The death of SaaS has been greatly exaggerated. Despite AI-driven fears, 56% of respondents expect to build less software and buy more from vendors (35% structural) vs just 17% planning to internalize more. 27% see no change in their build-vs-buy mix.

The AI boom is fueling extraordinary profits, but free cash flow is under pressure. Hyperscalers fund record capex while earnings climb. Trailing 4Q FCF peaked in early 2024 and is set to fall sharply — one reason AI looks like an earnings bubble, not a valuation bubble.

Dealers sit in moderately negative gamma, growing more short on downside — delta selling through weakness that amplifies declines. Upside is more nuanced: positioning turns supportive early, but a larger squeeze could force aggressive delta buying, fueling the move higher.

Tech selling. After being extremely stretched only recently, mega-cap growth & tech positioning has collapsed sharply, settling back at neutral levels (48th percentile).

US CPI paths by monthly pace: after the ~9% peak and the drop toward 2%, inflation is back near 4%. At 0.1% MoM it lands at 3.4%; at 0.5% MoM, 5.9% by 2027. Hartnett (BofA) sees 5% by November — a ~0.4% monthly pace.

How leveraged are the AI hyperscalers? Barely at all.

Net debt has surged to ~$240bn on AI capex. But net debt/LTM EBITDA sits near zero (~0.3x), after years of net cash positions. Earnings power absorbs almost all of it. Leverage is not an issue.

US tech performance vs the S&P 500 is tracking 12M fwd EPS — unlike 2000, when price fully decoupled from earnings. The three classic 'Big Top' signals: Fed hiking 3+ times, credit spreads widening 6–12m ahead, ISM near 60. None of them is present today.

Leveraged ETF AUM is surging toward $300bn, +50% YTD and almost entirely North America. Daily rebalancing has driven >$225bn of demand for global equities in 2026 — already above 2023's full-year record of $130bn, in just 5 months.

1970s US inflation (yellow) overlaid on 2013-present (blue), aligning Apr-2021 with the mid-cycle lull. Back then that lull preceded a second, bigger wave peaking in 1980. Prices are turning back up—and the analog is back on traders' radars.

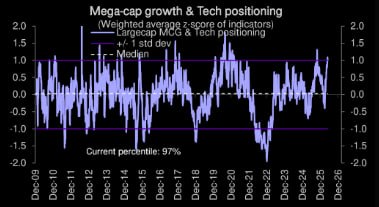

Mega-cap growth & tech positioning is back at the 97th percentile vs its distribution since 2010, with the aggregate z-score above +1 std dev. The market remains heavily long tech.

Q1 2026's earnings beat is shakier than it looks. Hyperscalers' "other income" hit a record ~34% of net income on gains from OpenAI/Anthropic stakes. Strip the AMZN/GOOGL boost and S&P EPS growth was ~16%, not ~25% — and at the median, EPS growth is just ~10%.

In 2022, IT moved inversely to rate expectations: more Fed hikes priced in, worse IT vs S&P 500. Sector ended -30%, ~12pts below market — pure duration sensitivity.

Options markets price ~50% odds of at least one Fed hike by end-2026. Into 2027, the implied probability of one or more hikes is roughly double that of one or more cuts, with "2+ hikes" becoming the most likely scenario by June 2027 (~40%).

Option extremism. Investors keep chasing the rally: call share of total options volume has exploded to ~70%, while put demand keeps collapsing toward multi-year lows. At this pace, puts may soon become an endangered species.

SOX/MAG7: after years of underperformance, semis are taking the helm from the Magnificent 7. The ratio ripped from its 2025 lows to 0.442, a multi-year high. The AI trade is rotating out of mega-caps and into the picks-and-shovels.

Sharp asymmetry in the dealer gamma profile: on an upside move, market makers flip quickly into short gamma, hitting peak short exposure around a +3% spot move. Short gamma means dealers buy as the market rises and sell as it falls, amplifying the move rather than dampening it.

Prime book exposure to semis & semi equip just hit record highs: ~11% gross, ~19% net of total global exposure. Crowding is extreme in a narrow leadership group. The risk isn't broad panic—it's a leadership unwind. Momentum hedges & rotation trades look increasingly attractive.

@Amena__Bakr Three months is also exactly how long it takes for war-risk premia to migrate from headlines into the calendar — front-to-6th spread and tanker rate curves have already priced what the deployment is supposed to signal. Optionality always gets bought before the press release.