We've experienced tremendous growth @whatifventures as we recently eclipsed $100mm AUM.

With that, we are growing into new verticals and adding Defense technology as our second primary focus next to healthcare.

To date, we’ve been very focused on healthcare, and going forward we are going to expand that mantra to HEALTH AND FREEDOM.

Since inception, What If Ventures has deployed $100mm+ into 86 startups with a significant concentration in healthcare. Our original mission, based on my personal sobriety journey, was to invest in mental health startups. That led to opportunities to invest in healthcare more broadly over the years and we’ve done just that.

As we’ve had access to more capital, and built more relationships in the venture community I’ve wanted to expand into other verticals. One logical vertical for me is Defense and Industrial technology.

Why?

I’m a @WestPoint_USMA graduate for one, and I served in the Army as an infantry officer after college. After business school, I spent 7 years as an investment banker covering the Aerospace & Defense sector at @UBS , then at @jpmorgan in NYC. This experience and the relationships I built during those years have led to very interesting defense tech startup deal flow, and an ability to leverage my relationships to help those startups both with the DoD and with the Primes (who were my former clients as a banker).

In the last 6 months What If Ventures has invested in a handful of defense tech startups. These companies so far include @umbraspace , @FirehawkAero , Raven Space Systems, @AeonIndustrial and @samaraaero.

I believe that we are entering a new age in America and globally. The United States has seen a large portion of industrial manufacturing outsourced to other parts of the world. This manufacturing base is / was the cornerstone of our defense industrial base.

As manufacturing has moved offshore, we have put ourselves in a position to experience supply chain shortages all across the defense and industrial landscape. We are seeing shortages in munitions, machinery, weapons, supplies, fuel, and many other components. These shortages have been experienced while we simply supply our allies for their fights. Imagine where we would be if we were engaged in a full-scale conflict today.

The American government, the @DeptofDefense , and other agencies have made it a priority to foster American ingenuity to build new technologies, new capabilities and expand manufacturing capacity here in America to support dual-use missions. And we are going to invest heavily in this over the coming years.

By leveraging my military experience, the relationships I’ve built over many years and my working knowledge of the defense landscape, we will invest in the technologies and capabilities that bring about a new era of American readiness, dynamism and industrial defense capability.

Consensus investors literally cannot outperform the market.

Healthcare has been absolutely decimated in the public markets. Even more so in the private markets.

Now is the time to bet on the sector.

Latest analysis here:

https://t.co/kAndnZHB38

6 years sober today 🙏

I wrote an update on my recovery journey so far, and the building of @whatifventures to help find solutions for people like me:

https://t.co/YtvDz9H4gf

Healthcare is outperforming the S&P500.

Since early July, the $XLV and our Disruptive Healthcare Peer group are both outpacing the broader market.

The only thing that has outpaced them all is the drop in interest rates (also shown in this chart as the inverse of the 10-year).

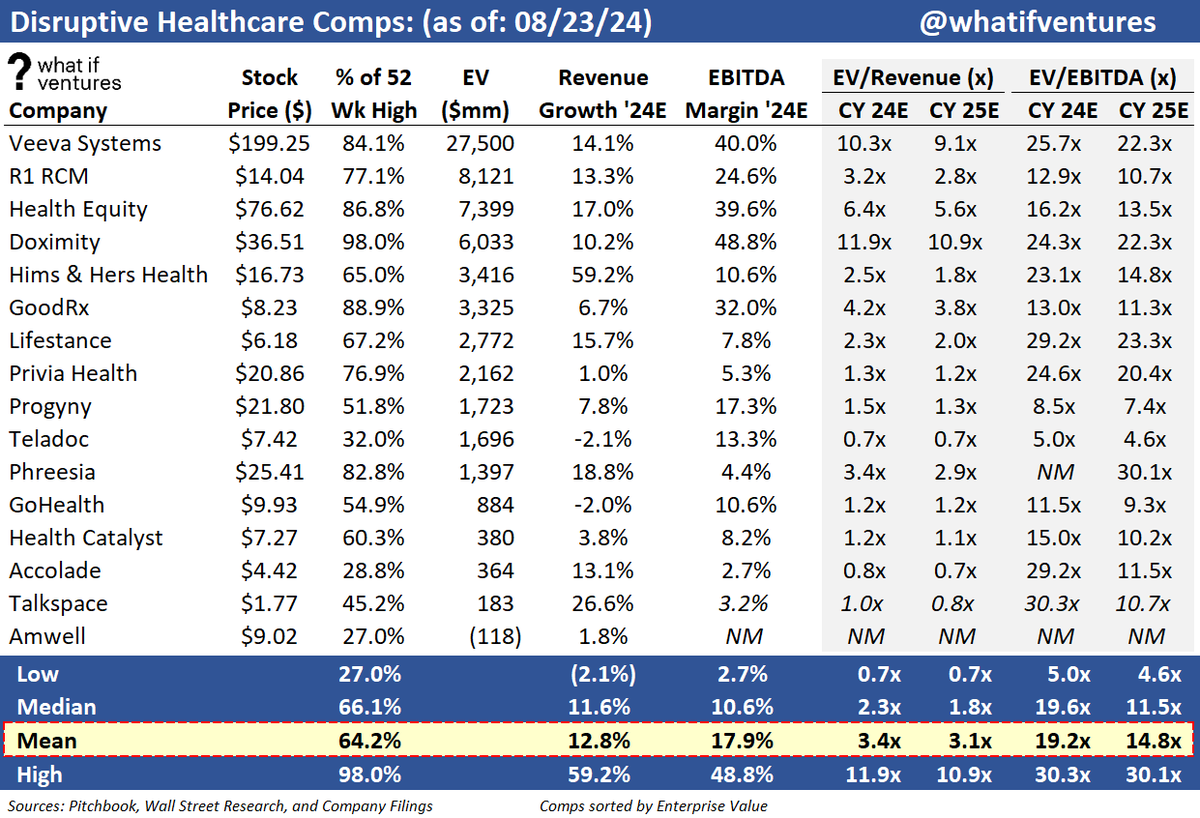

Disruptive Healthcare public companies traded well last week with valuations ticking upward as the group outperformed the broader market.

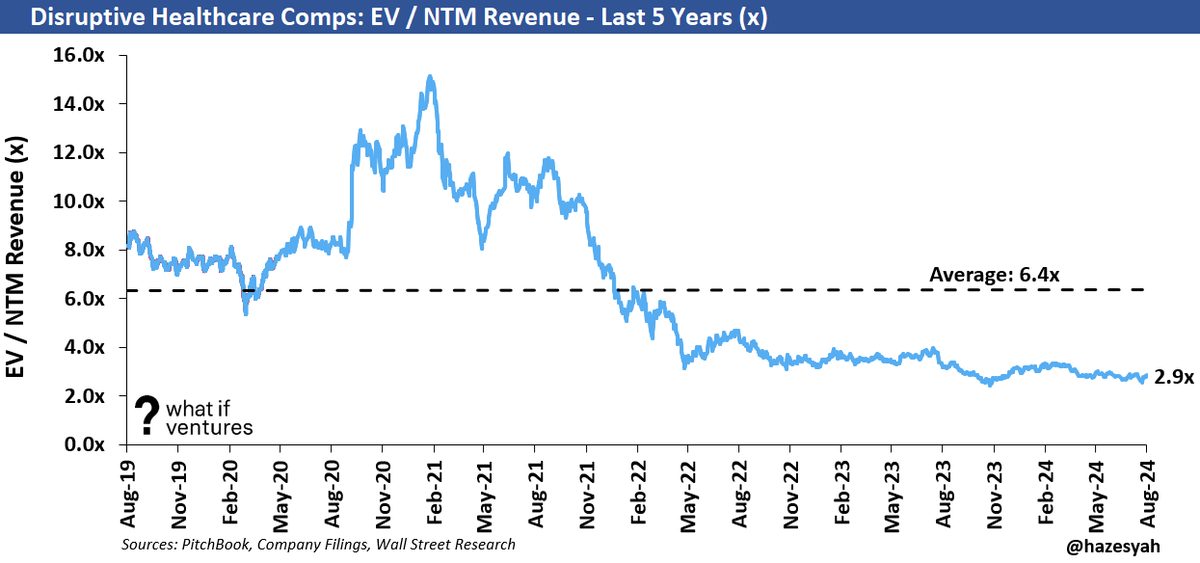

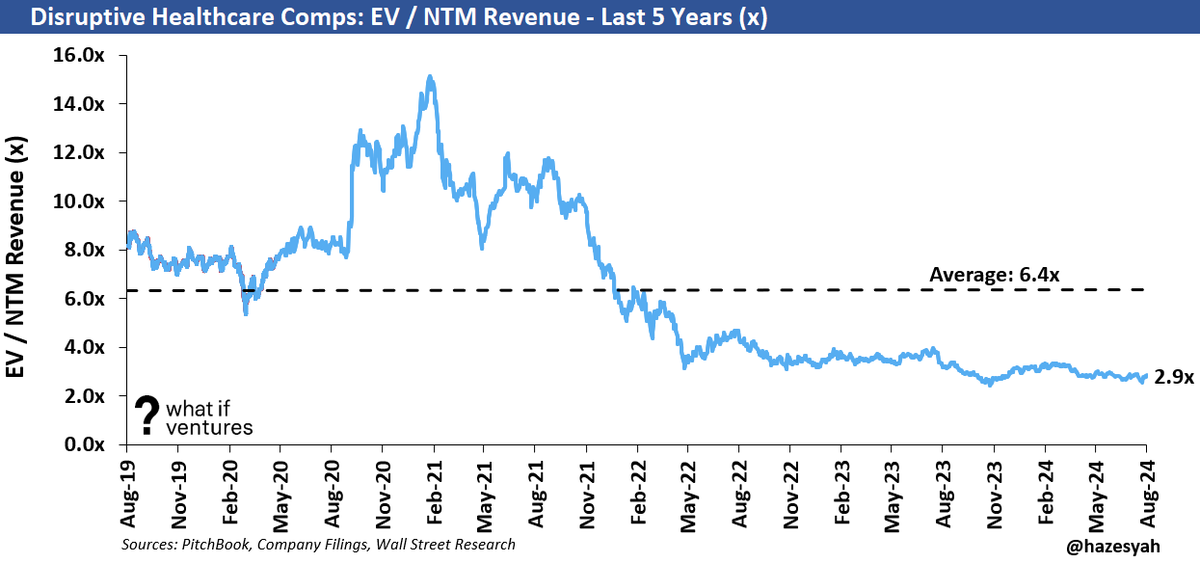

The broader group is trading 3.0x NTM Revenue.

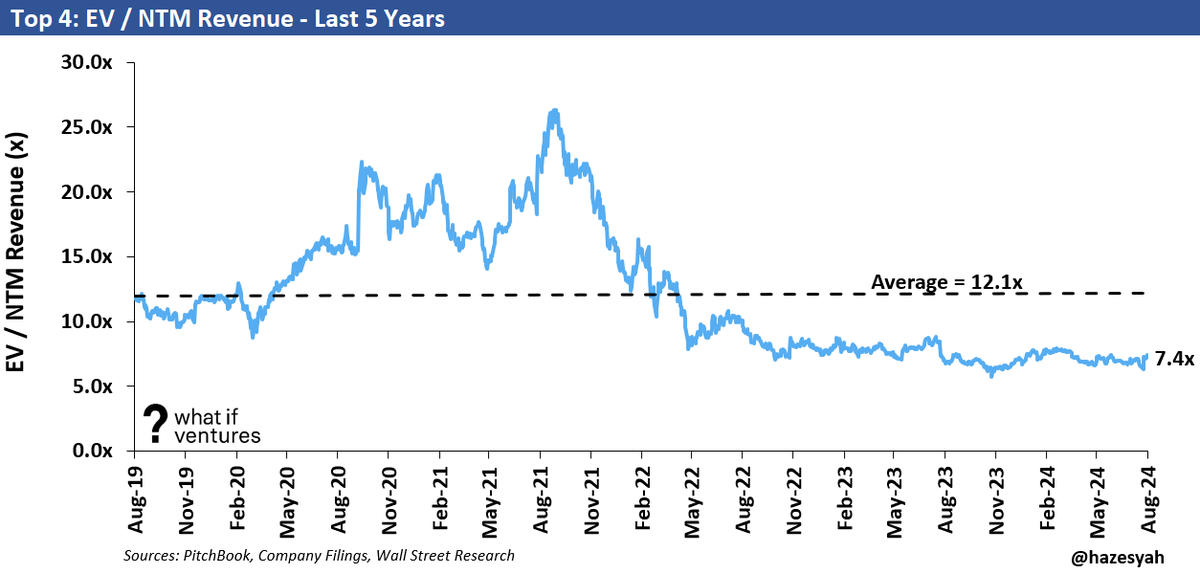

The top 4 names are trading 7.7x NTM Revenue.

EV / NTM Revenue for the top 4 names (high margin, high growth subset of the broader group). These names trade more like startups than any others in the space.

We attempt to understand correlation between macro trends and how healthcare companies trade in the public markets. This impacts how startup financing rounds are priced.

This chart by Goldman Sachs shows how the $XLV has performed relative to the S&P500 this year.

High growth, earlier stage public healthcare companies are trading at 3.3x 2024 revenue.

The top names in the group are trading at over 7x.

This data reads across to private market healthcare (startup) valuations (which are slightly higher than this range but not by much).

🚨Our preliminary #HLTHUSA 2024 agenda is out & it’s a game-changer!

Packed with the hottest topics in health tech, policy shifts, & dynamic debates, this is our BIGGEST and BOLDEST yet.

Take a look for yourself…https://t.co/XDziCaO2qA

See our top highlights 👇

Happy weekend! Excited I have pieces coming up for you all on:

— advanced primary care

— fintech/ HealthTech

— an OB-Gyn’s take on all the menopause startups in the market

It’ll be a fun fall!

Subscribe away :)

What are Healthcare startups worth today?

What valuation makes sense for current healthcare startup funding rounds?

One way to approach these questions as an investor, or startup founder is to look at where the small cap / disruptive healthcare public comps trade.

Over the last 5 years, the small cap disruptive public Healthcare peer group trades around 6.4x NTM revenue. For the sake of simplicity, you can compare NTM revenue to Annualized Runrate Revenue in a startup. Although it's not a perfect comparison, we're talking about comps here which isn't an exact science.

Today that same peer group is trading at 2.9x NTM Revenue. However, when we look at a subset of the group with the greatest growth and highest margins, we see a 5 year NTM revenue multiple average of 12.1x and a current multiple of 7.4x.

Interestingly enough, when I look at the range of ARR multiples I'm seeing in private funding rounds today, I'm seeing a range somewhere between 3x and 8x ARR on average. Yes, I've seen some higher and I've seen some lower multiples, but the vast majority seem to be falling into that range recently.

That range correlates with the end points of the broader group (on the low end) and the smaller higher growth ground (on the high end). Which makes sense.

If you want to see this kind of data on a regular basis, you can follow our Disruptive Healthcare newsletter for free. Today, there are over 4,200 subscribers that read it weekly.

You can find the newsletter here: https://t.co/UWfQdHZ6IV

What are Healthcare startups worth today?

What valuation makes sense for current healthcare startup funding rounds?

One way to approach these questions as an investor, or startup founder is to look at where the small cap / disruptive healthcare public comps trade.

Over the last 5 years, the small cap disruptive public Healthcare peer group trades around 6.4x NTM revenue. For the sake of simplicity, you can compare NTM revenue to Annualized Runrate Revenue in a startup. Although it's not a perfect comparison, we're talking about comps here which isn't an exact science.

Today that same peer group is trading at 2.9x NTM Revenue. However, when we look at a subset of the group with the greatest growth and highest margins, we see a 5 year NTM revenue multiple average of 12.1x and a current multiple of 7.4x.

Interestingly enough, when I look at the range of ARR multiples I'm seeing in private funding rounds today, I'm seeing a range somewhere between 3x and 8x ARR on average. Yes, I've seen some higher and I've seen some lower multiples, but the vast majority seem to be falling into that range recently. That range correlates with the end points of the broader group (on the low end) and the smaller higher growth ground (on the high end). Which makes sense.

If you want to see this kind of data on a regular basis, you can follow my Disruptive Healthcare newsletter for free. Today, there are over 4,200 subscribers that read it weekly. I say weekly, but to be honest, I don't get around to publishing it every single week, but I do my best.

You can find the newsletter here: https://t.co/0u0mrL8pOx

@whatifventures

Is it really already August? We've been very active investing so far this year at @whatifventures.

Through August '24, we have invested in 16 healthcare startups so far in 2024. We've deployed $8.8mm year to date in those deals.

Since inception in 2020, we have invested over $90mm into 78 healthcare startups. Our north star is mental health with the vast majority of our deployment in that sector. However, over the years, we have evolved to invest in healthcare and biotech broadly when we find the right opportunities.

We have deployed the $90mm out of our syndicate structure so far (on a deal by deal basis backed by over 4,000 Limited Partners). We recently launched our first traditional venture capital fund. Fund 1 will be a small $10mm fund focused on early stage mental and disruptive healthcare startups.

I'm excited about what I'm seeing in the market for mental health startups right now. Please reach out if you have questions about fundraising, valuation, capital markets, business models or any other startup related questions. We'd love to help in any way we can! The best way to reach out is through our website: https://t.co/xnA4kOBm8h

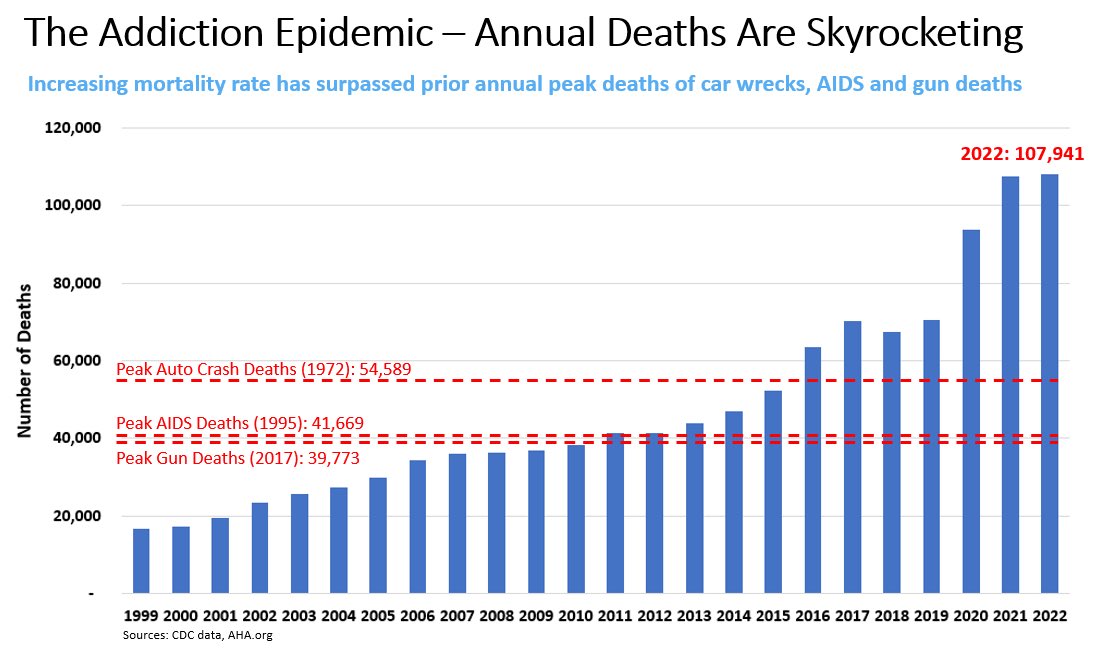

Addiction is the real epidemic. It’s killing more people than some of the most discussed public health crises of all time.

Addiction deaths surpass 100,000/year in consecutive years now.

What’s worse, it’s to blame for even more deaths than these stats show.