful. They're terrible to invest through. The aftermath of them is even worse."

The problem, he explains, is that bubbles tend to come with the territory whenever something genuinely new arrives:

"The entire history of financial markets suggests whenever you have a profound new technology, whether it's AI, whether it's the internet, whether it's the PC, whether it's railroads, whether it's canals, you almost always get a bubble because markets are efficient. Investors understandably become excited about this new technology."

He borrows a phrase from Michael Mauboussin to describe the moment everyone starts believing the same thing:

"There's a breakdown in diversity. Everyone comes to believe in this. You get a bubble and then that bubble funds the buildout that the new technology required. And that's exactly what happened with the internet."

But this time, @GavinSBaker thinks it could play out differently:

"I am optimistic that we may avoid a bubble this time. Smoother for longer is what we all want."

The reason isn't investor discipline. It's physics. Baker points to two fundamental shortages: watts and wafers.

The watt shortage, he believes, will get solved: "We're going to address the watt shortages with orbital compute for sure in the next 5 to seven years."

The wafer shortage is different. That one, he argues, is going to last and the reason comes down to the people running Taiwan Semi:

"The wafer shortage I think is going to persist for a long time… Taiwan Semi is run by flinty old men and women in their 70s… they're the most important people in Taiwan. The president of Taiwan [is] irrelevant. They are Taiwan and they view themselves as the guardians of Morris Chang's legacy."

To show how seriously they take that legacy, Baker tells a story from a visit more than two decades ago:

"I remember going to Science Park in Taiwan more than 20 years ago… asking did they think they could ever catch Intel? And they said, 'It's a beautiful dream, but it's probably for our grandchildren.' And they did it in one lifetime."

That sense of custodianship, he explains, makes them deeply cautious about expanding. Because a boom-and-bust cycle would be a disaster for the company they're protecting. Even Nvidia can't move them:

"Jensen goes there every 3 months and maybe they expand 5%. He wants them to double or triple. And if they doubled or tripled the capacity, Nvidia could probably sell $1.5 to $2 trillion worth of chips next year. I really believe that. But the other side of that might be very painful for everyone."

Baker's conclusion is almost counterintuitive: the very people refusing to chase the boom may be the ones who prevent it from becoming a bust.

"These flinty old men and women who are safeguarding Morris Chang's legacy are helping us all avoid a bubble by enforcing a real-world physical constraint that simply has not been present in past precedent technologies."

The AI capex spend is so insane that Google is raising equity from Berkshire Hathaway through a private placement to fund spend on infrastructure

Berkshire is receiving $10B split across Class A and C shares at a roughly 6% discount to share price