前天参加区块先生年会,从 @RiverdotInc co-founder那了解到satUSD的核心「链上质押借USD,能在任意链上进行使用。」

They will do something big! 谢谢区块先生 @mrblock 办的优质活动,让大家知道好项目。

谢谢 @River4fun 活跃整个社群!

Last day to introduce $satUSD!

Join the River Flow and Dance with satUSD!

satUSD is the soul of @RiverdotInc and @River4fun, uniting DeFi from fragmentation to cohesion. Whether minting, staking, or contributing to the community, it offers stable returns and growth opportunities.

Act now: visit https://t.co/CT5zv4h8Ix, connect your wallet, and start your Omni-CDP journey.

Follow @RiverdotInc and @River4fun, join River4FUN, earn Pts, and reap rewards—let’s “Flow with River” together!

#satUSD #RiverEcosystem #DeFi #LayerZero #TGE #BNB

Today I saw a ton of people sharing sensational headlines like “Microsoft bans employees from using AI” and stuff like that — they’re all just pure clickbait.

$MSFT $NVDA

Today I saw a ton of people sharing sensational headlines like “Microsoft bans employees from using AI” and stuff like that — they’re all just pure clickbait.

$MSFT $NVDA

Microsoft just banned its own engineers from using AI.

The tool was literally costing MORE than the humans it was supposed to replace.

They lied to you about AI adoption and now the whole narrative is blowing up:

Microsoft gave thousands of engineers access to Claude Code six months ago and encouraged them to use it.

Engineers loved it and adoption exploded. But then the invoices arrived.

Token-based pricing means every query, every code review, every debugging session costs money. At scale across 100,000 engineers, the numbers became so large that Microsoft issued an internal order to cancel nearly all Claude Code licenses by end of June and force everyone onto their own cheaper tool instead.

The company that invested $5 billion in Anthropic just told its own people to stop using Anthropic's product because it costs too much.

Uber's story is even worse...

Their CTO Praveen Neppalli Naga told The Information that the budget he planned for the full year was "blown away already" by April.

Uber had rolled out Claude Code in December 2025. By March, 84% of their 5,000 engineers were using it with 70% of all committed code coming from AI systems.

Heavy users were burning $500 to $2,000 per month each. Naga himself spent $1,200 in a single two-hour demo session.

The company had even built internal leaderboards ranking engineers by how much AI they used. They literally gamified the spending and then ran out of money.

Now look at what Nvidia's own VP of applied deep learning Bryan Catanzaro said to Axios last month. Direct quote:

"For my team, the cost of compute is far beyond the costs of the employees."

This is a VP at the company that SELLS the chips saying that using AI is more expensive than paying humans.

Think about what this means for the entire AI narrative.

Every CEO on every earnings call for the past two years has said the same thing:

AI will make us more efficient, reduce headcount, and cut costs.

The stock market rewarded every company that said it.

Fired workers, stock goes up. Announced AI adoption, stock goes up.

But the actual companies deploying AI at scale are discovering the math doesn't work. The MORE employees use AI, the HIGHER the bill.

Goldman Sachs forecasts a 24x increase in token consumption by 2030 as companies adopt AI agents. Gartner just published a report showing that even though individual token prices will drop 90% by 2030, total enterprise AI costs will go UP because agents consume exponentially more tokens per task than basic tools.

Meta built an internal dashboard called "Claudeonomics" to track which employees use the most AI. Amazon started pushing engineers to "tokenmaxx," their internal term for consuming as many AI tokens as possible.

Both companies are spending hundreds of billions on AI infrastructure this year alone.

And Microsoft, the company that bet its entire future on AI, just told 100,000 engineers to stop using the tool they liked best because the per-token bills got out of control.

The companies building AI are telling investors it saves money. The companies using AI are finding out it costs more than the humans it was supposed to replace. And even the company that makes the chips just admitted it through its own VP.

This is the gap nobody on Wall Street is pricing in.

$725 billion in AI infrastructure spending this year across Big Tech. And the first companies to actually deploy these tools at scale are already pulling back because the economics don't work.

What do you think?

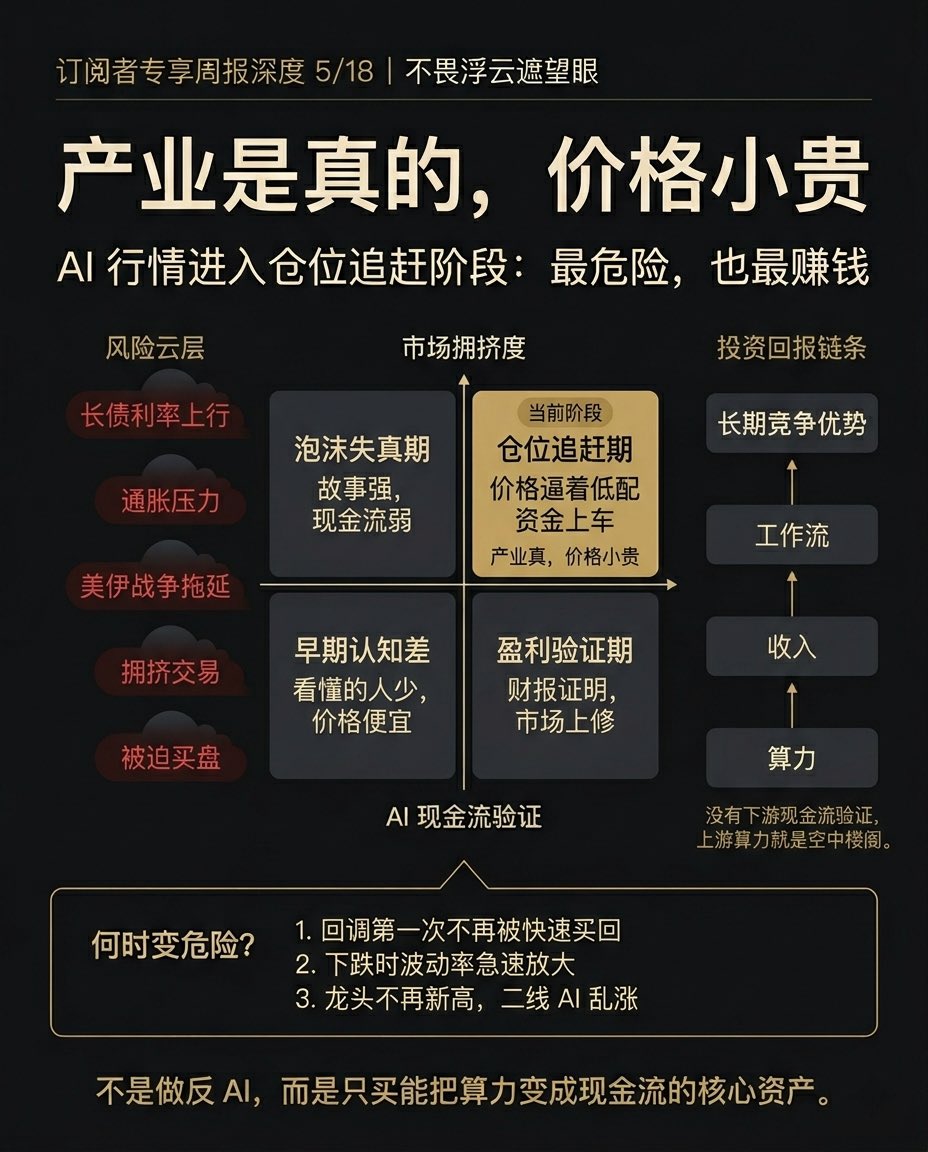

$NVDA Q1 FY2027 Earnings Blowout Summary! (Released May 20)

🚀 Revenue: $81.6 Billion ✅ YoY +85% ✅ Crushed expectations

Data Center dominates 92% of revenue! Blackwell platform is fully exploding — AI demand is unstoppable 🔥

📊 Key Highlights at a Glance:

• EPS $2.39 (YoY +214%)

• Gross Margin steady at 75%

• Q2 Guidance: $91 Billion (continued double-digit growth)

• Dividend 25x surge + $80B new buyback authorization!

👍 Pros (Major Strengths)

•AI factory buildout at unprecedented speed

•Networking revenue YoY +199%

•Rock-solid ecosystem moat (Agentic AI + full-stack platform)

•Massive cash flow → super generous shareholder returns

👎 Cons (Risks to Watch)

•92% revenue concentration in Data Center

•China market completely excluded due to export controls

•Operating expenses rising fast

•Valuation already sky-high — any small miss could spark volatility

Bottom line: This is a monster earnings beat! AI demand isn’t slowing — it’s accelerating. NVIDIA remains the clear AI king 👑

Will the stock keep running? Or time to be cautious? Drop your thoughts below 👇

#NVIDIA #NVDA #AI #Earnings #Blackwell #Investing

(Data from official report — Not investment advice)

Note: The $160M convertible notes completed in April (which actually closed on April 17) were not included in the core financial statements of the Q1 2026 earnings report.

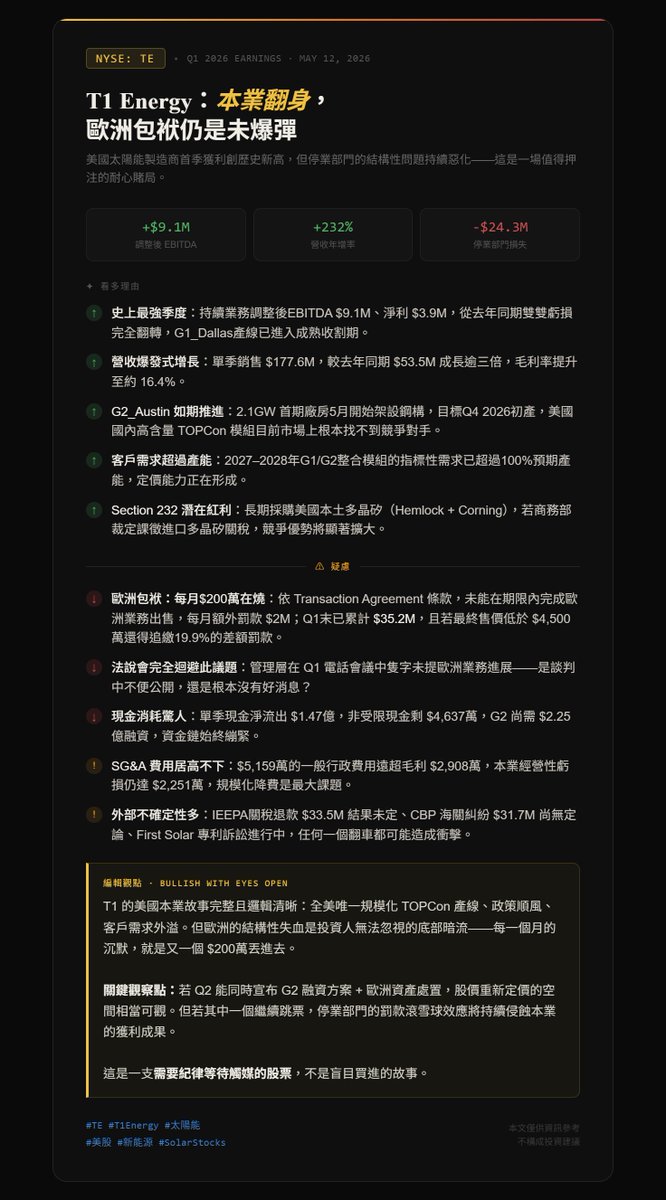

$TE | T1 Energy Q1 2026 — Quick Take 🧵

Best quarter ever on the core business. A quietly compounding European liability nobody wants to talk about. Here's the full picture.

📈 The Bull Case→ Adj. EBITDA hit $9.1M — full reversal from losses a year ago. G1_Dallas is in harvest mode. → Revenue tripled YoY to $177.6M. Margin expanding on mix shift to fixed-price contracts. → G2_Austin on schedule — domestic TOPCon cells at scale, a product that simply doesn't exist elsewhere in the U.S. → Customer demand for 2027–28 already exceeds 100% of anticipated production capacity. → Section 232 ruling = direct tailwind if domestic polysilicon wins.

⚠️ The European Problem→ $2M/month in contractual penalties until the European assets are sold. Accrued total: $35.2M and counting. → Management said nothing about European disposal on the earnings call. Silence during negotiations, or just no good news? → Discontinued ops liabilities ($56.4M) now massively exceed remaining assets ($11.8M).

🎯 Bottom Line

The U.S. story is real. But the European bleed is the tax every bull pays until it's resolved.

Watch for a Q2 announcement combining G2 debt financing + European asset sale. That's the re-rating trigger. If either slips again, the discontinued ops snowball keeps eating into hard-won core earnings progress.

Catalyst-dependent trade. Not a set-and-forget.

For informational purposes only. Not investment advice.

#TE #T1Energy #SolarStocks #CleanEnergy #USManufacturing