Prioritise economic freedom, technological innovation & digital privacy. Ex-entrepreneur. DeFi maxi. Nuclear & renewables for abundant low-cost energy for all.

This is a really interesting article but for me it highlights 2 very important errors in societal thinking:

"It's nobody's job to create jobs" - incorrect!!

It's everybody's job to create their own job.

This is the fundamental re-framing in society - it's why we've seen an explosion of entrepreneurialism not just in the traditional sense but also in solo owner-operator businesses like influencers and even OF girls.

As the tools get more widespread, the cost of adoption comes down and then AI makes them more powerful so the net result is that we can all express our commercial ambitions with much lower overhead (and therefore risk).

"It's technology enabling the rich to do their own work" - incorrect again!!

It's technology enabling us all to do our own work.

As above we have to get away from this absurd idea that capitalism (which is originally a Marxist and pejorative term for those who hoard capital to the detriment of the workers) is evil: we ALL have capital to some degree or other (financial, time, skills) and how we allocate that is up to us.

At its most fundamental AI is reducing the amount of capital needed to start or grow your business - this is inherently better for workers than capital holders because it actually erodes the competitive advantage that existed in the status quo ante - the cost to play the game has fallen, more people will play, more will succeed because the unfair moat of having the capital is eroded.

We have to reframe in this manner to enable people to see a brighter future for themselves rather than a diminished and dependent one, which is what UBI suggests.

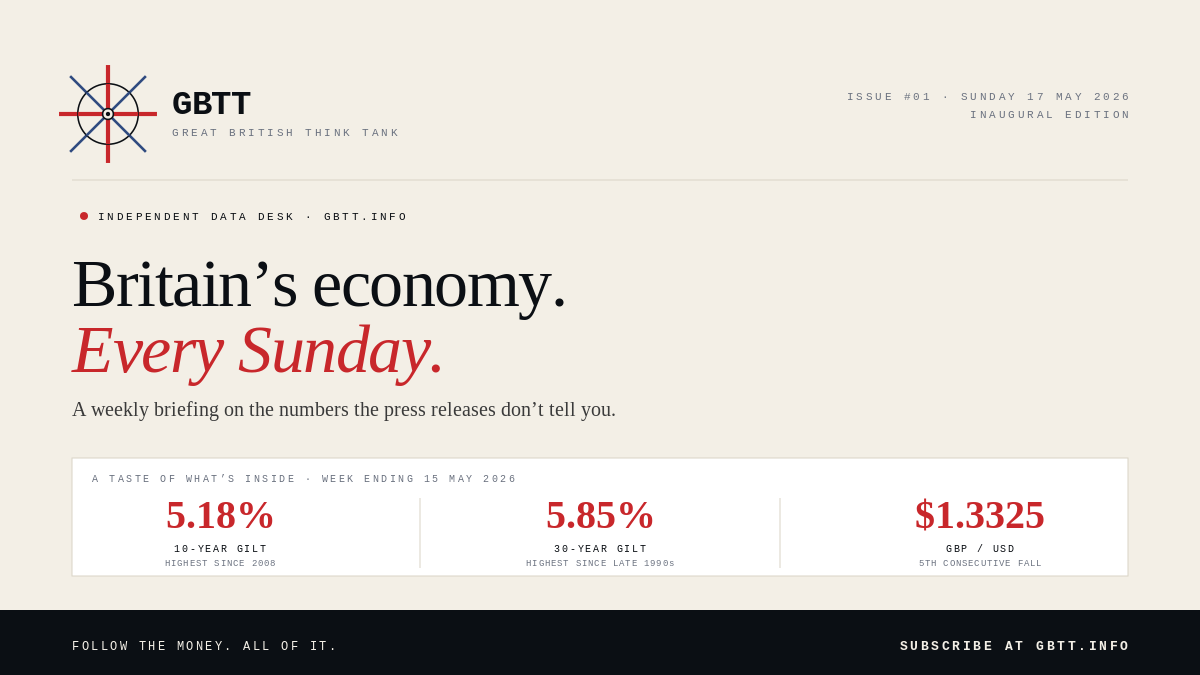

Britain's economy. Every Sunday.

Data, not vibes.

Issue #01 lands tomorrow. Last chance to subscribe before launch.

A taste of what's inside:

✅10-year gilt 5.18% — highest since 2008

✅30-year 5.85% — highest since the late 1990s

✅Sterling: 5th straight fall

https://t.co/3nhwacbRVM

Britain's minimum wage is today set at 61.1% of the median wage of a full-time worker. This is one of the highest levels in the OECD. Only Colombia (92.3%), Costa Rica (87.1%), Chile (74.6%), Mexico (73.7%), New Zealand (68.7%) and France (62.5%) sit higher on the same measure.

In Australia, the equivalent figure is 53.9%. In Germany, 50.6%. In the Netherlands, 48.3%. In the United States, 25%. The Nordics don't have statutory minimum wages at all.

What, then, is the basis for the belief that raising the minimum wage even higher and compressing labour income in Britain still further is a good idea? The National Minimum Wage was introduced in 1999 and has consistently grown faster than both earnings and consumer prices. When it was introduced in April 1999, it was set at £3.60 per hour. In inflation adjusted-terms, that would be some £7 per hour today. Some 45% lower than the £12.71 National Living Wage for 2026.

Returning to the relative-wage measure, in 2000, the British minimum wage stood at 41% of the country's median wage. Meaning that from the year 2000 to 2024, the minimum wage increased by more than 20 percentage points relative to market wages. In Australia and the Netherlands, by comparison, the minimum fell by over 4 points versus the median wage over the same period. In the United States, by 11.

Notably, when the Labour Party left power in 2010, the figure for Britain was 46%. The bulk of the increase has occurred since the adoption of the "National Living Wage" policy in 2015, when it stood at 48.7%.

In absolute terms, the British minimum wage in 2000 was equivalent, in purchasing power parity-adjusted dollars, to the minimum wage in the United States. Today it's double. In 2000, it was 33% lower than the minimum wage in Netherlands, today it's higher. The same is true for Belgium. It's now 50% higher than Korea's or Japan's.

Yet, since 2008, British productivity growth has been abysmal. The idea of productivity forcing (that expensive labour forces businesses to invest in automation and capital) has empirically failed in the UK. (It's also worth asking how a continuously increasing minimum wage interacts with the increase in the labour wedge from the recent hike in National Insurance contributions.)

With respect to public spending and taxation, from 1996 to 2001, the British state was spending some 35.1% of GDP on average and raising 34.7% of GDP in revenues. Public sector net debt was brought below 30% of GDP. Today, by contrast, the British state is spending 44.6% of GDP, raising 40.3% in revenues, and public sector net debt is equivalent to 93.8% of GDP.

So public expenditure has increased by some 10% of GDP, with the increase funded by a mixture of higher taxation (around 5.5% of GDP) and borrowing (some 4.5%). Over the coming years, government revenues are forecast to rise to the highest levels since the 1940s. Spending is already the highest in Britain's peacetime history.

Britain has, over this period, gone from being a relatively low-spend, light-tax model relative to its peers, closer to Australia, Japan, Switzerland, or the United States, to one that spends more than the OECD average (42.6% of GDP in 2023).

What is the basis for the belief that the next increase in spending, taxation and borrowing will succeed where the last 10 percentage-point increase in the size of the state did not?

In reality, both policies (increasing the minimum wage and higher public spending) are acting here as self-validating moral commitments rather than instruments whose effectiveness is an empirical matter to be analysed and evaluated. A higher minimum wage may produce better outcomes under some labour market structures and worse under others. It also depends, critically, on where you start. At 41% of the median wage, the case was perhaps plausible. At 61%, it is not. Similarly, public spending may raise long-run supply potential when directed toward productive uses in a supportive institutional environment; when it is not, it simply dissipates as input cost inflation.

Britain's productivity failure since 2008 is a serious problem that has attracted serious analytical work. On planning and land use restrictions, on the collapse of business dynamism, on resource misallocation. Ms. Rayner treats the symptoms of Britain’s productivity failure —stagnant living standards, weak wages, and high costs— as evidence that more of the same is needed.

But shifting an ever larger portion of the economy into the public sector, which has shown no net productivity growth since the mid 1990s and where productivity remains markedly lower than it was pre-COVID is not a recipe for improving aggregate performance. The burden therefore falls on those, like Ms. Rayner, who claim that the continued, relentless application of such demand-side, redistributive tools has any prospect of solving what are, fundamentally, long-standing structural problems with the supply side of the British economy.

Good intentions are not enough here. Results are what matter. A party, or a politician, that does not distinguish between the two is not fit to govern.

My totally outrageous and not at all serious 10 point plan to save Britain.

1) The entire Labour government does the honourable thing and resigns on the basis that remaining in office merely guarantees it will preside over the eventual loss of economic control.

2) Officially acknowledges that, without IMF backing and access to dollar liquidity, Britain’s current economic model is structurally unsustainable — particularly for a country whose comparative advantage is supposedly financial credibility.

3) Establishes a government of national unity in which day-to-day economic management is handed to industry-backed technocrats and entrepreneurs under a four-year “rebuild or bust” mandate.

4) Pegs sterling to the dollar in order to restore monetary credibility and halt the slow transformation of Britain into an upper-middle-income crisis economy. [Alternatively removes all barriers to USD stablecoins and allows explicit dollarisation that way.]

5) Slashes corporate taxes, accelerates planning reform, and dismantles layers of administrative and regulatory drag in an emergency bid to revive productivity and private investment.

6) Restricts full NHS eligibility to citizens and settled residents, with everyone else moved onto a contributory or fee-based system outside emergency treatment.

7) Realigns British industrial, defence and trade policy explicitly around American strategic priorities in exchange for preferential access to US capital, markets and dollar funding.

8) Offers Washington broad regulatory and geopolitical alignment — including on technology, energy and security policy — in return for expedited customs access and a de facto economic stabilisation umbrella.

9) Reopens the North Sea at full scale, removes remaining extraction constraints, and adopts the official position that “drill, baby, drill” is now a matter of national solvency.

10) Cancels the Diego Garcia deal immediately on the grounds that no country negotiating for IMF support should be voluntarily reducing its strategic collateral.

The other option is all of the above but joins the eurosystem or China instead.

My totally outrageous and not at all serious 10 point plan to save Britain.

1) The entire Labour government does the honourable thing and resigns on the basis that remaining in office merely guarantees it will preside over the eventual loss of economic control.

2) Officially acknowledges that, without IMF backing and access to dollar liquidity, Britain’s current economic model is structurally unsustainable — particularly for a country whose comparative advantage is supposedly financial credibility.

3) Establishes a government of national unity in which day-to-day economic management is handed to industry-backed technocrats and entrepreneurs under a four-year “rebuild or bust” mandate.

4) Pegs sterling to the dollar in order to restore monetary credibility and halt the slow transformation of Britain into an upper-middle-income crisis economy. [Alternatively removes all barriers to USD stablecoins and allows explicit dollarisation that way.]

5) Slashes corporate taxes, accelerates planning reform, and dismantles layers of administrative and regulatory drag in an emergency bid to revive productivity and private investment.

6) Restricts full NHS eligibility to citizens and settled residents, with everyone else moved onto a contributory or fee-based system outside emergency treatment.

7) Realigns British industrial, defence and trade policy explicitly around American strategic priorities in exchange for preferential access to US capital, markets and dollar funding.

8) Offers Washington broad regulatory and geopolitical alignment — including on technology, energy and security policy — in return for expedited customs access and a de facto economic stabilisation umbrella.

9) Reopens the North Sea at full scale, removes remaining extraction constraints, and adopts the official position that “drill, baby, drill” is now a matter of national solvency.

10) Cancels the Diego Garcia deal immediately on the grounds that no country negotiating for IMF support should be voluntarily reducing its strategic collateral.

The other option is all of the above but joins the eurosystem or China instead.

Oh Stephen, 5,000? Really?!

To quote Grok “Modern world-class AI data centres typically house 100,000 to over 500,000 GPUs in a single cluster, with leading hyperscale facilities pushing toward or beyond 1 million GPUs as gigawatt-scale builds accelerate.”

But sure, the UK’s sovereign intelligence is assured with our Brizzle cluster. 👍

Economically illiterate: why does further social spending promote social cohesion? And who foots the bill for this social spending?

Either it’s the already historically over-burdened tax base or it’s the bond market. Neither fancies that.

Or, of course, you print money, MMT-style. And watch the resulting debasement drive CPI and asset-inflation which dramatically worsens wealth inequality.

I dare you to debate me - but I suspect you can’t, because you don’t even understand what I’ve written, despite its simplicity.

This is deeply, deeply wrong - a working person who generates £250,000 of tax for "National Insurance" (an Orwellian term in its misdirection, I feel) ends up significantly worse off than a free-loader who never generated any NI contributions at all.

Read the whole thread. THIS. MUST. STOP.

£100,000 in. £3.30 out.

A working life of National Insurance contributions buys you, at retirement, £3.30 a week extra over the person who never paid in.

Less than a latte.

The contributory state pension is dead. Almost nobody is told. 🧵

£100,000 in. £3.30 out.

A working life of National Insurance contributions buys you, at retirement, £3.30 a week extra over the person who never paid in.

Less than a latte.

The contributory state pension is dead. Almost nobody is told. 🧵

It's fairly clear that the EU, the UK and potentially even some US states are soon going to attempt to ban VPNs.

These efforts will of course fail, but you might want to make sure you already have one installed on your devices ahead of time - @mullvadnet, @nym and @ProtonVPN are all decent options (DYOR).

Finally, as a fallback, you may want to look into eventually running your own VPN, if there is a real app store clamp down. A useful technical guide is in the thread, and you may want to bookmark this for later.

Hopefully you won't ever need it, but it's here just in case.

🇪🇺 Die EU baut die Mauer weiter!

Dein Vater schiebt dir 12.000 Euro in bar über den Küchentisch. Kaution für die neue Wohnung. Über Jahre gespart. 50er-Scheine. Er reicht sie dir, du nimmst sie entgegen. Ein normaler Vorgang. Generationen haben das so gemacht. Vater an Sohn, Geld in die Hand.

Ab dem 10. Juli 2027 ist genau dieser Moment illegal, sobald das Geld zur Wohnung weiterwandert. Nicht weil du etwas falsch machst. Sondern weil Brüssel entschieden hat, dass es das nicht mehr geben soll.

Ich hab mir die letzten 18 Monate angeschaut. Vier Verordnungen. Ein Muster.

Sommer 2024. Die AML-Verordnung 2024/1624 wird verabschiedet. Bargeldobergrenze 10.000 Euro. Ab 3.000 Euro Identifizierungspflicht beim Händler. Strafen bis 40 Prozent der Summe. Scharf gestellt am 10. Juli 2027. Privatpersonen-Bargeld zwischen Familie und Freunden bleibt erlaubt. Aber der Moment, in dem Geld in den Wirtschaftskreislauf eintritt - Auto, Wohnung, Schmuck, Goldhändler - ist erfasst, dokumentiert, zentralisiert.

April 2025. Die EU-Kommission startet "Going Dark", später umbenannt in "ProtectEU". Im Juni 2025 folgt der Fahrplan. Sommer 2026 soll die Gesetzgebung kommen, die VPN-Anbieter zwingt, Daten zu speichern. No-Log-VPNs werden in Europa illegal. Mullvad hat im Dezember 2025 öffentlich angekündigt: Wenn das durchkommt, verlassen sie den EU-Markt. Anonyme Internetnutzung - abgeschafft.

Frühjahr 2026. Die Chatkontrolle wird offiziell entschärft. Schlagzeile in jeder Zeitung: "EU stoppt Massenüberwachung." Die Wahrheit im Kleingedruckten: Die "freiwillige" Scan-Erlaubnis für Anbieter läuft weiter, zweite Verlängerung gerade durch. Patrick Breyer warnt seit Jahren: Was als "freiwillig" verkauft wird, wird zur Pflicht, sobald die Infrastruktur steht. Die Infrastruktur steht. Niemand spricht mehr drüber. Genau das war der Sinn der Verzögerung.

Juli 2026. MiCA-Stufe-2 wird vollständig wirksam. Jede Krypto-Plattform in der EU braucht eine CASP-Lizenz. Travel Rule scharf, Name, Adresse, Geburtsdatum bei jedem Transfer ab 1.000 Euro. Stablecoins wie USDT sind in der EU regulatorisch erledigt. Nicht weil der Markt das wollte, sondern weil Brüssel keine Konkurrenz für den digitalen Euro duldet, der parallel im Anflug ist.

Ende 2026. EU-weite Altersverifikation in allen 27 Mitgliedstaaten. Pseudonymität im Internet - Geschichte. Wer was kommentiert, wer was liest, wer was schaut. Alles an deinen Ausweis gebunden.

Schau dir das nochmal an.

Bargeld eingeschränkt. Krypto identifiziert. VPN ausgehebelt. Chats geöffnet. Internetzugang an deinen Personalausweis gekettet. Wer hat noch eine Hintertür übrig?

Niemand. Genau das ist der Plan.

Das ist kein Zufall. Vier Verordnungen, präzise hintereinander gelegt, jede für sich harmlos begründet, Geldwäsche, Kinderschutz, Sicherheit, Verbraucherschutz. Alle zusammen ein Käfig. Keine offene Debatte, keine Volksabstimmung, keine Notbremse. Du wirst nicht gefragt. Du wirst auch nicht gewarnt. Du wirst zugemauert, eine Verordnung nach der anderen.

Ich erzähl dir das, weil es niemand sonst zusammenhängend ausspricht. Die meisten Medien zeigen dir jeweils einen Stein und nennen ihn vernünftig. Ich zeig dir die Mauer.

18 Monate. Vier Verordnungen. Ein einziger Bauplan.

Das war der Plan. Du warst nur nicht der Bauherr. Ich war auch nicht eingeladen. Aber ich kann lesen. Und du kannst es jetzt auch.

Yes, but worth noting that a USD stablecoin doesn’t have to be US backed unless it wants to be GENIUS compliant. There is a Hong Kong $ stablecoin that is effectively pegged to the USD (the HK $ has been pegged at ~7.5:1 for decades) but is backed by Chinese gov assets.

Point being that that if you use USD GENIUS-compliant stablecoins then they keep you within the political purview of the US gov.

But many countries don’t want that risk and can use other stablecoins that are effectively USD but sit outside of all US financial rails.

Therefore, $ stablecoin use does not necessitate UST demand dollar for dollar.

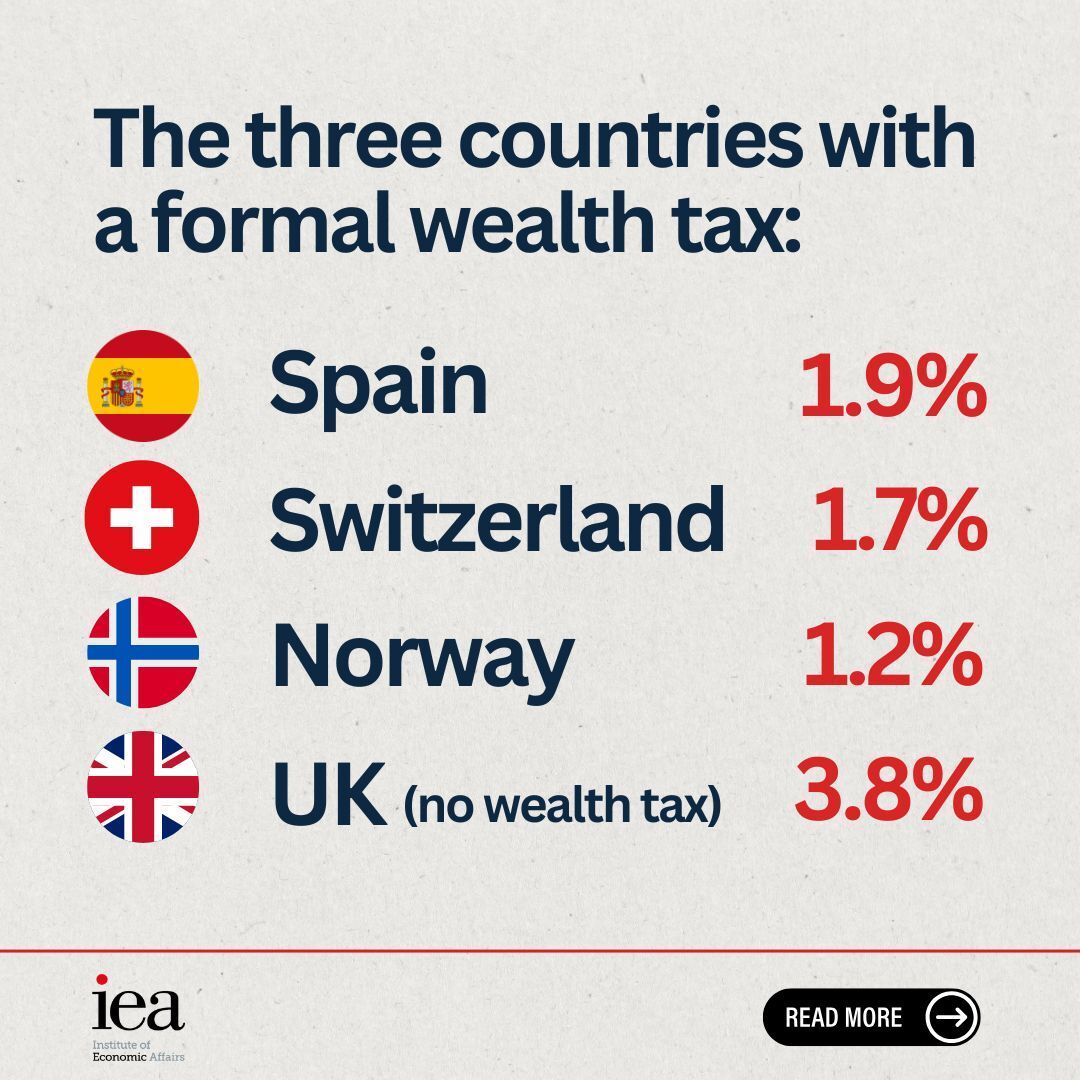

🇪🇸 Spain has a wealth tax. It raises 1.9% of GDP from wealth-related taxes.

🇨🇭Switzerland has a wealth tax. It raises 1.7%.

🇳🇴 Norway has a wealth tax. It raises 1.2%.

🇬🇧 The UK has no wealth tax. It raises 3.8%.

The argument that we don't tax wealth doesn't hold up.

🇬🇧 Britain has no wealth tax. Yet it raises more tax from wealth than every country that does - Spain, Switzerland and Norway - and every other OECD nation.

We shouldn't be looking for more ways to tax wealth.

We should be looking at more ways to create it.👇️