Solo sé que no sé nada; en IA y negocios, menos. Excofundador. Siempre con algo entre manos. DeFi/GenArt/ReFi: relación complicada. PhD | MRes | MSc×2 | MEng

@SiloIntern ser, can you expand on how is it different than morpho? Also, any deals that are coming to silo that are not possible in other lending platforms? Thx

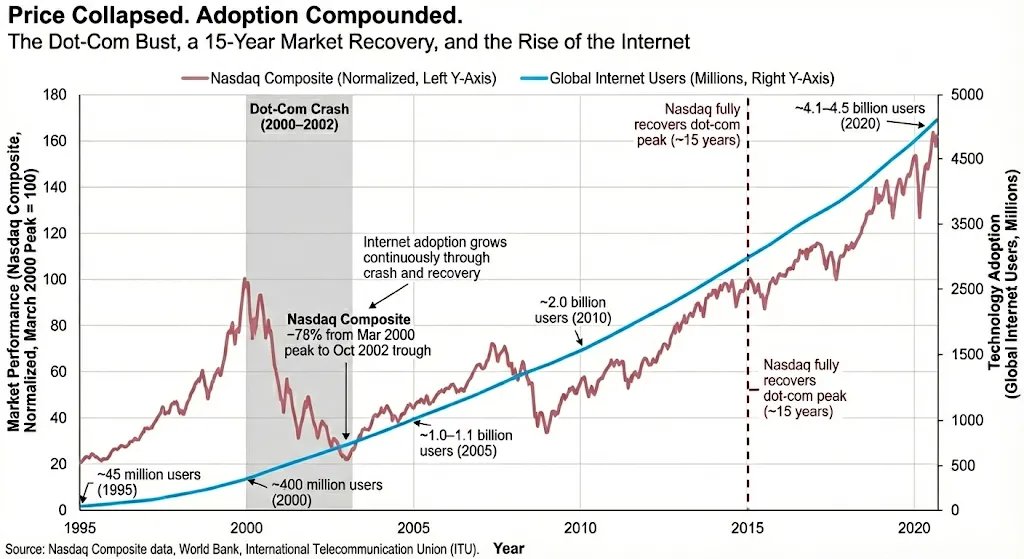

Everyone thinks the crypto selloff is crypto-native. The real story is a TradFi entity running a multi-leg carry trade that unwound.

Follow the funding chain. A HK entity borrows yen at 0.75% (the BOJ’s highest rate in 30 years, up from near-zero). Uses that cheap leverage to build a multi-leg position across IBIT options, Binance crypto, and precious metals. Three asset classes, one funding currency, zero margin for error.

Oct 10 was the first crack: $19.16B in crypto liquidations, the largest single-day wipeout ever. Prime broker gives them 90 days to recover. So they double down on precious metals, which had been ripping. Gold and silver were up 65% and 145% respectively in 2025. Looked like a reasonable recovery bet.

Then Kevin Warsh gets nominated as Fed Chair on Jan 29. Markets read that as hawkish dollar policy. Gold drops 11%. Silver drops 31% in its worst day since 1980. The recovery trade is now a second hole in the balance sheet.

Feb 5 was the margin call heard across three asset classes simultaneously. IBIT traded $10B in volume (284 million shares, shattering its prior record). Put options hit 25 volatility points above calls, the highest skew ever recorded. Silver plunged another 20% to below $71 before bouncing. Bitcoin fell from $73,100 to $62,400 intraday, its first time below $70K in 15 months.

Here’s what most people are missing. Nasdaq removed position limits on IBIT options in January 2026. That regulatory change allowed exactly this kind of concentrated leveraged exposure to build up in a single ETF. One entity could now take a position large enough to move the entire market on unwind.

The 13F filings drop Feb 14. That’s when we’ll see which single-asset funds based in Hong Kong were holding outsized IBIT positions. But the story isn’t who. The story is the plumbing.

Cheap yen funded the trade. IBIT options concentrated the risk. Precious metals were supposed to be the hedge. When all three legs failed in sequence, the forced selling cascaded across crypto, metals, and options simultaneously. Michael Burry called this a “collateral death spiral” earlier this week, where falling crypto collateral forces liquidation of metals positions, which triggers more margin calls, which forces more crypto selling.

This is what happens when carry trade leverage meets concentrated ETF options meets thin commodity liquidity. Three separate markets, one funding source, and when the music stops, they all sell at once.

The crypto market crashed because a currency trade went wrong on the other side of the Pacific, and the new ETF options infrastructure made it possible to concentrate that bet at a scale that could move $10B in a single session.

@captnhayz@FraxForce@fraxfinance I can't agree more with frax. The counter argument is that they always chase narratives instead of being strong on one. So, how can we onboard these ones? It's always and has been about stables?

I had a scenario related to the regular cycle that good coins will pump. Scenario B was this one. So, I found protocols fitting both to bet on @Frax was the one I allocated the most.

Ethereum's next major upgrade, "Fusaka" goes live in under a month.

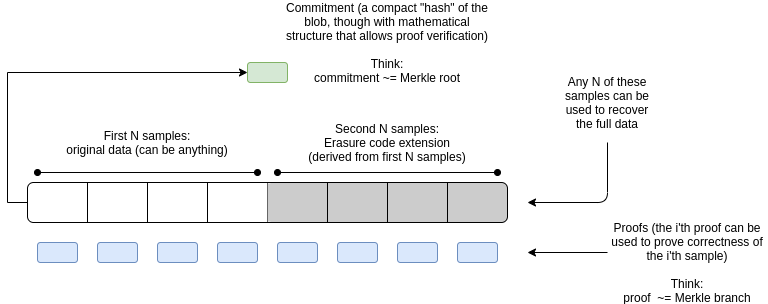

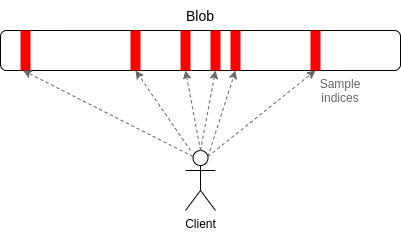

Its core feature, called PeerDAS, lets nodes store only parts of each blob instead of the entire thing.

This lets Ethereum scale to more blobs per block.

More blobs → cheaper DA → cheaper L2 transactions.

PeerDAS in Fusaka is significant because it literally is sharding.

Ethereum is coming to consensus on blocks without requiring any single node to see more than a tiny fraction of the data. And this is robust to 51% attacks - it's client-side probabilistic verification, not validator voting.

Sharding has been a dream for Ethereum since 2015 , and data availability sampling since 2017 ( https://t.co/Fa0jKFgObW ), and now we have it.

That said, there are three ways that the sharding in Fusaka is incomplete:

* We can process O(c^2) transactions (where c is the per-node compute) on L2s, but not on the ethereum L1. If we want to scaling to benefit the ethereum L1 as well, beyond what we can get by constant-factor upgrades like BAL and ePBS, we need mature ZK-EVMs.

* The proposer/builder bottleneck. Today, the builder needs to have the whole data and build the whole block. It would be amazing to have distributed block building.

* We don't have a sharded mempool. We still need that.

But even still, this is a fundamental step forward in blockchain design. The next two years will give us time to refine the PeerDAS mechanism, carefully increase its scale while we continue to ensure its stability, use it to scale L2s, and then when ZK-EVMs are mature, turn it inwards to scale ethereum L1 gas as well.

Big congrats to the Ethereum researchers and core devs who worked hard for years to make this happen.

@FlyingTulip_ Posible TGE? airdrop???

DeFi todo-en-uno: spot/swaps, perps con leverage y cross-margin en una sola cuenta (más lending). Menos fricción, ejecución on-chain. Fundador: @AndreCronjeTech (@yearnfi@SonicLabs).

To-do: https://t.co/UjAKPtrNzW

@Saxenasaheb If you go for a MBA, my advice is that you either go to a top university or don't do it at all. The most important asset is the networking you are going to do. Best of luck, and apply to many of them so that you can select afterwards. Go to a prep school for the GMAT