Introducing Winus Financial AI Skills

Elite desks don't rewrite their analysis playbook every time the market moves. They build once and deploy everywhere.

Skills packages your exact methodology — backtesting, portfolio stress testing, cross-asset analysis across equities, bonds, options, FX, and commodities — into a 1-click workflow your whole team runs.

Built on 20 years of financial expertise. 100+ countries. 40+ financial roles.

Stop reprompting. Start systematizing.

#InvestmentEducation #TradeIdea

https://t.co/56EjuY3g80

🚨 Markets wanted a rate-cut signal.

Warsh said: not so fast.

At Sintra, the new Fed Chair pushed back on the market’s favorite playbook:

📌 No tolerance for inflation above 2%

📌 No clear rate path

📌 No forward guidance

📌 No more trading every Fed phrase as a policy signal

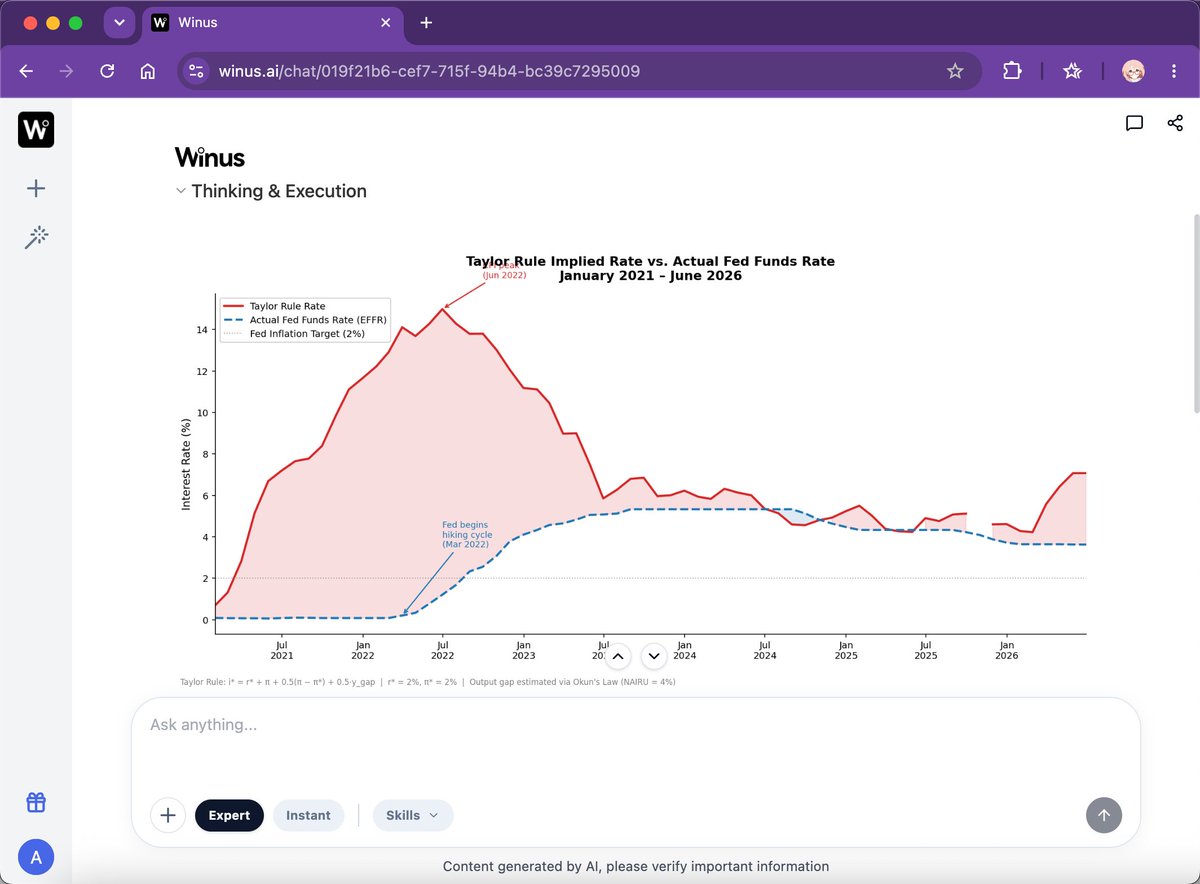

The Taylor Rule chart adds an important layer. 📊

Under multiple assumptions, the implied policy rate remains above the actual effective fed funds rate.

That does not mean the Fed must hike.

But it does mean “cut now” is not the obvious answer if you start from inflation, employment and rule-based policy pressure.

The key shift:

The Fed may stop feeding the market answers.

The market needs to rebuild its framework around data.

Track macro indicators, test Taylor Rule assumptions, and connect Fed signals with market reactions using Winus:

https://t.co/HtW6ZLYofE

#Fed #FederalReserve #Warsh #TaylorRule #Inflation #RateCuts #MacroResearch #Markets #Winus

Despite record FX interventions and a 31-year high interest rate, the Japanese Yen ($JPY) has officially become the world’s weakest major currency—down nearly 40% since 2022.

Why is Tokyo's billions-dollar defense failing against market forces?

A breakdown of the macro reality. 👇

The Gravity of a 345-bps Gap 📉 The Bank of Japan raised its policy rate to 1% (highest since 1995), but the Fed’s recent hawkish turn keeps the U.S.-Japan policy rate gap at a massive 345 basis points. With U.S. 10Y Treasuries yielding ~4.45% vs. JGBs at ~2.61%, the lucrative yen carry trade remains unstoppable. Investors borrow cheap yen to chase higher dollar yields.

The Liquidity Contradiction 🔄 The BOJ is trapped. While raising rates, it deferred bond-tapering to 2027, continuing to pump ~2 trillion yen monthly into the market. Why? To shield its staggering 1,343 trillion yen public debt from a systemic bond market collapse. This stealth liquidity effectively neutralizes its own rate hikes.

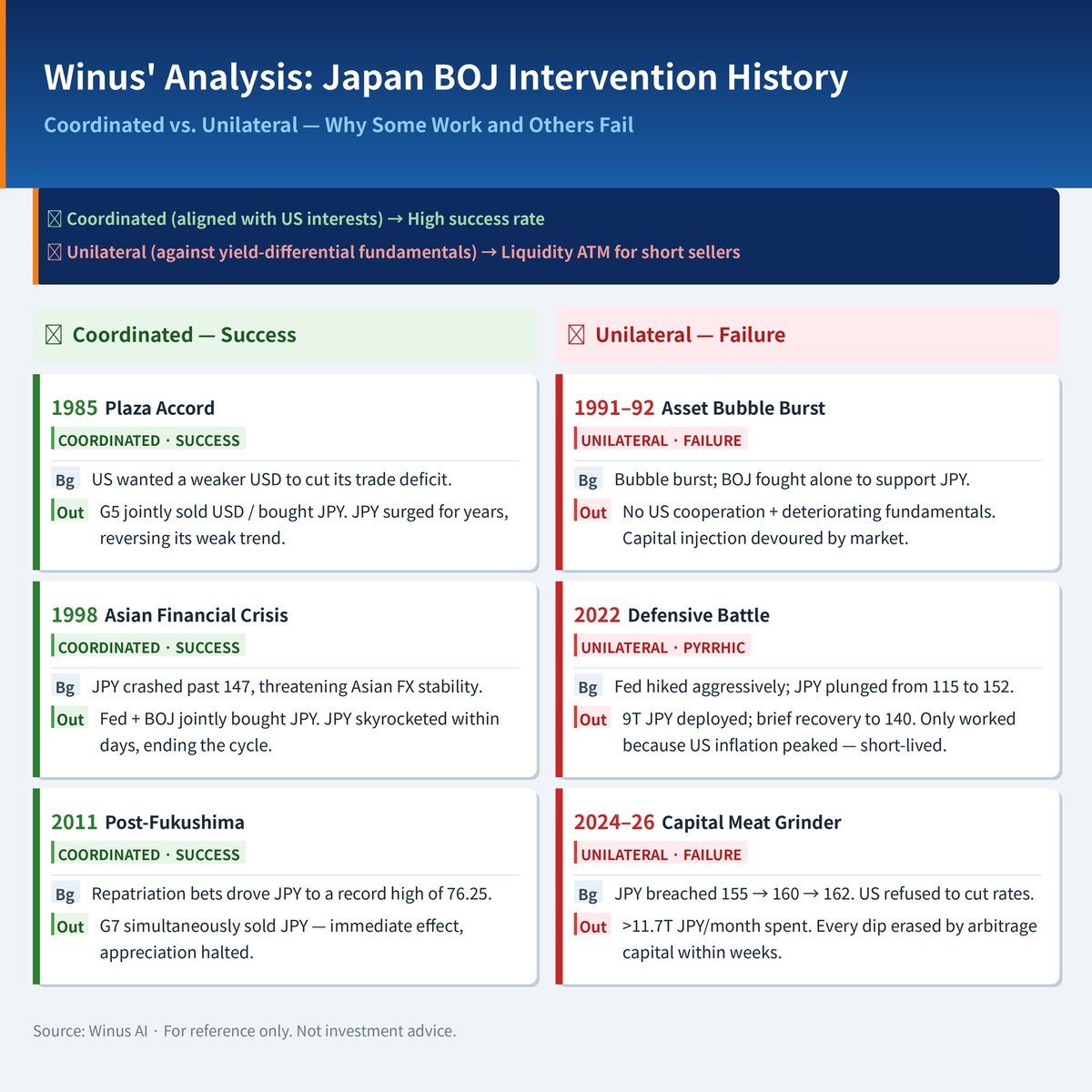

Only the Fed Can Save the Yen 🇺🇸🇯🇵 Data shows $JPY is down 3.9% against the greenback this year, but stable against the Euro. This is a story of broad dollar strength, not systemic yen abandonment. Unilateral Japanese intervention can only buy time; a true reversal requires either a Fed pivot or a 1985 Plaza Accord-style coordinated intervention—both highly unlikely in the near term.

The Bottom Line 🎯 Expect USD/JPY to consolidate in the 153–161 range for H2. Unilateral interventions are just speed bumps against macroeconomic laws.

Cut through the market noise. Access institutional-grade insights, historical FX intervention timelines, and deep macro analysis instantly with Winus AI.

👉 https://t.co/BDsiL57AY2

#FinancialAnalysis #FinTech #WinusAI #CarryTrade #FixedIncome $USD #CentralBanks #MonetaryPolicy #JGB #Forex #USDJPY #FederalReserve

@Meta may be turning its AI capex problem into a cloud business.

Bloomberg says Meta is exploring “Meta Compute”, meaning selling excess AI compute and model access to outside customers. $META shares jumped.

Bull case:

$META finally has a clearer ROI story for its $125–145B 2026 capex plan. If spare compute becomes revenue, AI infrastructure shifts from cost center to business line.

Winners:

$META — cloud could become a re-rating catalyst

$NVDA — more cloud providers = more GPU demand

$AVGO — custom chip partner

Power/data center names — capex supercycle beneficiaries

Losers:

$CRWV and $NBIS — customer may become competitor

AWS/Azure/Google Cloud — long-term competitive risk

$MU — near-term sentiment hit, though AI memory demand is still intact

The real question: is Meta becoming the 4th hyperscaler, or is this just a way to justify massive AI spending?

🚨 AI hardware just got hit hard — and now U.S. markets face an even bigger test.

The trigger was $META.

According to Sina Finance, $META is reportedly building an internal business code-named “Meta Compute,” aiming to sell unused AI compute capacity to external customers.

That would put $META in direct competition with $AMZN’s AWS, $MSFT Azure and $GOOGL Cloud.

The market reaction was brutal — and very telling. 👇

$META jumped more than 10% at one point and closed up 8.81%.

But upstream AI compute suppliers were crushed:

$CRWV and $NBIS plunged 14% to 17%, while the Philadelphia Semiconductor Index $SOX dropped nearly 6%.

The fear suddenly changed.

For months, the AI story was simple:

compute is never enough.

Now investors are asking a much more uncomfortable question:

What if too much compute gets built? ⚠️

At the same time, Kevin Warsh made the Fed message even tougher.

Speaking at the ECB’s annual central banking forum in Sintra, Portugal, Warsh again made clear that the Fed will not provide forward guidance on the future rate path.

Every meeting will be decided based on the latest data.

That makes this week’s U.S. jobs report much more important. 📊

Normally, nonfarm payrolls come out on Friday.

But because of the U.S. Independence Day holiday schedule, the June jobs report will be released earlier — at 8:30 a.m. ET on July 2.

Markets are already cautious.

$DJI futures slipped about 63 points, or 0.1%.

$SPX futures fell 0.1%.

$NDX futures were slightly lower.

Overnight, all three major U.S. indexes closed in the red.

The $DJI briefly rose more than 423 points and touched a record high, before giving back gains and closing below flat.

The $SPX fell 0.2%.

The $IXIC dropped 0.7%.

The clearest selling pressure came from AI hardware and chip names.

The VanEck Semiconductor ETF $SMH fell 5.4%, while $MU and $SNDK both dropped more than 10%. 📉

So the setup is clear:

Chip stocks are cooling.

The Fed is refusing to “spoil” the rate path.

And the jobs report now has extra weight.

Ned Davis Research strategist Rob Anderson sees rotation out of semiconductors as healthy.

But for short-term markets, the question is more immediate:

If payrolls come in strong again, will Treasury yields and the dollar keep pressure on risk appetite?

Winus analysis points to three lines to watch in the jobs report:

1️⃣ Are payroll gains still beating expectations?

2️⃣ Does the unemployment rate move lower?

3️⃣ Is wage growth picking up again?

Together, these will decide what the market trades next:

A resilient labor market —

or a Fed that has even less room to sound dovish. 🧠

#Winus #AI #Semiconductors #Meta #CoreWeave #Nebius #Fed #JobsReport #NFP #TreasuryYields #Dollar #Nasdaq #StockMarket #Investing

Is this a stock actually worth investing in?

$ASTS is building a satellite network that can connect directly to normal smartphones, no special hardware needed. The bull case is huge: 60+ carrier partners, including AT&T, Verizon and Vodafone, access to 3B+ potential subscribers, FCC approval, recent BlueBird launches, and ~$3.5B in cash to fund the rollout.

The bear case: the stock is already priced like the mission has worked. ASTS has a ~$33B market cap vs. just ~$71M FY2025 revenue, is still losing money, missed Q1 expectations badly, faces SpaceX/Amazon competition, and has major execution risk with every satellite launch.

Cramer calling it “speculative” is actually fair.

It is a high risk high reward stock

Here is what Winus AI had to say:

Hypothetically, if I had to pick one, I'd go with $SOFI (SoFi Technologies).

Here's my reasoning:

Why SOFI over the others:

Diversified business model: Unlike the others, SoFi isn't a one-trick pony — it spans lending, banking, investing, credit cards, and insurance. That gives it multiple revenue levers and some built-in resilience.

Bank charter advantage: SoFi actually holds a national bank charter, which gives it a structural cost-of-funding advantage over fintech peers. This isn't just a "growth story" — there's a real moat forming.

Path to profitability: SoFi has been delivering on GAAP profitability, which matters in a higher-for-longer rate environment. The market is less forgiving of "growth at any cost" these days.

Why not the others:

HOOD: Great platform, but heavily dependent on crypto trading volumes and retail engagement cycles. Revenue is lumpy and sentiment-driven.

ASTS: This is essentially a binary bet on satellite-to-phone technology working at scale. Massive upside if it works, but the technical and regulatory risk is enormous. Not where I'd put my only $10,000.

HIMS: Solid execution, but the GLP-1 compounding pharmacy model faces regulatory uncertainty. If the FDA eventually declares the shortage over, a big chunk of their growth engine could be at risk.

Bottom line: SOFI offers the best balance of growth potential and downside protection among the four. It's not the highest-upside pick (that's probably ASTS), but in a hypothetical "all in" scenario, I'd rather own the one with the widest moat and most durable earnings trajectory.

The Q4 report came out and I asked Winus AI to analyze it.

Nike beat earnings, but the stock story is still not clean.

$NKE revenue came in at $10.97B, and underlying EPS was about $0.20. Reported EPS looked much stronger at $0.72, but that included a $0.52 benefit from a one-time tariff recovery.

The problem: Nike Direct fell 7%, Greater China fell 12%, Converse fell 32%, and guidance still points to a slow turnaround.

For the stock, that means any short-term rally may be hard to trust unless investors see real sales growth, cleaner margins, and stronger China momentum.

Is Nike finally a comeback story or still a value trap?

Is anyone waiting to see @Nike earnings, but they're not really about Q4.

They’re about whether $NKE is a turnaround trade or a value trap.

The bar is low: about $10.85B revenue, $0.11 EPS, and China down ~20%. But options imply an ~8% move.

If margins hold above 40% and guidance improves, the stock can rip. If China or margins miss, the 12-year lows come back into play.

What would make you believe in the comeback?

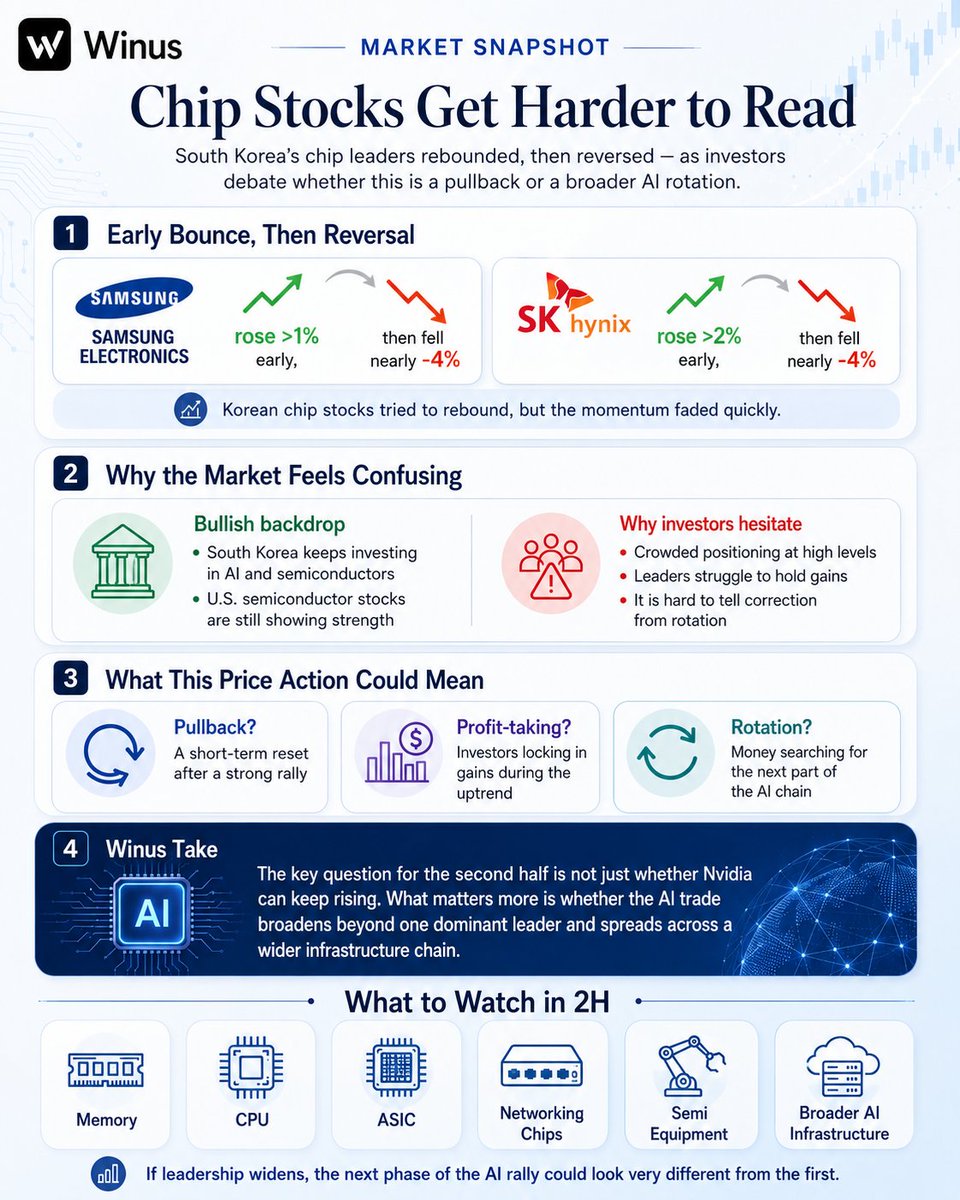

🤔 Chip stocks are getting harder to read again.

South Korean chip names tried to rebound in early trading, but the bounce quickly faded.

Samsung Electronics rose more than 1% and SK Hynix gained over 2% at one point — before both turned lower, with losses approaching 4% by the time of writing. 📉

That is the tension in today’s AI trade:

On one side, South Korea is still doubling down on AI and semiconductors.

On the other, chip leaders are struggling to hold gains as investors worry about crowded positioning at elevated levels.

Meanwhile, U.S. semiconductor stocks have continued to show strength, adding another layer of confusion. Is this a real pullback, or just profit-taking inside a longer uptrend? Is it divergence, or a rotation within the AI supply chain?

Winus analysis points to the key question for the second half:

It is not just whether Nvidia can keep rising. 🧠

The bigger issue is whether the AI trade can broaden beyond one dominant leader — into memory, CPUs, ASICs, networking chips, semiconductor equipment and the wider infrastructure chain.

If that happens, the next phase of the AI rally may look very different from the first.

Less about one mega-cap winner.

More about whether the entire AI infrastructure stack can keep expanding. ⚙️

#Winus #AI #Semiconductors #Nvidia #Samsung #SKHynix #MemoryChips #ASIC #CPUs #NetworkingChips #ChipStocks #TechStocks #Investing #StockMarket

The Yen Paradox: Why 5 Hikes Led to a 15% Collapse

Why has the Yen plummeted 15% to a 31-year low (USD/JPY hitting 162) despite the BOJ hiking interest rates 5 times? This isn't a glitch—it’s a structural fracture in the global monetary system.

Here is the breakdown. 👇

The Illusion of Tightening 📉 While the BOJ brought its policy rate to 1.0%, the macro reality hasn't changed. The rate hikes are too small and too slow. Japan is trapped by two massive structural handcuffs that prevent it from doing any real heavy lifting.

Handcuff 1: The Debt Trap ⛓️ Japan’s debt-to-GDP stands at a staggering 260%. A mere 2% rise in interest rates would increase government bond service costs by over 10% within two years. The BOJ wants to hike, but it can't—doing so too aggressively would trigger a fiscal crisis.

Handcuff 2: Fake Inflation & Weak Demand 🛑 Japan's inflation isn't driven by a booming economy; it’s imported cost-push inflation (energy & food). Real wage growth lags behind actual price hikes. Consumer spending is dead, leaving the BOJ with zero economic runway.

The $19.2 Trillion Carry Trade Monster 🐙 According to BIS data, the global Yen carry trade (including derivatives and swaps) has ballooned to a jaw-dropping $19.2 trillion. As long as the US-Japan yield differential remains a yawning chasm, the Yen remains the world's ultimate funding currency.

The Fed is Driving the Bus 🚌 The Yen’s trajectory doesn't depend on Tokyo; it depends on Washington. If the Fed hikes further, it effectively insures the carry trade. Under a +75bps Fed scenario, the market is already eyeing USD/JPY at 165+.

Asian Currency 'Firewalls' 🧱 In 1995-1998, a weak Yen triggered the Asian Financial Crisis. Today, the ultra-cheap "Made in Japan" label forces regional exporters into competitive devaluation. However, Asia now has deeper FX reserves—building "defensive walls" rather than collapsing.

Bottom Line: The textbook logic isn't broken; the structural reality has changed. A 260% debt load means the BOJ can’t hike effectively, and a $19T carry trade means the market doesn't believe they will.

For the deep-dive data, real-time CFTC positioning, and complete macro scenario modeling, check out the full breakdown by Wind AI Winus: 👉https://t.co/BDsiL57AY2

#GlobalFinance #Investing #ForexTrading #WindAI #Yen #BOJ #MacroEconomics

#Fed #FederalReserve #USDJPY

The Dow 52,000 headline sounds bullish.

But a price-weighted index getting lifted by a high-priced new member, with negative breadth underneath, is not the same as a broad market breakout.

The real test is July: does leadership broaden, or was this just quarter-end optics?

Super Week Ahead: Central Bank Giants Gather at Sintra Amid High-Stakes US Jobs Data and Rising Geopolitical Tensions

🚨 Key Market Implications & Risk Management

Liquidity & Volatility Alert: The shortened US trading week will compress volume. Thinned liquidity will inevitably amplify any knee-jerk reactions to macro data.

Tech Valuation De-risking: The central bank panel at Sintra and Thursday's NFP data will dictate the pricing for Q4 rate hikes. [Trading Strategy: Deploy Wind AI Winus to monitor global growth stock valuation percentiles and implement defensive hedging before the data drops.]

Energy Supply Chains: US-Iran tensions in the Strait of Hormuz could abruptly inject a geopolitical premium into crude oil and logistics markets.

A-Share Alpha Capture: China’s upcoming manufacturing PMIs provide a health check on domestic industry, while early H1 earnings previews show an 89% positive rate in tech and advanced manufacturing.

🛠️ The Trader's Arsenal:Overwhelmed by macro noise? You need a smarter AI co-pilot. Wind AI Winus dynamically tracks global macro variables and instantly parses mid-year corporate earnings surprises. Navigate this volatile July with data-driven confidence 🔗 https://t.co/iKxvqulxWX. #Sintra2026 #NFP #StraitOfHormuz #Semiconductors #WindAI #Winus #FinTech

Three tests for U.S. stocks this week: Warsh’s first major Fed appearance, June payrolls, and the ECB forum’s AI-financial-stability debate.

The AI trade is no longer just about growth. Rates, wages, capex and cost pass-through may decide Nasdaq’s next move.

https://t.co/HtW6ZLYofE

📉 The AI trade is cooling again in Asia.

Korea’s KOSPI fell as much as 3% shortly after the open, while the Korea Exchange once again triggered a circuit breaker for the KOSDAQ market.

Chip heavyweights also came under pressure: Samsung Electronics and SK Hynix both dropped more than 4% at one point. ⚠️

On the surface, this looks like another short-term pullback in the AI hardware chain.

But the real concern is deeper:

AI investment is still accelerating — while the market is starting to question the payback cycle.

According to Sina Finance, citing Korean media, South Korean President Lee Jae-myung is expected to host a public briefing where Samsung Electronics and SK Hynix will unveil large-scale investment plans.

The total investment could exceed 1,000 trillion won over the next decade — roughly $648 billion. 💰

For the industry, that signals continued expansion in semiconductors and AI infrastructure.

For public markets, it raises a more practical question:

Can this level of capex eventually translate into enough revenue, profit and cash flow?

The pullback may look sudden, but it is not just profit-taking.

Last week, memory chip stocks saw sharp swings — first selling off, then getting reignited by Micron’s strong earnings. Micron’s message was clear: AI infrastructure demand is still supporting memory, HBM, servers and hardware. 🔋

But that is exactly where the debate begins.

The stronger the supply-side expansion becomes, the more investors want proof that demand can keep up.

Winus analysis points to a shift in the AI trade:

The market is no longer satisfied with chip shipments, data center capex and compute expansion alone.

Investors are now watching AI application revenue, enterprise willingness to pay, usage frequency and the return-on-investment timeline. 🧠

The next phase of the AI trade may not be about who spends the most.

It may be about who can prove the spending actually pays off.

#Winus #AI #TechStocks #Semiconductors #Samsung #SKHynix #KOSPI #KOSDAQ #Micron #HBM #DataCenters #Capex #Investing #StockMarket

We’ve officially entered the era of of AI cost engineering.

@coinbase reportedly cut AI spend nearly in half while usage kept climbing by routing tasks smarter and boosting cache hits from 5% → 60%.

Here is what Winus AI has to say

Winners: Coinbase, open-weight models, GLM/Kimi, AI efficiency teams.

Losers: premium-priced frontier APIs.

Is this the new enterprise AI playbook?

#fintech #AI #coinbase #SmartRouting

The market is not treating the US-Iran headline as full peace yet.

Brent gave back most of its war premium. Airlines rallied. Stocks jumped.

But US gold prices rebounded around the headline, suggesting investors still want insurance.

I used Winus AI to fact-check the reaction.

Is it a real de-escalation or a 48-hour trade?

BREAKING: The US and Iran have agreed to halt strikes and meet this week, per Axios.

The announcement comes just one hour before US stock market futures are set to reopen.

![winus_ai's tweet photo. Super Week Ahead: Central Bank Giants Gather at Sintra Amid High-Stakes US Jobs Data and Rising Geopolitical Tensions

🚨 Key Market Implications & Risk Management

Liquidity & Volatility Alert: The shortened US trading week will compress volume. Thinned liquidity will inevitably amplify any knee-jerk reactions to macro data.

Tech Valuation De-risking: The central bank panel at Sintra and Thursday's NFP data will dictate the pricing for Q4 rate hikes. [Trading Strategy: Deploy Wind AI Winus to monitor global growth stock valuation percentiles and implement defensive hedging before the data drops.]

Energy Supply Chains: US-Iran tensions in the Strait of Hormuz could abruptly inject a geopolitical premium into crude oil and logistics markets.

A-Share Alpha Capture: China’s upcoming manufacturing PMIs provide a health check on domestic industry, while early H1 earnings previews show an 89% positive rate in tech and advanced manufacturing.

🛠️ The Trader's Arsenal:Overwhelmed by macro noise? You need a smarter AI co-pilot. Wind AI Winus dynamically tracks global macro variables and instantly parses mid-year corporate earnings surprises. Navigate this volatile July with data-driven confidence 🔗 https://t.co/iKxvqulxWX. #Sintra2026 #NFP #StraitOfHormuz #Semiconductors #WindAI #Winus #FinTech](https://pbs.twimg.com/media/HL9-CPSbgAAxR0T.jpg)

![winus_ai's tweet photo. Super Week Ahead: Central Bank Giants Gather at Sintra Amid High-Stakes US Jobs Data and Rising Geopolitical Tensions

🚨 Key Market Implications & Risk Management

Liquidity & Volatility Alert: The shortened US trading week will compress volume. Thinned liquidity will inevitably amplify any knee-jerk reactions to macro data.

Tech Valuation De-risking: The central bank panel at Sintra and Thursday's NFP data will dictate the pricing for Q4 rate hikes. [Trading Strategy: Deploy Wind AI Winus to monitor global growth stock valuation percentiles and implement defensive hedging before the data drops.]

Energy Supply Chains: US-Iran tensions in the Strait of Hormuz could abruptly inject a geopolitical premium into crude oil and logistics markets.

A-Share Alpha Capture: China’s upcoming manufacturing PMIs provide a health check on domestic industry, while early H1 earnings previews show an 89% positive rate in tech and advanced manufacturing.

🛠️ The Trader's Arsenal:Overwhelmed by macro noise? You need a smarter AI co-pilot. Wind AI Winus dynamically tracks global macro variables and instantly parses mid-year corporate earnings surprises. Navigate this volatile July with data-driven confidence 🔗 https://t.co/iKxvqulxWX. #Sintra2026 #NFP #StraitOfHormuz #Semiconductors #WindAI #Winus #FinTech](https://pbs.twimg.com/media/HL9-EqMbUAIemDt.jpg)