Quantitative Easing (QE), whereby the Federal Reserve buys US Treasuries to finance the U.S. government’s deficit spending, is essentially printing money without restraint.

By contrast, a revaluation of the gold owned by the US Treasury (8,133 metric tons) would provide the US government with a finite liquidity boost; approximately $1 trillion at a gold price of $4,000 per ounce. Issuing gold bonds would theoretically impose discipline on U.S. government spending, because the gold would eventually have to be repaid.

Consequently, QE and unchecked deficit spending erode foreign sovereigns’ confidence in US Treasury bonds, while a US Treasury gold revaluation and the issuance of gold bonds would strengthen that confidence.

It doesn’t matter what regular people think of this. They are not foreign sovereign buyers of U.S. Treasury bonds.

The Milkshake Theory idiots believe the U.S. Treasury market has zero problems. Meanwhile, the Gold bugs think it won’t get a bid no matter what. They are both wrong.

The reality is that there is a serious problem in the U.S. Treasury market. However, the U.S. government can still nudge it back into controllable territory by shrinking the Fed’s balance sheet and raising rates; both of which can only be achieved through a UST gold revaluation and the issuance of UST gold bonds in this juncture.

Trump can revalue the U.S. Treasury’s gold without Congressional approval.

#Gold #Silver

What we are watching in markets are the first cracks in the illusion that the US can fund $2T deficits in perpetuity, fund debt-funded AI buildouts, reshore the industrial base, fund the Iran war, and roll over existing US Federal debt without YCC or its functional equivalent.

"We make the best graphene in the world"

Graphene is a "miracle" material 200X stronger than steel, lighter than aluminum and 20X more conductive than copper

Hydrograph Clean Power HGRAF https://t.co/FP1WyypC4n

Hydrograph SNYTHETIC pure graphene will produce 70% to 90% bottom line profit margins.

When you attempt to compare Hydrograph’s graphene to others you realize that there is NO comparison.

"We make products lighter, faster and stronger."

Hydrograph has patented the evolution of material science

Christopher M. Sorensen Kansas State University Inventor of HydroGraph Graphene Technology

Watch Youtube https://t.co/IjFZDO7daN

Is Graphene the new OIL ?? https://t.co/QFZd7LM96v

Hydrograph video Nuclear Scientist Kerry Landis and Newsletter writer Jay Taylor Excellent

https://t.co/KYW04aaNxJ

Jay Taylor "HydroGraph is indeed the most exciting and transformative company story I have covered over the past 40+ years that I have edited J Taylor’s Gold, Energy & Tech Stocks."

Kerry Landis Nuclear Engineer : "...... I've looked deeply into Hydrograph....... And, and my conclusion, and you'll hear more about it today is that this is probably, no, it is the best growth opportunity I've seen in 40 years."

”I’ve been investing for 30 years and studied the broad history of the best stock stories over the centuries. There has never been a better story.” - Kevin Bambrough on HydroGraph

#copper #PH #Investing #100Baggers #Healthcare #ValueInvesting #Stocks #multibaggers #MadAboutStocks

#CleanTech #GrapheneRevolution

#hydrograph #nanomaterials #alternativeenergy #superconducting #conductivity #electronics

$UEC The Uranium & Nuclear stock squeeze is going to be parabolic for this tiny sector. Everyone is focused on AI power demand, but according to the IEA, data centers rank only 5th in projected electricity demand growth through 2030 on the low end!

AI isn't competing for power in a vacuum. It's competing with the entire growing world with even bigger demand for basic needs.

The market is massively underestimating how tight electricity markets will become. Clean baseload energy is going to be the next big investment from big tech as governments push back on emissions. We also have a massive deficit of Uranium 2.3 billion lb deficit by 2045. $NNE $SMR $OKLO $LEU

BREAKING NEWS

THE EUROPEAN CENTRAL BANK IS WARNING THAT THE UNITED STATES RISKS TRIGGERING FINANCIAL CRISIS WITH IRAN WAR

Interesting that they would say this out loud. 🤔

The TAM for turbostratic fractal graphene is just so ridiculous… the more deep work my team does, the more ridiculous the NPV’s become. The wait is going to be worth it.

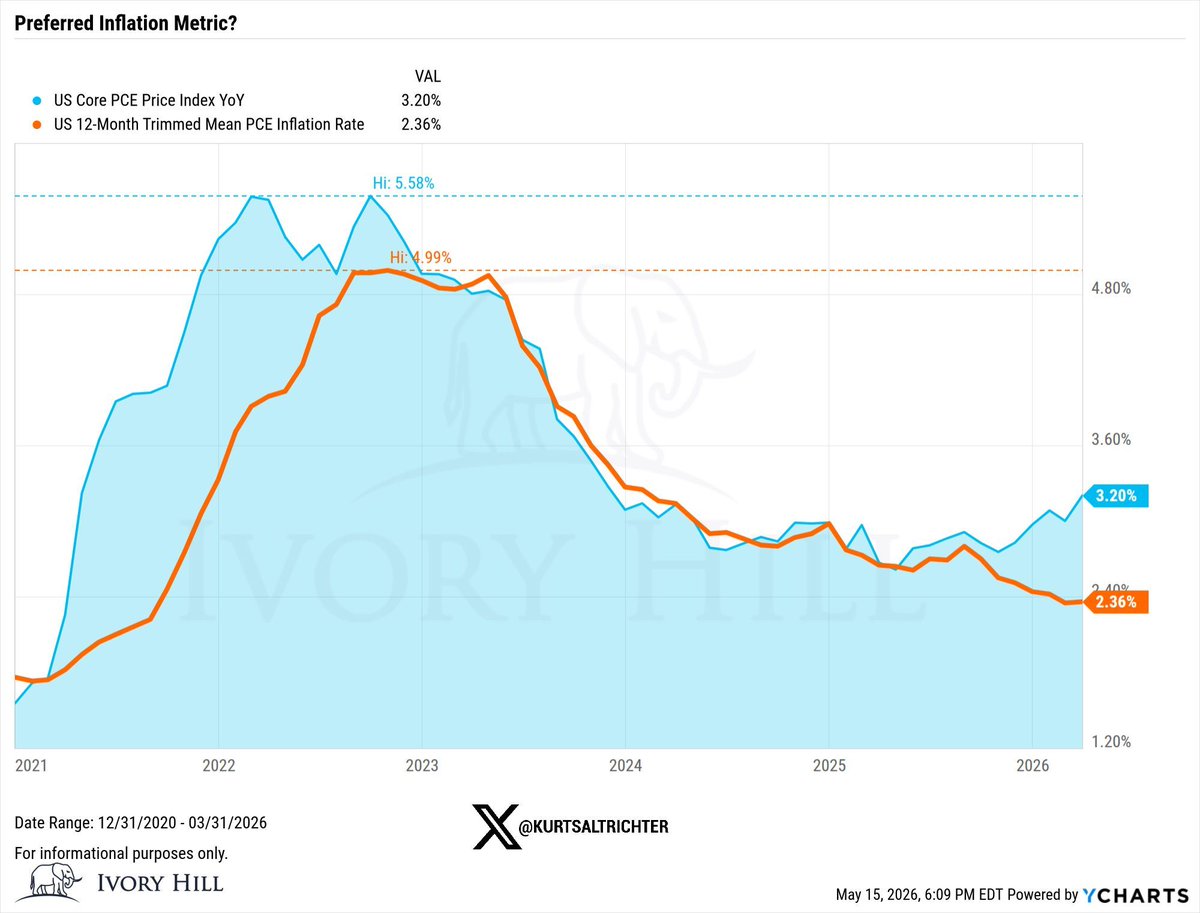

Warsh has signaled he wants to change the Fed’s preferred inflation gauge.

The Fed has used Core PCE, which excludes food and energy, as its benchmark since 2000. Warsh favors Trimmed Mean PCE, which removes the most extreme price movements each month instead of excluding whole categories.

The practical difference: Trimmed Mean PCE currently reads 2.36%, well below the 3.20% reading on Core PCE. Depending on which measure the Fed follows, the case for rate cuts looks very different.

This is not a minor procedural change. The metric the Fed uses to gauge inflation directly determines when it judges the economy to be at target.

If Warsh moves the committee toward Trimmed Mean PCE, he is mathematically moving the Fed closer to a declared victory on inflation, which creates runway for rate cuts even as headline readings stay elevated.

You’d think with 400+ Ph.D. economists and 500+ researchers on the payroll, the Fed would run the most sophisticated macro forecasting operation on the planet, leaving Bloomberg and every major hedge fund in the dust. Not even close. When the data doesn’t cooperate, just change the data.

Same thing I saw in the Army when time or weather worked against higher leadership, and we would quietly move the goalposts rather than admit the standard couldn’t be met. Can you tell why I didn’t stick around for the full 20 years?

My view on the updated $hg $hgraf presentation

It was worth the wait for EPA. It will be well worth the wait for the gas plant signing and incoming contracts that should roll in post that announcement.

Nobody is putting in huge orders and press releasing tonnage until the capacity visibility is there.

80-85 companies and growing. Many over 1000 tonnes.

These orders will be coming through and the stock is destined for 10x or $20-30 bln market in 12 months or less

There’s many patents in the works too.

At Turbostrata we are in the process of working on some custom masterbatches for products we are developing and hope to launch these as quickly as possible. Our team wants products being sold with 12 months. Some of our products involve drop in masterbatching to OEM manufacturing lines.

With all the chaos going on in the world. It’s tough to get time and attention. Manufactures are struggling with supply chain issues and others grappling with tariffs and many looking at regulations changes. This creates a bit of short term headwind as people are all ‘busy’ dealing with the chaos of the moment but at the same time the macro is for a huge tail wind for $HG graphene. It’s solves so many problems.

PFAS elimination, recyclability, energy efficiency, carbon credits, off setting rare earths, supply chain certainty. USA domestic production. But ability to also produce in Europe and the UK.

Good things come to those who wait.

Some thoughts kept bouncing around my brain as a consequence of following the https://t.co/HoizdB217m $HGRAF boards, and a feeling that many are focused on individual trees and missing the forest. The announcement of HydroGraph’s participation in the Needha conference in NYC this week added more fuel. So thought I’d pan out regarding some catalysts and timelines I’m thinking about.

The big epiphany I had is that there’s a lot happening below the water. I was aware of this before, on a tree-by-tree basis, but suddenly it hit me just how *interrelated* many of these catalysts are—and how smart I believe HydroGraph CEO Kjirstin Breure is. And not to pick on any particular CEO posters, but it was a couple of @BiLoCellHy posts that really opened my eyes. He noted “…it’s a delicate timeline…they need to redomicile before contracts, because the more the company is worth, the more they pay in taxes on the redomicile…”. It’s so obvious, spelled out like that! Even I got it. Love the collective intelligence on the $HGRAF CEO and X boards/communities!

So I spent the weekend thinking about catalysts, what comes when, and how tied together they are—or are not.

Redomicile – Domestic (US) Commercial Contracts – DoD/DoW/DARPA Partnership & RFI Announcement(s) – UK & EU Contracts & Partnerships Announcements – Asian (esp S Korea and Australia) Contracts & Announcements – Institutional Investor Conferences & Related Investment Announcements

The big picture view is that HydroGraph is trying to accomplish several things in the shortish term of 3- to 6-months:

· Maintain and increase the $HGRAF share price. They’ve done a great job of reaching NASD eligibility with minimal dilution, but modestly increasing the share price going into the uplisting will have a significant impact on how post-uplisting investors, especially institutional investors, view $HGRAF as a nice-to-have, must-have, must-have-damn-the-price, or…don’t care/avoid-this-pig. Last is very unlikely, given HydroGraph’s product line, but black swans, good and bad, happen.

· Get the ducks lined up in the proper order. Identify the optimal tax exit from Canada, and overlay it with optimal NASDAQ uplisting, and determine an initial rough timeframe. I’m sure this has already been done. With the possible exception of Kevin Bambrough, no-one on these boards is privy to this info—nor should we be. But if it makes sense for the company’s valuation growth and overall advancement, I’m confident they’ve had this in their collective pocket for at least a month or two.

· Identify key valuation accelerators to the NASDAQ uplisting and start lining them up now. Smaller contracts, like Sparc, can come out immediately. They are great confidence boosters but will have only small impacts on $HGRAF valuation near term most of the time. But large contracts with significant auto companies, small nuclear reactor manufacturers, aerospace companies, and defense-adjacent or outright defense contractors that can be lined up for a series of orders creating an instant backlog will have an outsized impact on post-NASDAQ share price movement.

· In tandem with the value accelerators related to manufacturing and Fractal Graphene demand, announce the signing of the acetylene contract, and a schedule for completion of the Bellville production facility. The timeline should be 6 months or less—and deliverable on time.

· In conjunction with the announcement of the acetylene deal and the production facility expansion, announce placed orders for a large number of Hyperion units, at least 25; 50+ would be better—which lines up with delivering the initial backlog orders within 3 months, if possible, of the Bellville facility’s opening.

· At the same time that the new, large Hyperion order is announced, reveal that the Austin facility has stockpiled significant tonnage to help address the announced product backlog immediately.

These events are somewhat fluid in order. I’m not clairvoyant, nor do I possess inside knowledge. But on occasion I’m okay at connecting dots others have missed. I’d love to hear a productive conversation around this.

@BambroughKevin When is their open house. I attending. I’d like to meet you Kevin. I got in a little later than you but I’ve been accumulating ever since. Phil. Lufkin,Tx

@Paul41583@JayTaylorMedia I would think he probably didn’t have a choice. The interview won’t happen as that would open up legal issues. Jay I appreciate all your work. I to have a large position thanks to Kevin B. Early on.