Jim Simons on why he never hired finance majors or people from the investment industry

“You can teach a physicist finance , but you can’t teach a finance person physics”

The AI loop is not a fraud. That is what makes it dangerous.

$MSFT / $AMZN / $ORCL fund capacity → $NVDA / $AMD sell the shovels → $CRWV leases the data centers and buys the GPUs → AI labs commit future spend → suppliers book revenue → equity valuations validate the next financing round.

Everyone sees the revenue.

The real question: how much is end-user cash flow and how much is recycled capex financed by the same handful of balance sheets?

The first fracture likely shows up in the leveraged middle: $CRWV, GPU-cloud peers, data-center lease structures, private credit.

But the larger asymmetry may be $NVDA itself.

Not because Nvidia is a bad company. It is probably the best company in the chain. But “best company” and “safe stock” are not the same thing when the market is pricing permanent hypergrowth off a spending cycle that may have been pulled forward.

A modest slowdown in AI ROI, utilization or hyperscaler capex does not need to kill AI.

It only needs to make the market ask a different question:

What are normalized earnings for $NVDA, $AMD, $ORCL, $VRT and $ETN when the arms race turns into return-on-capital discipline?

That is where the multiple cracks.💣

In 2002 a credit card stock fell 60% in two days on fraud rumors. Everyone sold.

Two outsiders did their own digging even called the CEO's old college classmates decided the crowd was wrong, and turned $26k into $526k on a single options bet.

How 👇

https://t.co/1lU5e4vOXf

The most important chart of the month isn’t $NVDA. It’s a token index almost nobody tracks.

The Silicon Data LLM Expenditure Index measures what the market actually pays for AI tokens the closest thing we have to a real-time P&L of the AI buildout. It just rolled over hard.

Citadel Securities flagged it in a macro note this week & their interpretation should make every AI bull uncomfortable: spend isn’t falling because demand died. It’s falling because customers got their first real token bills and started trading down. Frontier models swapped for cheaper ones. Experiments cut. Inference budgets capped.

That’s elasticity. The thing every “demand is infinite” model conveniently left out.

Follow the mechanism: AI revenue forecasts assume customers consume more compute every quarter, forever, at any price. But compute, power, cooling, and memory bandwidth are scarce so prices ration. And rationing means the frontier doesn’t get abandoned, it gets concentrated. A few balance sheets keep playing. The rest of the market quietly downgrades to “good enough.”

Two-tier AI economy. Priced like one tier.

The street spent two years asking what these models can do. The customers just started asking what they cost. Those are different questions and only one of them shows up in earnings.

Watch the token index, not the keynotes. Capability tells you the story. Spend tells you the truth.

Michael Burry’s $NVDA Nvidia short isn’t really a bet against AI.

It’s a bet against the sustainability of AI spending.

Three customers now make up roughly 64% of Nvidia’s accounts receivable.

In 2020, it was 33%.

That’s not broad demand. That’s concentration.

Burry’s point is simple:

The market is treating today’s AI capex as permanent.

What if it’s not?

Right now, hyperscalers are in an arms race. They’re benchmarking models, chasing leaderboard rankings, and building capacity at breakneck speed.

But eventually the race slows.

When it does, the question becomes:

Who is the incremental buyer?

Because when a trade is crowded and demand is concentrated, the exit door gets very small.

The AI story may be real.

The spending curve is what Burry is betting against.

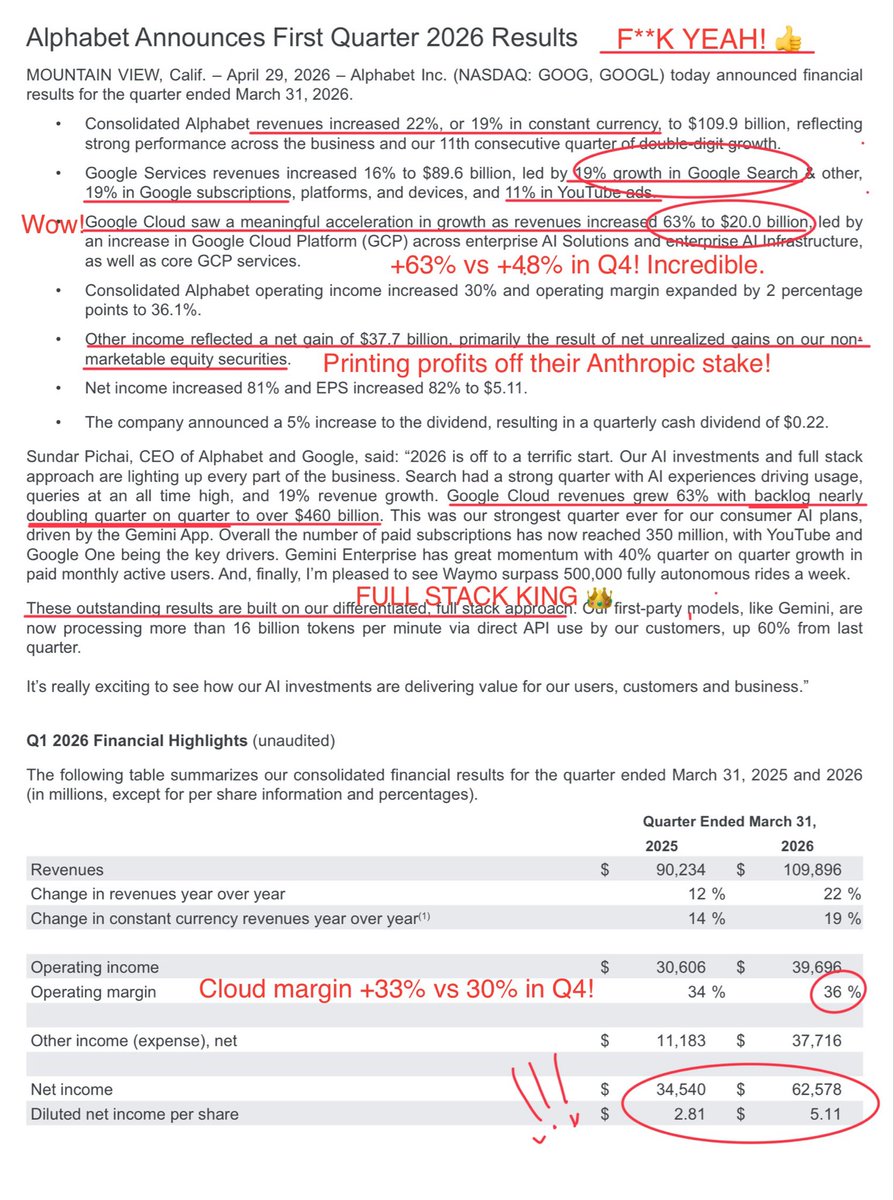

The $GOOG numbers were absolutely MIND-BLOWING.

Revenue +22%. Cloud +63% (WTF???) up from +48% in Q4, with record margin at 33% despite huge capex. Search accelerated yet again to +19%. The opposite of dead! Total Op margin at 36.1% (+200bps) = staying lean!

Just STUNNING. 🤯

The global debt crisis is set to get even worse:

Total sovereign and corporate bond issuance is estimated to rise to a record $28.8 trillion in 2026.

That would mark the 4th consecutive annual increase and would also DOUBLE the average pre-pandemic levels.

Corporate debt issuance is set to surge to a record $6.9 trillion, while government debt issuance is expected to rise to $21.9 trillion, also an all-time high.

By comparison, governments and corporates issued $23.7 trillion of debt in 2020, during the pandemic.

As a percentage of GDP, global issuance is expected to increase to 23.3%, the 2nd-highest on record, only behind the 27.5% peak during the pandemic in 2020.

To put this into perspective, the 2008 Financial Crisis peak was 21.4%.

The world is borrowing ABOVE crisis levels.

When geopolitics hits shipping lanes, watch the freight, not the headlines.

Breakwave Tanker Shipping ETF $BWET is ripping tanker rates are the purest play on Hormuz risk. Longer routes, tighter supply, higher day rates.

Smart money follows the freight.

BWET. One of the tickers that matters this week🗞️

Trump’s Hormuz deadline hits Tuesday 8PM ET. He’s bluffed 3 times already. Iran told him to pound sand.

This ETF is 90% Middle East → China crude freight futures. Up 243% YTD. A geopolitical bet sitting on a US exchange.

Ray Dalio: “Something needs to prick the bubble to cause a market crash.”

Historically, what ended overvalued markets was something that led to substantial outflows of cash, generally rate hikes or quantitative tightening.

Up until now, we didn’t have an environment for a rate hike, this is changing now as inflation is set to tick upward due to increasing oil prices and tariffs.

If the Fed hikes rates, it may trigger secular outflows, leading to the crash of this market.

Nobody can know what’ll happen, but it’s important to position accordingly now.

Regardless of what happens, you should be staying in your high-quality and undervalued positions.

Also raise cash allocation preparing for the worst, and if it happens, be ready to buy.

For those who position correctly, a crash is good news. However, I still don’t believe there’ll be a real crash.

What’ll likely happen is that Iran situation will be resolved over the next couple of weeks, and market will partially recover. That recovery can sustain and we may see new highs if Q1 earnings come above expectations.

In short, caution should be the governing paradigm now, but it’s also important to keep optimism since this market still has strong tailwinds as well, not just headwinds and uncertainty.