Quantum BioPharma $QNTM has filed a major lawsuit against banks/brokers for possible market manipulation and possibly naked shorting its stock on October 20th, 2024. Our market cap was over USD$ 1 Billion and has been reduced to now around USD$ 10 Million. We seek damages in excess of 700MM USD.

Some salient points are

1. Quantum Biopharma (Nasdaq: QNTM) (CSE: QNTM) on 20th October 2024 files a US federal lawsuit against CIBC World Markets. RBC Dominion Securities Inc. and others for alleged stock price manipulation/spoofing. The case has been filed in the Southern district of New York. These banks named are the American counterparts of the Big Canadian banks

2. Christian Attar Law Group believes this is one of the top 5 biggest case for stock price manipulation/spoofing that they have seen in the past 21 years that they have been prosecuting market manipulation complaints

3. The damages being claimed are more than $700,000,000 USD (Seven Hundred Million US Dollars)

4. The law firms Christian Attar and Freedman Normand Friedland LLP have decided to take and file this case on a contingency basis so there will no material financial pressure on the Company to bear the legal costs associated with this case. This speaks volumes about the strength of the case

5. These law firms, working with industry experts, conducted an extensive investigation into the Defendants’ conduct, and have concluded that there is sufficient evidence of market manipulation for the Company to pursue claims against the Defendants.

6. The company’s stock in January 2020 was trading over $460 USD (taking into consideration post-splits or present terms) per share with a market cap close to almost One Billion dollars. The Company’s share price as of market close today Dec 03, 2024, was $4.470 USD per share with a market cap of less than $10 Million USD.

7. The company believes that besides CIBC and RBC there are other banks/brokers who are also involved in this alleged market manipulation scheme in the company’s stock. One of them possibly is the one that was served a very big fine by US regulators. The company will refrain from naming them at this point until more conclusive evidence has been gathered.

8. Even after filing the court case these banks have kept on with their market manipulation of our stock and we see our stock being shorted and manipulated on almost a daily basis. This is how much disregard these institutions have for regulations and have no fear whatsoever of any persecution.

9. The work we are doing can possibly save lives in the future but being constantly battered by these institutions is hindering our ability to do anything.

You can access the link below to see the interview I gave for further insights

https://t.co/BrvojC5gfN

Copy of the complaint, the PR and other stuff can be found on the Quantum Vs Banks Page of our website

https://t.co/qMV3Z0oYPj

Over 9,000 People Are Urging President Trump to Implement a Temporary Ban on Short Selling to Investigate NAKED SHORT SELLING 🚨

Like 👍 if you think Trump should take immediate action on naked short selling

📣📣PATRICK BYRNE KNOWS EXACTLY WHAT IS GOING ON AND HOW TO STOP IT IN A WEEK

NAKED SHORT SELLING IS ILLEGAL 🚨🚨🚨

@PatrickByrne would have been the ultimate choice as the

SEC Chairman not Paul Atkins who has a very questionable past.

But to the best of my knowledge was not even considered. Sadly Patrick has openly said he wouldn't want the job. But he would have been great as he knows with first hand experience the level of corruption in the Capital Markets and Regulatory agencies.

SEC COULD FIX IT BUT CHOOSE NOT TO‼️

These FINRA fines are a joke.

Pictet - $610,000 fine

Blue Ocean - $550,000

For $300 Million in transactions and more than $150 Million Shares.

FINRA never says what companies’ were impacted or by how much.

“According to FINRA, between February 2022 and March 2023, Pictet executed approximately US$300 million worth of transactions, involving over 150 million shares.

Those transactions included US$30 million in over-the-counter (OTC) securities — with more than 70% of these trades being executed through an affiliate’s omnibus account, which was used by some clients that were financial firms based in jurisdictions known for financial secrecy…..”

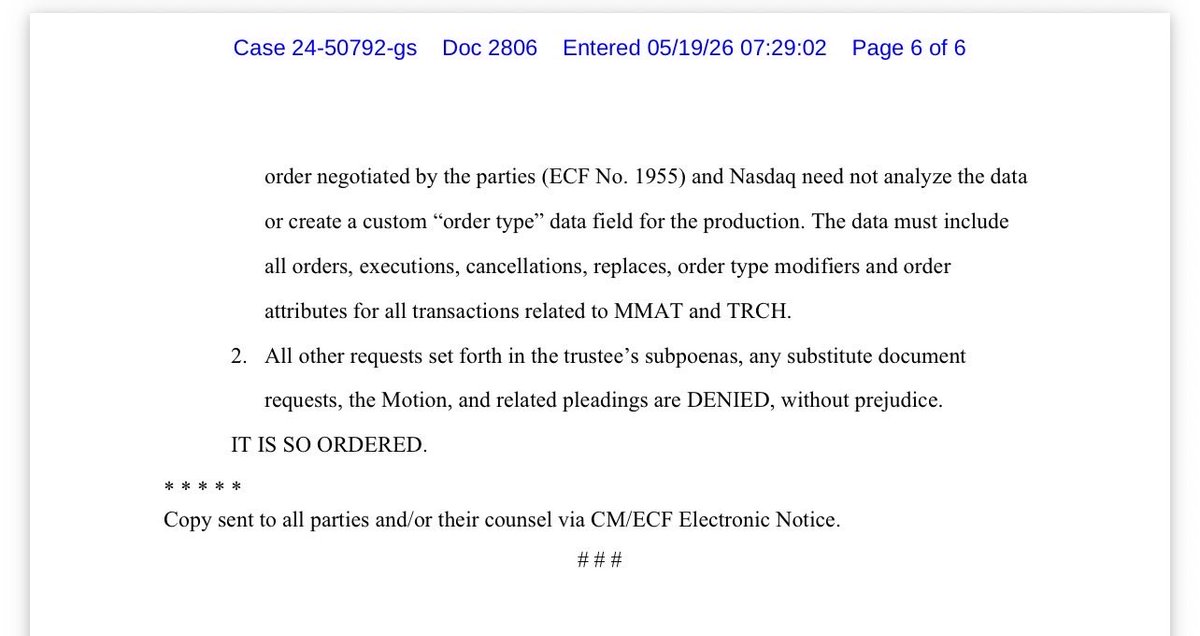

🚨Breaking news: 🦋

@Nasdaq just LOST its Motion to Quash.

Read that again s l o w l y . . .

The Bankruptcy Court in Nevada has now ordered Nasdaq to produce extensive $MMAT/TRCH trading data under Rule 2004, including RASH and CORE data, order attributes, cancellations, replaces, executions, and related transaction records covering nearly FOUR YEARS.

The Court was NOT persuaded by the ‘undue burden’ argument, noting that producing ~15GB of spreadsheet data is not exactly impossible for… Nasdaq. (One $10 usb stick)

Even more important, the Court explicitly recognized the Trustee’s AUTHORITY to investigate whether wrongdoing occurred on behalf of the estate, including potential claims tied to stock trading activity.

Translation:

This investigation is very much ALIVE.

For months, some people mocked and undermined the Trustee’s efforts, claimed discovery would never happen, and acted like every subpoena didn’t get served initially and that it would be crushed before daylight. Instead, the wall keeps cracking.

FINRA discovery.

Now Nasdaq discovery.

And the Court explicitly referenced separate pending motions involving Citadel, Virtu, and Anson.

Interesting times ahead.

Turns out Rule 2004 is not just a decorative suggestion.

To the Trustee and legal teams, incredible respect.

It takes courage to walk into rooms filled with institutions that have virtually unlimited resources and say:

‘Produce the data’

And to the echo chambers already warming up their spin machines tonight…

You may want to read the actual order first. 🤝

Blessings to all.

Quantum BioPharma Reaches Key Midpoint Milestone in Groundbreaking Imaging Study with Massachusetts General Hospital

Promising Early Data Strengthens Potential of Novel PET Technology to Advance Development of Lucid-MS for Multiple Sclerosis

https://t.co/iZ1c9GlVlY

#MGH #Harvard #Biotech #MS #MultipleSclerosis #PETStudy #PETtracer #Demyelination #LucidMS $QNTM

$MMTLP @realDonaldTrump@POTUS@WhiteHouse@JDVance@VP

Dear President Trump

On behalf of the MMTLP community, They write to you today as proud members of the MMTLP community who are the teachers, firefighters, veterans, small-business owners, and working families who placed their hard-earned savings into the U.S. capital markets with the expectation of fair play, transparency, and honest oversight. A formal letter from the MMTLP community—now sits on your desk. That letter respectfully requests your signature and leadership in demanding full transparency and accountability regarding the events surrounding the trading halt and subsequent collapse of MMTLP. The documented retail losses exceed $5 billion, yet no comprehensive investigation has ever been completed, no responsible parties have been held to account, and the American public still has no clear answers about how a listed security was effectively erased from the market overnight.We know you have spent your career fighting for Main Street against the entrenched interests of Wall Street and unelected regulators. Your commitment to draining the swamp and restoring fairness to our financial system is exactly why we turn to you now. Signing the MMTLP community letter would send an unmistakable signal that retail investors will no longer be treated as collateral damage in a system that protects the powerful while leaving ordinary Americans to bear the losses. Mr. President, your signature on that letter would be more than a formality—it would be a declaration that the voice of the American investor will finally be heard. It would restore confidence that the markets belong to the people, not to a select few who operate behind closed doors. We stand ready to support you in any way possible to ensure this long-overdue accountability becomes reality..Thank you for your time, your leadership, and your unwavering defense of the American people. We look forward to your prompt action on the MMTLP letter currently before you.

Sincerely,

Retail United Advocacy Group and millions of investors worldwide.

On behalf of 68 thousand of MMTLP investors. https://t.co/wdUOW9H5Tq

🧠🧵 Lessons from the Front Lines: Wall/Bay Street’s Darker Side

When regulators don’t refute the claims… they silence the claimant.

Let’s walk through actual court filings. 👇

1/

This isn’t a theory.

This is from filings involving the BCSC and OSC.

Instead of addressing alleged market misconduct…

👉 They went to court to restrict communication.

2/

Read what they’re asking the court to do:

“Mr. Bockhold be restrained and enjoined from contacting the Commission Applicants…”

“…including commissioners, employees… and their family members”

Not investigate.

Not rebut.

Restrict. Silence. Contain.

3/

They go further:

“may only communicate… by sending email communications to [official addresses]”

Translation:

👉 You don’t get access

👉 You don’t get dialogue

👉 You get a controlled inbox

4/

Now look at how they frame the individual:

“complaints were often voluminous, repetitive and contained much extraneous information”

Classic tactic:

Discredit the messenger

→ Avoid the message

5/

They admit this has been going on for YEARS:

“Since 2014, staff… have spent significant time reviewing each of Mr. Bockhold’s complaints”

So:

👉 A decade of complaints

👉 Multiple reviews

And still… no transparent outcome.

6/

Instead of conclusions, we get this:

“did not find evidence of the alleged collusion”

“insufficient evidence to warrant additional technical review”

No detail.

No disclosure.

No accountability.

7/

Then the narrative shifts:

“conduct… has reached a level of abuse and harassment”

This is the pivot.

From:

👉 Market allegations

To:

👉 Personal conduct

8/

Why?

Because once it becomes about “conduct”…

They never have to answer:

👉 Short selling mechanics

👉 FTDs

👉 Prime broker activity

👉 Market maker balance sheets

9/

And here’s where it escalates:

Contacting “family members” and “threats of further litigation”

This is the justification they need for court intervention.

But ask yourself:

👉 Why does it get to this point?

👉 Why no transparent resolution earlier?

10/

Even internally, they admit:

“finite public resources”

“time, energy and expense”

That’s the real issue.

Not the claims.

👉 The cost of dealing with them.

11/

And here’s the key move:

“the BCSC could further restrict his communications”

Not:

❌ “we will investigate further”

❌ “we will publish findings”

Instead:

👉 We will limit your voice

12/

This is how systems defend themselves.

Step 1: Ignore

Step 2: Dismiss

Step 3: Reframe as “problematic actor”

Step 4: Legally contain

13/

Meanwhile…

No ruling on:

❌ Market structure

❌ Naked shorting

❌ Institutional conduct

Just…

👉 Who gets to speak

14/

If regulators are confident…

Why not:

✔ Publish findings

✔ Address claims directly

✔ Show the data

Instead we get process over substance.

15/

This isn’t about one case.

It’s a pattern:

👉 Control narrative

👉 Avoid engagement

👉 Protect the system

🧠 The question isn’t whether you agree with the claimant.

It’s:

Why won’t the system engage on the facts?

#Canada #Markets #BCSC #OSC #WallStreet #BayStreet #ShortSelling #MarketStructure #FTD #Transparency #Finance @BCSC_Info@ontariosec@brianlilley@CBC@CTVNews@TorontoStar@zsaeed@mario4thenorth@Martyupnorth@stockmannnbroo@kshaughnessy2@annvandersteel@Malone_Wealth@_cvpaynes___@cvpayne

🧠🧵 Lessons from the Front Lines: Wall/Bay Street’s Darker Side

Short & Distort isn’t a theory. It’s a structure.

1/

For months I’ve been documenting the same pattern:

👉 short reports

👉 coordinated selling pressure

👉 price suppression despite volume

👉 liquidity that disappears when needed

This isn’t random.

It’s structural.

2/

Now it’s not just observation.

It’s being litigated.

Case in point:

Northwest Biotherapeutics v. Canaccord Genuity et al.

Allegations include:

• spoofing

• fake liquidity

• price suppression

🔗 https://t.co/5KdLSKLKGj

3/

Defendants included major players:

• Citadel Securities

• Virtu Americas

• Canaccord Genuity

• others across the market-making stack

Not fringe.

👉 This is the system.

4/

The court didn’t dismiss everything.

Key claims were allowed to proceed.

👉 A U.S. federal court found parts of this plausible enough to litigate

5/

Now layer in:

Honig v. Anson Funds Management

A separate lawsuit alleging a multi-year “short-and-distort” strategy.

6/

Different case.

Same structural questions:

👉 Who is positioned first?

👉 Who controls liquidity?

👉 Who controls narrative timing?

👉 Who benefits?

7/

And this isn’t isolated.

The SEC has already taken action against Anson entities for misleading disclosures tied to relationships with activist short publishers.

8/

Now look at what independent compilations (marketfrauds, Bockhold materials, affidavits) keep pointing to:

Not proof.

But patterns:

• coordinated narratives

• pressure campaigns

• repeat appearances across names

9/

Now connect the structure:

Hedge funds → directional pressure

Dealers → capital + execution

Market makers → liquidity + spreads

Media/research → narrative impact

10/

When the same ecosystem can:

👉 raise capital

👉 trade the stock

👉 provide liquidity

👉 amplify narratives

👉 profit from volatility

You don’t need coordination.

👉 You get aligned incentives.

11/

And this is where people get it wrong.

They scream “manipulation.”

Instead of asking:

👉 Who controls flow?

👉 Who controls liquidity?

👉 Who benefits?

12/

Now add a critical structural point:

Based on documented participation across deals,

Anson appears repeatedly alongside dealers like Canaccord in capital markets activity.

13/

That’s not an allegation.

It’s a structural observation:

👉 repeat participation

👉 concentrated relationships

👉 recurring overlap

14/

And when the same players show up across:

• capital raises

• trading activity

• short-side pressure

The relationship itself becomes part of the story.

15/

Now zoom out even further:

In situations like MMTLP, firms like Jane Street are reportedly retaining legal counsel around unresolved trading/settlement issues.

16/

That matters.

Because when major liquidity providers are lawyering up you’re not looking at a one-off.

You’re looking at stress in the system.

17/

Then Canada moves in the opposite direction.

CIRO steps away from mandatory buy-ins / forced close-outs.

18/

Translation:

❌ No hard settlement enforcement

❌ No forced close-outs

✔️ More reliance on dealer discretion

19/

So if:

• short pressure exists

• narratives move price

• settlement discipline weakens

What forces equilibrium?

20/

Because without forced buy-ins…

you don’t need manipulation.

You just need:

👉 time

👉 pressure

👉 liquidity advantage

21/

Now layer in optics.

Doug Ford appearing at Moez Kassam’s home (per Moez’s own public post).

Toronto Life elevating the same figures as top-tier influence.

22/

Not an accusation.

A transparency question:

👉 How do capital, media, and political access intersect?

23/

And where are:

• OSC

• CIRO

• RCMP

in terms of clear public response?

24/

Not accusing.

Just asking:

👉 What’s being investigated?

👉 What’s been concluded?

👉 What’s being communicated?

25/

Final thought:

If positions come first…

liquidity shapes price…

narratives arrive on time…

and enforcement weakens…

26/

Are markets reacting?

Or being led?

🔥 #WallStreet #BayStreet #MarketStructure #ShortSelling #ActivistShorts #HedgeFunds #Liquidity #Finance #CapitalMarkets #Trading #Transparency #CIRO #OSC #RCMP #MMTLP #NWBO

@SECGov@TheJusticeDept@FINRA@OSC_News @CIRO_org @RCMPGRCPolice@fordnation@whisskier@annvandersteel@Malone_Wealth@zsaeed@stockmannnbroo@_cvpaynes___@cvpayne