Building a few little things: @premargin. Failed: @tryflare. Sold: @MENAbytes. I also write Termsheet, a newsletter on startups and VC in emerging markets.

Public company data in the Middle East is surprisingly hard to work with.

For a lot of my writing on Termsheet, I do it regularly, and the process is painful.

Data scattered across exchange websites (and some other portals), PDFs that won’t open, financials in different formats.

You sometimes end up with 10 browser tabs open just to understand basic stuff about one company.

To solve this, I am building this little thing called @Premargin with @ritwickdsouza.

It lists all the public companies across Saudi Arabia, UAE, Qatar, Kuwait, with their financials (a bit light at the moment but more coming soon), disclosures, and fundamentals.

There’s also a screener that allows you to filter companies by stock performance, valuation, ratios, and a few other things.

Nothing fancy at the moment. Just the data you need, organized like it should have been from the start.

Still early, still building. But it works. I am using it myself.

Play with it here https://t.co/9xuG1bw60m. And please do share your feedback.

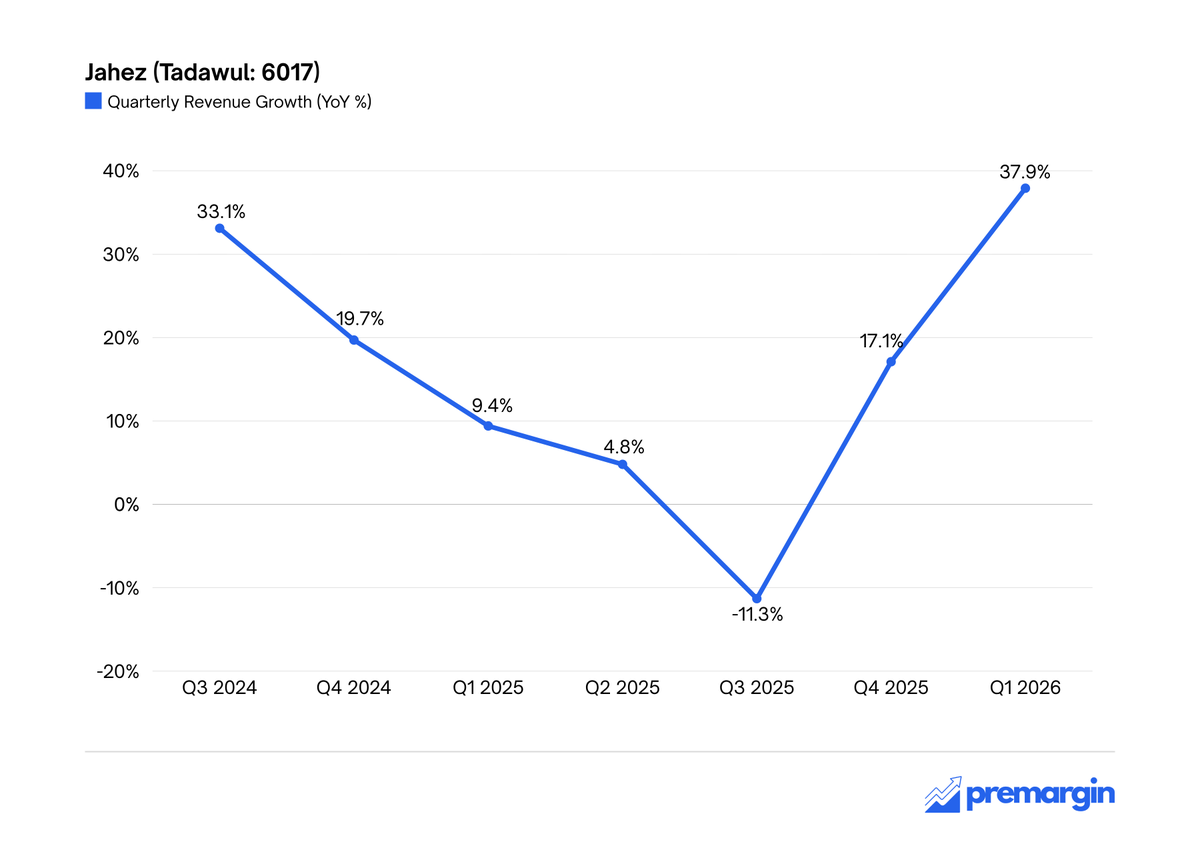

Jahez: Saudi decelerating. Non-KSA growing exponentially (thanks to Snoonu). At this pace, non-KSA should become the larger revenue contributor next quarter.

When Jahez acquired Snoonu last years, the deal valued the Qatari startup at more than one-fifth of Jahez's own market cap at the time.

It looked expensive to many.

Food delivery acqusitions in the region have a long history of looking expensive initially.

Talabat. HungerStation. Carriage. InstaShop. Zomato UAE. Yemeksepeti.

Most looked expensive in the moment. Many aged very well.

Jahez acquired 76.5 percent of Snoonu in July 2025 for $245 million. Its market cap at the time was about $1.5 billion.

That means 16 percent of its market cap of or about 21 percent on an implied valuation basis, for Snoonu.

And this was not a small company.

Snoonu was doing $140 million in annual net revenue and growing significantly faster than Jahez - which was making a little over $590 million in net revenue at the time. Snoonu would have represented roughly 19 percent of the combined entity’s revenue base.

On 2024 numbers, Jahez paid around 2.3x Snoonu’s revenue while Jahez itself traded at around 2.5x revenue.

(On earnings, the multiple looked more expensive).

The more important thing however was timing.

Jahez announced the acquisition almost three quarters after Keeta entered Saudi Arabia.

By then, the company had likely seen enough to realize that growth in Saudi was going to become increasingly difficult as long as Keeta continued funding all sides of the marketplace with subsidies.

And that should have played a major role in the decision to acquire Snoonu.

The latest earnings now show how important Snoonu has become inside the Jahez universe.

The company noted in its Q1 2026 earnings:

“Group net revenue grew 37.9% YoY to [$193.2 million], driven primarily by the consolidation of Snoonu, which led to a 5.6x revenue growth in Jahez’s non-KSA segment, more than offsetting a 12.0% decline in the KSA segment.”

Based on Termsheet estimates, Snoonu’s contribution to Jahez’s Q1 2026 revenue was likely between $60 million and $70 million.

That would mean Snoonu potentially contributed up to 36 percent of Jahez’s total quarterly net revenue.

In other words, without Snoonu, Jahez’s group revenue in Q1 2026 would likely have declined by over 5 percent.

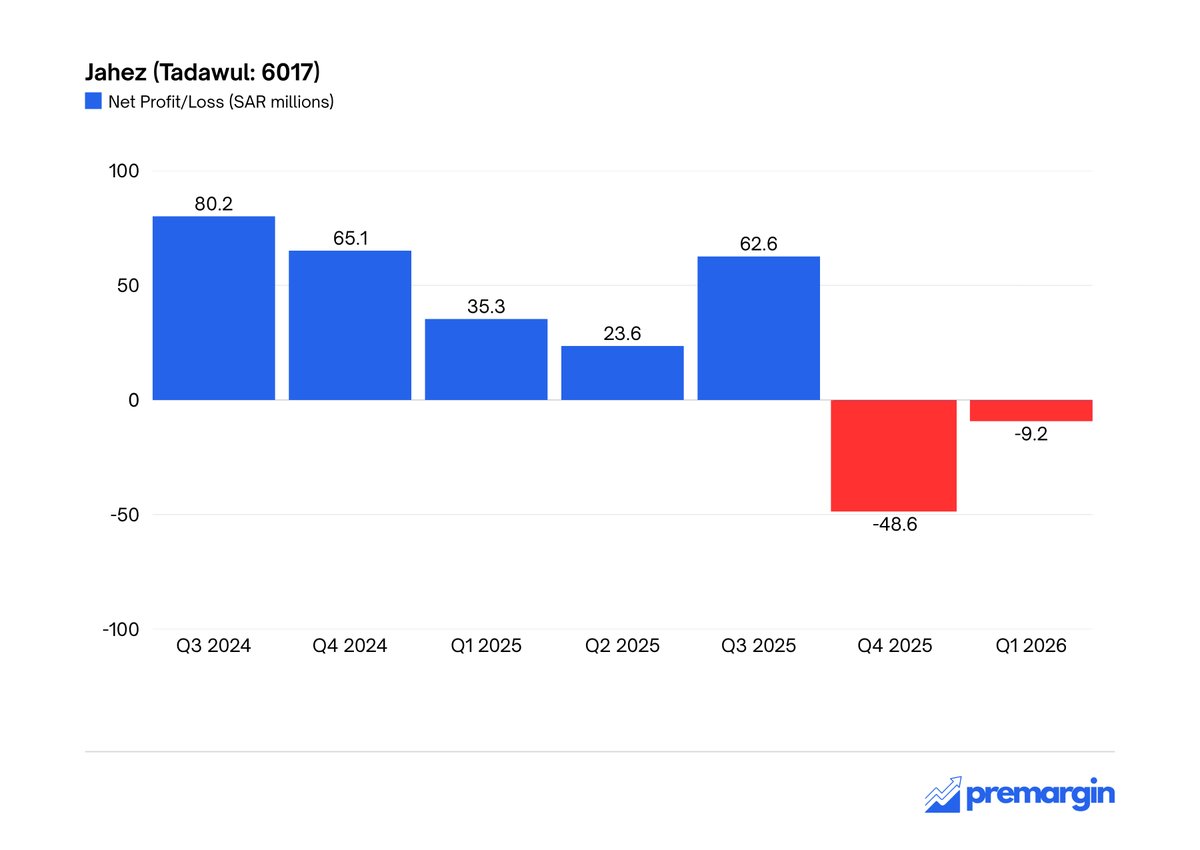

Jahez stock has been crushed. Since the acquisition, market cap is down over 55% to $682m.

Keeta’s aggressive Saudi expansion weighs on sentiment. Without Snoonu outlook would be worse as core growth slows and margins compress.

Mgmt said market share rose in Q1 2026 vs Q4 2025, but no figures. Market remains unconvinced.

Jahez’s stock fell more than 7 percent on the day it announced earnings and is down more than 12 percent since then.

Investors appear far more focused on the pressure Keeta continues to create in Saudi.

Which is also what makes Snoonu increasingly important for Jahez.

The acquisition was initially framed as international expansion. Increasingly, it is also starting to look like a partial buffer against the pressure building in its core market.

More on Termsheet.

Raza Mohsin needed motor testing equipment for the @VLEKTRA factory. China was too expensive. A local engineer took an advance and delivered something that never worked.

Then someone walked in with a different offer.

No degree. No English. No CV. His only credential was 15 years of working alongside his electrician father.

What happened next is the best argument I've heard for where Pakistan's real talent actually lives.

Ninja is reportedly working with banks to potentially IPO in Saudi over the next few months.

But.

There’s a lot that stands in their way.

There are four Saudi internet/tech companies that have gone public so far.

Jahez. Rasan. Tasheel Finance. Nice One.

Jahez and Nice One are trading well below their IPO price; down about 70 percent and 60 percent respectively.

Tasheel Finance is also trading slightly below its IPO price.

Rasan is the only exception, up more than 300 percent since listing. But it’s a company with software-like growth and margins, so it cannot really be used as a reference for something like Ninja.

If we expand the pool beyond Saudi, Talabat is also down over 40 percent since listing in the UAE.

And that is before we even get to what’s happening to the category itself.

Since Keeta’s expansion into the Kingdom, competition in food and grocery delivery has intensified significantly. Rising CAC. Compressing margins. Companies going out of business. Shgardi. Careem (Food). Nana.

Jahez reported net losses in its latest two quarters after 19 straight profitable quarters.

Quick commerce was already a category public investors looked at cautiously because of structurally weak margins and the number of global failures it has produced.

(Now Saudi has Nana too).

And Keeta will likely put even more pressure on margins, at least for the time being.

Private investors may still be comfortable paying 1.5x GMV.

But public investors, given how tech (except Rasan) has performed and what’s happening in the category more broadly, may not be so generous.

Despite all of this, I am still bullish on the category and on Ninja as a company.

But I don’t think this is the right time to go public.

More on Termsheet. Soon.

The three $10 billion+ Saudi companies growing revenue at over 20% year-over-year.

You can use the screener on Premargin to track and screen public companies across the region using different metrics, including YoY growth.

The experience is a bit clunky for now, but it works.

At the moment, the easiest way to save screens is by bookmarking the links.

Native support for saved screens, additional financial metrics including CAGR, historical growth, and more, is coming over the next few weeks.

If you'd like to track companies though, the first version of watchlists is already live.

Only three Saudi-listed companies with market capitalizations above $10 billion grew revenue by more than 20% in 2025.

Elm led the group with 27.8% YoY revenue growth, followed by Al Rajhi Bank and Sulaiman Al Habib.

Track on: https://t.co/SzaWpTHR5J

They’ve grown both revenue and net profit at a CAGR of about 18% over the past five years, the fastest growth among these top companies.

https://t.co/8YctIMZX7c

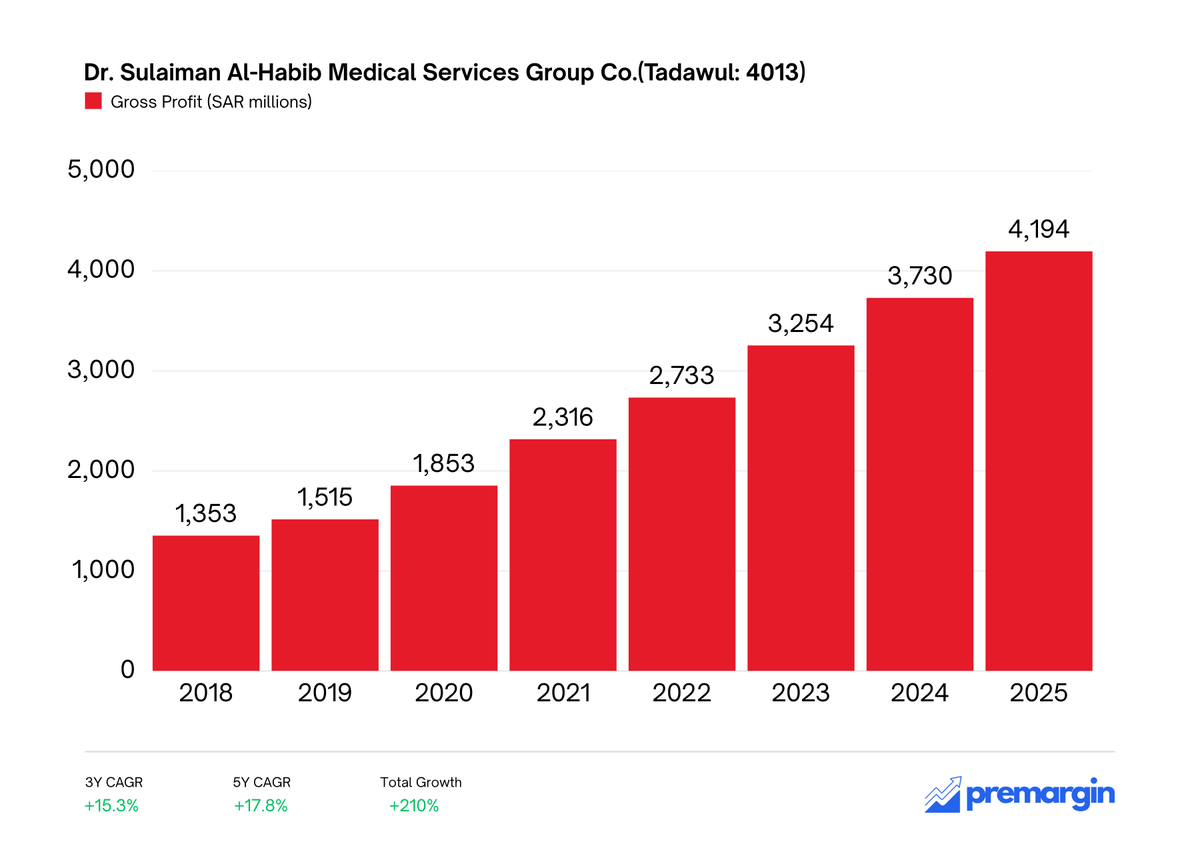

Dr. Sulaiman Al Habib Medical Services Group 2025 recap:

Revenue: SAR 13.7B (+22% YoY)

Gross profit: SAR 4.19B (+12% YoY)

Net profit: SAR 2.40B (+4% YoY)

Quick insights:

Profit growth lagged revenue growth

Margins down after 2023 peak

Net margin ↓ ~17.5% (2018 levels)

📊👇

There are nine Saudi companies with a market cap of over $20 billion. Including Aramco.

Seven of these are owned/controlled by the state, mainly through PIF.

The two that are not owned by the government are Al Rajhi Bank and Sulaiman Al Habib Medical Group.

Al Rajhi first hit $20 billion market cap in early 2010s. About 25 years after its IPO.

Sulaiman Al Habib went public at about $5 billion in 2020 and reached $20 billion market cap in just two years.

At its peak, the company was valued at $26.5 billion.

It is probably one of the least discussed large-scale private sector success stories to come out of Saudi Arabia.

PS. You can use Premargin's stock screener to track this list in real time and screen listed companies across GCC markets by market cap, revenue, profitability, valuation multiples, and other financial metrics.

Saudi Arabia’s largest listed companies excluding Aramco.

Banks dominate the top of the market, while mining, telecom, utilities, petrochemicals, and healthcare round out the list.

This ranking can be tracked live on Premargin’s stock screener: https://t.co/GBUVxYtRPE

There are nine Saudi companies with a market cap of over $20 billion. Including Aramco.

Seven of these are owned/controlled by the state, mainly through PIF.

The two that are not owned by the government are Al Rajhi Bank and Sulaiman Al Habib Medical Group.

Al Rajhi first hit $20 billion market cap in early 2010s. About 25 years after its IPO.

Sulaiman Al Habib went public at about $5 billion in 2020 and reached $20 billion market cap in just two years.

At its peak, the company was valued at $26.5 billion.

It is probably one of the least discussed large-scale private sector success stories to come out of Saudi Arabia.

PS. You can use Premargin's stock screener to track this list in real time and screen listed companies across GCC markets by market cap, revenue, profitability, valuation multiples, and other financial metrics.

Dr. Sulaiman Al Habib Medical Services Group 2025 recap:

Revenue: SAR 13.7B (+22% YoY)

Gross profit: SAR 4.19B (+12% YoY)

Net profit: SAR 2.40B (+4% YoY)

Quick insights:

Profit growth lagged revenue growth

Margins down after 2023 peak

Net margin ↓ ~17.5% (2018 levels)

📊👇

Pakistan makes the world's clothes. The brand is never ours.

Rastah changed that. Bieber. Chalamet. London Fashion Week. All from Lahore.

Sat with Zain Ahmed (@zainoo_95) to understand how. The pricing strategy. The inventory disasters. The community that defended the brand and the future of celebrity endorsement.

Full episode out now.

Introducing Claude Design by Anthropic Labs: make prototypes, slides, and one-pagers by talking to Claude.

Powered by Claude Opus 4.7, our most capable vision model. Available in research preview on the Pro, Max, Team, and Enterprise plans, rolling out throughout the day.

The startup ecosystems that scaled fast almost always had someone engineering the conditions early.

Stanford's Frederick Terman actively pushed his students to start companies nearby and helped build the infrastructure around them. That deliberate act of clustering is a big part of how Silicon Valley got its head start.

Shenzhen was a policy decision before it was a phenomenon. Singapore's tech scene was seeded by government-backed VC programs, not organic momentum.

Saudi has been doing something similar. Jada has been systematically backing local and international fund managers to invest in the Kingdom. SVC has been deploying into fund managers and co-investing directly in deals. These were deliberate interventions designed to build the infrastructure of an ecosystem.

And it's worked. Saudi has grown into the largest VC market in the region, a shift that would have been hard to imagine a decade ago.

Not taking anything away from the underlying fundamentals: the largest economy in the region, a young and largely tech-savvy population already primed for digital adoption. But the interventions mattered.

There's something that gets underappreciated though. A thriving ecosystem doesn't automatically produce great companies.

If you look at where the most interesting companies actually come from, inside any ecosystem, it's almost always from a surprisingly small radius.

A cohort of founders who knew each other. A shared office where a few teams overlapped at the right time. An investor who was physically present and close enough to help when it mattered.

This happens because trust and utility travel through repeated, unplanned contact. A founder doesn't benefit from every other founder in the city, they benefit from the people they're genuinely in orbit with. The ones they run into, have unscheduled conversations with, and build real context alongside.

When you concentrate enough of the right people in the same physical space - capital, experience, and early-stage hunger - you're creating the conditions that have historically preceded serious company formation.

This is what the team at @colabswork is trying to build deliberately with their first campus in Riyadh. I've been working with them as an advisor for the last few months, and it's a considered effort.

What's telling is who they've brought in as founding members. One of the leading VC firms in the region. A founder with two exits. A young Saudi team building in the loyalty space. That's a considered mix.

They're trying to engineer the conditions that produce the next generation of meaningful companies out of Saudi.

This is extremely ambitious. Trying to punch above their weight. But the early signals, both in intent and in who’s showing up, are directionally right.

Whether that works depends on execution over the next few years.

COLABS Narjis launches next week.

If you're building something in Saudi and want to be part of what they're putting together, worth reaching out to @omarsshah.

Not the full picture, but interesting.

Sorted by lowest P/E, Tadawul mid-caps ($1B–$10B):

~6.5x earnings, below book

Banks <1x P/B

ROE from ~8% to 35%

Explore full screen: https://t.co/CzG9Yuca0A

Build your own → filter, sort, save (bookmark for now)

Saudi is one of the most important places in the world to build the future. That’s why I’m excited to see @colabswork open its first location COLABS Narjis in Riyadh, in collaboration with Rakan AlRashed, Faisal AlRashed at Waseel Partners Investments.

We invested in COLABS in 2022 because we believed they were building more than a coworking space. They’re a platform that helps entrepreneurs, operators, and investors come together, collaborate, and compound each other’s ambition.

Riyadh is one of the most dynamic innovation hubs in the region today, and it deserves spaces that match the energy of the people building here.

For founders, builders, and companies looking to get started in Saudi, @omarsshah and the COLABS team are a great first call. They can help with setting up and make the right introductions to get you moving.

Congrats to the COLABS team on this milestone. Look forward to seeing what gets built at COLABS Narjis, Riyadh.