LIVE:Ghana Publishing Company Limited has seen a jump in profit, rising to GH¢16.9 million in 2025 from GH¢2.2 million in 2024

https://t.co/yMtI5lbVuQ

#BeyondTheNumbers | #JoyNews

ANA'S COCOA SECTOR

Winston Tackie joins Arise News Global Business Report to discuss Ghana’s planned $1 billion cocoa bond programme aimed at funding cocoa purchases locally, reducing reliance on foreign loans, and reforming the country’s cocoa financing and pricing system.

1. I promised to do an essay with a bit more meat than my earlier post on Bank of Ghana’s recent bombshell. Here goes. Since it was rushed, if you see a typo or data glitch, please forgive.

2. For those totally clued out, this is about Ghana’s central bank doing some accounting magic to blunt the force of alarmingly large losses arising from its otherwise impressive exchange rate and inflation gains of the last year.

3. In 2025, reserves climbed to about $13.8bn, inflation returned to target, and the cedi staged a spectacular comeback. After two years of turbulence.

4. The governor got a spring in his step and the Finance Minister ordered a new suit with specially inflated shoulder pads.

5. Whilst the gains have been real, the machine that has been delivering this economy-cooling love has been running hot. Red steaming hot!

5. Bank of Ghana (BoG) created cedis to buy gold, converted the gold into dollars, then borrowed a lot of the cedis back through OMO bills to stop inflation. And did a boogie round the block.

5. Call it macroeconomic judo: beautiful when it all comes together, dangerous when the mat starts slipping.

6. The price tag of the show ticket is brutal.

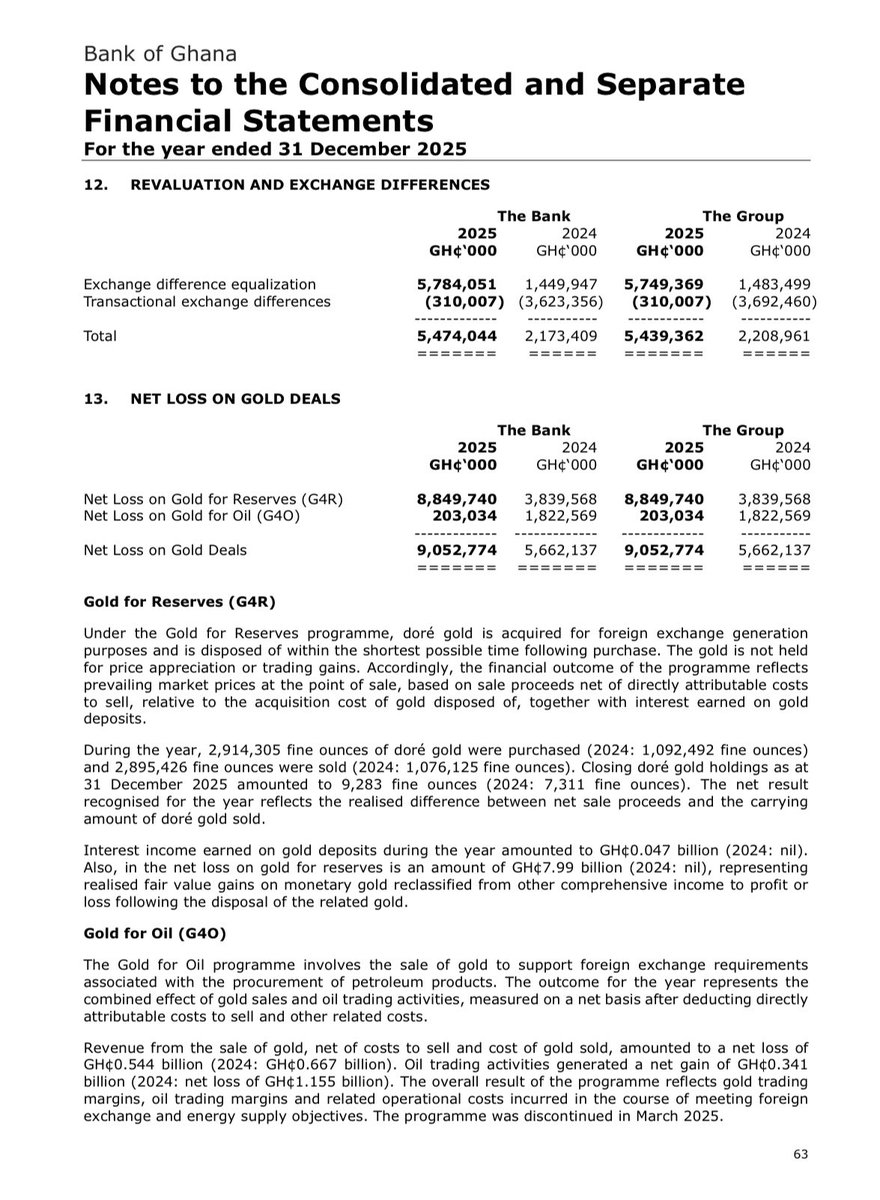

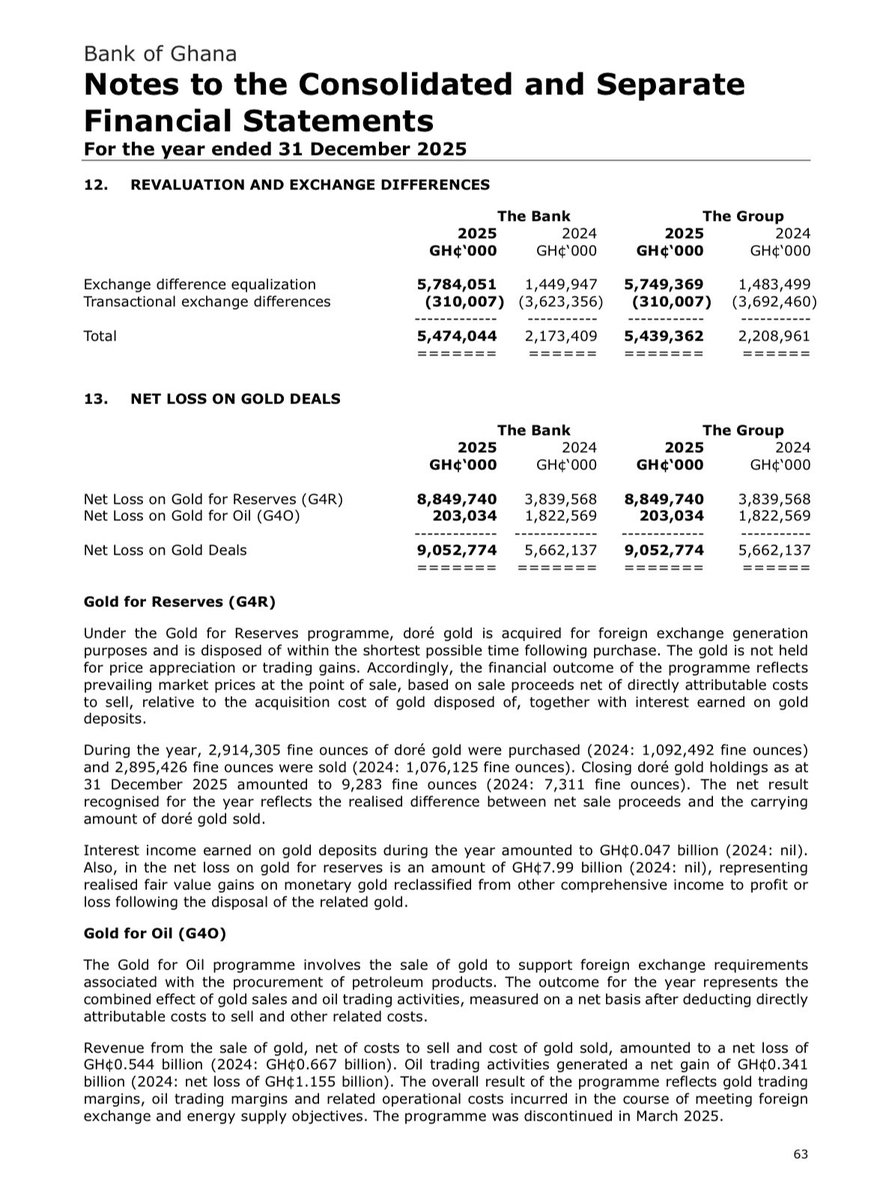

7. BoG lost about $1.25bn in 2025, while wider comprehensive losses pushed the damage toward $2.8bn.

8. Its negative equity is now around $9bn. Because BoG is a central bank, nobody serious is writing an obituary. This is not the case of the Bank of the city-government of Amsterdam in the 18th Century.

9. But that doesn't mean that the losses are a footnote either. The "negative equity" number (pegged to GDP size) is among the highest the world has ever seen. One may still wonder: "can a central bank become technically insolvent?"

10. It can. Even if it doesn't keel over like the Bank of Amsterdam.

11. A more relevant question is whether BoG can keep paying for monetary stability without leaning on one-off tricks, opaque gold channels, and future Treasury rescue.

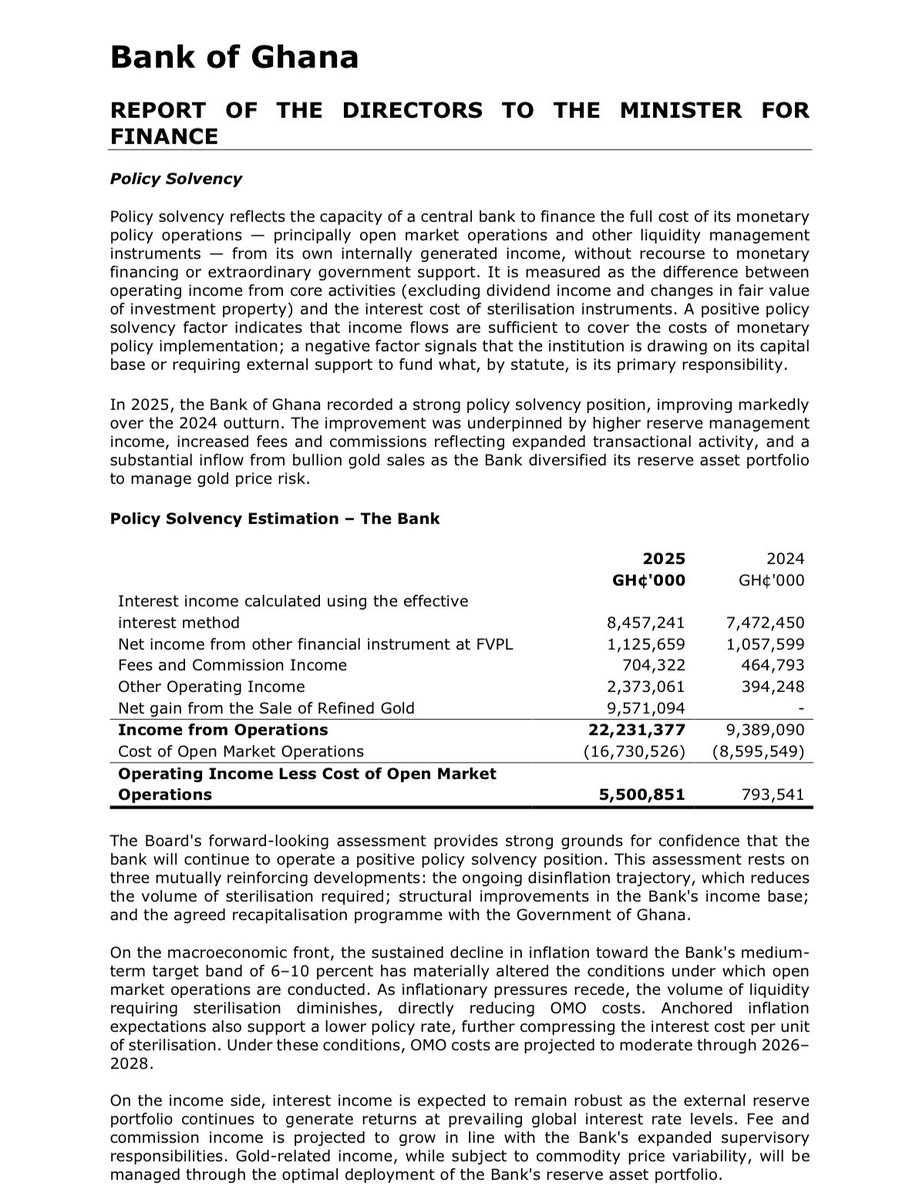

12. Strip out the big gold-sale gain and the celebrated policy-solvency surplus it has posted turns into a recurring deficit.

13. Meanwhile, nearly $9bn in OMO bills sits like a dammed-up river: fine if contained, dangerously inflationary if the wall cracks.

14. The gold programme has bought Ghana confidence, reserves, and breathing room.

15. It has also created a sterilisation treadmill where each victory needs another expensive victory just to keep going.

16. So yes, citizens should care.

17. It is actually in the middle of calm that one must prepare for the storm.

18. Except, of course, that in a katanomic democracy [], finding a sizable enough audience to care enough about Policy over Politics can be like hunting for cheap waakye in East Legon.

Read more here:

https://t.co/SptaZhnp9O

The Bank of Ghana reported a loss of 8.8 billion cedis from its Gold for Reserves program, which is largely implemented by the Goldbod. That’s more than double the $214 million reported by the IMF, which covered up to the third quarter of 2025.

The government has disbursed 4.5 billion cedis to the Goldbod for trading. It’s not difficult to see how that capital could be quickly depleted under the current operating model. That’s why some of us keep focusing on the model itself.

It’s not just about buying gold and bringing in foreign exchange. In the past, emphasis has been placed on how much forex is generated, but the cost at which it is obtained and the impact on trading capital and the BoG’s books are equally important.

The challenge remains how to purchase gold from small-scale miners at a discount sufficient to cover trading and related costs without depleting capital while also reducing a loss in volumes. Timing also matters, as does enforcement to reduce smuggling. There is still a lot of work to be done. If we rush to declare success prematurely while losses are being incurred, the hard work will not get done.

If the state cannot #StopGalamseyNow, it should not also be buying galamsey gold, recording losses, and then needing to recapitalize the Bank of Ghana and the Goldbod as a result.

Ghana’s economy has made significant progress over the last 16 months. Inflation is down, the cedi is stronger and lending rates have declined. For millions of Ghanaians, that is real and it matters.

But two things can be true at once.

The institution helping to deliver these outcomes is also under serious financial strain. The Bank of Ghana owes more than it owns by 96 billion cedis, a gap that grew by 35 billion cedis just last year alone.

To keep inflation down, the Bank borrows from commercial banks to remove excess cedis from circulation. The interest cost of that borrowing reached 16.7 billion cedis last year, the single largest expense on the Bank’s books.

The next largest expense on the Bank’s books was losses from its gold deals. On the gold for reserves program, managed through the Goldbod last year, the Bank lost 8.8 billion cedis. So while Goldbod is celebrated for making over 900 million cedis surplus, the Bank’s books are taking a big hit.

The Bank says it remains policy solvent, meaning it can fund its monetary policy operations without going to the government or other sources for help. But that was only possible because it sold physical gold reserves (the gold sale was a controversial discussion point for a while). Strip those sales out and it would have been policy insolvent on its core operations.

The government has committed to recapitalise the Bank of Ghana between 2026 and 2032. That money comes from the national budget, which means resources meant for schools, hospitals and social programs may be diverted to fix the central bank’s balance sheet.

These are not abstract accounting losses. They are real losses that Ghanaian taxpayers will eventually pay for.

The macroeconomic gains are genuine. The losses are also real. The deteriorating situation of the central bank is also real. All deserve to be part of the conversation.

Free online UNDP Courses and Training opportunities are open to everyone ♻️

The United Nations Development Programme (UNDP) offers free, high-impact online courses designed to help you build skills for real-world global challenges.

What you’ll learn: Climate Action and Sustainability, Biodiversity Finance, Human Rights and Governance. Digital and Future Skills.

Why this support: In today’s rapidly changing world, these are not optional skills, they are essential for career growth and global impact.

Whether you’re a student, researcher, entrepreneur, or professional, this is your opportunity to learn from a leading global institution.

UNDP Apply Platform: https://t.co/Q1gacv8IY2

UNDP Course Catalogue (programs): https://t.co/BPEpxEXzI4

Formez-vous, le futur n’attend pas

The International Monetary Funds offers dozens of free courses taught by IMF economists, accessible globally through its online learning system.

https://t.co/s3kjyQrT2A

1. The Ghana Accelerated National Reserve Accumulation Policy (GANRAP) can help transform Ghana from a country that struggles during crises into one that weathers the storm. The ongoing US–Israel–Iran war (and other ongoing geopolitical uncertainties) is exactly the kind of shock GANRAP is designed to insure against. Uncertainty has become the norm of the day, but developing economies, through cleverly designed policies, can partially weather the storm.

2. In this empirical analysis by Dr. Stephen Lartey [University of Sussex] and I, we highlight the following:

3. Without GANRAP: At 5.7 months of cover and oil at $100/bbl, Ghana’s reserves decline but are not exhausted. With a current account surplus of US$756m/mo and gold co-movement, import cover actually increases even without GANRAP. Risk remains only if gold co-movement breaks down.

4. With GANRAP: At 15+ months of cover — held in gold that appreciates during crisis — Ghana’s reserves grow. Import cover reaches set benchmarks by year two, reflecting gold price appreciation (+9.1%) and incremental ASM formalisation. GANRAP FX generation rises to more than US$28 billion (median estimated) at crisis prices — more than offsetting the US$1.99bn oil shock. Inflation stays within 5%-7% band.

Access full analysis @ https://t.co/uWazSm78cj

NB: Views our own.

Where is capital going as interest rates plummet?

With treasury yields hitting single digits, institutional liquidity is pivoting to the GSE, fueling a 46.74% YTD rally

This rotation from fixed income to equities positions the GSE as a primary wealth creation engine in Ghana

It’s always great to join the Joy News Beyond the Numbers crew. I shared some thoughts on the state of the nation.

There is no doubt that the government has done well in stabilizing the macroeconomic environment. Indicators that affect people’s personal economies are all trending in the desired direction. However, we have seen periods of stability before. Those periods also largely relied on commodities. The real challenge is how we build on this stability and sustain the gains!

COCOBOD management takes a 20% pay cut. Senior staff accept 10%. Now pressure mounts for deeper restructuring — including possible staff rationalization.

I discussed with Winston Tackie what this means for COCOBOD’s future.

@JoyNewsOnTV@Joy997FM@winstontackie

🚀 THE MARKET IS MOVING

💰 Market capitalisation is rising, showing that the total value of listed companies is increasing.

💥 The Composite Index return is also up, indicating overall market growth.

#GhanaStockExchange

![mytheoz's tweet photo. 1. The Ghana Accelerated National Reserve Accumulation Policy (GANRAP) can help transform Ghana from a country that struggles during crises into one that weathers the storm. The ongoing US–Israel–Iran war (and other ongoing geopolitical uncertainties) is exactly the kind of shock GANRAP is designed to insure against. Uncertainty has become the norm of the day, but developing economies, through cleverly designed policies, can partially weather the storm.

2. In this empirical analysis by Dr. Stephen Lartey [University of Sussex] and I, we highlight the following:

3. Without GANRAP: At 5.7 months of cover and oil at $100/bbl, Ghana’s reserves decline but are not exhausted. With a current account surplus of US$756m/mo and gold co-movement, import cover actually increases even without GANRAP. Risk remains only if gold co-movement breaks down.

4. With GANRAP: At 15+ months of cover — held in gold that appreciates during crisis — Ghana’s reserves grow. Import cover reaches set benchmarks by year two, reflecting gold price appreciation (+9.1%) and incremental ASM formalisation. GANRAP FX generation rises to more than US$28 billion (median estimated) at crisis prices — more than offsetting the US$1.99bn oil shock. Inflation stays within 5%-7% band.

Access full analysis @ https://t.co/uWazSm78cj

NB: Views our own.](https://pbs.twimg.com/media/HCotyUFa8AA09v5.png)