$RKLB $ASTS: Shoutout to fellow space nerds for making it to Dow Jones News! @JacobKeeton20@BrettKrieger12@SpaceInvestor_D

These 'nerds' earned millions betting on space years before the SpaceX IPO made it cool

By Christine Ji

(MarketWatch) -- Everyday investors - like a 'Star Trek' fan, an accountant and an engineer - use satellite imagery, track planes and visit rocket-launch sites

After quitting his semiconductor-engineering job last year, 35-year-old Jacob Keeton left his hometown of Beaverton, Ore., and embarked on a 12,000-mile road trip across America and back. Over the span of 11 weeks, Keeton drove through Idaho, Utah, Oklahoma and many other states, visiting over a dozen national parks on his journey.

The ultimate destination and reason behind Keeton's voyage was an unassuming six square miles of land hugging the Atlantic Ocean. For decades, Wallops Island, Va., has been home to a NASA rocket-testing facility. More recently, it's begun to accommodate launch pads for an aerospace company called Rocket Lab (RKLB). Keeton has accumulated tens of thousands of Rocket Lab shares and become a millionaire, brokerage documents reviewed by MarketWatch show.

For Keeton, it's been a dream come true. "I've been a sci-fi nerd and space fan my whole life," Keeton told MarketWatch. He now identifies as "semi-retired," attributing his work status to the 40 hours a week or more he spends monitoring his Rocket Lab investment and the space industry at large.

"I haven't got to visit the other facilities yet, but they're all marked on my Google Maps," Keeton said. "I've searched imagery of every kind from every facility. I've looked up tax records for anything that might have some nugget of information." He's even bought satellite imagery to track Rocket Lab's construction progress at Wallops.

Keeton also made a pit stop in Florida to see 28-year-old accountant and fellow space investor Brett Krieger. Together, Krieger, Keeton and a third collaborator known anonymously as Space Investor host a weekly Tuesday live audio broadcast on X, drawing listeners ranging from thrill-seeking retail investors to NASA scientists. Krieger and Space Investor have seen the value of their portfolios inflate to millions of dollars over the past two years as Rocket Lab shares exploded by over 2,300%, to $108 as of Tuesday, and its market valuation reached $63 billion.

The trio - who met on X through Rocket Lab discussion threads - made risky bets on a company whose success once seemed just about impossible. They are part of a crew of swashbuckling space enthusiasts and retail traders who explored for riches in the cosmos and now look smart on the eve of the blockbuster SpaceX IPO. These stargazers evoke comparisons to the investor cults that have surrounded stocks like Palantir (PLTR). While there is some overlap - Krieger currently owns Palantir shares and Space Investor has traded them in the past - investing large sums of money in rocket science demands a unique degree of grit and idealism veering on masochism.

Krieger's investment plunged him into an open-source intelligence community that obsessively tracks every crumb of Rocket Lab news and data. "There are people going over to the New Zealand facilities every day, taking pictures of the Neutron progress or tracking planes, boats and shipping supplies over to Virginia," Krieger said.

For decades, space exploration stagnated under the purview of bureaucracy-steeped government processes. Many scientists viewed Elon Musk's mission of building a private spaceflight company with contempt as SpaceX rocket launches failed one after another, incinerating some of Musk's personal fortune and putting his companies on track for bankruptcy in 2008.

Rocket Lab CEO Peter Beck seemed to stand even less of a chance when he founded the company in 2006, as an amateur rocketeer with no college degree and no funding. Beck hails from the southern tip of New Zealand, a country whose dominant industries are dairy products and tourism. But Beck had the crazy idea of creating a small rocket that would make frequent and cheap trips to space. As Beck later recalled on the "Relentless" podcast, in the early days he would scavenge for spare parts in junkyards to save money.

Today, Rocket Lab's small-lift Electron rockets act like outer-space Ubers, delivering clusters of satellites into custom trajectories on behalf of imaging companies, government agencies and researchers. Electron is the second-most-launched U.S. rocket, trailing only SpaceX's Falcon 9. The company has also built its own vertically integrated satellite-manufacturing division.

For his contributions to the New Zealand aerospace industry, Beck was knighted in 2024. "We all call him Sir Peter Beck out of respect," Krieger said.

Rocket Lab has yet to turn a profit. The company is currently spending hundreds of millions of dollars building Neutron, a much larger rocket scheduled to be test-launched on Wallops at the end of this year. The stock trades at a rich valuation multiple, 100 times trailing sales, according to FactSet.

But against all odds, Rocket Lab and other private space companies have created a vibrant commercial ecosystem at a time when space is once again capturing the hearts and minds of mankind. SpaceX's impending public listing has sparked an industry-wide rally in space stocks. Missile defense systems, orbital data centers, asteroid mining and Mars colonies: The final frontier beckons with untold riches and glory that Rocket Lab and others are racing to claim.

Rocket Lab's loyal supporters are confident that Beck and the company will be successful. "He's a madman genius," Space Investor said.

'I sold half of my portfolio to pay down my house, car and all my debt'

Rocket Lab successfully completed 21 Electron launches in 2025.

Keeton first heard about Rocket Lab when he was a college student studying mechanical engineering, following the inaugural launch of its Electron rocket in 2017. His classes included satellite design and orbital mechanics, and he worked on a university project to build the base station for a ground launch system. When rumors swirled in March 2021 that Rocket Lab planned to go public via a reverse merger with a special purpose acquisition company, Vector Acquisition Corp., Keeton jumped in and bought 200 shares of the SPAC.

Rocket Lab officially debuted on the Nasdaq COMP in August 2021. Over the next few years, Keeton accumulated as much as 50,000 shares of the company even as the stock bottomed at $3.53 a share in April 2024.

Keeton's average cost per share was $6.36 in September 2024, according to brokerage records. As Rocket Lab increased the cadence of its Electron launches and reported a blowout quarter in November 2024, the stock shot up.

At the beginning of 2026, Keeton trimmed his Rocket Lab position as his portfolio hit a peak of $6.4 million. Keeton now holds around 11,000 shares of Rocket Lab; brokerage records viewed by MarketWatch show that Keeton has realized over $3 million in Rocket Lab gains. Keeton has invested in other space names such as AST SpaceMobile (ASTS), but he noted that Rocket Lab has always been his biggest holding. On top of buying and holding, Keeton likes to trade momentum-based options, he said.

The "space craze" was what lured Space Investor back to stock picking after a decade on the sidelines. "I've always been looking to the stars...watching 'Star Trek,' 'Star Wars,' all of that," Space Investor said. In his free time, he builds Lego rockets and model rocket kits with his children. "We launch rocket models every summer together," Space Investor said.

Making risky investments and borrowing excessively had nearly bankrupted him during the financial crisis, Space Investor told MarketWatch, but the 2019 public debut of space-tourism company Virgin Galactic (SPCE) inspired Space Investor to set aside a few thousand dollars into a "YOLO" account.

Space Investor initiated a position in Rocket Lab in 2023 after reading "When the Heavens Went on Sale," a book about the commercial spaceflight industry starring new space startups like Rocket Lab, Planet Labs (PL), Astra Space and Firefly Aerospace (FLY). Impressed by author Ashlee Vance's description of Beck's dogged determination, Space Investor aggressively built up his position as shares of Rocket Lab fell. He set buy orders for 100 shares every 10-cent drop, accumulating up to 10,000 shares of Rocket Lab for as little as $3.50 per share, according to brokerage documents.

Over the past year, Space Investor says his portfolio of space stocks - which also included names like AST SpaceMobile and Redwire (RDW) - crossed the $1 million mark. "I sold half of my portfolio to pay down my house, car and all my debt," Space Investor said.

Space Investor would only speak on condition of anonymity. MarketWatch reviewed Space Investor's brokerage records and verified his identity.

Wall Street takes off

Over the past 18 months, institutional investors have joined the Rocket Lab trade and their participation in the stock has steadily grown, leading Needham analyst Ryan Koontz to initiate coverage of the stock in April 2025. Like the retail crowd, institutional investors have been charmed by Beck and his executive team, which Koontz believes is a major selling point for Rocket Lab.

Rocket Lab successfully completed 21 Electron launches in 2025, giving Wall Street a major boost of confidence in the company. "There's a heavy fixed cost to running multiple launch facilities," Koontz told MarketWatch. "If you're not doing enough launches, it shows up in your margins, and it's not pretty." Rocket Lab's gross margins reached a record high of 38.2% in the most recent quarterly report, up from 28.8% a year ago, according to company filings.

Koontz himself has been a space enthusiast his whole life. "I was always kind of a geeky kid," Koontz said. "It was always something of interest to me, outer space and rockets and that sort of stuff." Decades ago, he worked as a telecommunications engineer before becoming a sell-side analyst. With the recent influx of institutional capital into the space economy, previously inconceivable technological advancements are suddenly within reach.

"There's been more and more engagement as they come up to speed on the whole sector and realize that this is no longer just a little niche defense and aerospace play," Koontz said of institutional investors. "It's becoming a commercial force and it's starting to disrupt terrestrial industries."

But Rocket Lab retail investors are not just fair-weather friends. As the stock languished in penny-stock territory around the end of 2024, insurgent squads of space enthusiasts huddled in scattered corners of the internet. Space Investor's posts from that era would generate the occasional like or two. Outsiders would sometimes stumble across the Rocket Lab community and be swept up in its orbit.

Brett Krieger sports official Rocket Lab gear.

That's how Brett Krieger found his way to Rocket Lab and became the millionaire he is today. A skeptic when he first heard about the company in 2023, Krieger soon changed his mind as he learned more about Rocket Lab. The company's space-systems business is a "one-stop shop," Krieger said. "They can build your constellation, they can launch it and they will operate it."

Krieger doubled down on his Rocket Lab position as the stock troughed. While Krieger declined to disclose his exact holdings, documents viewed by MarketWatch show that he's built up a substantial position in Rocket Lab with an average cost basis of $6.73 per share, gaining millions over the past three years. Krieger further immersed himself in the online community of space-stock fanatics and last year he opened a position in AST.

"When the Heavens Went on Sale" - which was adapted into a 2024 HBO documentary titled "Wild Wild Space" - has since become a canonical text in the Rocket Lab community, credited for bringing mainstream awareness to the company. An anonymous X account by the name of @SpaceGhost has assembled a Rocket Lab Wiki compiling every interview, commercial satellite deal, transcript and available piece of data on the company.

Rocket Lab investors geek out over the company's signature aesthetic, from its sleek black carbon-fiber Electron rockets to a custom-built mission-control center designed with pitch-black walls and crimson LED lighting. Krieger describes the room as "Darth Vader-themed." It's a vibe that Beck has leaned into by playing the "Star Wars" soundtrack throughout the headquarters, according to Vance's book. Fans purchase Rocket Lab-branded shirts, jackets, model rockets and even baby onesies.

These self-described space nerds don't just live online. In April, Krieger drove two hours to Florida's Cape Canaveral to watch Blue Origin's third launch of its New Glenn rocket, which was carrying an AST BlueBird satellite. He was joined by fellow enthusiasts and investors, some of whom had flown in past midnight to catch the early-morning April 19 launch.

Krieger and Keeton both plan to travel to Wallops to attend the Neutron launch later this year. Plans are circulating amongst the community to charter a private jet and throw a massive party, Krieger said.

'The second-worst thing that can happen'

Blue Origin's next major test was not as successful as the one Krieger witnessed. On May 28, a fiery mushroom cloud enveloped Cape Canaveral as New Glenn's engine malfunctioned during a pre-flight test, blowing up the rocket, launch pad and other nearby infrastructure.

"They say in the industry destroying a launch pad is the second-worst thing that can happen," Keeton said, "with the first being loss of a crew." The explosion has reportedly set back Blue Origin's progress by at least six months, not to mention derailed satellite-deployment timelines across the entire industry.

Shares of Rocket Lab, AST, Planet Labs and other space stocks tumbled in the aftermath. It's a stark reminder of the space industry's inordinate risks, especially for newer space investors who entered the arena amidst the roaring momentum of the past two years.

However, Clear Street analyst Greg Pendy sees the Blue Origin mishap as an opportunity for Rocket Lab to seize market share. "We see a backlog of satellites looking to launch, with canceled missions," Pendy told MarketWatch. When rockets do come back online, Pendy anticipates major congestion at launch points in the U.S. "Rocket Lab is unique because they have the ability to launch not only from the U.S. but also New Zealand," Pendy added.

With the SpaceX IPO coming this week, space investors face another source of uncertainty. Undoubtedly, Musk's SpaceX is the trailblazer to which the rest of the industry owes its existence. But it's also a ruthless competitor, and its record-smashing public listing threatens to crowd out other names in the space ecosystem.

"Everyone is wondering if it's going to suck up liquidity in the field or if it's going to draw more eyes and liquidity," Keeton said. "I personally think it's going to be a bit of both."

After the SpaceX IPO, Keeton plans to take a break from actively monitoring his space investments. His next plan for retirement is very down-to-earth. "I'm moving into a van starting this summer," Keeton said.

-Christine Ji

Look everyone... don't ever be concerned with my positions; be concerned with the risk you are taking.

I've been trading for 43 years and have had only a few single-digit drawdown years. All of my trades are made from very low-risk entry points and always with a hard stop loss in place.

I could turn out to be wrong and the market may have already made its low. If so, I'll get stopped out. That's the business.

I'm wrong just as often as I'm right. The difference is that my risk is always defined and controlled. What matters is not being right all the time; what matters is that the risk taken relative to the potential reward, adjusted for batting average, is managed in a way that produces a profitable outcome over a large sample of trades.

That's how I've approached the market throughout my entire career, and it's no different today. The distribution of gains and losses over time forms a profitable bell curve because risk always comes first, and risk is always managed in relation to reward.

My favorite 800V Power Semiconductor stocks ranked:

1. $WOLF (Wolfspeed) $2.7B market cap — The most asymmetric setup in the entire space. Wolfspeed controls the SiC substrate bottleneck, the foundational material every other SiC device maker needs. If the fab reaches target utilization, revenue could 3-5x from the current ~$713M run rate, and gross margins would inflect from negative to 40%+. At $2.7B, the market is pricing in heavy skepticism. A successful execution would make this a $10B+ company.

2. $NVTS (Navitas Semiconductor) $6B market cap — If Navitas captures even 2-3% of the AI data center power conversion TAM over the next three years, that’s a $500M+ revenue business on a fabless cost structure with 40%+ gross margins. The GaN IC technology is proven, the GeneSiC SiC portfolio adds a second vector, and the 59% revenue concentration in one AI-infrastructure distributor tells you where the growth is coming from. From a 3-year view, the revenue base could be 10x larger than today.

3. $AEHR (Aehr Test Systems) $1.5B market cap — The purest picks-and-shovels play on SiC scaling. Every SiC wafer that Wolfspeed, onsemi, STM, Infineon, or Rohm produces needs burn-in testing, and Aehr’s FOX-XP platform is the standard tool. Revenue is ~$100M and growing rapidly, but SiC production volumes are projected to 5-10x over the next five years. Aehr’s revenue is directly levered to that ramp with high incremental margins. A $100M revenue equipment company serving a market that’s about to quintuple has obvious math.

4. $VICR (Vicor Corporation) $5B market cap — Vicor’s factorized power architecture and power-on-package modules solve a physics problem that gets worse with every GPU generation: delivering 1,000+ amps at sub-1V to a processor die without unacceptable voltage droop and heat. If this architecture becomes standard in AI accelerator designs, Vicor’s content per server could be $500-1,000+. Revenue is ~$400M today. In a bull case where 2-3 major AI chip platforms adopt Vicor’s approach, this is a $2B+ revenue company at 50%+ gross margins, a $25B+ market cap.

5. $AOSL (Alpha & Omega Semiconductor) $1.5B market cap — The most overlooked name in power semi. AOSL makes power MOSFETs and PMICs for computing, server, and industrial applications. At $1.5B market cap and ~$650M revenue, it trades at ~2.3x sales, a fraction of MPWR’s 37x. The company is modestly profitable, has real products shipping into server power applications, and would benefit enormously from any broadening of AI power demand beyond the top-tier suppliers. This is the deep value pick: if the AI power theme lifts all boats, AOSL re-rates from 2x to 5x sales and the stock doubles without heroic assumptions.

Honorable mentions:

$DIOD $XFAB $ON $POWI $MPWR

The AI-Infrastructure buildout is the biggest wealth-creation event this decade.

These 8 stocks will profit the most:

1. $CRWV | CoreWeave

The biggest NeoCloud provider in the entire world.

Backed by $NVDA via. a $2B investment and a technical collaboration.

- $99B backlog

- Massive Hyperscaler deals

- Fastest growing Neo-cloud by absolute numbers

Revenue is expected to grow by 1500% until 2030.

🧵👇

Copper can't keep up with AI. That's not an opinion, it's physics.

Every data center being built right now is replacing electrical connections with light. NVIDIA confirmed it with $4.5 billion in direct investment.

I mapped 25 public companies across the photonics value chain:

Every AI cluster being built today hits the same wall. A hundred thousand GPUs mean nothing if the data can't move between them fast enough. Copper maxed out years ago and photonics replaced it: lasers, optical fiber, and transceivers that push data at the speed of light. The AI transceiver market doubled in two years. NVIDIA committed $4.5 billion across three photonics companies this year alone. This is where the infrastructure money is going.

Here's the full value chain:

🔬 MATERIALS & WAFERS

This is the bottom of the chain. Every laser and transceiver starts as a wafer substrate: indium phosphide, gallium arsenide, germanium, specialty glass. Nobody above this layer can produce anything without these inputs, and right now the most critical one, indium phosphide, is the tightest material in the entire AI supply chain. The gap between demand and capacity is getting worse, not better.

I think this is the most asymmetric layer on the map. Investors chase the transceiver companies and ignore who grows the substrates underneath them. But NVIDIA is writing checks worth billions in cash and warrants to lock up supply from this exact layer. First link in the chain, last to get attention, and the one that chokes everything above it if it breaks.

Tickers: $GLW, $AXTI, $IQE, $AIXA, $AMS

💡 CORE PHOTONIC DEVICES

This layer converts electricity into light and back. Without it, zero data moves through fiber. NVIDIA dropped $4 billion into two companies here this year just to secure production capacity, and both of them joined the S&P 500 within weeks of each other. That should tell you how fast this went from niche to essential.

The supply gap is not closing. The companies shipping next gen lasers at volume can be counted on one hand, and switching suppliers takes years of requalification. Order books stretch past twelve months. Every next generation GPU cluster consumes more of these components than the last, and no one can substitute them on short notice. I watch this layer more closely than any other.

Tickers: $IPGP, $COHR, $LITE, $LASR, $SIVE

🔌 COMPONENTS & MODULES

The companies here take raw lasers and detectors, package them into finished transceivers and modules, and ship them straight to hyperscalers. If the layers below are the engine, this is the vehicle that actually reaches the customer. Hyperscaler purchase orders land here. The revenue acceleration shows up here first.

What I like about this layer is that you can underwrite it today, not in two years. These are businesses with signed capacity commitments and product already moving. The consolidation angle matters too: larger photonics players have already started absorbing standalone module companies, and whoever remains independent gains pricing power as options thin out.

Tickers: $AAOI, $MTSI, $VIAV, $LPTH

⚙️ SYSTEMS & EQUIPMENT

No company above this layer can manufacture a single photonic component without the machines built here. One of these names holds 100% of the EUV lithography market with zero competitors. Others supply the bonding equipment for co packaged optics or the process control instruments used across the majority of advanced packaging lines. If photonics is the gold rush, this is the layer selling the picks.

My honest take: this is where the smart, patient capital parks. Equipment companies have pricing power and multi year order books that generate cash through full capex cycles. They attract holders who don't panic on the first pullback. The stocks don't run 1,000% overnight, but they compound while everything above them swings, and that tradeoff is worth more than most people give it credit for.

Tickers: $ASML, $BESI, $ASM, $LPKF, $MKSI

🔍 TEST, METROLOGY & YIELD

The most ignored layer on this map, and arguably the one with the cleanest business model. Every wafer, laser, and transceiver has to be tested and verified before it ships. As speeds climb and photonic devices get more complex, the testing challenge compounds fast. The industry is now constrained not only by what it can build but by what it can prove actually works.

Yield is money. Better defect detection means better margins for every company upstream, which is why foundries keep buying test equipment even when they slash budgets everywhere else. These are capital light businesses tied to every unit of production across the chain. Last check before product hits the customer, and one of the few layers where demand doesn't cycle down when the rest of semis softens.

Tickers: $CAMT, $FORM, $AEHR, $ONTO, $VIAV

🧠FINAL THOUGHTS

The NVIDIA capital concentration tells the whole story. One company wrote $4.5 billion in checks to three photonics suppliers in a single quarter. That is a company locking down the one input that could bottleneck its GPU deployments: the optical interconnect.

Returns across this sector have been historic over the past twelve months. But separate the revenue growers from the narrative trades. Some of these companies are printing real quarterly numbers that would impress in any sector. Others are carrying multi billion dollar market caps on sub $100 million in annual revenue. Same sector, wildly different risk.

Every generation of AI infrastructure from here forward needs more photonics. Not less. The copper to light transition inside data centers is early. Co packaged optics is barely in deployment, and 1.6T transceivers are ramping with 3.2T already on roadmaps. The chain locks together: stress on any single link reprices every link above it.

10 WAYS TO BUILD AN AI POWER PORTFOLIO

1. $OKLO effectively building the “local nuclear plant” the AI economy will require by placing reactors directly next to data center campuses for 24/7 onsite generation.

2. $BE fuel-cell onsite power play helping data centers bypass the grid with dedicated energy for AI clusters with product backlog up 250% YoY to $6B.

3. $CEG nuclear baseload backbone of the AI era with a 20-year $MSFT PPA tied to the Three Mile Island restart to supply the 24/7 carbon-free power.

4. $VST hybrid power engine of AI combining nuclear, gas & storage with a 20-year $META agreement covering 2,600+ MW across three nuclear plants.

5. $GEV industrial supplier rebuilding the U.S. grid providing the turbines, transformers & hardware every AI-driven upgrade cycle depends on with $163B in backlog.

6. $VRT infrastructure gatekeeper for AI compute controlling the cooling & power systems that $NVDA class clusters cannot run without with Q1 backlog up 80% YoY to ~$12.5B.

7. $EOSE long-duration storage solution for a grid under strain helping utilities smooth volatility as AI demand overtakes supply.

8. $NEE clean-energy arm of the AI buildout with largest renewable development pipeline in the country positioned directly into data center load growth.

9. $LEU only U.S. source of HALEU fuel making it essential for powering the modular reactors needed around future AI campuses backed by ~3B DOE contract.

10. $UUUU secures the domestic uranium supply chain by turning nuclear fuel into a national-security asset for the AI age.

I mapped 25 public companies across 5 sectors of the Space economy: rockets, satellites, earth observation, lunar exploration and defense.

SpaceX IPOs in weeks at $1.75 TRILLION and most people have zero exposure to the sector it's about to reprice.

🧵 Full breakdown below:

🛰️ LAUNCH & ACCESS

The foundation layer. Nothing happens in space without getting there first.

$RKLB : Rocket Lab

The one I watch most closely in this sector. Q1 2026 hit a record $200M+ in revenue with a backlog over $2.2B. Electron is one of the most reliable small launch vehicles ever built (87 launches, 83 successes). But the real catalyst is Neutron, their medium lift rocket targeting megaconstellation deployment. First launch planned late 2026. Designed to compete with Falcon 9. Peter Beck has quietly built a vertically integrated space platform: rockets, satellite buses (Photon), spacecraft components, and now aiming for human spaceflight class capability. This isn't just a launch company anymore.

$FLY : Firefly Aerospace

IPO'd August 2025. Growing 40% quarter over quarter. Designs and manufactures launch vehicles, satellites, and lunar cargo spacecraft for Artemis missions. Very early in its public life, not profitable yet, but the growth rate is hard to ignore and the government contract pipeline gives long term visibility.

SpaceX (expected $SPCX)

Not yet public but about to be. Filed S1 on May 20, 2026. Expected to list on Nasdaq around June 12. Targeting $1.75T to $2T valuation. $18.7B in 2025 revenue with Starlink alone doing $11.4B. This is not just a rocket company. It's a global internet infrastructure monopoly being built from orbit. The IPO raise could hit $40B to $80B, shattering Saudi Aramco's record. When this lists, it re rates every single company on this map.

Blue Origin (private, often paired with $BA)

Jeff Bezos' rocket company. Still private. Developing New Glenn (medium to heavy lift) and Blue Moon lunar lander for NASA's Artemis program. Now launching AST SpaceMobile's BlueBird satellites, which tells you they're becoming a serious commercial launch provider. Watch for a potential public listing down the road.

$LDOS : Leidos

The quiet giant. One of the largest US defense and IT services contractors with deep space integration capabilities. Mission systems, satellite ground infrastructure, cybersecurity for space assets. Not a pure space play but they touch nearly every government space program. The kind of name nobody talks about that keeps showing up in every contract announcement.

📡 SATELLITE COMMS

This is where revenue is scaling fastest. Connecting the planet from orbit. And personally I think this subsector is the most investable part of space right now because the business models most resemble traditional recurring revenue.

$ASTS : AST SpaceMobile

The most ambitious play on this entire map. Building the first space based cellular broadband network that connects directly to unmodified smartphones. No dish. No special hardware. Your regular phone picks up signal from satellites. Partners include AT&T, Verizon, Vodafone, Rakuten, and Google. FCC just authorized commercial SpaceMobile service in the US. BlueBird 6, the largest commercial comms array ever deployed in LEO, successfully launched. Sitting on ~$3.5B cash and over $1.2B in contracted revenue commitments. This is either a generational infrastructure buildout or the most expensive bet in telecom history. The partner list tells me it's the former.

$VSAT : Viasat. Legacy satellite broadband

Airlines, military, maritime, enterprise. Facing Starlink competitive pressure but the defense angle is the real floor here. Government contracts provide stability that pure commercial satellite plays don't have. Not the sexiest name on this list but the kind of stock that holds up when the speculative ones get cut in half.

$IRDM : Iridium Communications

Operates the only satellite constellation providing truly global voice and data coverage, including the poles. 66 cross linked LEO satellites. Critical for maritime, aviation, government, and IoT. Extremely sticky revenue, high margins, constellation fully refreshed with Iridium NEXT. One of the most underappreciated cash flow machines in the space sector. Not flashy. Just prints. If I had to own one space stock for a decade and not touch it, this would be near the top of the list.

$GSAT : Globalstar

Became a much bigger story after Apple selected them to power the iPhone Emergency SOS via satellite feature. Apple invested heavily and Globalstar is building next gen satellites to expand the partnership. The Apple relationship alone makes this a completely different risk profile than most small cap space names. Effectively a satellite infrastructure play with the most valuable company on Earth as your anchor customer.

$SATS : EchoStar / Inmarsat

Operates one of the broadest geostationary satellite fleets globally. Maritime, aviation, government, enterprise connectivity. Large legacy business generating real cash flow while positioning for next gen services. The kind of mature operator that the market ignores during hype cycles and then remembers when it wants quality.

🌍 EARTH OBS & DATA

The intelligence layer. Imaging the planet daily and turning raw pixels into actionable decisions.

$PL : Planet Labs

The largest fleet of Earth observation satellites ever deployed. Daily imaging of the entire planet's landmass. Feeds agriculture, forestry, defense, insurance, and climate monitoring. Planet is the "data layer" of the space economy. If you believe Earth observation becomes as essential as GPS (and I do), Planet is the company best positioned to own that layer at scale.

$BKSY : BlackSky Technology

Real time geospatial intelligence. The play here is AI powered analytics layered on satellite imagery. Where Planet goes wide (image everything daily), BlackSky goes deep (real time intelligence for specific targets). Heavy defense and intel community customer base. Smaller but differentiated.

$SPIR : Spire Global

Satellite powered data analytics via a constellation of nanosatellites collecting weather, maritime, and aviation data. Business model is data as a service: they sell the analytics, not the hardware. Weather forecasting, ship tracking, supply chain intelligence. Interesting because unit economics improve with every satellite added to the constellation.

$TRMB : Trimble

Positioning, modeling, and data analytics across construction, agriculture, transportation, and geospatial workflows. Not a pure space company but deeply dependent on satellite positioning systems and increasingly integrating space based data into precision applications. Massive installed base. Real earnings. The boring but profitable way to play the space data theme.

$GILT : Gilat Satellite Networks

Ground segment technology: VSATs, amplifiers, modems, and managed network services. Israeli company with deep defense relationships. Every satellite constellation needs ground infrastructure to function. Gilat builds that infrastructure. Under the radar but essential.

🌙 EXPLORATION & ON ORBIT

The frontier. Lunar missions, space manufacturing, orbital services, asteroid mining. The highest risk and highest potential upside tier on this map.

$LUNR : Intuitive Machines

This one has been on a tear. Revenue nearly tripled year over year in Q1 2026 after closing the $800M Lanteris acquisition in January. Now expanding into satellite comms, orbital data processing, and deep space networking. Participating in the Space Force Andromeda program with a $6.2B ceiling. Also acquiring Goonhilly Earth Station. Went from "cool lunar lander startup" to vertically integrated space infrastructure company in about 12 months. The acquisition strategy is aggressive but so far the revenue is backing it up.

$RDW : Redwire

Space infrastructure and on orbit manufacturing. Revenue growing nearly 60% YoY with a record backlog approaching half a billion. Makes solar arrays, structures, sensors, and is pioneering manufacturing in microgravity. If the thesis that zero gravity unlocks materials impossible to create on Earth proves out, Redwire is the picks and shovels company for that entire category.

$KTOS : Kratos Defense & Security Solutions

Unmanned systems, satellite communications ground systems, cybersecurity, and hypersonic drone development. Their space division builds command and control infrastructure for satellite operations. The intersection of space and autonomous defense systems is exactly where government budgets are accelerating fastest.

$BWXT : BWX Technologies

Nuclear technology for defense and space. Provides nuclear propulsion and power systems for NASA and DoD. Nuclear thermal propulsion is considered essential for deep space missions to Mars and beyond. If humanity goes to Mars, BWXT technology is very likely on that spacecraft. Long term thesis but anchored by near term defense nuclear revenue that makes the wait very comfortable.

$ATRO : AstroForge

The asteroid mining company. Pre revenue. High risk, true moonshot category. The thesis: asteroids contain platinum group metals worth trillions. AstroForge is building spacecraft to go extract them. Most people will dismiss this as science fiction. Fair enough. But every transformative sector had a moment where it sounded like science fiction, and the people who mapped it early were the ones who captured the asymmetry.

🛡️ DEFENSE PRIMES

The trillion dollar backbone. When governments write space checks, these are the companies cashing them. Real revenue. Real earnings. Real dividends. The stability layer of the space economy.

$LMT : Lockheed Martin

Largest defense contractor on Earth. Space division builds GPS satellites, missile defense systems, Orion spacecraft (Artemis), hypersonic systems. Won the next gen missile warning satellite program. When the US government needs something in orbit, Lockheed is usually the first call.

$NOC : Northrop Grumman

Built the James Webb Space Telescope. Makes solid rocket boosters for nearly every US launch vehicle. Operates Cygnus cargo spacecraft for ISS resupply. Deep, long duration government contracts with decades of visibility.

$RTX : RTX (formerly Raytheon Technologies)

Missile defense, radar, satellite payloads, communications systems. Pratt & Whitney builds rocket engines. Collins Aerospace provides spacecraft avionics. The merger created a space/defense conglomerate that touches virtually every program in existence.

$LHX : L3Harris Technologies

Space and airborne systems. Satellite payloads, ground terminals, electro optical sensors, communication systems for classified programs. Key contractor on the Space Development Agency's proliferated LEO constellation for missile tracking. Growing rapidly as "space as a warfighting domain" becomes official Pentagon doctrine.

$GD : General Dynamics

Submarines, combat vehicles, IT services, and space. GDIT division provides mission critical IT infrastructure for space operations, ground segment systems, and satellite data processing. Not the flashiest space exposure but deeply embedded in the classified programs that quietly fund this entire sector.

📊 THE ETF PLAY

$NASA : Tema Space Innovators ETF

Launched March 31, 2026. Actively managed, 20 to 40 holdings. And the real differentiator: direct pre IPO exposure to SpaceX through an SPV, something retail investors literally cannot access anywhere else. If you want one click space economy exposure with SpaceX embedded, this is it.

🧠 FINAL THOUGHTS

Five sectors. 25 companies. The full stack of the space economy.

SpaceX targeting $1.75T+ at IPO. When it lists, it becomes the gravitational center of this entire map. Every supplier, every competitor, every adjacent company gets re rated. The Arm IPO repriced chip IP in 2023. The SpaceX IPO reprices space.

What stands out to me looking at this map:

The pure plays (Rocket Lab, AST SpaceMobile, Intuitive Machines, Redwire) are where the growth is. Revenue doubling and tripling year over year. But these carry higher risk and most are still unprofitable.

The defense primes (Lockheed, Northrop, RTX, L3Harris, General Dynamics) are where the stability is. Real earnings, dividends, and space as a growing share of revenue. Lower upside but much lower downside.

The satellite comms layer (Iridium, Globalstar, AST SpaceMobile) is where the business models are proving out fastest. Recurring subscription revenue from connectivity. This part of space most resembles a traditional business.

I'm not saying buy everything on this list. I'm saying map it. Understand the layers. Know which companies have real revenue versus aspirational roadmaps. Know where the government contracts are versus the commercial bets.

This sector is where AI stocks were before ChatGPT made everyone a believer. The difference is the space crowd hasn't had its catalyst moment yet. The SpaceX IPO might be exactly that. The people who already mapped the landscape will move first.

2026 has been an amazing year so far, with many great stocks giving excellent returns. Here are some names with best YTD returns and made a new ATH last Friday.

$AXTI $BE $SIMO $VPG $ARM $TTMI $PENG $OSS $GFS $DELL $MRVL $MDA $AMD $SMTC $SKYT $LSCC $ACMR $ALAB $LRCX $CORZ $HPE $ASML $CRDO

The future of AI is agentic.

There will be billions of AI agents. Every person and company will have multiple agents.

That makes cybersecurity one of the most interesting sectors to watch.

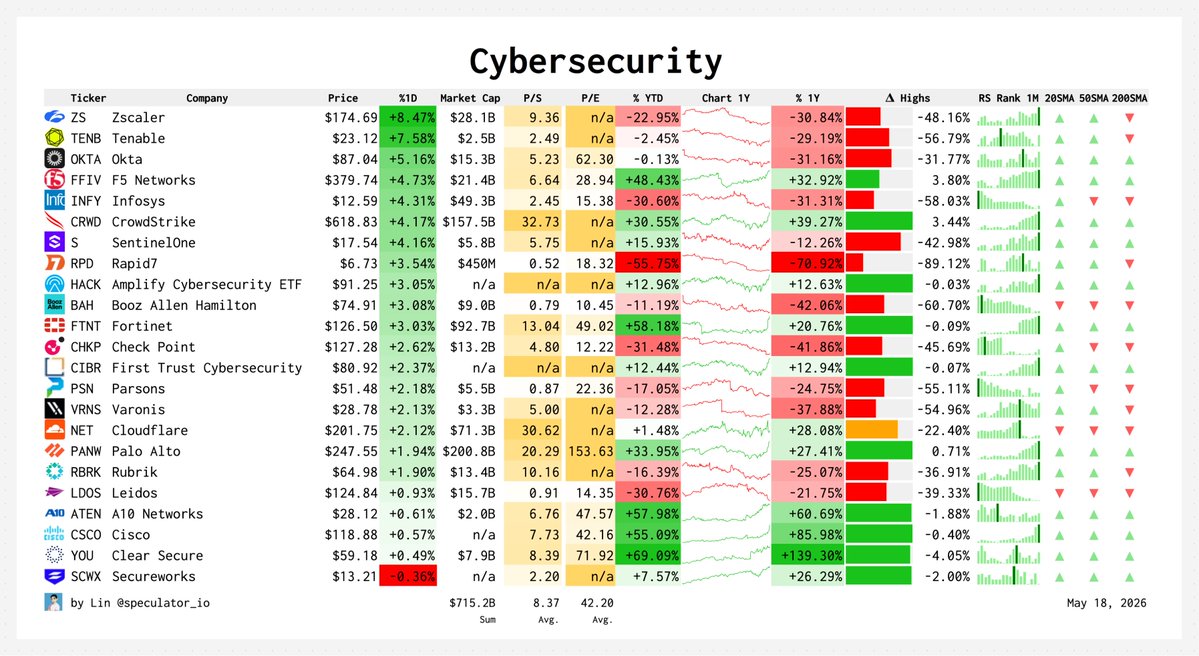

Threat Detection

$CRWD CrowdStrike

$PANW Palo Alto Networks

$S SentinelOne

Network Security Providers

$FTNT Fortinet

$FFIV F5 Networks

$CSCO Cisco

$ATEN A10 Networks

$CHKP Check Point

Cloud Security

$NET Cloudflare

$ZS Zscaler

$OKTA Okta

Biometric Identity Verification

$YOU Clear Secure

Identity and Access Management

$OKTA Okta

Vulnerability Management

$TENB Tenable

$RPD Rapid7

$SCWX Secureworks

Data Security and Analytics

$VRNS Varonis

IT Services and Consulting

$INFY Infosys

$BAH Booz Allen Hamilton

$LDOS Leidos

$PSN Parsons

Cybersecurity ETFs

$HACK Amplify Cybersecurity ETF

$CIBR First Trust Cybersecurity ETF