Has the Income-tax Act, 2025 quietly expanded Tax Audit applicability for small businesses? YES!!

Section 58(3) now provides that where an eligible presumptive taxpayer declares profit below 6%/8% and total income exceeds the basic exemption limit, maintenance of books and Tax Audit becomes mandatory.

Under the post-2016 Section 44AD regime, many taxpayers with turnover below ₹1 crore could avoid audit unless the specific 5-year lock-in condition of Section 44AD was triggered.

Take a small shopkeeper with ₹80 lakh turnover and 4% actual profit. Under a literal reading, Tax Audit becomes mandatory despite turnover being below ₹1 crore.

But the bigger impact may be on salaried taxpayers doing F&O trading!

Example:

Salary Income: ₹25 lakh

F&O Turnover: ₹80 lakh

F&O Profit: ₹50,000

Since total income exceeds the basic exemption limit due to salary income and business profit is below presumptive rates, the taxpayer may get pulled into Tax Audit requirements.

Thus, a person earning salary and making a small profit from F&O transactions will now end up facing a Tax Audit merely because of one drafting change in the new law.

#IncomeTaxAct2025 #TaxAudit #44AD #CAProfession

A divorce lawyer who handled 200+ failed marriages told me this:

I asked,

“What patterns do you see?”

He said:

“Men ignore the same red flags every time.”

After watching hundreds of relationships fail, one thing is clear:

Some women must be avoided at all costs, for the sake of your bloodline.

Here are 6 of them:

Here is the Drive link containing complete access to 1,000+ draft templates. The collection includes documents related to Income Tax, Company matters, Composition deeds, Agreements, and various miscellaneous legal drafts.

Drive link 🔗- https://t.co/CqNQWZZRFV

Indian accountants, tax consultants and CAs, if you want to catch the US accounting, tax and finance offshoring wave from India, and start earning over 2 lakh per month, what is your best option?

What credential will get you there very fast - from Indian accounting, tax filing and bookkeeping work to US clients immediately?

There are 2 credentials that help the most - CPA and Enrolled Agent of the IRS. But which one is better for beginners?

CPA vs Enrolled Agent — which one should you do?

Most people ask the wrong question.

The REAL question is:

“What gets me earning from US clients the FASTEST… with the HIGHEST credibility?”

Here is the truth nobody tells you:

CPA is amazing — but it’s slow.

- 120–150 credit hours

- Experience requirement

- 6 exams

- Low pass rates

- 1.5–3 years to finish

- Expensive

If you want the long-term brand, CFO track, audit rights… CPA wins.

But if you want US dollars quickly:

EA (Enrolled Agent) is the highest-ROI first step for anyone outside the US.

Here’s why:

1. EA is fast

3 exams. 66 percent pass rate.

Most people finish in 3–6 months.

2. EA is cheap

A fraction of CPA exam + evaluation + state-board cost.

3. EA can be taken in India

Prometric centres. No travel. No degree requirement.

4. EA gives you “instant credibility” with US firms

It’s an IRS credential. Unlimited practice rights in federal tax.

US CPA firms love offshore EAs because the talent shortage is insane.

5. EA helps you get more than just tax work

This is the part nobody says aloud:

Once a firm trusts you with tax… they ALSO trust you with:

- Bookkeeping

- Catch-ups

- Clean-ups

- Month-end close

- Prep for tax returns

- Client communication

- Workflow support

If you already know US accounting, EA becomes your credibility badge.

It says:

“I understand US rules. I clear US exams. I’m not a random freelancer.”

6. EA → money in 6–12 months.

CPA → money after 1–3 years.

So the real decision framework is simple:

Choose EA if you want speed, income, and credibility NOW.

Choose CPA if you want the biggest long-term brand LATER. I recommend you do EA first and then CPA too.

The smartest offshore accountants do this:

EA first → start earning → get US experience → then decide on CPA.

Stop thinking “CPA OR EA”.

Start thinking:

“What gets me PAID first?”

Share this with accountants and CA/half CA friends - it may just change their lives.

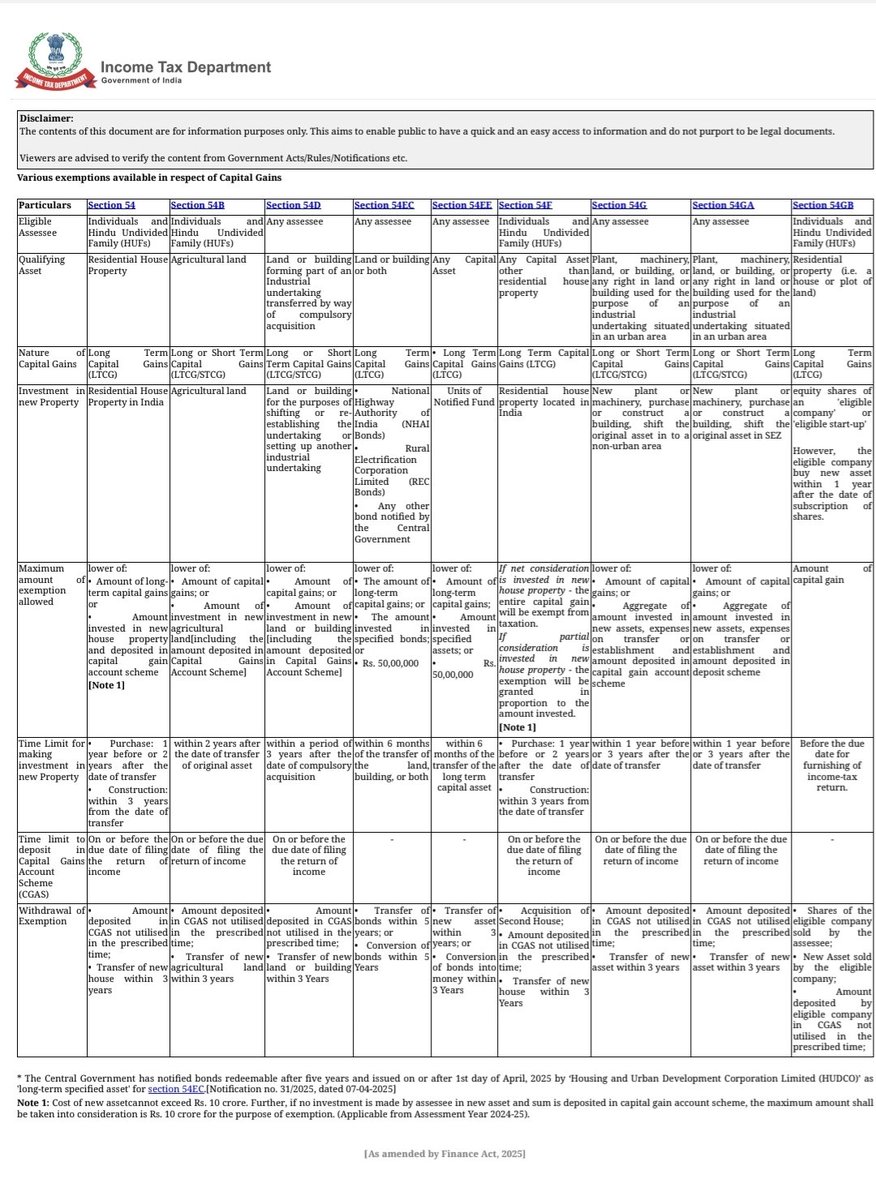

Various exemptions available in respect of Capital Gains with reference to FY 2025-26

Section Covered

Section 54

Section 54B

Section 54D

Section 54EC

Section 54EE

Section 54F

Section 54G

Section 54GA

Section 54GB

Thanks for this Tabular Chart @IncomeTaxIndia

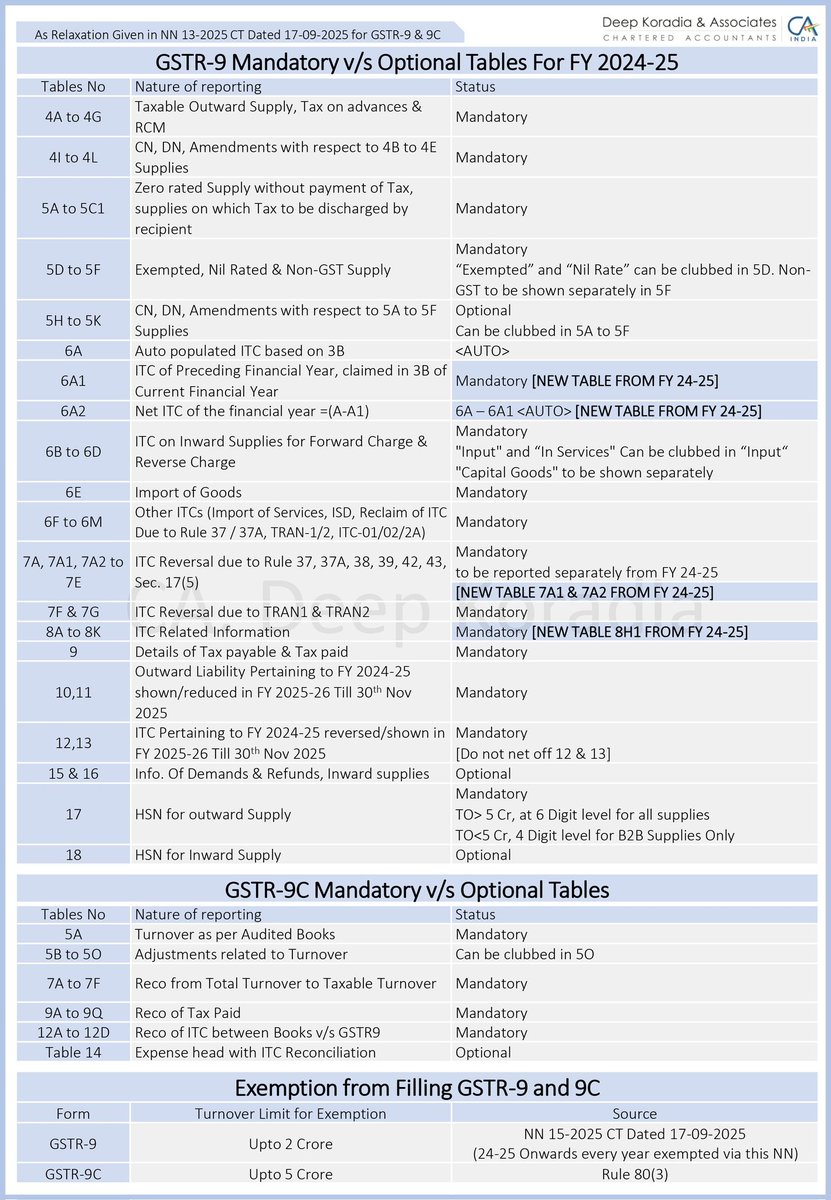

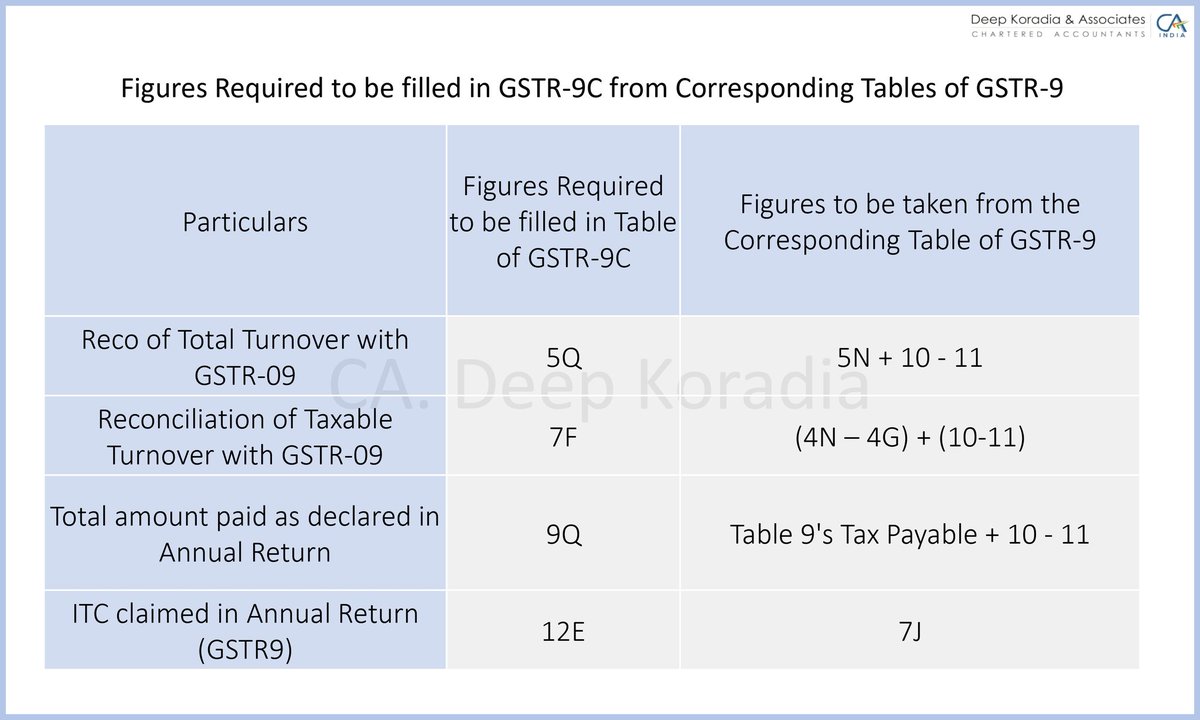

GSTR-9 & GSTR-9C: Mandatory vs Optional Tables for FY 2024-25 (Pic 1)

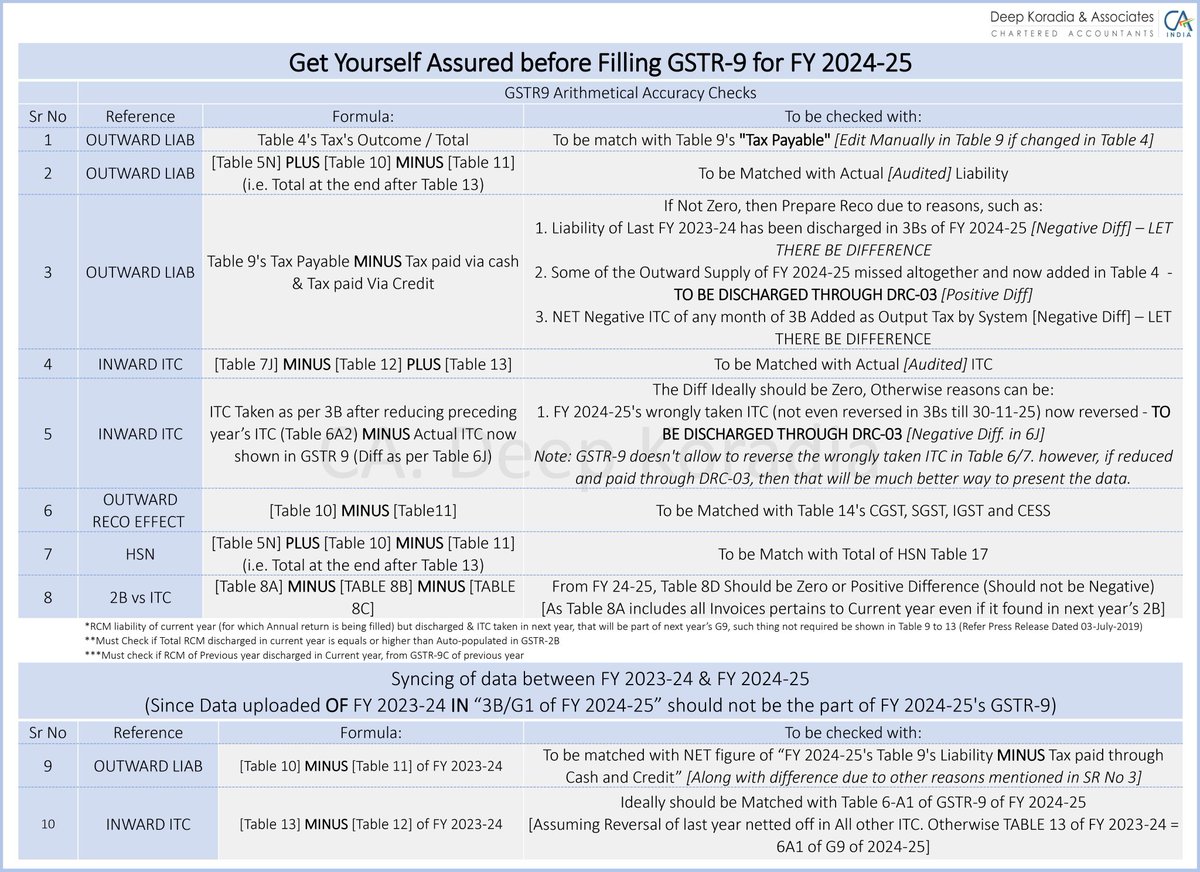

GSTR9 Arithmetical Accuracy Checks (Pic 2)

Linkage between GSTR-09 and 9C

(Figures to be taken from GSTR-09 while filling GSTR-9C to upload error free Json on first Go) (Pic 3)

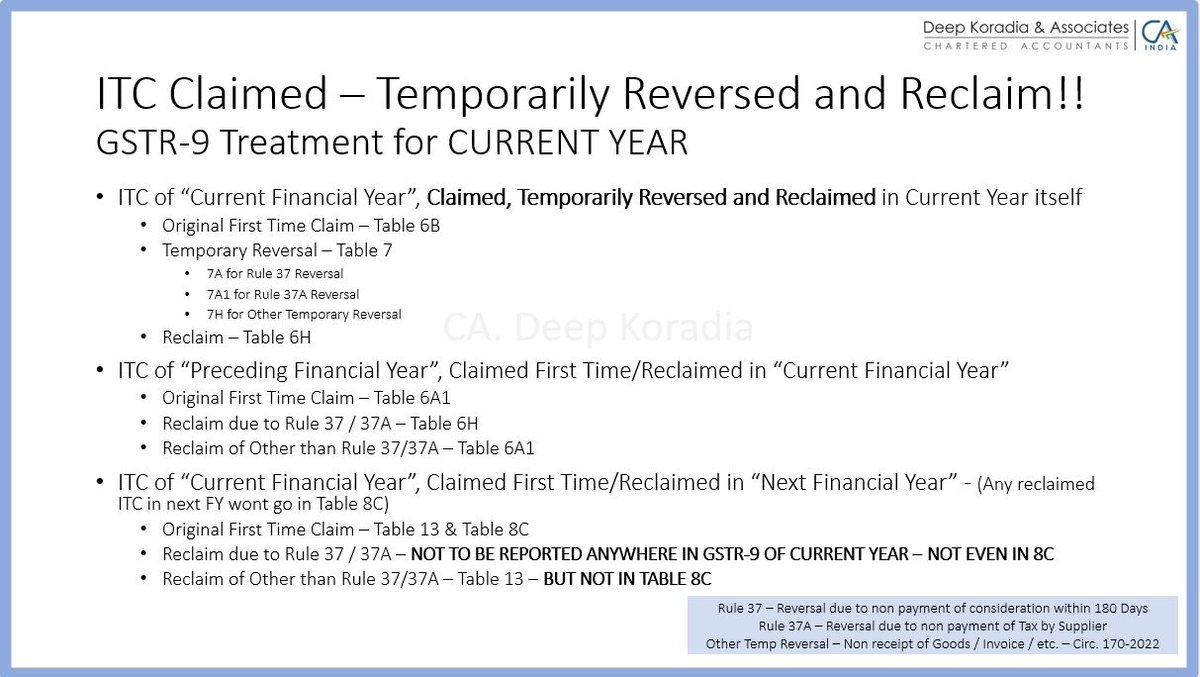

Treatment of ITC Claimed – Temporarily Reversed and Reclaim in GSTR 9 (Pic 4)

All Content Credit to @DEEPKORADIA sir

GSTR-9 Self-Tutorial File Download

Our Team GSTpanacea has prepared a Self-Help file on GSTR-9 covering almost all details of each table and how to handle it.

To download the same, please reply to this tweet/post with:

"GSTR"

Check your DM and follow the steps.

Bonus: Excel File to cross-check.

Note: 1) Post valid for 400 DM's or 24 hours. After that post will be closed. 2) Quote Tweets will not be considered only reply to original tweets will work.

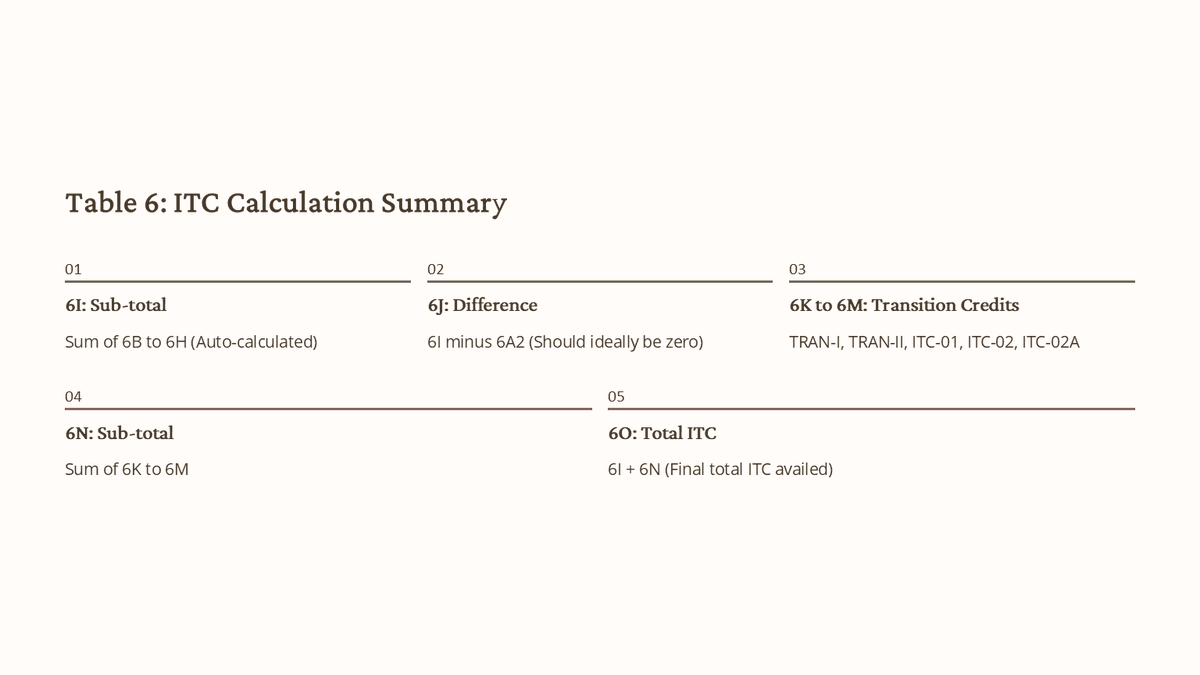

🚨 GSTR-9 Key Changes 🚨

🧾 1. Key Change – New Sub-Table 6A(1)

➡️Earlier, taxpayers struggled to report ITC of the previous FY availed in the current FY GSTR-3B.

➡️They often used “Others” or negative entries → confusion + inconsistency.

✅ To fix this, Sub-Table 6A(1) has been introduced in GSTR-9 for FY 2024–25.

📌 Now you can separately report:

👉 ITC of the preceding FY availed in the current FY (through GSTR-3B filed from April to Oct, up to 30th Nov).

🎯 Objective:

Better clarity & uniformity in ITC reporting.

📊 2. Impact on ITC Reporting

The new structure in Table 6 of GSTR-9 looks like this:

➡️6A(1): ITC of preceding FY availed in current FY

➡️6A(2): Net ITC of current FY (excluding 6A(1))

This bifurcation ensures precise categorization & reduces mismatches.

3. Compliance Tip

Before filing, review your GSTR-3B carefully!

✔️ Segregate ITC correctly between 6A(1) & 6A(2)

✔️ Cross-check FY-wise ITC claims

Doing this = smoother assessments + fewer notices 🚀

@TimesAlgebraIND IIT Bombay is prestigious college, funded with public money. Because of him, people's money gone waste and one caliber person has missed the opportunity.

@TimesAlgebraIND This is not spirituality... hinduism always says to practice spirituality on par with work. It never says, practice spirituality by ditching job.

Late Fee for GST Returns (Pic 1)

E-Invoicing under GST (Pic 2)

Blocked Credit u/s 17(5) (Pic 3)

Waiver of Interest and Penalty for 2017-18 to 2019-20 (Pic 4)

Content Copyright and Credit to @KMSCAFirm@AmishKhandhar@Rashminvaja

Link to Buy "GST Book" and other publications by @KMSCAFirm

https://t.co/HJqkbhKPoT

Procedure and conditions for closure of proceedings under section 128A in respect of demands issued under section 73 as per Rule 164 & Circular No. 238/32/2024-GST.