Fusion is the Power of the Cosmos and Solar Power is its prime derivative with wind a 2nd or 3rd derivative energy source from our Sun

But just how much Land Would It Require To Get Most Of Our Electricity From Wind & Solar?

Not much at all ! https://t.co/uzC4jyqXn2

We just launched our US Electricity Index.

- Analyze regional pricing differences.

- Monitor changes in energy costs over time.

- Compare household & business electricity expenses.

- Trends in the U.S. electricity market.

Lights on ⚡️👇

Micron will be a $3,000 stock and here is exactly why (Save this).

For 25 years, the price of memory only went one direction, down.

From 1957 to 2020, the cost of a gigabyte of DRAM dropped by a factor of ten every five years, a straight, unbroken line driven by Moore's Law and chronic oversupply.

Starting in 2025, that line reversed for the first time in history not because of a supply shock, but because AI created a structural demand surge the memory market had never experienced before.

The supply constraint has a hard clock attached to it.

From the moment AI demand inflects to the moment qualified memory output is actually available, you are looking at a minimum of 7 to 8 quarters, nearly two full years of lag.

The pipeline runs from demand inflecting, to Big Tech locking in long term agreements, to EUV fab orders being placed, to tools shipping and customers qualifying, to qualified HBM and DRAM finally coming out the other end.

That means the demand wave that hit in 2024 and 2025 will not see meaningful supply relief until late 2026 at the earliest, and Goldman Sachs models DRAM undersupply persisting through 2027 to 2028.

The demand numbers explain the magnitude.

A full AI system uses approximately 65 times more HBM than its predecessor, and servers are projected to account for 59% of all DRAM demand by 2028 up from 37% in 2023.

Every data center built as part of the $1.1 trillion capex cycle multiplies that demand further, and HBM production consumes so much wafer capacity that it has created a secondary shortage in general purpose DRAM as a direct side effect.

The pricing confirms it.

DRAM contract prices rose roughly 62% in 2026, server DRAM margins at Samsung and SK Hynix crossed 80%, and hyperscalers have shifted from buying memory opportunistically to signing 3 to 5 year long-term agreements just to guarantee supply exists.

The question is no longer about price but whether you can secure supply at all.

Micron is one of only three companies on earth that can produce HBM at scale, and it has sold out its entire 2026 HBM allocation before it comes off the line.

Full-year HBM revenue estimates for Micron sit at $13.2 billion, the HBM market is growing at 41% annually and projected to reach $100 billion by 2028,

And chipflation is now spreading from data centers into smartphones and consumer electronics meaning this price cycle has consequences far beyond AI infrastructure.

Memory is no longer a commodity but rather the scarce resource the entire AI economy cannot function without and Micron owns one of three keys to unlock it.

Come join Milk Road Pro for our full breakdown, the complete picture of the AI memory supercycle and our entire AI thesis.

Link below!

THE MEMORY SECTOR WILL BE TESTED NEXT WEEK.

$MU reports earnings on June 24.

If Micron can confirm AI demand remains strong.

The entire memory trade could see another leg higher.

$SNDK $WDC $STX will be the main watch with

Secondaries and laggards possible best runners.

MEMORY INFRASTRUCTURE

$RMBS $SIMO $MRVL $AVGO

MEMORY EQUIPMENT

$AMAT $LRCX $KLAC $ONTO

EMERGING MEMORY

$MRAM $GSIT $NVEC

Two extreme views dominate the DTC discussion for $ASTS:

Either “literally no one will use it”

or “everyone will use it and service will be crappy”.

So, I decided to actually model the **** out of this question.

I built a bottom-up model for the Continental US market combining

population density data (LandScan)

dynamic leisure population redistribution (OIS, NHSA)

FCC coverage (4G LTE)

Monte Carlo simulations across 2,000 satellite beams

in order to estimate real-world Block 2 satellite load.

Result on a busy weekend: One satellite can comfortably serve 8,000 concurrently active users which covers 90 % of simulated scenarios.

TL;DR

Again, Abel has thought of everything. Block 2 is well-positioned to capture the early market opportunity.

Full write-up with lots of pictures → https://t.co/0FqHhgF74O

#ASTS

Big things are happening in the satellite-to-cellular space! If you are following the tech behind space-based 5G, a recent research paper from the Fraunhofer Institute drops a massive validation blueprint for the industry. Let's dive in.

$ASTS

🐟🐈⬛

1/

$ASTS 🚀 New PhD-level DTC models just dropped — don’t miss these.

#1 Global TAM

Austrian Economics-inspired model puts the global Total Addressable Market for Direct-to-Cell satellite at ~$50B, nicely diversified across regions.

Full breakdown: https://t.co/UcWKkvfzIL

#2 Real-World Block 2 Load

Bottom-up Monte Carlo model (LandScan density + dynamic population + FCC coverage + 2,000 beams) shows:

One Block 2 satellite comfortably handles 8,000 concurrent users on a busy weekend — covering 90% of scenarios.

Abel thought of everything. Block 2 is perfectly positioned for early market dominance.

Full write-up with charts: https://t.co/MYtUllmnt2

This changes how we think about $ASTS scalability.

#ASTS #SpaceMobile #DirectToCell

🚨🚨🚨This is HUGE. BB8-10 successfully in orbit. This de-risks the entire 2026-2027 thesis in ways most people don't realize. Let me break down what actually gets unlocked.

First, what these specifically are. Three 6-ton Block 2 satellites, each a 2,400 sq ft phased array - the largest commercial arrays ever sent to LEO, built from modular "microns." With the AST5000 ASIC: 10 GHz processing, nearly double the Block 1 speeds.

Here's what is de-risked:

Manufacturing line validated. ASTS builds satellites from modular "microns" at its Midland campus. BB8-10 in orbit proves the Block 2 production-to-orbit pipeline works end to end. BB11-33 already in production, arrays done through BB28. This validates the factory, not just the satellite.

BB7 loss neutralized. BB7 was lost on Blue Origin in April - a $155-160M hit. SEC filings confirm a replacement launch is coming under contract terms. BB8-10 succeeding proves the deployment machine survives a failure and keeps moving.

Path to the 25-satellite beta threshold. ASTS needs ~25 satellites (5 Block 1 + 20 Block 2) for non-continuous service - enough for operators to run trials. BB8-10 moves the count toward it. AT&T + FirstNet beta was guided for 1H 2026. These birds are part of getting there.

Three revenue streams it touches:

1) Government: dual-use capability runs on these Block 2 birds. $73M+ in disclosed defense contracts (HALO $30M + SDA $43M) plus the uncapped MDA SHIELD IDIQ. I model atleast $500M government revenue by 2027.

2) Gateway/service prep: each market activation needs ground integration - ASTS listed 17 countries, 2.9B people, already in progress. More satellites = more activation = more recognized revenue.

3) Beta/commercial: the on-ramp to the AT&T/FirstNet beta and eventual continuous service at 45-60 satellites.

Spectrum optionality rides on this hardware. The 8-K confirms 1,150 MHz of tunable low/mid-band MNO spectrum, 45 MHz MSS, 60 MHz S-band priority rights. Block 2's digital beamforming tunes across all of it. The spectrum is worthless without satellites in orbit to use it. Every launch activates more of that spectrum position.

What this is NOT: continuous nationwide coverage. That needs 45-60 satellites. Anyone claiming instant US coverage is wrong.

What this IS: proof the factory works, the Block 2 design works, the deployment survives setbacks, and the path to beta service and the defense revenue ramp is real and moving.

The market prices launch risk. Tonight removes a big chunk of it. Then every subsequent launch compounds - satellites, spectrum, defense, beta, all on the same hardware.

Built from microns in Texas. Largest arrays in LEO.

We are just getting started!

$ASTS 🛰️

Successful launch!🚀🚀🚀🚀🚀🚀🚀🚀🚀🚀

All satellites were captured within minutes and already orbiting Earth with all systems nominal.

Congratulations to the incredible AST SpaceMobile team! 250Y U.S.A. 🌎📶 🤠

1/ We have been training RNNs wrong for decades.

Backpropagation through time (BPTT) forces sequential updates, creating unstable O(T) gradient paths.

What if we could train highly expressive, non-linear RNNs with flat, parallelized O(1) gradients?

It is now possible. 🧵

Within our body, different cell types exhibit a varying pace of aging. Discovery of how that can be tracked by cellular proteomics, from a tube of blood, and what that means for health outcomes, For example, the clock of brain astrocytes and development of Alzheimer's disease. @NatureMedicine@wysscoray

This takes organ clocks to the next level!

https://t.co/7k296L8tGw

What Lisa Su actually held on stage:

A mini PC the size of a lunchbox running Qwen3-235B locally, with no cloud and no discrete GPU

Inside: the Ryzen AI Max+ 395, 128GB unified memory, 110GB usable as VRAM on Linux

The first x86 chip that handles 200+ billion parameters on a single die

AMD claims it beats the RTX 5080 by several times on memory-bound models — because the 5080 simply cannot fit them

$1,400 to $2,500 once. cloud bills run $200 to $400 a month

It pays for itself in a few months, then costs nothing per request

This is not a faster GPU. it is the first real argument that your AI does not belong in someone else's data center

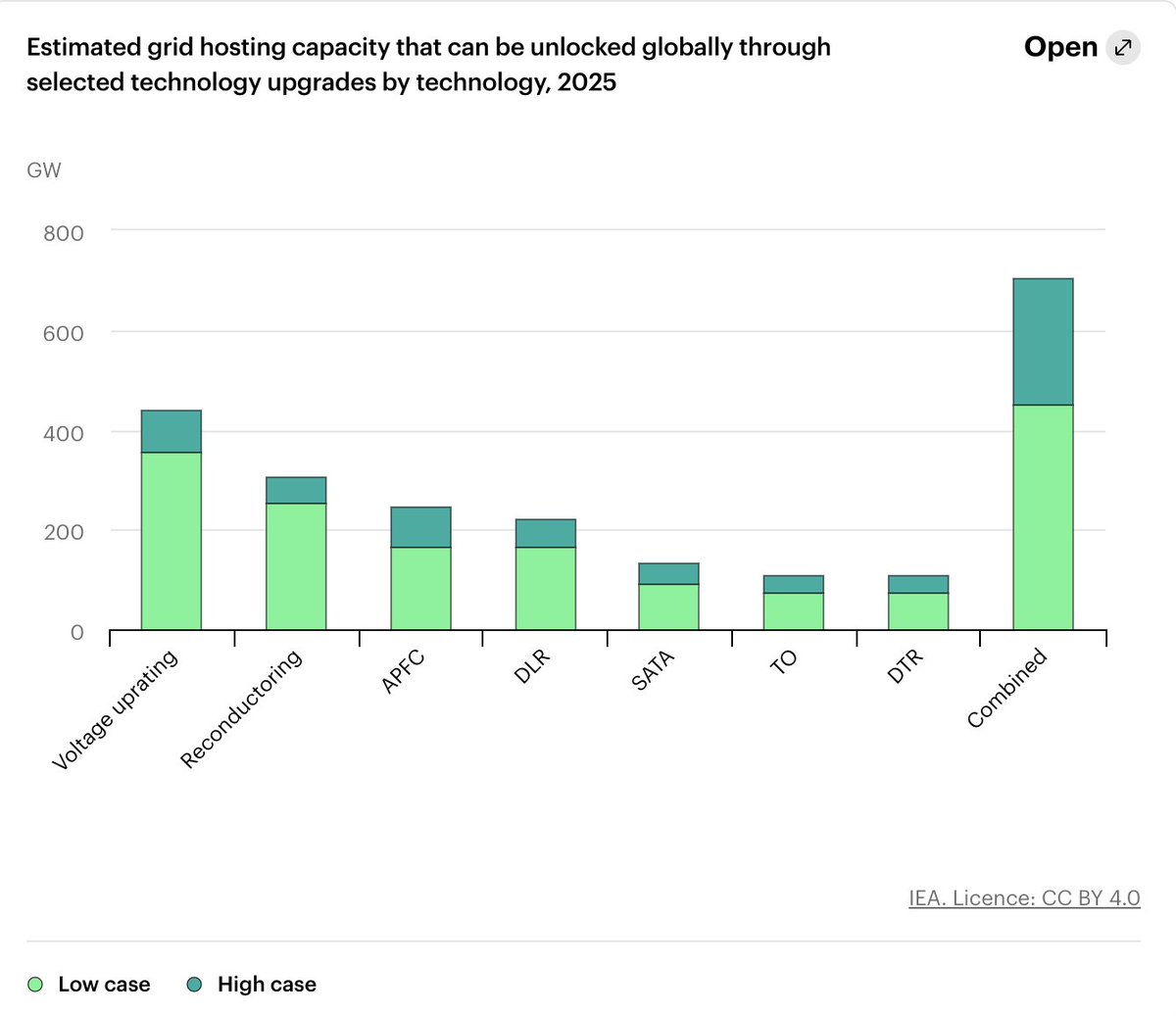

Get used to hearing the following term — Grid Enhancing Technologies (GETs)

Using GETs we can unlock up to ~750GW of added power capacity globally

The grid has more capacity potential, we need to unlock it with new approaches

ARK INVEST JUST SAID STARLINK IS ABOUT TO COMPETE DIRECTLY WITH EVERY MAJOR CELL CARRIER

And @wintonARK thinks SpaceX $SPCX is going to beat all of the carriers

Here's why:

Connectivity today is completely geographically fragmented. You're a Verizon customer in the US, but the second you move to Europe you're someone else's customer. A business operating in 10 countries has 10 different telecom relationships.

Starlink fixes that.

"That's what Starlink is basically doing, amortizing connectivity across the entire world. That gives them the ability to become a truly global telecom provider, which nobody has been. Nobody can do that today."

The next move: SpaceX launches its own cellular brand. Default satellite, fail over to cellular. Right now it's the reverse.

Today sheet metal fabrication requires custom dies for most cuts.

This required tooling runs that can take months and experts that the US has lost.

NTop built a Class 3 UAV airframe with using zero hard tooling.

It is a massive shift to garage builders and startup companies.

Alex just dropped a fascinating piece.

We've spent years measuring the cost of compute.

Now we're starting to measure the price of intelligence.

If GPU-hours are the oil wells of the AI era, tokens are the barrels. The launch of a token price index may seem niche today, but it could become one of the most important economic signals in AI.

The next phase of this industry won't just be about smarter models.

It'll be about what intelligence is actually worth.

Read Alex's article. 👇