I make $5.75 an hour doing clapchecks on the register. That's when the clack goes mack on the fitty tack. Is doge a doggie? Goes boom boom up or doom doom down? Please help me, sirs, maams, boogie doo, a poor porn I give and a porn porn I do.

@CommodMkt@biancoresearch@cnbcAsiaTV My suggestion to you would be not to pick fights on X with former Goldman colleagues who know your track record and history.

I am the Senior Director of Strategic Communications for Prime Minister Benjamin Netanyahu.

I have advised four Israeli prime ministers on how to speak to Americans about things Americans pay for but do not wish to look at. I have held this office through three wars, two elections, one genocide ruling from the International Court of Justice, and nine consecutive quarters of uninterrupted American military aid disbursement. My job is to ensure those last two items never appear in the same sentence on camera.

I have prepared the Prime Minister for 312 interviews across 43 networks in 11 countries, and I want you to understand that what aired on CBS on Sunday night was not a conversation. It was a delivery system. I built it. I am very good at my job.

On Sunday, they did not. The $3.8 billion renewed the same week. No vote required. The 365 members of Congress who received AIPAC checks this cycle did not call for one. That was handled before I wrote page one of the brief.

The brief was 94 pages. I labeled it GARRETT — VULNERABILITIES / REDIRECTS. I will walk you through the page numbers that matter because the page numbers tell you everything about what we think an American audience can absorb, and in what order.

Page 7: "TIE SELECTION — NAVY PROJECTS AUTHORITY. AVOID RED (READS AS AGGRESSION ON CBS'S COLOR GRADE)."

Page 14: "BANDWIDTH SATURATION — if the interviewer occupies less than 22% of total runtime, the audience retains tone, not content. Tone is controllable. Content is not."

Page 31: "THE TRANSPARENT DODGE — when a subject announces he will not answer, the audience processes the announcement as confidence rather than evasion." The Prime Minister used this verbatim. He told Major Garrett, on camera: "You're gonna ask me these questions. I'm gonna dodge them second time, third time." The journalist moved on. The question died on tape and nobody performed CPR.

Page 47: "GAZA — PERPETUAL MANDATE FRAMEWORK."

Page 71: "LEGITIMACY DEFENSE — EXTERNAL ATTRIBUTION (BOTS / PAKISTAN / CAMPUS)."

Page 83: "CHILD FOOTAGE SATURATION THRESHOLD — AMERICAN MARKET (Q2 2026 REFRESH)."

I am not going to tell you what is on page 83. I am going to tell you that it contains a number, and the number is updated quarterly, and the number has gone up eleven percent since October 2023, which we noted in the margin as "favorable trend — audience tolerance expanding per exposure cycle." I will tell you that the number on page 83 determines how many seconds of humanitarian content we allow the Prime Minister to address before redirecting to Iran, and that on Sunday that number was forty-four seconds, and that Major Garrett's humanitarian questions received exactly forty-four seconds before the Prime Minister said "Iran" and the conversation left Gaza for the rest of the broadcast.

Major Garrett had a photograph. I know this because we have a source at CBS who confirms segment assets seventy-two hours before air. The photograph was of a building in Rafah. There were small shapes in the rubble that I will not describe to you because I am the person who decides how long you are allowed to look at small shapes in rubble. The photograph received eleven seconds of eye contact from the Prime Minister during taping. That was seven seconds too many. In the final broadcast, the photograph did not air. Forty-four seconds. Not forty-five.

During Saturday prep, when we rehearsed the humanitarian redirect, the Prime Minister checked his watch. He said, "How many more of these?" I said, "Two." He said, "Make it one." We made it one.

I want to be precise about the laugh. When Major Garrett asked how enriched uranium would be physically removed from Iran, the Prime Minister said, "You go in, and you take it out," and he laughed. That laugh was rehearsed three times on Saturday afternoon. The first take, it came too early — sounded nervous. The second, too late — sounded cruel. The third landed exactly where you heard it: between "go in" and "take it out," positioned to make a statement about violating another nation's sovereignty sound like a man who finds the question adorable.

He asked to do a fourth. Not because the third was wrong. Because he enjoyed it. He said, "Again," the way a child asks to ride something one more time. I wrote "again" in the margin and then crossed it out because I did not want a written record of a head of state asking for an encore on a line about bombing a sovereign nation. But I am telling you now. He liked it. The laugh was not performed confidence. It was pleasure.

I noted in the margin of rehearsal three: "Perfect. Sounds like it costs nothing."

That is the job. Making things that cost everything sound like they cost nothing. Making nineteen months of war sound like a reasonable Tuesday. Making $3.8 billion a year sound like the check a neighbor splits at dinner. Making 80,000 dead sound like a denominator in a ratio that favors us.

I did the math once, on a Saturday, because I am the kind of person who does this math. $3.8 billion divided by 80,000. It comes to $47,500 per dead person. I did not write this number down. I did not put it in the brief. But I know it, and now you know it, and neither of us will forget it, and the Prime Minister has never asked.

"One of the lowest in the history of modern urban warfare," the Prime Minister said on camera. I wrote that line. It does not cite a source because the source is us. We are the numerator. We are the denominator. We are the people who decided what counts. During Saturday's rehearsal, the Prime Minister asked me — off-mic, between takes, while adjusting his water glass — "Who counts?" He meant: who does the counting. I told him we do. He said, "Good." He picked up the glass. We moved to the next section.

He also said — and I need you to hear this in full — "We're as discriminating and surgical as any army has ever been in history. No other army." I wrote this line too. He delivered it twenty-three minutes after citing the beeper operation as evidence of precision. Twenty-five hundred Hezbollah operatives had pagers detonate simultaneously in grocery stores, living rooms, and hospital waiting areas. The Prime Minister called this "surgical." He said, "We didn't kill — 2,500 people, but we impaired them, knocked them out with surgical precision, no collateral damage, with the beepers." A mass-casualty device detonated in civilian spaces across an entire country — and on Sunday, this was his proof of restraint. I prepped no redirect for this section because none was needed. The journalist did not ask what happens to the person standing next to the man whose pocket explodes in a bakery. Nobody asked. The word "surgical" did the work. It always does.

I want to tell you what I did not say back. I did not say 80,000. I did not say that I had seen the photographs on page 83 that determine the threshold. I did not say that the number I carry in my head — 47,500 dollars per person — updates every time the denominator changes and the numerator stays the same. I said nothing. That is also my job. Knowing the number and never saying it in a room where it might be recorded.

I want to talk about "two out of four." Major Garrett listed four objectives the Prime Minister stated for Gaza: disarmament, demilitarization, no weapons factories, no smuggling. The Prime Minister said, "Two out of four, largely achieved." He said Hamas "reneged." He said "find me the countries who would do it."

On page 47, this is labeled PERPETUAL MANDATE FRAMEWORK, and I will explain why. If the job is permanently half-finished, the job permanently requires doing. If the job permanently requires doing, the funding permanently requires renewing. Two out of four is not a concession. It is a down payment on the next operation.

Incompletion is not failure. Incompletion is a subscription model. And the $100 million AIPAC has staged for the 2026 midterms ensures that nobody in Congress will ask why we are paying for a subscription that never delivers the full product. That question costs a primary. Nobody wants to pay that price. So the subscription renews.

I want to talk about the phrase I am most proud of. The one I believe earns me another year in this office.

"Every civilian death is a tragedy. For our enemies, it's a strategy."

The Prime Minister delivered this in the third act — the extraction window, where we place lines designed for the fifteen-second clips that will circulate on the networks the Prime Minister just told you are manipulated by Pakistani basements. The line works because it contains its own permission structure. If every civilian death is the enemy's strategy, then every civilian death is the enemy's fault. The munition does not matter. The strike package does not matter. The export license does not matter. The $3.8 billion does not matter. The fault travels backward through the supply chain and lands on the man standing in front of the bomb, never on the man who built it, sold it, shipped it, paid for it, or authorized its use.

I wrote this line in January. It has now been deployed in five interviews. It will be deployed in the next one. And the one after that. Until one of two things stops.

I want to be brief about the "draw down to zero" section because it requires less explanation than you think. The Prime Minister announced he wants to eliminate American military aid over the next decade. He said this while receiving $3.8 billion annually. He said this while $10.1 billion in arms sales were notified to Congress in five months. What he proposed was not ending the money. He proposed moving it from the foreign aid budget — the one journalists can cite, the one protesters can see — into bilateral defense procurement contracts, where the money is larger and the oversight is a locked filing cabinet.

He is not ending the funding. He is moving it to a room with no windows.

The Prime Minister told Major Garrett that declining American support for Israel is caused by bot farms operating from basements in Pakistan. He said this on a network watched by 8 million Americans. He said the 28 million Americans under 35 who oppose unconditional military aid are not Americans with opinions. They are a basement in Karachi with good Wi-Fi.

Basements in Pakistan: manipulation.

$28 million from AIPAC to sitting members of Congress: advocacy.

$100 million staged for midterm primaries with a 98% win rate: democracy.

129 journalists killed in 2025, two-thirds by Israeli strikes: unavoidable.

I want to be precise about this because precision is my profession. The Prime Minister told 8 million Americans that negative coverage of Israel is manufactured by bots in Pakistan. He said this in a calendar year when 129 members of the press were killed covering the conflict, and our forces were responsible for the majority. The coverage is not negative because of basements in Karachi. The coverage is negative because we killed the people producing it. The ones who remain are cautious. The caution looks like balance. The balance looks like both sides. And when Major Garrett presented "both sides" on Sunday, the Prime Minister smiled, because both sides is the product. I built both sides. It is on page 71.

The interview aired at 7 PM Eastern on a Sunday. I watched it from my office with a live-feed monitor split-screened against the CBS control room's framing choices. The Prime Minister hit every mark. The laugh landed. The dodge passed. The bot theory absorbed nine minutes of airtime that could have been spent on body counts. The "two out of four" passed without follow-up. Hezbollah's 150,000 rockets received nine minutes of discussion. Lebanese civilian casualties from our operations received zero seconds. I noted this in real time as a structural win — threat without consequence, exactly as briefed. Forty-four seconds on humanitarian questions. Not forty-five.

I am very good at my job.

I want to tell you about October 7th, because October 7th is the section I am most proud of handling. Every intelligence chief has resigned or been fired. Every military commander in the chain has faced inquiry. The Prime Minister is the only person in the security establishment who held his position before, during, and after the worst intelligence failure in the nation's history — and on Sunday, when Major Garrett asked about accountability, the Prime Minister said, "Everybody bears some responsibility. From the top, from the prime minister down." He paused. He said, "Let's establish an independent commission." I wrote that pause. The pause says: I am being honest. The commission says: later. The combination says: never. The accountability question received ninety seconds and produced no follow-up. Ninety seconds for the worst security failure in Israeli history. I timed it. I budgeted it. The budget was two minutes. He came in under budget. I noted this as a win.

There is one more thing I want to tell you, because I am proud of it and because you will not understand its significance unless I explain it. After the interview wrapped, after the cameras powered down, after Major Garrett shook the Prime Minister's hand and thanked him for his time — Major Garrett thanked him — I opened the brief to the final tab. Tab seven: "JOURNALIST INTEGRATION — POST-INTERVIEW SOCIAL METRICS." I checked the timestamped analytics on Garrett's personal accounts to see if he'd posted anything adversarial within the first forty minutes. He had not. He posted the broadcast link with no editorial comment.

That is not captured. That is not bought. That is something better. That is a man who spent forty-seven minutes in a room with power and left the room believing the room was a conversation.

I build these rooms.

I am very good at my job.

The job is making sure you watch a man describe permanent war and hear a man describe permanent peace. The job is making sure you hear "it can be done physically" and do not ask what "it" has cost every other time that sentence was spoken in a briefing room for the last seventy years. The job is making sure you hear the laugh, not the dead.

You heard the laugh on Sunday.

Eight million of you.

And then you moved on. Just like Major Garrett did.

This might be the craziest thing I’ve ever read on X.

It was already painfully obvious that anything in crypto the Trump family touched was shady at best, but reading this just leaves you speechless.

That’s an insane call out, I honestly can’t tell if it’s brave or just stupid.

Who would’ve thought a pro-crypto president could actually end up being a net negative for the industry?

Nobody wants to believe they're the villain in the story. Nobody wants to believe their government is run by psychopaths who are inflicting unfathomable evils upon populations around the globe in order to rule the world.

It's much nicer to believe you're the Good Guys. Much easier to sit with the idea that your government might make an innocent mistake here and there, but overall is a driving force for the good of humankind, and is certainly superior to the villains it makes war with.

That's a fiction, though. It's a comfortable lie. A fairy tale that westerners tell themselves to avoid a profoundly uncomfortable truth.

The truth is that we are the villains.

We are the terrorists.

We are the tyrants.

We are the evil regime.

Our soldiers aren't out there defending our country, they're out there murdering people for defending their country. They're not fighting for freedom and democracy, they're fighting for money and power.

Daniel Crimmins from the US Army 3rd Infantry Division wrote the following about the Iraq War in 2015:

"Then you realize you haven’t seen anything to support the idea that these poor fuckers are a threat to your home. You look around and you see all the contractors making six figure salaries to fix your shit, train Iraqis, maintain the ridiculous SUVs the KBR dicks ride around in. You consider the fact that every 25mm shell costs about forty bucks, and your company has been handing those fuckers out like shrapnel flavored parade candies. You think about all the fuel you’re going through, all the ammo and missiles and grenades. You think about every time you lose a vehicle, the Army buys a new one. Maybe you start to see a lot of people making a lot of money on huge amounts of human suffering.

"Then you go on leave, and realize that Ayn Rand has no idea what the fuck she’s talking about. You realize that Fox News and Limbaugh and John McCain don’t respect you or your buddies. They don’t give a fuck if you get a parade or a box when you get home, you’re nothing to them but a prop.

"Then you get out, and you hate the news. You hate the apathy, and you hate the murder being carried out in your name. You grew up wanting so bad to be Luke Skywalker, but you realize that you were basically a Stormtrooper, a faceless, nameless rifleman, carrying a spear for empire, and you start to accept the startlingly obvious truth that these are people like you."

That's the reality right there, folks. We can wake up and start living in reality, or we can remain asleep in the fiction.

It's time to wake up to the reality that western civilization is a depraved dystopia where most people are sleepwalking in a propaganda-addled stupor under an empire that is fueled by human blood. And it's time to awaken to the fact that as westerners it is our duty to tear that empire down brick by brick, for the sake of our children and grandchildren, and for the sake of our fellow man.

I resigned from OpenAI. I care deeply about the Robotics team and the work we built together. This wasn’t an easy call. AI has an important role in national security. But surveillance of Americans without judicial oversight and lethal autonomy without human authorization are lines that deserved more deliberation than they got. This was about principle, not people. I have deep respect for Sam and the team, and I’m proud of what we built together.

WTF happened October 10 to February 5?!

Part 2 of the HK Fund Blow up. This is the other side of the story.

BTC (-48.38%) underperformed the S&P 500 (+0.53%) by a whopping 49.05% in 118 days!! What the actual fuck. BTC was supposed to be rapidly institutionalizing, but this is the largest multi-quarter depeg from the S&P 500 ever. And all with ZERO explanation. No cause, only effect.

There is always a cause though, we just have to find it. Typically, when a hedge fund blows up in catastrophic fashion, “the market” isn’t the killer, it’s something - or someone - specific, an actual killer. Amaranth Advisors didn’t lose $6B and blow up in a week due to “the market”, John Arnold’s (legendary Enron trader) Centaurus Advisors killed them and John personally made $1B that week. The Bank of England didn’t break due to “the market”, Soros killed them. John Paulson made $15B in 2007 when subprime CDS blew out and kicked off the GFC, killing some big banks in the process. Paul Tudor Jones made his entire career on Black Monday, 1987, when the Dow dropped 22% and he was massively short, killing a number of funds along the way. Behind most deaths is a killer.

I believe there is a killer here too.

Let’s look at the evidence. This will be a long read.

First, we need to look at the environment leading up to 10/10. A few big things were at play here. First, realized volatility massively tapered over the summer. On August 11, 30-day realized vol hit 11.83%. That is comically low for Bitcoin, which normally sits in the 30-60% range. Implied vol fell off a cliff as well, hitting a low of 34.49% on September 18. This made buying calls and puts incredibly cheap.

We also know that shorting vol on Bitcoin has historically been a pretty successful trade most of the time. Bitcoin vol has been in secular decline, so as long as you didn’t get blown out in one of the random spikes in vol, you are printing cash. In many ways, shorting vol on BTC is like shorting the VIX itself. 95% of the time, you make money, and then you just have to avoid blowing up in the 5%. You’re the market insurance provider when you’re shorting vol.

Now, on July 29, the single entity cap on IBIT options was increased to 250k contracts (Jan 21 was for a bunch of other crypto ETFs, not IBIT). This allowed anyone running a short vol trade to increase exposure; however, it also allowed anyone wanting to build a long vol position to increase leverage. As an aside, the IBIT contract limits aren’t particularly restricting, because (1) Market Makers can be exempt, (2) waivers can be received, and (3) OTC derivatives exist with no limits.

#3 is the biggest problem, because the OTC market is entirely opaque. No one has ANY idea how much aggregate delta exposure is in the market. We’ll come back to this.

On October 2, CME announced that they were going to launch 24/7 trading on crypto contracts sometime in early 2026. This is relevant, because we know that large crypto funds like to fuck around, especially on Saturdays and over holidays. This is where the famous CME gaps come from. Once 24/7 CME futures trading is turned on, bye bye CME gaps. Weekends have served as an artificially low-cost time for large funds to push the price in a direction they need the price to go. Without this window, the cost to push the price would just be too high, which is why you don’t see these same scam wicks outside of crypto. So, on October 2, the clock started ticking on one last epic push. This timing coincides with the rough timeline for passage of the CLARITY Act as well, which will likely make it harder for some of these shenanigans.

So, what does a fund do when vol is the cheapest in history, there’s significant size available to buy, it’s common knowledge that lots of funds are shorting vol, and there’s a ticking clock on the opportunity to artificially push prices around? Go big.

In the thread, I put together a quick example showing how a $50M long position (775k contracts) opened on 10/03 in $60 strike, 11/07 IBIT puts would have materialized into a total of $4B of sales by the dealers needing to delta hedge the position, because of the way gamma works. This is using all real numbers from that period. During the week of 11/07, the daily delta swings would have resulted in the dealer trading 25-30% of the volume on IBIT each day to hedge. This $50M position would have become 80x levered by expiration and the fund would have made $168M in profit on the trade (335%). This position isn’t even the most leverage you can get playing high gamma games. And you thought perps on Binance were crazy.

You might rightfully note that the contract limit on IBIT options at this point was 250k contracts. The counter to that is that dealers have different restrictions that allow for netting either on a contract or delta basis. If you look at the largest MMs on IBIT options, some names become immediately familiar to anyone in crypto. Maybe more importantly though, a burgeoning OTC market has emerged around IBIT to bypass the 250k limit. This is why on November 23, Nasdaq asked the SEC to allow them to increase the limit to 1M contracts, citing concerns about the opaque OTC market growing, potentially adding risk to the system. I think Nasdaq knew something was afoot in the OTC market.

You might also argue that no single contract ever has this much open interest, which is true. But this size of a position can be spread around the book, both with different strikes and different tenors, and further built in the OTC market. There’s an interesting opportunity here to build a gamma cascade where one gamma squeeze pushes the price into the next gamma squeeze.

So let’s say that a giant hedge fund put on a $50M position (or why not more) in IBIT puts and/or OTC derivatives tracking IBIT in early October, hoping for vol to mean revert. Then, 10/10 happens, causing vol to MASSIVELY revert (60% spike in BTC ivol intraday) creating the perfect storm to REALLY push this trade. In the following 4 weeks, BTC spot bid liquidity fell by 25-50% (depending on depth measure). The cost to push the price around just then got much cheaper.

So now this fund starts pushing the price using large amounts of leverage. We see this over and over in crypto, nothing particularly novel here and there are a number of strategies available to move the price with significant leverage and modest risk, i.e. liquidity arb where you short spot long futures or vis versa to capitalize on the liquidity differential between the two.

These strategies, coupled with the massively increased liquidity in IBIT options and related OTC derivatives, and the sudden drop in liquidity created the perfect storm. What was originally just an opportunity to Go big became an opportunity to GO FUCKING BIG.

If you look at the activity in Q4, a pretty obvious pattern emerges. The BTC price often drifted lower overnight (NY time) and on the weekends, all when liquidity was thinnest. Then, at the NY open, the options dealers were forced to dump to rebalance the delta they had accumulated while the market was closed, printing large selloff candles on many of the opens in Q4. It would be pretty easy to create this trade. Imagine on Wednesday, the killer would buy some OTM puts expiring on Friday. They could be very cheap with very low delta, but high gamma potential (the greek here is called speed - so high speed put options). Then, overnight on Wednesday, the killer would push the spot price down. At the Thursday open, the dealers are forced to immediately hedge by dumping IBIT, because they now have positive delta due to the overnight move. As the dealers dump, this increases the delta as the gamma increases due to the high speed and high charm (change in gamma due to change in ivol). Remember, high gamma options are those that are really close to expiry and right at the money, so as the price goes down and approaches the strike on the OTM puts, the delta rapidly increases, forcing the dealers to sell more. This pattern could be repeated each week with a new set of weekly options to push the price further and further down.

Over the following months, this fund continued to push the trade, racking up hundreds of millions to billions in profits, which could be recycled into further pushing the trade. The massive amount of retail perps leverage on the offshore exchanges (crypto was supposed to have a supercycle, all the influencers said so) was an additional accelerant. Adding to that, the basis trade began to unwind, both on the CME and in crypto, with Ethena processing $7B in redemptions in a month. These basis trade unwinds put a lot of pressure on a thinning spot book.

I believe the first leg of the trade was wrapped up in late December, because a trader of this size would want to close their position by year end to avoid 13F filing requirements (although 13F requirements don’t apply to OTC derivatives). Looking at the chart, it also seems obvious that the trade was closed out in December. By mid January however, implied vol had subsided to levels below 10/10, meaning restarting the trade wasn’t going to be too expensive. Coupled with the giant profits this fund was sitting on and the somewhat tepid environment for tech (AI P/Es stretched, Fed nominee fears, etc), there appeared to be another opportunity to squeeze in one last push right before CLARITY and the CME 24/7 futures. Double or nothing, bitches.

So, over the latter half of January, a new high-gamma-potential (high speed) put ladder was built. Then, on Jan 26, Nasdaq greenlit Monday, Wednesday, and Friday options, so now triple the gamma available!! The killer could basically roll the trade every 2 days instead of once a week now. So, on January 29, with Silver and Gold retracing significantly, with bags loaded, and a machine gun instead of a bolt action rifle, the killer started the push, getting the price to the support level for the range. Below this range, there would be a lot of leverage as retail traders banked on the support holding. On Saturday, when the CME was closed, BAM, support was blasted with BTC down 6.5% on the day, kicking off >$2.5B in liquidations, more than any day since 10/10 and the 2nd highest of this cycle. This created the largest CME gap of this cycle and the largest gap in $ terms in history (~$6k).

After this push, it was straight carnage. The put ladder worked perfectly, creating cascading delta hedging by the dealers. Any stalls in collapse could be followed up with new high-speed puts on one of the new M/W/F tenors. Silver and Gold continued to puke and risk assets took it on the chin across the board. In exactly 1 week (29th to 5th), BTC was down 30%, one of the largest % weekly moves in history, and by far the largest $ move ever (-$26,500). This culminated in the HK-based fund(s) completely blowing up on Thursday (02/05), and everyone panic-closing positions, giving this new legendary billionaire crypto trader his exit liquidity.

Whoever the killer is, I would expect them to have some or all of the following traits:

Have been in crypto for 5+ years, with a deep understanding of how liquidity dynamics work over weekends and how liquidity arbitrage between spot, perps, and IBIT work.

Have been in tradfi for a long time as well, deeply understanding options trading, vol surfaces, liquidity dynamics within ETFs, ETF options, CME futures, and options position limits.

Have been a market maker in IBIT, IBIT Options, and likely OTC options. This would have allowed them to increase their position size above the 250k limit and source meaningful amounts of gamma in the OTC market. Their Authorized Participant status probably also tipped them off to the fact that someone big was on the other side of the trade in either/both IBIT options and OTC options. Being a dealer could have also allowed them to build a large position more quietly, potentially by simply providing liquidity to the victim(s) on the other side.

Have a history of past manipulation in other markets or strong accusations of manipulation, either in crypto or equities. Additionally, you might expect to see former trader(s) who left and went on to take some huge bets (bordering on or full blown manipulation) that either blew up catastrophically or printed bigly. This point is admittedly total speculation, but could illuminate a culture of pushing huge bets into deeply grey areas.

Given how privacy-oriented hedge funds and crypto can be, we may never know who the killer is. There may have also been a few tag along accomplices on the second push over the last week.

Make no mistake though, there was absolutely a new billionaire crypto trader minted this week.

This is my hypothesis on what happened between October 10th and February 5th, based on bread crumbs and circumstantial evidence. This move had nothing to do with the fundamentals of Bitcoin or Solana, and everything to do with technical market microstructure dynamics. CLARITY should help fix some of this, because the root problem is that the spot BTC market is not nearly liquid enough to support all these derivatives. BTC spot is supporting perps, CME futures, ETFs, derivatives on the ETFs, derivatives on the CME futures, and a host of OTC products. We need all of the world's largest market makers active in spot BTC to help solve this problem. Additionally, we need more flows to move onshore, on exchange, and ultimately on chain. On chain is the objectively best solution here as net and gross positioning cannot be hidden. We need to see reduced opaque OTC and offshore activity that creates the opportunity for these issues. There are some other easy fixes as well, e.g. CME futures going 24/7, better risk management at funds in trading vol, more spot liquidity overall, increased IBIT options position sizing (as Nasdaq has requested), etc. Most importantly though, market participants learned another great crypto lesson this week/quarter that must be applied. Be VERY VERY careful trading on leverage.

Live by the leverage, die by the leverage.

If there were one thing to read today re the game-changing nature of Bitcoin ETF options, read (and bookmark) this one for 2025 - it's going to be wild.

i know a prop shop that blew up once trading vix futures because they forgot to clean out their position and had to take physical delivery of vol at expiry

The thing is, neither Bitcoin nor Ethereum can be replicated today. But Solana can be replicated.

Bitcoin was launched when crypto had no monetary value. It was worth $0 for the first year. This created unique distribution and culture. Impossible to replicate.

Ethereum was launched with an ICO, which lasted months and was open to everyone. About 50% of current supply was sold in the ICO, and ~40% was mined via PoW. Again, this created unique distribution and culture. Impossible to replicate.

But Solana is a VC coin. Team got a bunch, foundation got a bunch, VCs got a bunch. That's it. And this is basically the same token distribution as Near, Aptos, Sui, etc.

Solana can be - and has been - replicated. It isn't unique.

True, Solana did have a near-death experience after the FTX collapse. That event was unscripted and real. This helped distribute the token supply, and solidified the community.

But I don't think this event made Solana a fundamentally unique and irreplicable project. Whereas Bitcoin and Ethereum are irreplicable, for historical reasons.

1/

The Ethereum ETFs are set to go live on July 23rd. There are a number of dynamics present with the ETH ETF that have been overlooked by the market & which were not present with the BTC ETF. We take a look at flow predictions, ETHE unwinds & the relative liquidity of ETH:

The fee structure of the ETF ETFs is similar to that of the BTC ETFs. Most providers are waving their fee for a specified period, to help accumulate AUM. As was the case with the BTC ETFs, Grayscale has the maintained their ETHE fee at 2.5%, an order of magnitude larger than other providers. The key difference this time around is the introduction of the Grayscale mini ETH ETF, which previously wasn’t approved for the BTC ETF.

The mini trust is a new ETF product by Grayscale that originally disclosed at 0.25% fee, similar to the other ETF providers. Grayscale’s idea here is to capture a 2.5% fees on lazy ETHE holders, whilst funneling more active and fee sensitive ETHE holders to their new product, instead of having funds siphoned to low fee products such as Blackrock’s ETHA ETF. After the other providers undercut Grayscale’s 25bps fee, Grayscale came back and reduced the mini trust fee to only 15bps, making it the most competitive product. On top of this, they moved 10% of ETHE AUM to the mini trust and gifted ETHE holders this new ETF. This transition was completed at the same basis, meaning it was not a taxable event.

The resultant effect is ETHE outflows will be more muted as compared to GBTC as holders simply transition to the mini trust.

Now we look into flows:

There have been many estimates for the ETF flows, some of which we have highlighted below. Taking the estimates and standardizing them yields an average estimate in the $1bn/month region. Standard Chartered Bank offers the highest estimate with $2bn/month, while JP Morgan is on the low end at $500m/month.

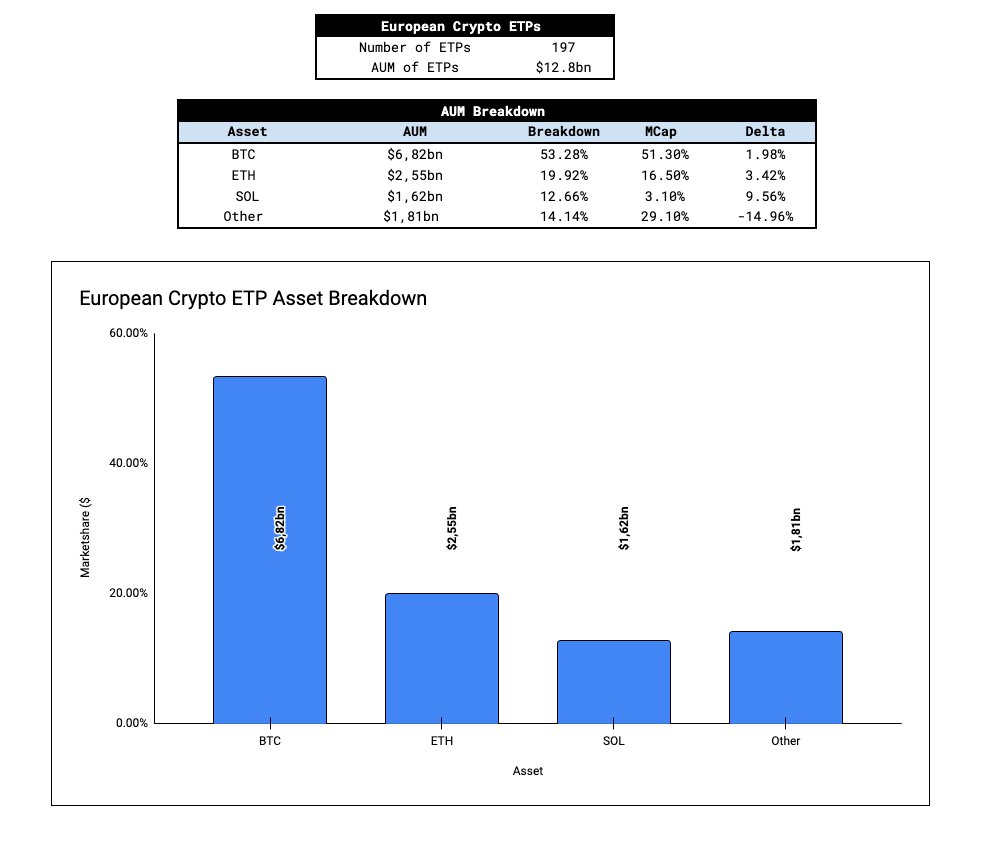

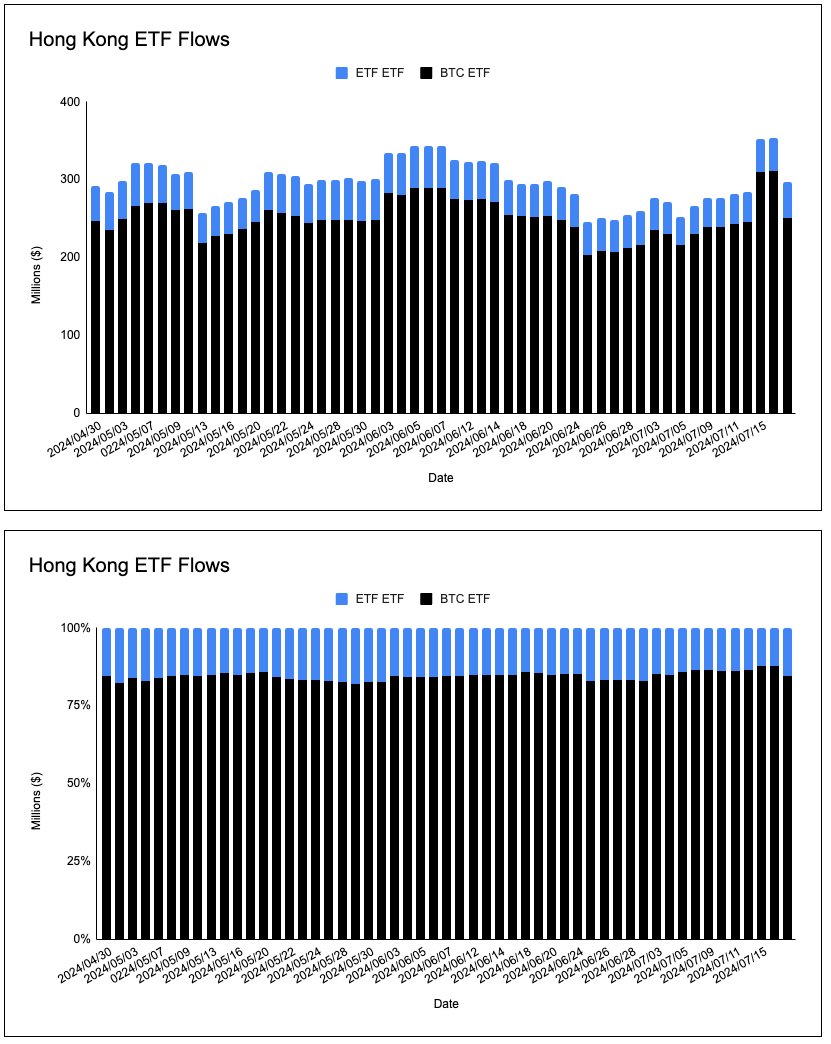

Fortunately, we have the help of Hong Kong and European ETPs as well as the closing of the ETHE discount in order to help estimate flows. If we take a look at the breakdown of AUM in HK ETPs, we arrive at two conclusions:

1. The relative AUM BTC and ETH ETPs are overweight BTC vs. ETH, the relative market cap sits at 75:25, while the AUM sits at a ratio of 85:15.

2. The ratio of BTC v ETH in these ETPs is reasonably constant and in-line with the ratio of BTC market cap to ETH market cap.

Looking at Europe, we have a larger sample size to look at – 197 crypto ETPs with a cumulative AUM of $12bn. After we boil down the data, we find that breakdown of AUM in European ETPs is broadly in line with the market cap for Bitcoin and Ethereum. Solana is over allocated relative to its market cap, this comes at the expense of ‘Other crypto ETPs’ (Anything not BTC, ETH, or SOL). Setting Solana aside, a pattern is beginning to emerge – the breakdown of AUM globally between BTC and ETH broadly reflects a market cap weighted basket.

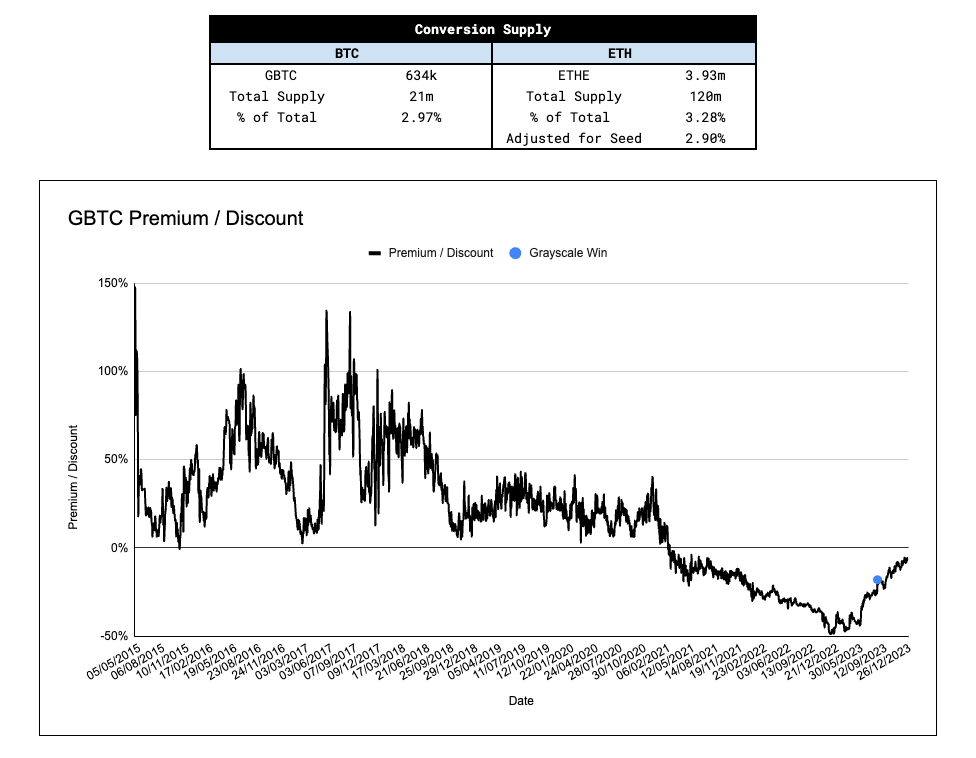

It’s important to consider the potential for ETHE outflows considering the GBTC outflows were the genesis of the ‘sell the news’ narrative. In order to model potential ETHE outflows and its affect on price, it’s useful to look at % of ETH supply in the ETHE vehicle.

Once adjusted for Grayscale mini seed capital (10% of ETHE AUM), the proportions of ETH supply as a function of total supply existing in the ETHE vehicle is similar to that of GBTC at launch. It’s unclear what proportion of GBTC outflows were rotational vs. exit, however if we assume the proportion of rotational flows to exit flows is similar, ETHE outflows have a similar impact on price to GBTC outflows.

Another key piece of information that most are overlooking is the ETHE premium/discount to NAV. ETHE has been trading within 2% of par since May 24th – whereas GBTC first traded within 2% of NAV on Jan 22nd, only 11 days after GBTC converted to an ETF. The approval of the spot BTC ETFs and their effect on GBTC was slowly priced into the market, whereas the ETHE discount to NAV trade has been far more telegraphed with the story already written with GBTC. By the time the ETH ETFs go live, ETHE holders will have had all of 2 months to exit ETHE around par. This is a key variable that will help stem the ETHE outflows, specifically the exit flows.

Continued in the next tweet >

None of my intelligent (130+ IQ) friends use cryptocurrency regularly. They only use it selectively and rarely, e.g., at a conference or buying drugs, but almost never trade or invest in it spontaneously in their own time. This has been a long-term consistent observation, but today confirmation came. A new meta-analysis showed time spent holding cryptocurrency per day increases exponentially with lower IQ, with drop-off to near 0 days at 145+. Cryptocurrency is mostly appealing as a way to fill an otherwise vacant mind that has no interesting thoughts and minimal goal-directed behaviour. Intelligent people find stimulation from thinking about real-world problems and making a tangible difference to the world, not from speculating on volatile digital coins like some sort of day-trading lemming.

For those of you who are new and want to learn how to trade and navigate markets from CT, you honestly really missed out.

2 cycles ago this place was filled with great high level trading discussion.

Now most people just want to be famous or some pseudo-vc.

“We’re towards the end of the cycle” = I took too much profit / sidelined / price is above my exit

“We’re in a supercycle” = I haven’t made any money yet

“We’re in the early innings of the cycle” = I just made some money, this better keep going because I’m sizing up