US and Iran reach a peace deal.

Iran gets:

1. $12B unfrozen immediately and $12B in another 60 days.

2. They are demanding an additional $300B reconstruction fund which US hasn't confirmed.

3. Removal of sanctions on Iranian oil.

4. End to Israeli military operation in Lebanon

5. US removes their naval blockade.

US gets:

1. An open and free Strait of Hormuz

2. A 60-day period to negotiate details of Iran's nuclear program including enrichment levels etc.

Both sides are claiming victory.

@WillBiddy_ No sir, check the numbers again.

180 bps sequential spike in marketing expense. Higher g&a which can be attributed to semrush.

Their capex is <1% of revenue. I am not sure which infrastructure investment are you referring to.

$ADBE claims that they are seeing 40% traffic growth driven by "intent based searches" (summarise pdf, pixelated art).

But their income statement shows something different.

Sales and marketing expenses spiked 180bps in Q2.

Is the freemium pivot really driven by demand?

@gibby_joe52901@realroseceline These actions don't make any sense to do via a prompt box. You can cycle through 8 different fonts to see which one you like through point and click in 20s.

When you want to open a file on your desktop, you don't go ask claude to open it. You just point and click.

All the $ADBE posts on X celebrating the "triple beat quarter" failed to point out that:

- Adobe actually lowered its ARR guidance

- The beat is not nearly as big as the earnings release suggests

Here is the math when you strip out their newly acquired Semrush business:

ARR guidance

10.2% target on $25.66B base = $28.28B.

$28.28B - $480M Semrush ARR = $27.80B organic ARR.

($27.80B / $25.66B) = ~8.3% organic growth vs. 10.2% original guidance in Q4 25

Revenue guidance

$26.55B (new midpoint) - $26.00B (old midpoint) = $550M total raise.

$550M - $320M (Semrush FY26 est.) = ~$230M organic revenue raise

Hit

~$500M total ARR adjustment = ~$250M (deferred CC price hikes) + ~$250M (freemium funnel sacrifice)

Adobe is taking the hit because they do not want to (or cannot) increase prices right now and risk alienating free users if they ask them to pay.

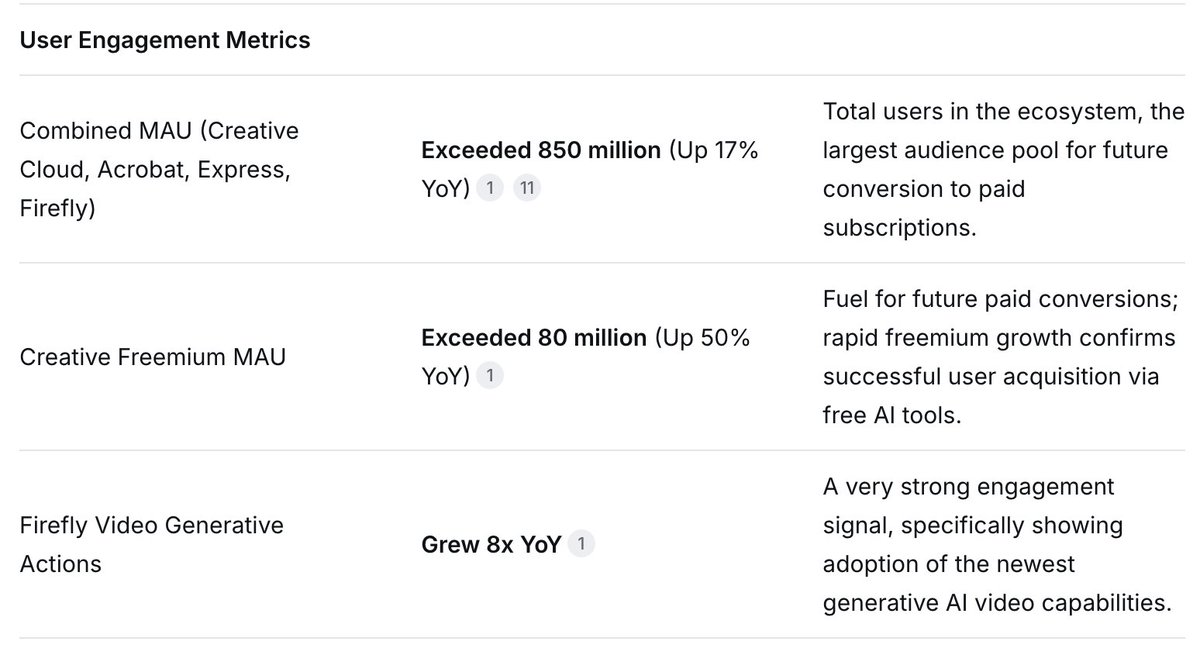

Traffic, MAU and usage are growing. But will they convert to revenue?

$ADBE claims that they are seeing 40% traffic growth driven by "intent based searches" (summarise pdf, pixelated art).

But their income statement shows something different.

Sales and marketing expenses spiked 180bps in Q2.

Is the freemium pivot really driven by demand?

Will users use AI prompts to place a text box, split clips at precise timestamps, change fonts, apply color masks?

Inferencing over the network is more expensive for these tasks both in $ and time.

The only creative tool required is a prompt box except for high end use cases is misguided assumption.

A balance of AI + basic + advanced tools is needed for different workflows.

It's up for debate whether $ADBE is well positioned to deliver these workflows but the argument that AI is going to replace all humans and software with a prompt box is .... meh.

To everyone who is scratching their head about why $ADBE dropped after such a great print.

- CFO exit

- Margins compressed, both GAAP and non-GAAP

- Non GAAP opex was up 14% (ahead of revenue)

- Freemium strategy may have poor future pay off as model switching costs are very low.

Some other interesting info:

- $ADBE spent 0.88% of their revenue in capex compared to SaaS peers, $CRM spent 1.3% and $NOW's 3.74%

- So freemium and discounted AI usage cause direct operating margin pressure as they reserve higher capacity at hyperscalers

- Both frontier labs are totally focussed on improving coding tasks and making unit economics work. The only heavyweight player investing heavily in media generation is $GOOGL - potentially using their own TPUs

- Generating media is substantially more expensive than generating text based tokens. 1 image costs ~2000 lines of code, 1 video is ~10000 lines of code. So its a massive driver of compute demand

- Which makes it quite compelling for $NVDA to have a deep partnership or even an equity stake

- Personal experience using Adobe products. Acrobat Reader is an exceptional product (especially AI read aloud), far superior than any other document viewer. Adobe Firefly's speech based models are impressive. Adobe Express is mid.

To everyone who is scratching their head about why $ADBE dropped after such a great print.

- CFO exit

- Margins compressed, both GAAP and non-GAAP

- Non GAAP opex was up 14% (ahead of revenue)

- Freemium strategy may have poor future pay off as model switching costs are very low.

Some other interesting info:

- $ADBE spent 0.88% of their revenue in capex compared to SaaS peers, $CRM spent 1.3% and $NOW's 3.74%

- So freemium and discounted AI usage cause direct operating margin pressure as they reserve higher capacity at hyperscalers

- Both frontier labs are totally focussed on improving coding tasks and making unit economics work. The only heavyweight player investing heavily in media generation is $GOOGL - potentially using their own TPUs

- Generating media is substantially more expensive than generating text based tokens. 1 image costs ~2000 lines of code, 1 video is ~10000 lines of code. So its a massive driver of compute demand

- Which makes it quite compelling for $NVDA to have a deep partnership or even an equity stake

- Personal experience using Adobe products. Acrobat Reader is an exceptional product (especially AI read aloud), far superior than any other document viewer. Adobe Firefly's speech based models are impressive. Adobe Express is mid.

I think the questions market is trying to answer are -

1. Will $ADBE be able to expand seats or raise per seat pricing moving forward? (incremental ARR)

2. And if not, whether that loss will be offset by AI first revenue (Firefly, AI assistant, Gen studio etc.)

If $ADBE hits it out of the park on both fronts, a re-rating is likely given the undemanding valuation.

Last quarter was one of the worst incremental ARR they posted, driven by race for freemium adoption and decline in stock photo business (~70M).

When problems arrive, they never go away in 1-2 quarters. But with this valuation and Adobe's distribution muscle, I think odds are in investor's favour.

Here is how much incremental ARR $ADBE added during last few quarters.

Q1 2025 - 450M

Q2 2025 - 580M

Q3 2025 - 660M

Q4 2025 - 920M

Q1 2026 - 400M

Q2 2026 - (TBA tomorrow)

This is the the number that decides whether $ADBE goes to $200 or $300 next.

Even if $ADBE loses 300 basis points of margin over the next 10 years to achieve a mid single digit growth ... at the current valuation, your investment will be paid back completely just with post-tax operating earnings over the next 10 years.

Shorts will be burned, eventually.

These were the most important metrics that $ADBE shared during their last earnings call.

The stock dropped because it turns out their AI business is cannibalising the stock photo business and the veteran CEO is stepping down.

I will be watching the credit consumption metric to see how well they can capture GenAI usage from within their products. What metrics will you be watching?

@ariaradnia They did infact added math and chess to their app.

It will be smarter to add both $duol and $adbe to the portfolio rather than mocking one and promoting the other.