After achieving a 103.5% return in the 2023 US Investing Championship and a 254% return in 2024, many of you have asked about the tools I use in my trading process. Today, I’m sharing my personal toolkit! 🛠️

But remember: tools don’t make the trader — they only enhance the skills you already have. If your strategy isn’t sound, no fancy platform will magically fix that.

Let’s dive in! 🚀

@JLawStock Well said. Investing is not a game of cause and effect; it is a game of probabilities. When facing headwinds, why not go hiking in a suburban park?

Core m/m SA at 0.36% above every single economist expectation above, which were already too high for the Fed.

No "confidence" gained by the Fed for 3 months now.

@fkronawitter1 Weekend thought: There is actually another reason to buy long-term bonds, and that is the cross-border bond buying demand brought about by overseas central banks such as the ECB and the BOJ starting easing cycles earlier.

@fkronawitter1 That's what I've been saying for the last six months. Our government invented a lot of words, but no real action. Most of these words come from XI's experiences in the countryside when he was young, which makes many investors very confused and do not know how to understand.

Third, post-real estate transaction consumption expenditures, such as furniture and home appliances, which have seen a decline in both volume and price over the past year, are likely to see a revival in sales and inventory demand.

This would benefit related service industries like intermediaries, moving services, and insurance, leading to a rebound in employment and added value in these sectors.

First, developers are accelerating construction amidst low inventory and high prices, boosting real estate investment. Second, as supply increases and mortgage rates decline, stimulating demand, real estate sales and transactions are expected to improve.

IF the U.S. real estate market rebounds, it could strengthen the sustainability of economic growth, potentially exceeding market expectations even without additional fiscal support. This recovery would be driven by several factors.

@fkronawitter1 I wonder if it would be better to express the Fed's doves directly through the ITB? The residential sector is not highly leveraged, the labor market is not bad, housing inventory is low... Lower interest rates, good for home sales

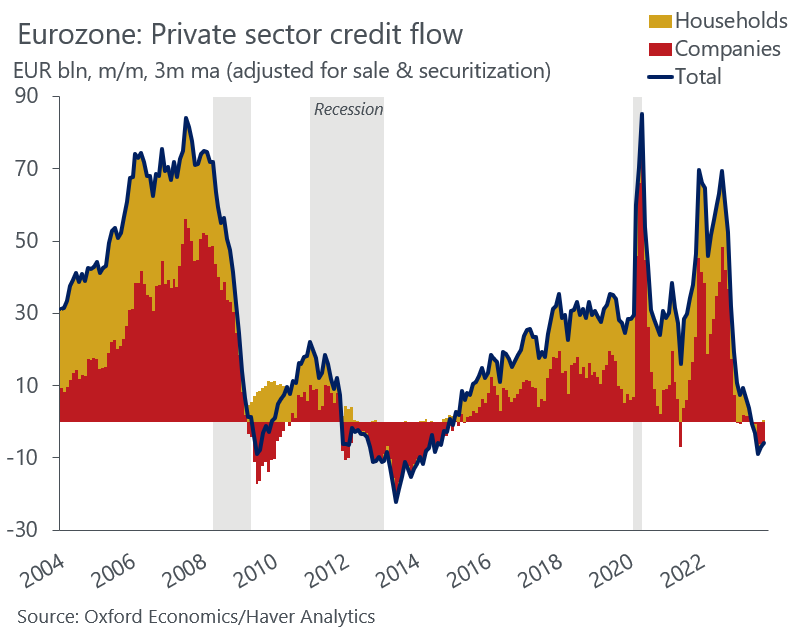

In a credit-based system, when credit to the private sector contracts, a recession follows. Q3 GDP was already negative in the Eurozone, so we're halfway there. Pandemic-era cash buffers make this cycle different, but a weak global backdrop and forces of gravity are hard to defy.

At this time, banks/financials can no longer be regarded as leveraged bonds and continue to attract allocation needs from insurance companies and pension funds. The rapid decline in JGB interest rates is not surprising.

That could happen again in China

Both the reduction of mortgage interest rates and the sharp decline in housing prices are the process of declining investment returns and rising debt risks in the old economy.