🚨Congressman Thomas Massie dropped the bombshell everyone was waiting for: He revealed Epstein's hidden list and exposed Kash Patel for lying to the American people. Massie says: 'The FBI has files with the names of 20 other men involved with Epstein in the sex trafficking network, including a high-ranking government official.'"

@ShadowofEzra Charlie publicly changed his mind on israel but they claimed he did . He never publicly said anything about Massie, but they claim he changed his mind.

Go fuck yourself @AndrewKolvet you are a diagrace

Thomas Massie just declared: “This government is under siege.”

And he exposed Susie Wiles and Pam Bondi for taking “millions of dollars from Bayer.”

“All three branches of this government are under siege by lobbyists and lawyers from a German company named Bayer.”

“They spent over $9 million lobbying … so that they don’t have to be liable for any damages their herbicide Roundup causes.”

“The Constitution guarantees people a trial if they’ve been harmed.”

“Why are we contemplating going against the Constitution?”

“The Attorney General has opined favorably for this German company in front of the Supreme Court about getting rid of any liability that they should have for any damages.”

“By the way, the President’s Chief of Staff and the President’s Attorney General worked for one of the biggest lobbying firms that’s received millions of dollars from Bayer.”

“Maybe that’s why we’ve seen an executive order that says that the production of this chemical from this German company is a national defense priority.”

“And we know why they’re doing that.”

“It’s to keep them from having any liability.”

“This is wrong.”

“We shouldn’t succumb to the lobbyists, not in the executive branch, not in the judicial branch, and certainly not here in Congress.”

If America would embrace capitalism and reject cronyism

in health care, agriculture, military contracting, insurance, media, technology, and banking,

we would experience a renaissance unprecedented in human history.

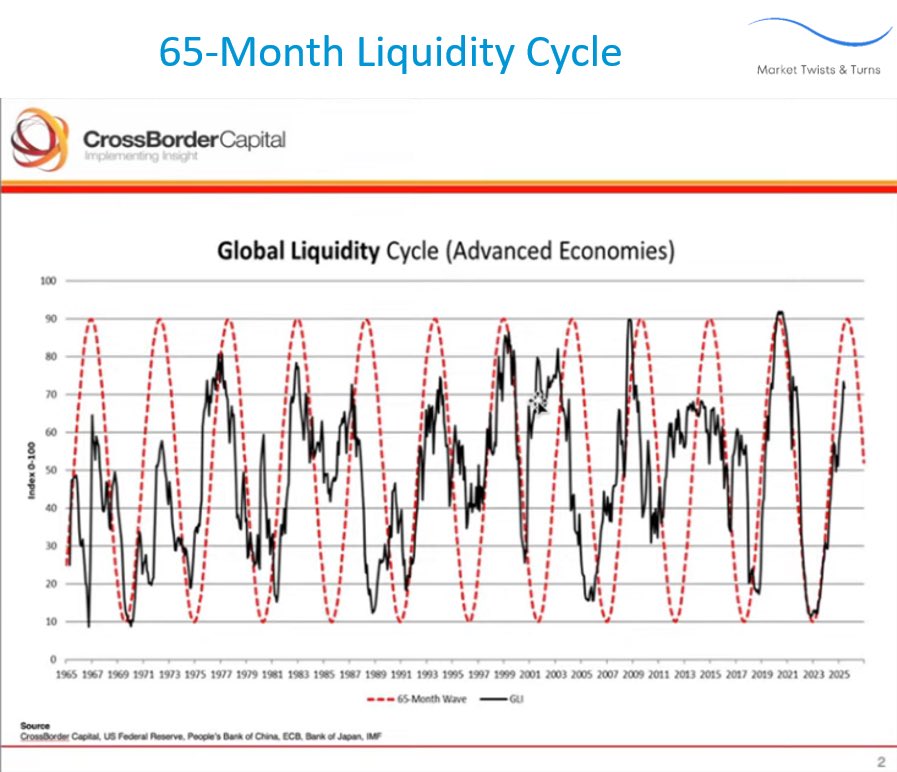

Where We Are in the 65 Month Liquidity Cycle (Nov 9, 2025)

Look past the noise and this chart by @crossbordercap shows global liquidity moves in a 65 month tide. The red dashed curve is the rhythm; the black line is reality. When the black line climbs toward the dashed crest, funding loosens, risk taking rises, and prices levitate. When it rolls over, air thins.

What the chart is showing

After the post COVID squeeze and the drain through 2022–23, the black line troughed in 2023 and has been rising. That ascent lines up with the policy pivot already in motion: two rate cuts into the fall, the scheduled end of balance sheet runoff on December 1, and reinvestments aimed at short dated Treasuries. That mix rebuilds bank reserves, eases overnight financing, and pulls the black line toward the dashed peak.

Where we are now

As of today, we’re late in the upswing, well past the halfway mark, approaching the crest. Reading the spacing of prior cycles on this same template (think 1998–03, 2011–16, 2016–21) and the slope of the current rise, the highest probability window for a peak sits in Q1 to early Q2 of 2026, roughly late March through June. There can be shoulders around the top when policy and deficits keep the pump running, but the cycle’s geometry points to spring.

How it travels through the system

•Front end of the curve: Reinvesting into bills adds a steady buyer. Repo softens, SOFR drifts down, and the cost of carry improves.

•Bank and dealer plumbing: Cheaper overnight money steadies balance sheets and encourages basis/carry trades. Liquidity feels abundant because funding is reliable.

•Credit and equities: Spreads grind tighter, primary issuance reopens, and multiples stretch, the discount rate investors feel is the front end, not the 30‑year.

•Long end: Term premium resists. Heavy Treasury supply, persistent inflation expectations, and foreign buyers demanding compensation keep 20–30 year yields relatively firm. The result is easier at the front, heavy at the back.

•Housing: With mortgage paydowns redirected toward bills rather than MBS, mortgage spreads don’t fully collapse. Rates improve at the margin, but not in a straight line.

•Dollar and commodities: A softer front end trims the dollar’s carry edge; late upswing phases often see a gentler dollar, firmer EM beta, and support for cyclical commodities.

•Global layer: Allies with weaker growth lean on U.S. liquidity; non aligned blocs keep building buffers and local currency pipes. That fragmentation keeps the long end sticky even as the front loosens.

What confirms we’re topping

Cycles usually peak with calm: volatility quiet, funding effortless, and bad news shrugged off. Tells to watch (not as advice, as diagnostics)

• Bills trading rich to policy; then that richness fades.

• Repo and SOFR stop drifting lower and stabilize.

• Treasury auctions start tailing at the long end even as the front stays easy.

• Credit spreads stop tightening before they widen; primary calendars thin.

• High beta equities stall while quality holds; breadth narrows.

• The dollar stops weakening despite easy funding. capital turns cautious.

What it means going forward

Late upswing liquidity props up valuations and stretches the cycle. It does not fix structural mismatches: large deficits needing term buyers, aging demographics pressing real resources, and a world reorganizing supply chains for resilience over efficiency. Historically, growth data lag the liquidity peak by several quarters; the party ends quietly and then all at once.

So, as of today November 9, 2025, we’re in the high tide’s approach. The chart’s rhythm and today’s plumbing both point to a spring 2026 crest. Expect markets to feel unusually orderly into that window…funding smooth, spreads tight, narratives confident. That’s how peaks like to look. The tide turns only when belief meets math.