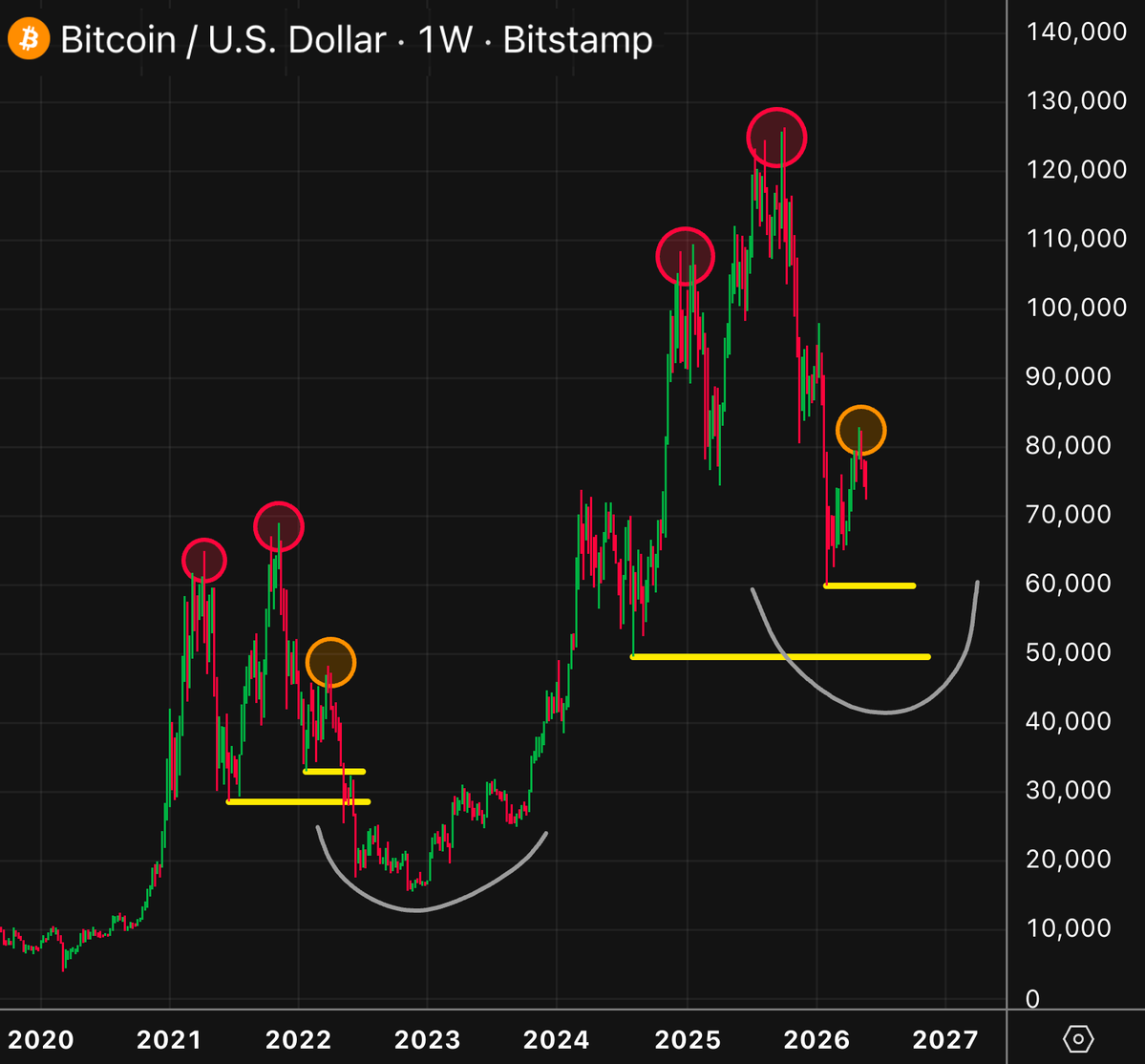

$ETH 20000$

$LINK 200$ End bull run

$XRP 3$ Mid-End bull run

$ADA 4$ Mid bull run (sell half to to ETH and LINK)

$SXP 6$ Mid bull run (sell all to ETH and LINK)

$RKLB has never been better positioned than it is right now imo:

• Record backlog

• Record cash for acquisitions

• Best yearly Electron cadence ever

• Closer than ever to Neutron's first launch

• Included in the Nasdaq 100

And yet, still ~32% down from its all-time high, meaning ~47% upside to reclaim it.

What's happening in the PC/Laptop Market

Sales & Growth

I expect unit sales to grow by 1%-2% YoY in 1H26 due to order pull-in and inventory buildup

Large inventory buildup is happening at the distributor level in 1H26 before 2H price hikes

We will see large production cuts at the OEM/ODM level in 2H26 as price hikes cause demand destruction

2H 26 sales will be down by 15%-18% YoY at least

Factors causing Price Hikes

As y'all know, contract DRAM/SSD prices are up by 200%-300% since mid 2025

Intel has raised the prices of its entry-level CPUs by 15%

ABF/IC substrate prices are up 20%

Effects of Price Hikes and the Current Market

OEMs are prioritizing higher-end SKUs to pass costs and protect their margins

Commerical/Enterprise segment is strong due to Windows 10 EoL and Win 11 refresh

ASPs are up by 17% compared to 2025, but margins and unit sales will go down

OEMs are downgrading memory & storage specs (less 32GB/16GB DRAM and 4TB/2TB SSD configs)

Apple is an exception due to their robust supply chain and bargaining power

MacBook Neo is gaining market share and shipments have been revised up from 5M to 10M

Future

Smaller players will continue to get squeezed by the larger players due to their supply chains and bargaining power

Low end segment (sub $600) will undergo an extinction event due to CPU/memory price hikes and MacBook Neo (No Chromebooks anymore)

Consumer segment will undergo a forced premiumization as vendors shift their focus towards higher end SKUs

Replacement cycles will be extended due to higher prices

AI PC adoption will be delayed due to price hikes

I don't expect a normalization of the market till 2028 and 2027 will be worse than 2026

I think $NBIS is a $600 stock by the end of the year, and the math is pretty simple.

Start with where it sits. A company growing revenue 684% year over year with $7 to $9 billion ARR guidance for 2026, the most blue chip customer list in AI infrastructure, and the largest owned data center buildout in the sector.

The foundation is already in place. Now look at what is coming.

Catalyst one. The Pennsylvania 1.2 gigawatt AI factory begins contributing. Every gigawatt that comes online is a step change in revenue capacity. This is the single largest piece of new capacity in the pipeline.

Catalyst two. The Meta contract ramps. The $27 billion deal is the largest in company history and it has barely started flowing through the numbers. As it ramps the revenue line re-rates hard.

Catalyst three. New capacity announcements. Nebius is targeting 4GW of contracted capacity by end of 2026. They are nowhere near that yet. Every new site, every new power agreement, every new hyperscaler contract is a catalyst between now and year end.

Catalyst four. The EBITDA inflection. They just flipped from a $53 million loss to a $129 million profit in a single quarter. The market re-rates hypergrowth companies dramatically when they cross into sustained profitability. That transition is happening right now.

Catalyst five. Analyst target chase. Citi already at a street high $287. Goldman raised 2027 through 2030 estimates by up to 54% in one move. Every quarter the company outruns the model and the banks raise again.

That cycle pushes price targets toward and past $400 through the back half of the year.

Run it forward. $9 billion ARR by year end at 20x revenue is $180 billion. As Pennsylvania ramps and the Meta deal flows the forward numbers support a market cap well north of that.

At a $600 share price this is roughly a $150 billion market cap on a company with the trajectory and partners Nebius has. That is not a stretch. That is the base case if execution continues.

684% growth. The buildout accelerating. The most important tech companies on earth as partners. The EBITDA inflection underway.

$RKLB

This is your last chance. After this, there is no turning back.

You take the blue pill — the story ends. You wake up in your cubicle, believe it’s impossible to compete with SpaceX.

You take the red pill — you stay in Wonderland… and I show you how deep the Neutron rabbit hole goes.

$ETH 1W chart | Big Picture

$ETH has been trading between $1-5k for 5 years now, and I believe this is just one giant Accumulation - Flat Correction (ABC)

My focus now is on this Rising Channel within the giant Accumulation and I think this year $ETH will break the Channel’s Support 📉

That will be the final Capitulation we need to end the Bear Market 🐻❌

My $ETH Downside Target for 2026 hasn’t changed — $1000-1300 (Buy Zone) 📍

It may go even lower and sweep the 2022 low, but I don’t count on that.

🎯 2027-2029 Bull Market Targets: $7.7k - $9.9k - $14k

I just initiated a brand-new 'Power Grid' position in my family portfolio.

The company is under $10B, growing revenue over 100% YoY, sitting on a record backlog and booking more than twice as much business as it ships.

Any guesses?

Here is an investment that will very likely 10x in 2–3 years

$ASTS $83 -> $830

$RKLB $124 -> $1240

$PL $41 -> $410

$STM $61 -> $610

$NBIS $219 -> $2190

Save it for 2029!