This covers

- 1995/2015, 2008-2015 (with/without McCloud) & 2015 only

- hospital doctors or GPs

- added years

- can add actual PSS when (if!) you receive it

- help plan CURRENT 25/26 year (when you can do something about it)

Register / see📹

https://t.co/Mt66LYfml8

Pls shr RT!

How can people plan with information that's years out of date? How can people know if they can do extras to help #waitinglists@wesstreeting

The NHS pension is a really important & really valuable part of reward package @NHSEmployers. Its being BADLY let down by administration

Full submission to HMRC. FIRST cost claim reimbursed. Then HMRC sends updated information. Asked to pay additional £1k saying it needs to re-do calculations. HMRC refuses to pay SECOND time. Radio silence from @ForvisMazarsUK Is there anything I can do @goldstone_tony@TheBMA

Brown envelope landed and no idea what to do?

My video below talks you through all you need to know about your RPSS (now been watched 12k times🙏)

You qualify for FREE expert accountancy advice if you

✅Paid AA in 15/16-21/22 (cash or scheme pays)

✅Pension growth ↑ in any yr 15/16-21/22 post-roll

✅Pension growth ↑ £40k in 22/23

“Triage on a page” to see if can reclaim cost of accountants: https://t.co/MuAdfXcFqq

Sign up here 👉: https://t.co/c171OlAJRP

Help video🎥: https://t.co/nYtIAS9S0S

Pls shr/RT/FB/WhatsApp colleagues not on socials

Quite a few people receiving revised or manual RPSSes currently. If you had already processed your RPSS to HMRC its no issue claiming again from NHSBSA who will cover the professional cost of an accountant to submit again to HMRC. Details of what do with your RPSS below 👇

Hoping your RPSS brown envelope is going to sort itself & the cheque will be in post? Bad news-it wont!

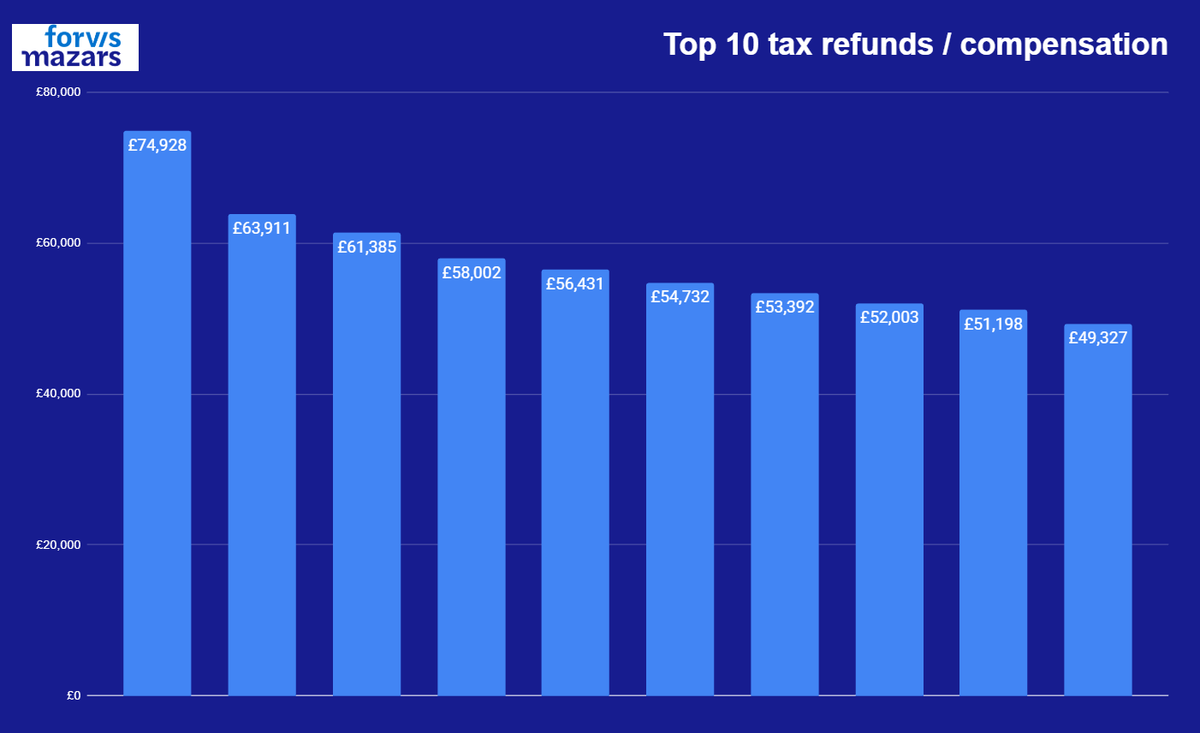

The good news is you can get expert specialist medical accountants to sort this for you, for free. Avg compensation over £14k, top 10 claimed below

https://t.co/aLd1DH7CqH

⚠️Lots of threads/posts on tapering, threshold, adjusted etc. Now we have March payslips can I tell you how I would approach it

1️⃣ Get your March 25 payslip. Note your YEAR TO DATE TAXABLE Pay. *IGNORE* gross pay and for now IGNORE pensionable pay. Dont use gross income and deduct pension contributions - the "taxable pay" already has them deducted so dont deduct it again.

2️⃣Do *NOT* add back in salary sacrifice for things likes cars and childcare. You are required to add in "relevant salary sacrifice arrangements made after 8 July 2015" - the key word here is relevant defined as "the individual gives up the right to receive general earnings or specific employment income in return for the making of relevant pension provision," - so DONT add cars etc back in.

3️⃣So you now have your NHS taxable income for the year. Now you need to add any other taxable income - think other PAYE, private practice, property, BIK, dividends, interest etc. Basically anything else that is subject to income tax. Less employment related Income Tax Reliefs claimed via tax return i.e. GMC, BMA, MDU etc

4️⃣Do NOT take off gift aid for normal charitable donations which is another common mistake Ive seen experts make. Note you can do this for the ridiculous £100k cliff calculation, but not threshold/adjusted

5️⃣So your NHS taxable income plus all other taxable income, less any other NON NHS pension contributions i.e. a SIPP, is THRESHOLD INCOME.

If this is below £200k you are not tapered and have the full £60k allowance and any carry forward (use the HMRC carry forward calculator to work out if you have carry forward - you will have needed both your RPSS to the 22/23 tax year and 23/24 PSS to work this out, latter obviously also delayed in England & Wales - you can estimate 23/24 using the tool below).

6️⃣If threshold income above £200k you need to work out ADJUSTED INCOME. You wont find out your PIAs for 24/25 until October 2025 but can estimate them using the link to the free tool and video below. If you are in 2008 its a bit more involved, and I wouldnt advise the NHS Employers modeller for this as for 2008 it ignores reckonable pay so is wildly innacurate. Adjusted income is THRESHOLD plus deemed PIA pension growth accross both schemes plus any other pension growth or SIPP contributions etc. The free tool below will help you calculate this.

7️⃣The free tool below will help you estimate your threshold and adjusted income, so see if you can expect a liability for 24/25 (due Jan 26, scheme pays Jul 26)

WHY IS THIS SO IMPORTANT in 24/25

Because of the 23/24 pay award paid in 24/25 and DDRB 24/25 many people will have VERY LARGE PIAs - Im year 14 (just) and my PIA is over £150k. That means if you go over THRESHOLD income, when you add in the PIA, tapering can be BRUTAL and reduce your allowance from £60k down to £10k - that might increase your AA tax charge by £22,500 (45% x £50k reduction).

So if your THRESHOLD income is CLOSE to £200k you can still DURING THE TAX YEAR ONLY i.e. the next 9 days or so make a SIPP payment to reduce it below threshold income to avoid tapering. Say your THRESHOLD income (step 5 above) is £210k you could make a £11k GROSS SIPP payment which would reduce your threshold income to £199k which could reduce your AA liability by £22.5k making the SIPP free.

See the worked examples in the video below

Free tool and video to work all this out is below

Free Tool: https://t.co/rVC2FzNF84

Self help video: https://t.co/UB9dqIyke5

Eurosiva course on IV anesthetic pharmacology & perio-op monitoring, “Make TIVA simple again”

CME EACCME®️ - 15

Lisbon, 2 days before Euroanaesthesia 2025

Interested in TIVA, anesthetic pharmacology, & perio-op monitoring?

Register & program 👉 https://t.co/HYoaWK7qDb

Most RSIs don’t need to be that quick.

Some do.

Are you training — or training others — to be slick ‘n’ quick if you’re faffing with pumps and TCI model theory?

Wonder if anaesthesia has gotten a little obsessed with training “off piste” before on the nursery slope.

1/ V. Important 🧵 if you are CONSULANT in England. This week I used my FREE modeller to identify & correct an error in #AnnualAllowance for 24/25 which I suspect may be a common error. It will save me over £2,600 from my AA liability, buckle up & see if you are affected

Ps RT

4/ You are going to need to my new free tool which models 23/24 and 24/25 AA since NHS pensions havent sent out "brown envelopes" for pension savings, and you need this for self assessment.

Instructional video: https://t.co/6QwfPPdwWK

Free Tool: https://t.co/qXxndVfVbF

IMPORTANT: Despite unprecedented failures @nhs_pensions admin in #AnnualAllowance this year, you're STILL required to self-assess by HMRC by 31st Jan 25

FREE help/tools 👇

Instructional video: https://t.co/6QwfPPcZ7c

FREE Tool: https://t.co/qXxndVfnm7

Pls RT/shr/whatsapp/FB

Who are your role models?

Has a trainer or colleague given you outstanding support?

Dr Sarah Thornton, Chair of our Nominations Committee asks you to recognise the achievements of those who have inspired you.

Find out about our awards 👇

https://t.co/wuuMrXcplf

@drmumsjt

1/ NEW & IMPORTANT: Join me this evening at 7pm Thursday for the pre release of this new free tool! Please share / RT (and D/L your TRS!) 👇

Key links:

Free pre-release tool: https://t.co/rVC2FzNF84

Request on demand: https://t.co/M5JI0pPGgK

7pm link: https://t.co/jdTmNd6Xki

Eleveld TCI model is useful for patient with extreme BW, & avoids BW adjustment problems w/Marsh or Schneider. But most hospitals are not equipped with an Eleveld TCI pump yet.

https://t.co/4zrK2ZezXO bridges this technological gap. It enables Eleveld TCI using any syringe pump.

There are 7.57 million people on NHS waiting lists.

Doctors want to work extra hrs to reduce the backlog, but are taxed up to 70pc for doing so. This means they are working more hours for less pay.

@RachelReevesMP tax rules are jeopardising NHS targets.

https://t.co/Ljrgzhx53I