Stablecoins made cross-border settlement faster.

But the hard operational questions remain:

- did the beneficiary receive the right amount?

- which rail failed?

- where did fees and FX move?

- which provider reference maps to which payout?

- what breaks at month-end reconciliation?

I’m researching this from the operator side.

If you run stablecoin payouts, off-ramps, contractor payroll, or payout ops, I’d love to compare notes.

Most reconciliation tools don’t solve problems.

They hide them so the dashboard looks clean and management stays happy. That little delta? They just swallow it and move on.

Finance teams call it “reconciled.”

Auditors and CFOs later call it a disaster.

🚀 ReconLayer is now open for free access-for a limited time.

Following the interest we’ve received from users, we’re opening @ReconLayer so more payment, finance, treasury, and operations teams can explore the platform and share feedback.

Stablecoins now represent a market of more than $312 billion. As stablecoin and cross-border payment activity grows, records become fragmented across providers, blockchains, banks, ledgers, ERP systems, CSVs, and APIs.

@ReconLayer brings this evidence together into one reviewable reconciliation case-helping teams understand:

⚡ What settled.

⚡ What broke.

⚡What finance should record.

#ReconLayer is still early, and your feedback will directly help us improve the product, integrations, matching logic, exception workflows, and finance-ready outputs.

Be part of the ReconLayer journey.

Explore the platform, test the workflows, and tell us what your team needs.

✅ Free access for a limited time

💬 DM us to get access

🛠️ Help shape the future of stablecoin payment reconciliation

#ReconLayer #Stablecoins #Fintech #PaymentReconciliation #CrossBorderPayments #Web3

@0xPolygon 's Marketplace Stablecoin Playbook makes one thing very clear:

Stablecoins may improve settlement speed, but marketplace payments still need serious reconciliation.

The underrated layer is knowing what actually happened after money moved.

This is exactly why we are building @ReconLayer

Thread 👇

Makes sense.

Do you know of any specific companies/operators publicly discussing this pain?

I’m trying to separate “structural issue exists” from “teams are actively buying tools/workflows to fix it.”

Even anonymized examples like “exchange treasury team,” “stablecoin payroll company,” or “cross-border PSP” would help.

1/

“Transfer completed” is not the end of the story.

For #neobanks, it is often the beginning of the real work finance and ops teams still have to handle:

🏦 Provider events

📄 Bank payout files

⛓️ On-chain confirmations

📘 Ledger entries

💸 Fees

🧾 ERP records

BNY - America's oldest bank, $59.3T in custody - will mint and redeem USDC directly from its custody platform before July ends.

Not through a partner. Not via a pilot. Directly.

This is not a crypto headline. This is a bank operations headline.

And it changes what stablecoin reconciliation means.

For the past year, reconciliation has been framed as a crypto-native problem.

Dashboards for on-chain teams.

Matching engines for DeFi treasuries.

Exception handling for digital asset firms.

That framing is now different.

When a G-SIB custody platform moves into stablecoin minting, the reconciliation surface is no longer "did the bridge API match the on-chain receipt? "

It is "did the custody ledger, the central bank reserve, the tokenized deposit rail, and the on-chain balance all settle to the same number at the same time? "

That is a different problem. It needs a different standard.

The UK just launched the same parallel system.

GBTD - Great British Tokenised Deposits - is executing real money pilots across multiple banks, mapped to Bank of England RTGS, scheduled for full production by 2027.

Two G-SIB jurisdictions. Two parallel money systems.

One shared gap: there is no bridge layer between tokenized deposits and stablecoins that proves settlement happened correctly across both.

The asset layer is being built by the biggest names in finance. The reconciliation layer is not.

This is where the work is.

We are building @ReconLayer because the gap between "payment successful" and "settlement proven" widens every time a new rail gets added.

Banks entering the space does not close that gap.

It makes the gap enterprise-critical.

The institutions are coming.

The infrastructure to run them is not.

Stablecoins are not the 'simple' part of crypto.

Everyone says the same thing: price stays close to a dollar, so what could go wrong.

A lot.

A user sends $100. The UI says 'Payment Successful' in 3 seconds.

Behind that green checkmark, four systems are recording four different versions of the same transaction.

Each one is correct. None of them match.

You don't have a stablecoin problem.

You have a reconciliation problem.

The race to zero is over for stablecoin rails.

On/off-ramp margins are compressing to single-digit basis points.

When the rail itself becomes free infrastructure, value moves up-stack.

Bridge says paid.

On-chain says confirmed.

Payout API says processed.

The bank statement shows a different number.

None of those systems is wrong.

None of them owns the full picture.

Reconciliation is not back-office hygiene.

It is the control plane.

And it is the only layer nobody is building.

Stablecoins look solved until you have to operate them.

A treasury dashboard can show a balance in real time while the workflow behind it is still manual: batch compliance jobs, weekly reconciliation reports, fraud rules built for ACH.

The payment clears in seconds. Your controls run overnight.

That gap is the real risk.

The companies that win won't be the ones with the biggest stablecoin balance.

They'll be the ones who can screen, match, and reconcile across rails fast enough to keep up with the settlement.

The asset is easy.

The operating model is the moat.

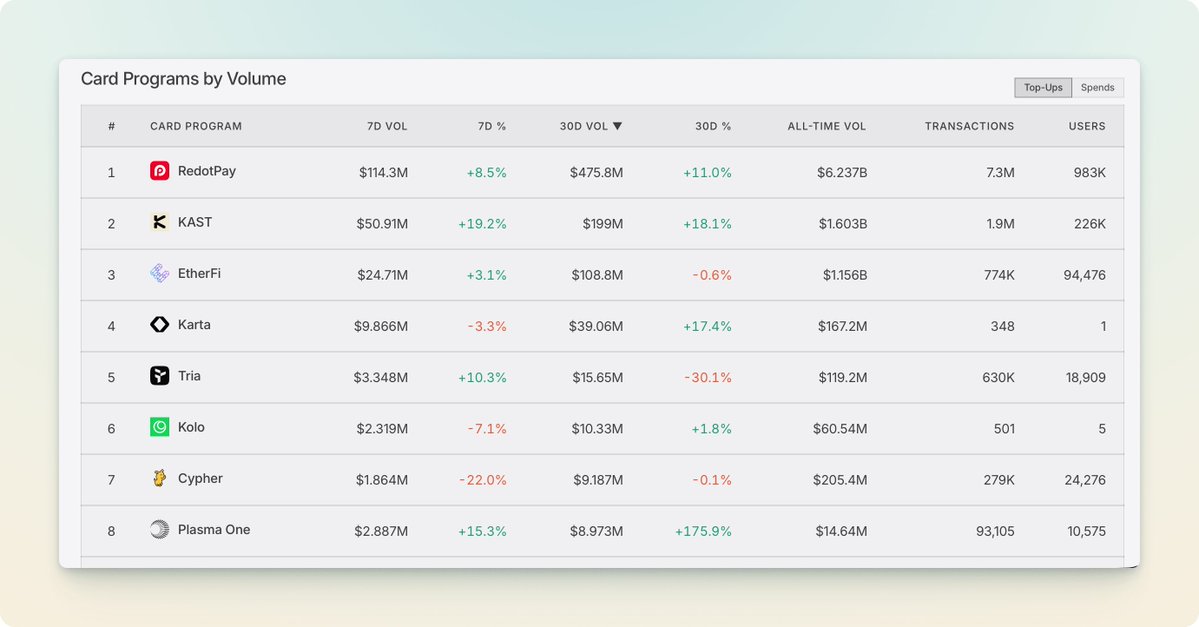

Stablecoin card deposits crossed $10B+ last month.

The chain is not the bottleneck anymore.

Stripe just added 140 partners to Open USD.

The press covered governance and zero-fee mint.

The ops reality:

- 140 settlement integrations, none standard

- Multi-chain finality with different confirmation times

- Yield that changes balances asynchronously

- No single authority who can answer "did this settle?"

Single-issuer stablecoin: one ledger, one call when numbers don't match.

Consortium stablecoin: 140 ledgers, 140 opinions, and a monthly close meeting.

This is fintech 2015-2020 all over again. Build fast. Reconcile for years.

When PayPal settles USDC, PayPal reconciles against Circle. Clean. One source of truth.

When OUSD settles across Tempo, Solana, and partner custodial wallets, who reconciles against whom?

Today: spreadsheets and Slack threads.

The next infrastructure battle won't be custody or issuance.

It will be who owns the truth when nobody owns the stablecoin.

Excited to see Open USD (@openstandard ) launching later this year.

As stablecoin volume grows, reconciliation across on-chain and traditional rails will become even more important.

@ReconLayer is built for exactly this - delivering clear, auditable reconciliation at scale in multi-rail environments.

#OpenUSD #Stablecoin #Reconciliation

Open USD @openstandard is launching later this year🚀

As stablecoin volume grows and more payments move on-chain, reconciliation in hybrid (on-chain + off-chain) environments will actually become more important, not less.

Tools like @ReconLayer are perfectly positioned to handle the increased complexity, exceptions, and multi-rail matching at scale.

#OpenUSD #Stablecoin #Reconciliation #Fintech

Stablecoin payments just hit $226B in B2B volume.

140+ companies just joined the Open USD consortium.

BIS and Coinbase are fighting about what stablecoins even are.

Everyone is watching the market.

Almost no one is watching the operations.

A payment that moves across three ledgers in 10 seconds still needs manual reconciliation across bridge APIs, on-chain logs, payout webhooks, and bank statements.

That work does not scale with the volume. It explodes with it.

The bottleneck is not settlement. Settlement became fast.

The bottleneck is knowing what actually happened after settlement.

Every exception, every missing webhook, every mismatch between expected and actual - still resolved by an ops team in a spreadsheet.

You can build the fastest rail in the world.

If the reconciliation still takes days, the payment is not finished.

Businesses don't want to handle wallets, private keys, and off-ramps.

So they don't anymore.

Customers pay in crypto. Merchants settle in dollars. The whole thing runs in the background.

Checkout wired this in with Coinbase. Visa's doing it. Stripe's building its own rail.

No end-user ever sees a wallet. This isn't stablecoins going mainstream.

That already happened.

It's stablecoins becoming invisible - the way infrastructure is supposed to work.

You don't think about TCP/IP when you load a webpage.

Soon you won't think about stablecoins when you pay.

AmEx is hiring a VP of Stablecoin Payments.

Stripe is incubating a stablecoin L1.

Toss Bank (15M users) is piloting stablecoin remittance.

Payment giants adding rails. None solving reconciliation.

Faster rails without matching is just faster chaos.

Stablecoin payments look clean from the outside.

➤ A payout is approved.

➤ USDC moves on-chain.

➤ A transaction hash appears.

➤ The product says “paid.” ✅

But finance still has one hard question:

Can we actually close the books on this?

That is the four-ledger problem. 🧵