Quieter week for #grains with the UK half-term & lack of global market direction leading #wheat lower vs last wk. #Barley flat, #OSR steady, #pulses quiet. Your weekly update from the grain store follows.

https://t.co/QrJb8Sq0X5

#Wheat steady as US/Aus supply tightens, #barley trade thin. #OSR firm on dry EU weather, new crop #pulses supported by rain. Crude $105, £/€1.15. Moisture meter clinic returns 17 June. Your weekly update from the #grain store. https://t.co/NwesiLLKGU #oatt#arable

Tomorrow sees our first moisture meter clinic. 10am-3pm here at the grain store. Join us for coffee and tea, cakes & a chat, plus Origin Soil Nutrition will be here to talk fertiliser options for the autumn. https://t.co/szPdde7sW3

Even after the #WASDE cuts, 26/7 world #wheat stocks sit about 1.3% above 5 yr av, which may cap rallies unless weather risk >. #Soybean & #OSR stocks are more comfortable, but crude & biofuel demand are > prices. via @AHDB_Cereals 3/3 #oatt#grains https://t.co/Qde5KwLk9x

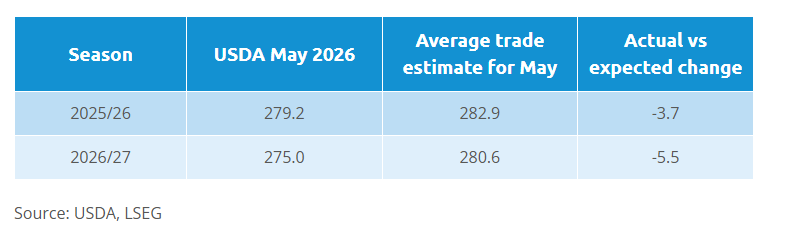

USDA May #wasde cut 25/26 and 26/27 world #wheat ending stocks versus trade ideas. Global wheat stocks are now seen 4.2 Mt lower YoY in 26/27 at 275 Mt, with the biggest < in the US. EU, Australia, Canada and Russia also see lower ending stocks. 1/3

USDA’s first look at 26/27 points to tighter #wheat & #maize, with wheat stocks 5.5 Mt below trade expectations & maize 10.9 Mt below. Maize ending stocks in 26/27 are forecast 6.5% down on the year and 8.9% below the 5yr av, pot the < since 13/14 if realised. 2/3

#Wheat firmer on tighter US supply, though new crop steadier after rain. Markets eased late week on lack of fresh China demand. #Barley quiet and well covered. #OSR supported but capped by LatAm beans. Your weekly update from the #grain store #oatt https://t.co/7zLzK3gI91

#Wheat eases after last week’s spike, rain helps UK/EU crops. #Barley steady, malting sentiment improving. #OSR softer but veg oil fundamentals tight. #Pulses & #oats quiet with crops in good shape. Your weekly update from the #grain store https://t.co/XfSBnQAlJ8 #oatt#arable

UK winter cereal crop conditions have dipped since late March, but still better than the same time in 2025 and above 2022–24. The recent rainfall over the BH wknd will have helped. https://t.co/4ftv75hp0p (via @AHDB_Cereals) #oatt#grains#wheat#barley#OSR

70% of UK winter #barley is rated good/excellent (52% good, 18% excellent), down sharply from 85% last month and only slightly above 68% a year ago, with conditions varying markedly by region. 2/2 #oatt#grains#arable https://t.co/4ftv75hp0p

@AHDB_Cereals have today published their April crop dev update: 75% of UK winter #wheat rated good/excellent (down from 82% in March but well above 60% last year), with dry conditions in much of England key to yield risk. 1/2 #oatt#grains#arable

#Wheat eases from 6-month highs on profit‑taking; US drought trims crop ratings. #Barley steady; new crop malting supported. #OSR surges on Middle East tensions. #Pulses & #oats quiet. Brent $111, €/£1.15. Your weekly update from the #grain store #oatt https://t.co/AWlSo8uZY7

#Wheat steady but weather risks building; #barley flat with limited demand. #OSR firm on crude oil rise. #pulses & #oats markets quiet but crops need rain. Crude back over $100, £/€ at 1.15. Your weekly update from the #grain store #oatt#arable https://t.co/aUKi8N44Mb

#Wheat & #barley eased on comfortable global supplies, while #OSR & #pulses held in choppy, rangebound trade. We are now taking storage bookings for harvest. Save the date for local events coming up at the #grainstore. Your weekly update #oatt#grains https://t.co/q5NDLM0Pmp

#Maize availability falls nearly 1Mt y/y as #imports shrink & #bioethanol disappears. H&I #oat use edges up to 519Kt on firm demand for #oat products & exports. Any #Ensus restart would add upside to H&I cereals. #grains#oatt https://t.co/U0jfd2sA1T /3

UK cereals S&D for ‘25/26 from @AHDB_Cereals. Human &Industrial (H&I) demand cut again to 8.99Mt, now the weakest since records began in ‘99/00 as brewing, malting & distilling (BMD) & flour demand slows. Feed use more resilient at 13.3Mt, just 65Kt below ‘24/25 #oatt#grains 1/

#Wheat & #barley doing more work in feed. H&I wheat trimmed to 6.5Mt (–625Kt y/y) with no wheat into #bioethanol, while H&I barley drops to 1.464Mt (–333Kt y/y, lowest since ‘90/91) as BMD struggles & more barley gets pulled into rations #oatt#grains /2

IGC #wheat sub‑index is up 6% on geopolitical and crude‑linked support plus US weather concerns. #maize is up 2% & at a 10‑month high. #rice down 3% on subdued buying and freight volatility; #soyabeans are 1% softer on weaker Argentina FOB values. @IGCgrains#oatt#arable

IGC forecasts world #grains production to fall 2% to 2.417mt, total supply contracts for the first time in 4 seasons. End‑season stocks to drop to 609mt, mainly in major exporters, despite another record in consumption (via @IGCgrains) https://t.co/V4ZloFQv3t

Fertiliser prices had already spiked higher pre‑Iran conflict & up £100/t since. Markets now eye @USDA#USDA Prospective Plantings (31 Mar), 1st 26/27 S&Ds in May & @AHDB_Cereals upcoming UK S&D & crop condition updates later this wk. https://t.co/4ftv75hp0p #oatt#arable#grains

1⃣ Grain markets eased last week as high near-term global supplies & rains in the US Plains pressured wheat & #maize, with May26 UK feed #wheat closing at £171.25/t (‑£3.20 w/w). (via @AHDB_Cereals) https://t.co/3dk1xQVvKY #oatt#grains#arable

2⃣ Oilseeds #OSR softened: May-26 Paris matif rapeseed fell 1.8% to €501.75/t, dragged by weaker Chicago #soyabeans, a stronger € euro & profit‑taking. #oatt#grains#arable