Production up ~10% YoY May.

Liquids prod up ~18% YoY May.

Capex down ~30% YoY April.

Shaping up to be another really nice quarter for debt paydown, despite summer gas and divy bump 😉.

No close 2nd for Canada dry gas 🍻.

$PEY $PEY.TO #COM#OOTT

https://t.co/lcL1puNkAJ

News Release - June 3rd 2026 - Selkirk Copper’s Final Phase 1 Drill Program Results Deliver High-Grade Mineralization Intersected Across Five Target Areas, and Rapid Progress on the Phase 2 Drill Program

Full release here: https://t.co/VNXIJSo9au

#SelkirkCopper $SKRKF $SCMI

With experienced leadership in place, huge exploration upside, and first nation invested, hard to find a better value/positioned name than @selkirkcopper. 6 weeks or so until the proof of underlying economics becomes obvious to all $scmi.v

A new @CruxInvestor article explores why brownfield #copper mine restarts are gaining attention, highlighting $SCMI $SCMI.v $SKRKF @SelkirkCopper and its Minto Mine restart strategy, existing infrastructure, Indigenous partnership model & more💥⛏️⬇️

https://t.co/3fDNyzz7pt

🚨 Important NEW Slide 🚨

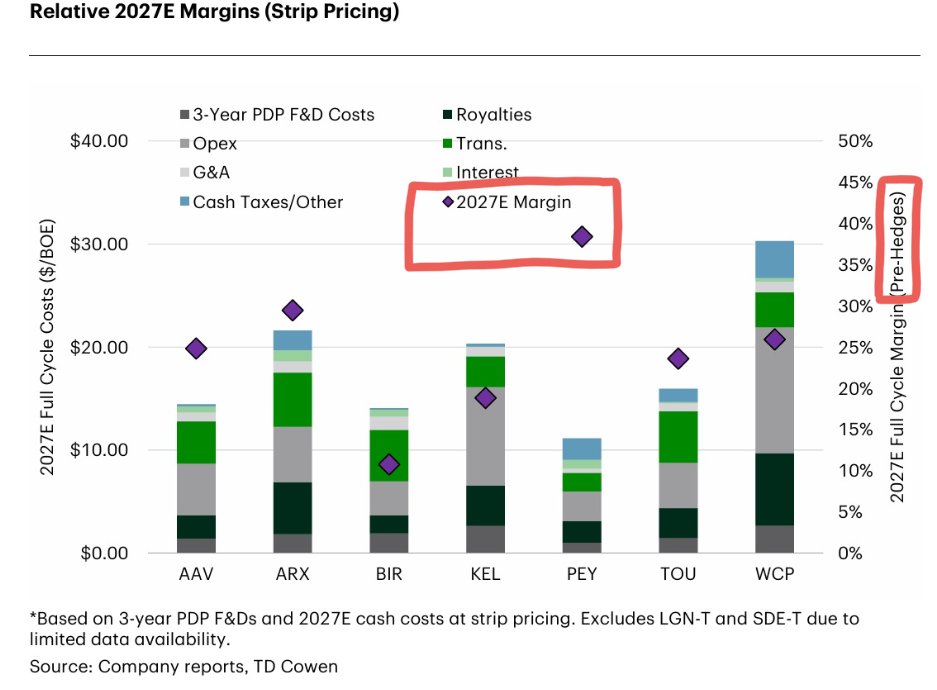

Like Warren Buffett used to say, “The market, like the Lord, helps those who help themselves. But unlike the Lord, the market does not forgive those who cannot calculate full cycle economics” 🔥 🚀 🔥 $PEY.TO

For the record.

The insanity is not that rates might be raised again, but that so many at the Fed seem eager to do it.

Fed policy works through the interest‑sensitive parts of the private sector, with housing at the front end of the transmission mechanism. With house price growth now slipping into negative territory, monetary policy is demonstrably in restrictive territory rather than accommodative. Nonetheless, the prevailing Keynesian consensus at the Fed and on Wall Street continues to argue for additional tightening in response to supply‑driven price shocks, effectively using demand destruction to solve a supply problem. That approach risks compounding the policy mistake: crushing housing and other rate‑sensitive sectors while doing little to address the underlying supply constraints.

@TokStocks@TokStocks good recent interview with CEO of @selkirkcopper, large position for me. On Cambria also. Have you done any work to assess potential found $ of Mt. Margaret asset? The big royalty concern, plus warrant overhang have kept me out of it to date. $camb.v $scmi.v

Phenomenal from Carney. Bravo.

“Carney said recent global shocks have threatened the availability of some forms of energy, putting other countries in a bind. He said Ottawa wants to move quickly to supply those resources, and if B.C. stands opposed to more development, his government will "be spending more time elsewhere in the country."

https://t.co/I7FqkLcjSE

Still completely under the radar, is the potentially massive resource expansion available on @SelkirkCopper existing claims to the north of Minto North. Selkirk's Phase II 50KM drill program is already underway, laying the ground-work for future discovery ... $SCMI.V

Join Selkirk Copper at The Mining Investment Event in Quebec, Canada.

🗓June 1-4, 2026

📍Centre des Congrès de Québec, Quebec, Canada

🔗https://t.co/KcfM0vEGBT

If you’re attending and would like to learn more about the Minto Mine, please connect with us.

#selkirkcopper#copper

$SCMI.v on top of this interview which is awesome. I have 3 historical docs from Minto Metals that should be of interest to all of us - https://t.co/XU3L0G2PHJ

https://t.co/Zjh1K4kzM8

https://t.co/YujXGpVvhS

I would recommend running them all through Chat - you will be buying more stock soon if you do :-)

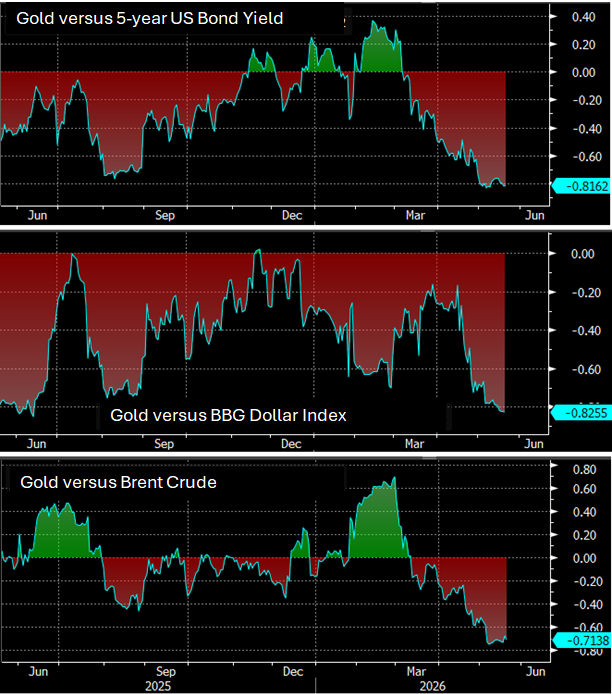

#Gold is currently showing very elevated inverse correlations with bond yields, the dollar and crude oil, underscoring the reaction function currently driving price action and what likely needs to change for bullion to attract a renewed bid. Rising yields increase the opportunity cost of holding non-yielding assets, a stronger dollar reduces gold’s appeal for non-US buyers, while higher crude prices are feeding inflation and rate-hike expectations rather than supporting gold through their traditional inflation-hedge channel.

The recent shift highlights how markets are currently focusing less on gold’s longer-term structural drivers - fiscal debt concerns, reserve diversification, de-dollarisation and central bank demand - and more on near-term macro headwinds. For gold to regain upside momentum, the market needs to see some easing in oil-driven inflation concerns, or renewed evidence that growth risks are beginning to outweigh inflation fears.

Charts from Bloomberg

Chart posted for $SCMI.v - Don’t sleep on learning this story

We are still so early on the path to production in 2028. But the stock is trading on incredible strength after strong showing on $35M over sub’d financing in April. 📈📈

One of my fav #Copper stories