@AdityaD_Shah In Gold I feel RJ,(Ritesh Jain) view is rational.

US want be manufacturing hub so for this dollar have to be weak and no other currency want to be reserve currency, so Gold is the only option for Net trade balance settlements. So next 5-6 years looks very good for Gold.

30 years in Indian markets. Lehman. COVID. Every crash in between.

@SunilBSinghania lesson?

Volatility isn’t the enemy. Impatience is.

New episode of Wealth by Motilal Oswal

@MotilalOswalLtd

https://t.co/VJ4YhXxF5K

#Deeptech going to deliver massive wealth for investors in coming decade. India has only handful of DeepTech companies.

You need to build expertise around it to make best of it. We started 3 yrs before. Still learning…

Don’t just buy because I’m saying. Work hard and build expertise first. It’s never late. Identifying businesses is easy, riding is difficult. That can happen only if you understand.

After Near Bankruptcy,

Suzlon had a massive turnaround in 2026,

Will the thrust on renewable energy,

Make Suzlon an investment opportunity?

Or

Will Suzlon again disappoint?

A deep dive🧵into Suzlon and what lies ahead?👇

India is not doing well because it does not have an AI or innovation story... this much is obvious at least if you go by what the chattering heads are saying

But is it the truth or just an easy, lazy narrative?

If the only thing working in the world markets is #AI how come so many old economy companies and small cap companies are doing so well globally?

Even with AI the story is no longer with the Magnificent Seven who are just spending stupendous amounts of money in order to remain in the game

It is the suppliers for the huge capex that are booming for now: #semiconductors, networking, hardware your name it

But don't forget these are highly cyclical industries and AI capex may not remain at these stratospheric levels forever

Then there is the question of whether all this spending will ever make economic returns on capital 🤔

The music is still playing but don't forget what happened to all those who are dancing to the mortgage music up until 2008

My Oped in The Economic Times today on the AI story: Myth, reality and outlook

@EconomicTimes@firstglobalsec@fghumsmallcase

I was interacting with a friend working at a startup, and it's horrifying to hear these stories and the pain they go through.

Many companies have unfair practices wherein, if a person wants to leave, his ESOPs are cancelled or reduced. Add to this the huge taxation burden that the employee has to go through, is a big pain point. Usually, the wealth creation is much lesser for the employee versus what he imagined and worked hard for.

I think taxation needs to be really reimagined/reformed in India.

People end up doing really stupid things just to avoid tax because it's so high!

Q-Line Biotech SME IPO opens today.

I recently visited their Lucknow manufacturing facility and spent time understanding the business, management and industry dynamics first-hand.

Some notes & observations from the ground 👇(1/10)

India’s tourism potential is far bigger than most of us realise.

Yes , infrastructure gaps, cleanliness, driving discipline, tourist convenience, ease of payment and general civic discipline remain real and visible challenges. But these are precisely the areas which, if improved meaningfully, can transform tourism into one of India’s largest economic opportunities.

My optimism comes from India’s unmatched diversity and scale. Very few countries offer spirituality, heritage, wellness, mountains, beaches, deserts, wildlife, cuisine and culture all together at this magnitude.

India’s tourism potential goes far beyond just Taj Mahal or Rajasthan palace hotels. Experiences like the Himalayas and Ladakh, Kerala backwaters, Varanasi ghats, Rann of Kutch, Coorg, Andaman Islands, Ranthambore, Jim Corbett, Kaziranga and Gir forests offer something truly unique at a global scale.

Architectural marvels like the Meenakshi Temple, Golden Temple, Kailasa Temple at Ellora and Khajuraho reflect a civilisational depth and artistic heritage that very few countries can replicate.

Places like Bali, Phuket and Vietnam prove what focused execution can achieve.

The raw material is extraordinary. Execution will determine the outcome.

India’s opportunity is even larger -but execution, governance, urban discipline and hospitality standards will ultimately decide how much of this potential we unlock. 🇮🇳

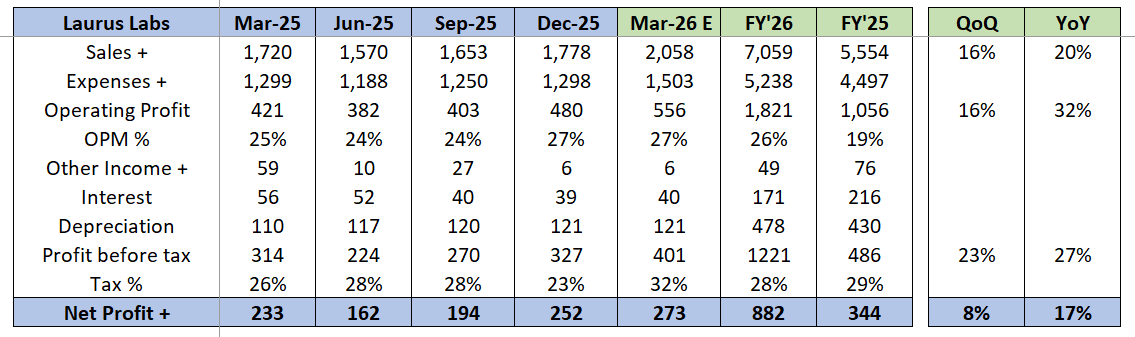

#LaurusLabs is widely tracked… yet poorly understood.

A love it or hate it stock you simply can’t ignore.

My take on FY26 results and Outlook.

A Thread...🧵

68% of India's pharma APIs come from China. The country called the world's pharmacy depends on one foreign supplier for the molecules in its medicine.

PLI for bulk drugs was launched in 2021. Five years in, 27 of 41 approved projects are operational. API import share has dropped from 70% to 68%.

That is not a typo. Two percentage points in five years.

The economics are brutal. China clusters fermentation, intermediates, and finishing in single industrial parks with subsidised power. Indian APIs cost 25-30% more to produce. PLI subsidy partially closes the gap. Partially.

One supply disruption from China and Indian generic exports hit shortage within weeks. The risk is structural; the response is incremental.

You do not win supply-chain wars two percentage points at a time.

If you want to create #wealth

- Stop following Bogus boys, they will only create entertainment for you and not wealth

- Spend time in understanding businesses and not criticizing them

- Find merits in the business and not faults

- Appreciate the efforts of the management and not demean it

- Promoter and founders have put in blood and sweat to build businesses, you can’t judge them using excel sheet

- Finding bad businesses and bad promoters doesn’t have any upside. Let the bogus boys do it.

#LaurusLabs#Q4FY26

Trying to take a stab at Laurus Labs Q4 earnings due on 30th April. Key metrics to watch

1. CDMO share % and growth outlook (~2000 Cr of CDMO Revenue for FY26 as guided by mgt)

2. Growth in Non ARV - Based on last qtr guidance it would be 2600 Cr (+- 200 Cr)

3. Gross Margins at 60%+ consistently

4. While Q4 PAT growth YoY will be subdued due to a 59 Cr one time gain on land sale last year, operating margins growth would be key

Revenue : For this to play out, Laurus would have to hit a topline of 2050-2100 Cr for the March Qtr (Atleast 20% Growth)

Revenue Breakup : CDMO will have to hit 600+ Cr Revenue (Refer Breakup).

Key Risks to watch out for:

1. CDMO revenue is extremely lumpy

2. Feb Export data showed 47% decline in export revenue (Hopefully this is just lumpiness and doesn't impact overall Q4 delivery)

Margins - Confident of Gross margins of 60%-61% based on the revenue mix and guidance from management in last con call. Based on the above, we can expect a PAT of ~250-300 Cr (Refer P&L breakup). This will be PAT growth YoY of ~17% (Optically due to one time gain of 59 Cr in base last year). However, underlying PAT growth would be a massive 44% normalized for it. These are conservative numbers in my view. However, FY26 PAT goes closer to 900 Cr !!!

Anything above 300 Cr PAT will be extremely good in my view. The stock has already run up in expectations and post results, i would expect it to consolidate post results.

Discl: Not SEBI registered. Only for learning purpose. No buy / sell reco. Invested personally.

I can help only genuine learners.

Not those who want stock tips.

I don't provide either free or paid stock tips.

Sorry for that. Stop asking stock names from me.