$CRDO

If it loses the correction band, it will also lose the BoS zone. After that, it could lead to a swing low that may extend all the way down to the support band

Every couple of months I post our top positions at @FirstWaveFund and since we sent our May investor letter a few days ago I don’t mind sharing those positions... here are the top 12 in alphabetical order:

AAOI, ALAB, APP, CRDO, HIMS, HROW, IREN, MELI, MU, NBIS, RDDT, TMDX

All estimates are my own. Every company mentioned in this post has risks so please do your own research and form your own opinions, thesis and conviction. Please don't waste your time asking me where I'd be buying or trimming... because I won't answer.

I spend alot of time building our models and thinking through all the possible variables and catalysts that will impact the reported financials but in reality trying to predict revenues, margins, dilution and earnings in CY2028 or FY2029 is not easy.

$AAOI

CY2025 revenues = $455M

CY2028 revenues = $10.70B

3 year revenue CAGR = 186%

CY2025 EPS = -$0.26

CY2026 EPS = $1.04

CY2028 EPS = $10.40

2 year EPS CAGR from CY2026 through CY2028 = 216%

Currently trading at 15.6x CY2028 EPS (not including cash/debt)

$ALAB

CY2025 revenues = $852M

CY2028 revenues = $3.88B

3 year revenue CAGR = 66%

CY2025 EPS = 1.84

CY2028 EPS = $8.55

3 year EPS CAGR = 67%

Currently trading at 48.7 CY2028 EPS (not including cash/debt)

$APP

CY2025 revenues = $5.48B

CY2028 revenues = $16.67B

3 year revenue CAGR = 45%

CY2025 EPS = $10.64

CY2028 EPS = $37.06

3 year EPS CAGR = 52%

Currently trading at 12.6x CY2028 EPS (not including cash/debt)

$CRDO

FY2025 revenues = $436M

FY2028 revenues = $4.11B

3 year revenue CAGR = 111%

FY2025 EPS = $0.70

FY2028 EPS = $10.68

3 year EPS CAGR = 148%

Currently trading at 25.5x FY2028 EPS (not including cash/debt)

$HIMS

CY2025 revenues = $2.35B

CY2028 revenues = $5.81B

3 year revenue CAGR = 35%

CY2025 EPS = $1.10

CY2028 EPS = $2.55

3 year EPS CAGR = 32%

Currently trading at 13.9x CY2028 EPS (not including cash/debt)

$HROW

CY2025 revenues = $272M

CY2028 revenues = $928B

3 year revenue CAGR = 50%

CY2025 EPS = -$0.14

CY2026 EPS = $1.09

CY2028 EPS = $5.64

2 year EPS CAGR = 127%

Currently trading at 7.6x CY2028 EPS (not including cash/debt)

$IREN

FY2025 revenues = $510M

FY2028 revenues = $6.60B

FY2029 revenues = $9.88B

4 year revenue CAGR = 110%

FY2025 EPS = $0.35

FY2028 EPS = $0.68

FY2029 EPS = $1.33

4 year EPS CAGR = 40%

Currently trading at 45.1x FY2028 EPS (not including cash/debt)

$MELI

CY2025 revenues = $28.89B

CY2028 revenues = $65.81B

3 year revenue CAGR = 32%

CY2025 EPS = $39.40

CY2028 EPS = $90.14

3 year EPS CAGR = 32%

Currently trading at 18.1x CY2028 EPS (not including cash/debt)

$MU

FY2025 revenues = $37.38B

FY2028 revenues = $274.18B

3 year revenue CAGR = 94%

FY2025 EPS = $8.29

FY2028 EPS = $151.32

3 year EPS CAGR = 163%

Currently trading at 7.5x FY2028 EPS (not including cash/debt)

$NBIS

CY2025 revenues = $530M

CY2028 revenues = $22.83B

3 year revenue CAGR = 250%

CY2028 EPS = $5.42

CY2031 EPS = $23.96

Currently trading at 47.8x CY2028 EPS (not including cash/debt)

3 year EPS CAGR from CY2028 through CY2031 = 64%

$RDDT

CY2025 revenues = $2.20B

CY2028 revenues = $6.24B

3 year revenue CAGR = 42%

CY2025 EPS = $4.54

CY2028 EPS = $14.15

3 year EPS CAGR = 46%

Currently trading at 12.3x CY2028 EPS (not including cash/debt)

$TMDX

CY2025 revenues = $605M

CY2028 revenues = $1.34B

3 year revenue CAGR = 30%

CY2025 EPS = $2.63

CY2028 EPS = $6.33

3 year EPS CAGR = 34%

Currently trading at 12.4x CY2028 EPS (not including cash/debt)

NFA.

DYOR.

*I own all of these stocks personally and so does @FirstWaveFund

**If you see any glaring mistakes in my numbers feel free to comment below and I'll double check my work/models.

ENJOY THE LONG WEEKEND.

GO SOCCER!!!!!

$VIAV got dragged down 30% with the optics names over InP supply and CPO timing. Neither one touches its business.

VIAV does not buy InP. Substrate prices have gone up drastically over the past year and that squeezes the companies making lasers and transceivers. VIAV sells the test gear, so it gets paid to certify whatever they manage to ship, at whatever cost structure they ship it.

The CPO fear is even stranger here. If CPO slips, pluggables stay in racks longer and VIAV keeps testing them like it does today. If CPO lands, it needs an entirely new class of test platforms that VIAV is already building.

$VIAV did ran over 300% in a year and raised $500M in equity back in May, so some digestion was coming either way. Worth noting the raise went to paying off debt, not funding the business. But the two headline fears driving this selloff are aimed at names that make optics, not the name that tests them.

I think earnings will wake people up again. $VIAV

$MSTR

I was expecting a slightly more drifting decline. It may still want to pull back toward its previous low around $110

I’m expecting the base work I marked with the black candle formation. But of course, this is not the word of God. Only after this bottom base forms and something starts to emerge can my perspective change in a positive direction

The Computex / GTC Taipei heat is real.

After Jensen Huang literally called Marvell ($MRVL) "the next trillion-dollar company" on stage, the market realized the AI trade has shifted from pure silicon to connectivity and deployment.

If you missed the $MRVL or $DELL runs, watch these 3 tickers. The catalysts are lined up:

1⃣ $AVGO (Broadcom) - The Catalyst is TOMORROW

➡️The Catalyst (June 3rd):

Broadcom reports Q2 earnings tomorrow after the closing bell.

Following Jensen’s announcement that copper cables are hitting a physical wall at 400Gbps+, the entire market is looking at Co-Packaged Optics (CPO).

➡️The Trade:

$MRVL caught the first wave, but Broadcom is the absolute leviathan in AI networking chips and custom ASICs.

Tomorrow's print will be a direct referendum on the custom silicon and optical networking thesis.

2⃣ $SNPS (Synopsys) — The Autonomous AI Engineers

➡️The Catalyst (June 4th):

Their GTC panel on AgentEngineer™ this Thursday will showcase multi-agent AI teams designing 3nm/2nm chips.

By deeply integrating Nvidia’s cuLitho, they've achieved a 20x speedup in lithography computation.

➡️The Trade:

Moving from a standard SaaS subscription model to charging a premium for autonomous "virtual engineering" labor.

3⃣ $PLTR (Palantir) - The OS for Agentic AI

➡️The Catalyst:

Nvidia’s massive push for local agents via RTX Spark and OpenShell faces a major enterprise roadblock: corporate data security and governance.

➡️The Trade:

Palantir’s AIP integrated with Nvidia's Nemotron models provides the exact guardrails enterprises need.

If Microsoft scales Windows-native agents, Palantir is the default bridge for enterprise security.

Let’s discuss:

Everything happening right now is absolutely insane -the market is shifting at warp speed.

What are your bets for the next wild runner to shoot into space? 👇

It's September 2026, stocks I bought under $20 and they exploded 1000%

1. $KEEL – Former Bitfarms. 2.2 GW pipeline. Hyperscaler leases incoming. Cheapest GW-scale AI land play (Leopold call)

2. $SATL – Satellite imagery feeds AI training + defense targeting. Fresh DoD contract proves the demand is real. $SPCX SPACEX play

3. $LAES – Every AI agent needs quantum-proof identity. SEALSQ embeds PQC in silicon. The security layer AI can't run without.

4. $POET – Optical Interposer replaces copper in AI clusters. Light moves data faster at half the energy. 800G design wins at record pace.

5. $ONDS – Wireless OS for AI-driven industrial drones. Defense + logistics demand exploding. First-mover advantage. (Trump call)

6. $CIFR – Massive power assets pivoting to HPC. Market repricing it as AI infrastructure owner, not just a crypto miner. Same as $IREN $CRWV $NBIS

7. $BTDR – AI cloud ARR up 60% MoM. 92% GPU utilization. 3 GW global capacity. Own-chip design cuts cost to near zero.

8. $CLSK – Situational Awareness fund loaded 12M+ shares. Massive power footprint waiting to flip into AI colocation. (Leopold bought)

9. $HIVE.TO – Canada's largest AI gigafactory incoming. 100K GPU build-out on 100% renewable power. $225M ARR target.

10. $NOK – Restructuring entirely around AI data center networking. $4B US bet. Optical division feeding hyperscalers directly.

♻️ RESHARE this post and write 1 comment, I'll DM you my favorite 1000% play for this week.

$MSTR

I’m following the black path. After the bottom formation here, which may take some time, I’m also eagerly waiting for the rally that will start.

I think it needs time. My kidneys are ready, I’m drinking plenty of water.

The path does not have to be exactly one to one

1/ On Feb 21 I told my boss aka my wife @LTwolfe that I had my third conviction call not yet appreciated + to buy a basket

*In 2016 it was NVDA, pitched publicly at Invest For Kids in Chicago (80x+) when Lux portfolio company Zoox was using NVDA chips and I predicted the narrative would change from gaming consoles PS4/Xbox to simulation and AI…

Everyone is watching $LITE, $COHR, $AAOI, $AXTI run. The photonics rotation is real and the AI capex thesis is well understood by now.

What isn't talked about enough is what comes after 800G.

Silicon photonics (what most of the above ship today) and InP both hit hard physical limits beyond 800 Gbps. The AI buildout doesn't stop there. Nvidia's NVLink 6 is already targeting 3.6 Tb/s per GPU. The whole stack has to move to 1.6T then 3.2T. Current materials can't get you there cleanly.

That's where TFLN comes in.

Thin-film lithium niobate isn't a new material, LN has been in telecom for 60 years. What changed is the fabrication. A smart-cut process now lets you bond a nanometer-thin film of LN onto a substrate, giving you all the electro-optic properties of the crystal in a form dense enough to build photonic integrated circuits. The result: modulators running 100+ GHz bandwidth, sub-1V drive voltage, and propagation loss under 0.1 dB/cm. Silicon works by pushing carriers around to change the refractive index. TFLN uses the Pockels effect, the field changes the index directly, no carriers, no lag, no extra heat. That's a generational gap in performance at the speeds AI infrastructure needs.

TFLN doesn't replace InP either. It needs a laser source from InP or a VCSEL. It sits on top of it.

The problem is supply. Nearly all TFLN wafers in the world come from one company: NANOLN, based in Jinan, China.

Raytheon literally said this out loud in their Mastermind AFRL contract filing. They described TFLN wafer production as dominated by a Chinese manufacturer and selected Gooch & Housego ($GHH, LON) to build the first domestic US production line in Ohio.

CPO (co-packaged optics) is the architecture pulling this forward. CPO integrates optical engines directly onto the switch or GPU package, cutting signal loss and power vs pluggable modules. CPO ports are forecast to be 30%+ of all 800G and 1.6T deployments in 2026-2028. At those speeds the modulator of choice converges on TFLN.

The stack is: hyperscaler capex -> CPO adoption -> 1.6T modulator demand -> TFLN wafer supply crunch -> whoever controls domestic production.

$AXTI is the InP layer. $GHH is the TFLN layer. Same thesis, different spot.

$GHH is a London-listed, small cap, and illiquid. Not a momentum trade. But if the CPO buildout plays out the way the optical interconnect market is projecting, the wafer supply chain gets stress-tested, then this Western producer with a Raytheon-backed production line looks very different at that point.

On top of that, $GHH is an undervalued, profitable and growing aerospace/defense/life sciences/telecom/industrial supplier.

Small position, long time horizon, high conviction on the structural setup.

$ZETA daily

In the grand scheme of things, it's still ranging between the 0.618 and 0.786 log Fibonacci levels at $16.27 and $23.68, respectively.

Could be forming an inverse head & shoulders bottoming pattern around the 0.618, which could then enable a move back up to $23 if the neckline around $19 is breached.

In my last article on LayTec, I mentioned that I would take a closer look at the remaining subsidiaries of Nynomic $M7U, this piece is intended to follow through on that commitment.

LayTec is undoubtedly the crown jewel within the Nynomic Group. However, the other companies are also compelling and well worth attention, each occupies a strong position within its respective niche. If I wanted to take a more promotional angle, I could easily lean on buzzwords like gas turbines, semiconductors, biotechnology, or even draw comparisons to companies like ONTO and highlight those connections. While such links do exist, emphasizing them too heavily would risk overstating the case.

Instead, I have deliberately taken a conservative approach in my sum-of-the-parts analysis. Based on this framework, I am confident that a 2x revenue multiple for the entire Nynomic Group is justified. The company is currently valued at 1.2x 2026 revenue.

Looking at the bigger picture, it also becomes evident that the individual subsidiaries have recently started to collaborate more closely, creating synergies and cost-saving potential that are not yet fully reflected in the current numbers.

https://t.co/p6rdC2wWd6

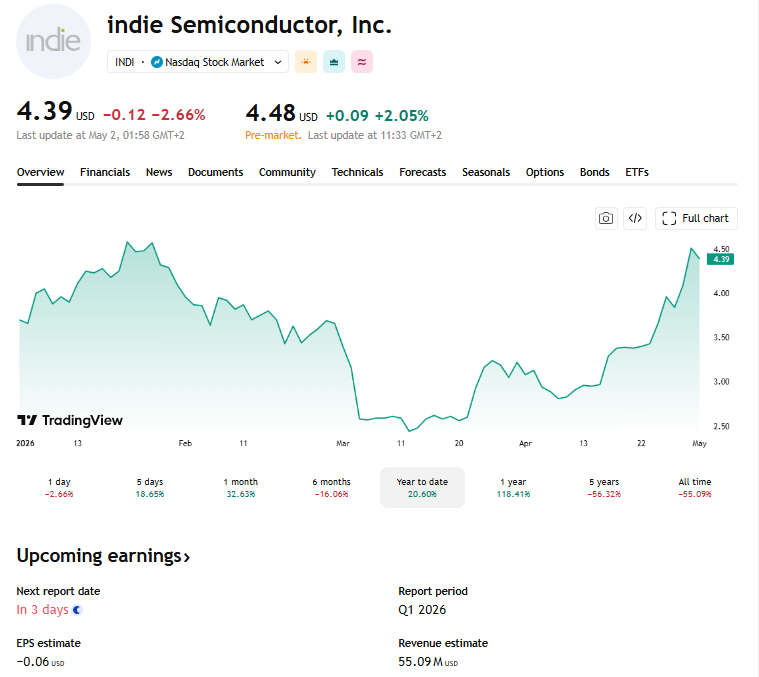

$INDI indie Semiconductor: Automotive Revolution or Cash Burn Trap?

indie Semiconductor is at the heart of the "software-defined vehicle" shift, providing crucial semiconductors for ADAS, user experience, and vehicle electrification.

With earnings scheduled for May 7, 2026, the company is under intense scrutiny.

While they boast a massive $6 billion strategic backlog, the market is increasingly focused on the transition from "design wins" to "positive cash flow."

With a significant short interest exceeding 30%, INDI is a high-stakes play in the automotive tech space.

Read my deep-dive analysis below.

1⃣Financial Health: The Cash Burn vs. Growth Race

According to recent SEC Form 4 filings (April 2026) and the Q4 2025 earnings recap, indie Semiconductor is navigating a complex financial landscape.

➡️Revenue Trajectory:

The company has guided Q1 2026 revenue to be between $52M and $58M ($55M at the midpoint).

This reflects a 20% sequential growth in its core business, offset by a planned decline in its Wuxi indie Micro subsidiary (expected at $21M).

➡️Insider Activity:

There has been notable insider selling recently.

President Ichiro Aoki and CFO Naixi Wu sold shares in April 2026 under pre-arranged 10b5-1 plans.

While often routine, the scale of insider sales (over 760k shares in the last quarter) remains a point of caution for retail investors.

➡️Path to Profitability:

Analysts expect an EPS of ($0.06) for Q1.

The company has a market cap of approximately $925M and a healthy current ratio of 3.73, but the focus remains on when the negative net margins will finally flip to green.

2⃣Market Dynamics: The 30% Short Interest Factor

$INDI is currently a prime candidate for extreme volatility due to its technical and sentimental setup.

➡️Short Interest:

As of early May, the short interest as a percentage of the float is at a staggering over 30%.

With over 12 days to cover, any positive surprise in the earnings call could trigger a violent "short squeeze."

➡️Technical Setup:

The stock has seen a massive 69% trend increase since March 2026, recently closing around $4.39.

It is currently trading above its 50-day moving average ($3.10), suggesting a bullish mid-term trend, though it faces immediate resistance at $4.72.

3⃣ Technological Moat: ADAS and Perception Platforms

Unlike general-purpose chipmakers, indie focuses on highly integrated, mixed-signal SoCs for automotive-only applications.

➡️Diversification:

Their sensors span Radar, LiDAR, Ultrasound, and Computer Vision. This "multi-modality" approach is their primary moat, making them an approved vendor for almost all major Tier 1 automotive partners.

➡️Content per Vehicle:

The primary investment thesis for INDI is the increasing semiconductor value per car.

As ADAS features move from luxury to standard, INDI’s "design wins" are expected to convert into steady production revenue through 2027.

4⃣Critical Success Metrics for May 7 (The Analyst Checklist)

To maintain its recent momentum, the upcoming earnings call must address four critical pillars.

➡️First, the Core Business Revenue Growth must hit or exceed the 20% sequential growth target.

Investors are looking for proof that the core ADAS business can decouple from the volatility of its smaller subsidiaries.

➡️Second, the Gross Margin Guidance is vital.

indie has been aiming for a "north of 60%" long-term target; any progress toward the 52-53% range in the short term will be seen as a major win for operational efficiency.

➡️Third, look for an update on the Strategic Backlog.

The $6 billion figure has been the headline for months.

The market now demands to see Pipeline-to-Backlog Conversion - specifically, how many of those "wins" have transitioned into firm, non-cancellable purchase orders for the 2026-2027 model years.

➡️Finally, a clear Cash Burn Reduction Plan is required.

With a negative net margin, the CEO must provide a definitive timeline for achieving EBITDA break-even.

If the company can prove it will reach profitability without needing further capital raises in 2026, the stock will likely break through its $4.72 resistance level.

⬇️Final Verdict:

indie Semiconductor is a classic "high-beta" automotive play.

Technically, the setup with 30% short interest makes it a "coiled spring" for the May 7 report.

Fundamentally, the company is delivering on revenue growth but still struggling with GAAP profitability.

➡️ Watch the Cash Flow and Backlog conversion.

The "story" of the $6B backlog is starting to age; the market now wants to see the "cash."

If the Guidance for Q2 2026 exceeds $60M, it will confirm that the automotive ramp-up is accelerating.

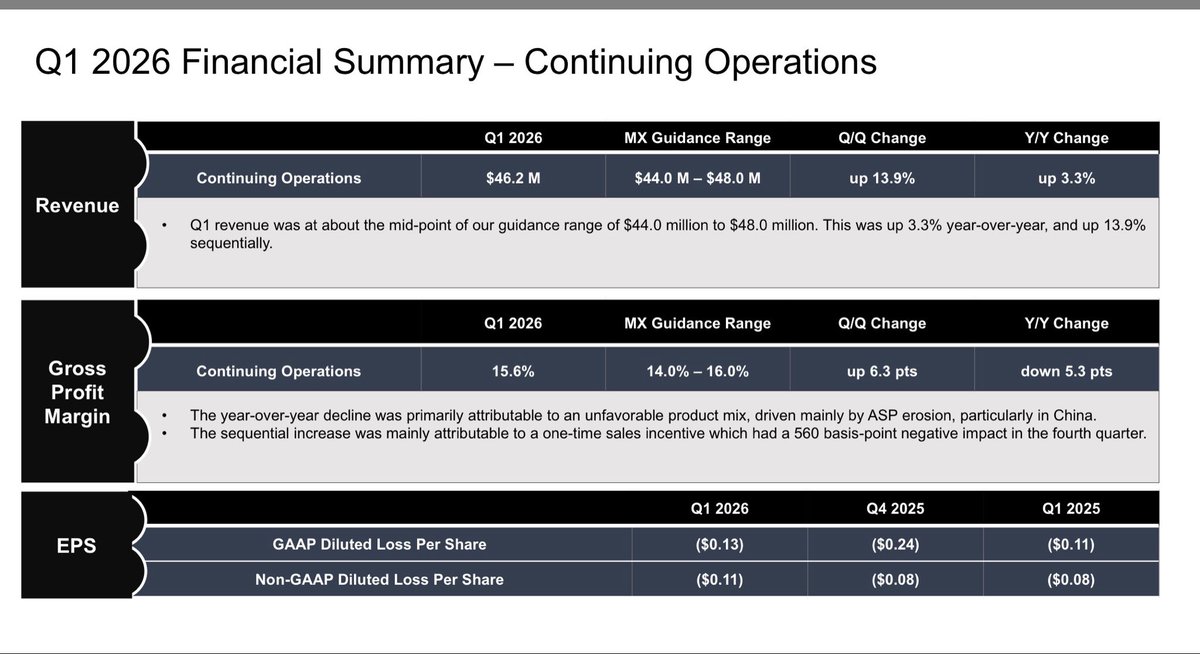

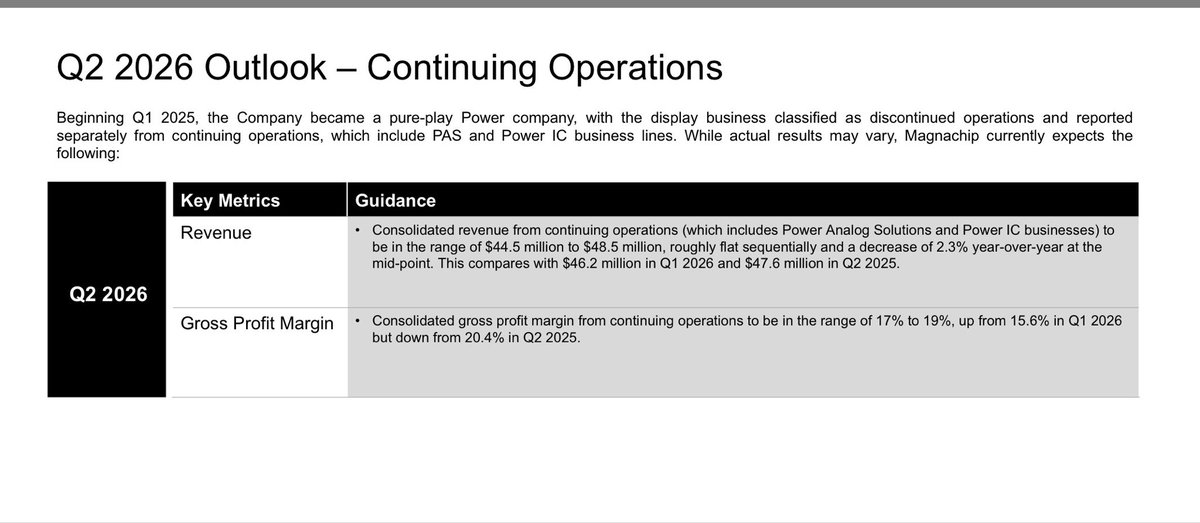

Magnachip $MX: The Anatomy of a Re-rating and a Harsh Lesson in Patience

The market is a brutal validator of narratives.

In my previous post, I warned of a "perfection hurdle" - a bar set so high that simply meeting expectations might not be enough to sustain April’s momentum.

The Q1 2026 earnings report confirmed this thesis: we received solid fundamental progress that ultimately lost out to an overheated sentiment.

Instead of focusing on the red candles on the chart, let’s look inside the filings.

That is where the true picture of the transformation is hidden.

1️⃣Operating Margins: A Return to Reality

Magnachip delivered a gross margin of 15.6% (up from 9.3% in Q4 2025).

➡️The Analysis:

This was a precise hit at the upper end of management’s guidance.

The company is proving that the pivot toward Power Analog Solutions (PAS) is fundamentally improving the profitability of every dollar sold.

➡️The Context:

Despite this progress, the market is still hungry for a return to the historical 20%+ levels.

However, standing in the way is a planned infrastructure upgrade at Fab 3 (Gumi), which will force downtime in the second half of the year.

This is an operational bottleneck that must be closely monitored.

2️⃣Inventory Dynamics: Moving Past the Glut

Perhaps the most interesting metric in this report isn't the earnings, but the DIO (Days Inventory Outstanding), which dropped to 77 days.

In the semiconductor sector, this is the key to distinguishing real demand from "channel stuffing."

Magnachip is effectively digesting its inventory, suggesting that the pull-through for the new 8th-generation MOSFETs in the server segment is authentic and organic.

3️⃣The Balance Sheet as an Insurance Policy

At the current market valuation ($135M), the company holds $94.6 million in cash.

This implies that at today’s prices, the market is valuing Magnachip’s entire IP portfolio, its South Korean fabrication facility, and the 55 new products slated for 2026 at a fraction of their replacement value.

This is a classic "Deep Value" setup, where the margin of safety is built on hard assets rather than just growth promises.

⬇️Conclusion:

Assessing the Cycle

Magnachip is currently in a difficult transition phase - caught between speculative euphoria and a long-term fundamental renovation.

This latest report strips away the "meme stock" label and returns the focus to pure operations.

An investor must now weigh two opposing forces:

➡️Short-term headwinds:

The planned downtime at Fab 3 and conservative Q2 guidance limit the room for explosive growth in the immediate months ahead.

➡️Long-term leverage:

Successful penetration of the Power Management market for AI servers, coupled with a valuation trading near cash-levels, creates an asymmetrical risk profile.

Rather than predicting price targets, the critical question to ask is this: do you believe in Magnachip’s ability to establish itself as a vital power-chain provider before their cash cushion thins?

The Q1 results suggest the foundation for this shift has been laid, but the path to full-scale profitability will be a process, not a singular event.

$NBIS looks poised for $185+ after the small tweezer top led to a perfect backtest of the 1.272 log Fibonacci level at $133, forming a hammer candle that signals a higher low

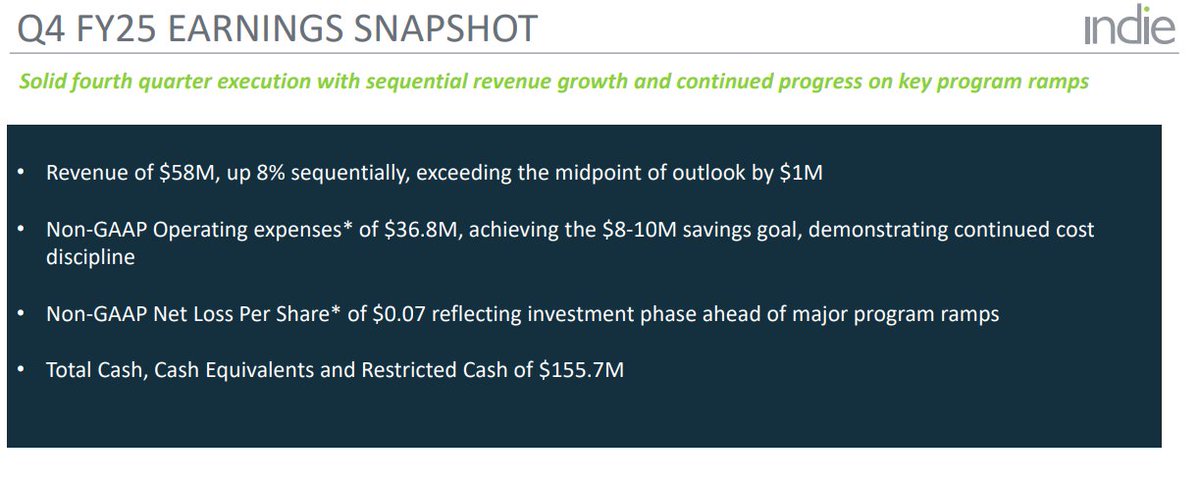

Everspin ($MRAM): Q1 2026 Earnings Update – Beyond the Market Reaction

Yesterday’s 38.59% price surge to $18.28 reflects a sharp market re-rating following a significant earnings beat.

For the long-term investor, however, the priority is determining if the fundamentals now support this valuation or if the move was purely sentiment-driven.

1️⃣ Financial Performance: Product vs. Licensing

Total revenue reached $14.9M, hitting the high end of management's guidance.

➡️ The Shift: Product sales grew 28% year-over-year to $14.1M. This is a vital transition; the company is moving away from sporadic licensing fees toward a recurring, product-based revenue model.

➡️ Margins: Gross margin remains healthy at 52.7%. This confirms pricing power in niche markets, allowing for high operational leverage as volume increases.

➡️ EPS Breakdown: While GAAP EPS was reported at $0.40, this was inflated by one-time tax benefits. The Non-GAAP EPS of $0.11 is the figure to watch, as it represents true operational profitability.

2️⃣ The $40M Defense Contract: A Revenue Bridge

The 2.5-year, $40 million agreement with a U.S. Defense Prime Contractor is the primary anchor for the current stock confidence.

➡️ Scope: The contract focuses on Toggle MRAM process technology and engineering services for the U.S. Defense Industrial Base.

➡️ Financial Impact: It secures roughly $16M in annual revenue. This acts as a "bridge," funding R&D and operations while the company waits for the longer design-in cycles of the automotive and AI Edge sectors to mature.

3️⃣ Valuation: Assessing "Fair Value" at $18

With a market cap now near $425M, the stock is trading at approximately 7x trailing sales.

➡️ The Benchmark: In the semiconductor space, a 7x P/S ratio for a company with $15M quarterly revenue suggests the market is already pricing in a significant portion of 2026–2027 growth.

➡️ Upside Requirements: To sustain a move toward the $25–$30 range, Everspin must break the $20M quarterly revenue barrier. This hinges on the 256Mb STT-MRAM qualification (expected July 2026) and the Microchip wafer ramp-up.

4️⃣ Risks and Operational Realities

Despite the momentum, several hurdles remain that require a cautious outlook.

➡️ Timeline Lag: The Microchip foundry partnership in Oregon is a marathon, not a sprint. Significant recurring orders from this deal are still not projected until 2H 2027.

➡️ Litigation Burden: Everspin is aggressively defending its patent moat. While necessary, these legal fees will continue to impact GAAP net income in the coming quarters.

➡️ Competitive Moat: High-density standalone modules remain Everspin's defense against eMRAM (embedded) solutions from giants like TSMC. Success depends on maintaining this technical lead in harsh-environment applications.

⬇️Final Assessment

The "inflection point" is becoming visible in the financial data, but the recent 38% vertical move has likely pulled forward much of the immediate upside.

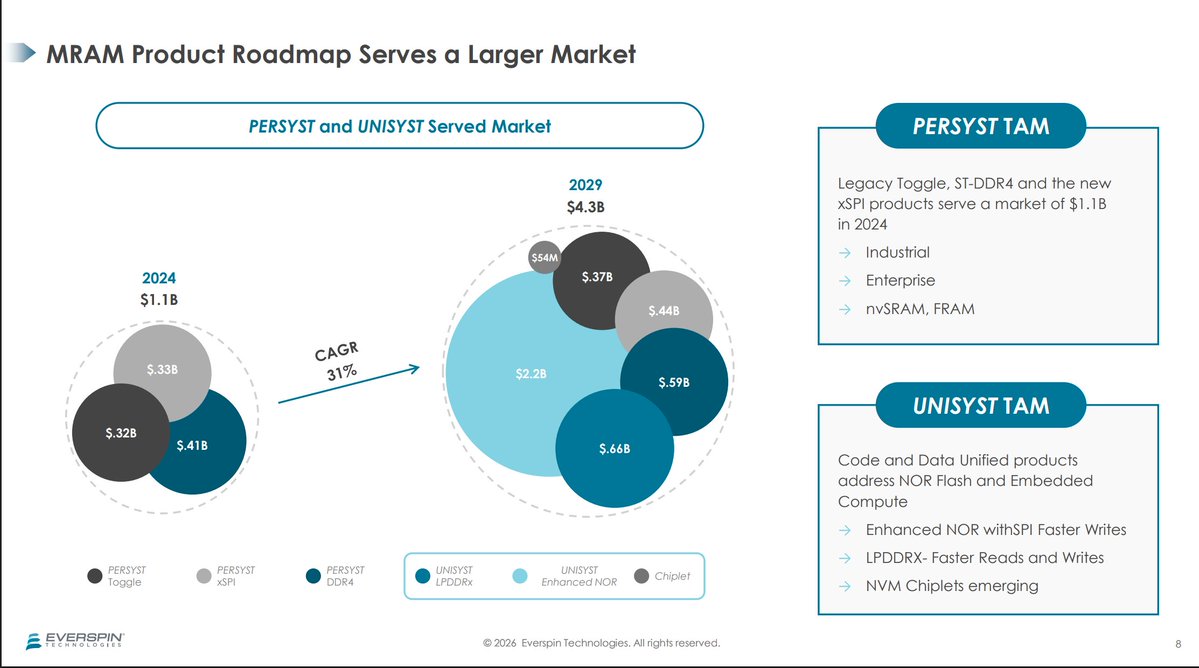

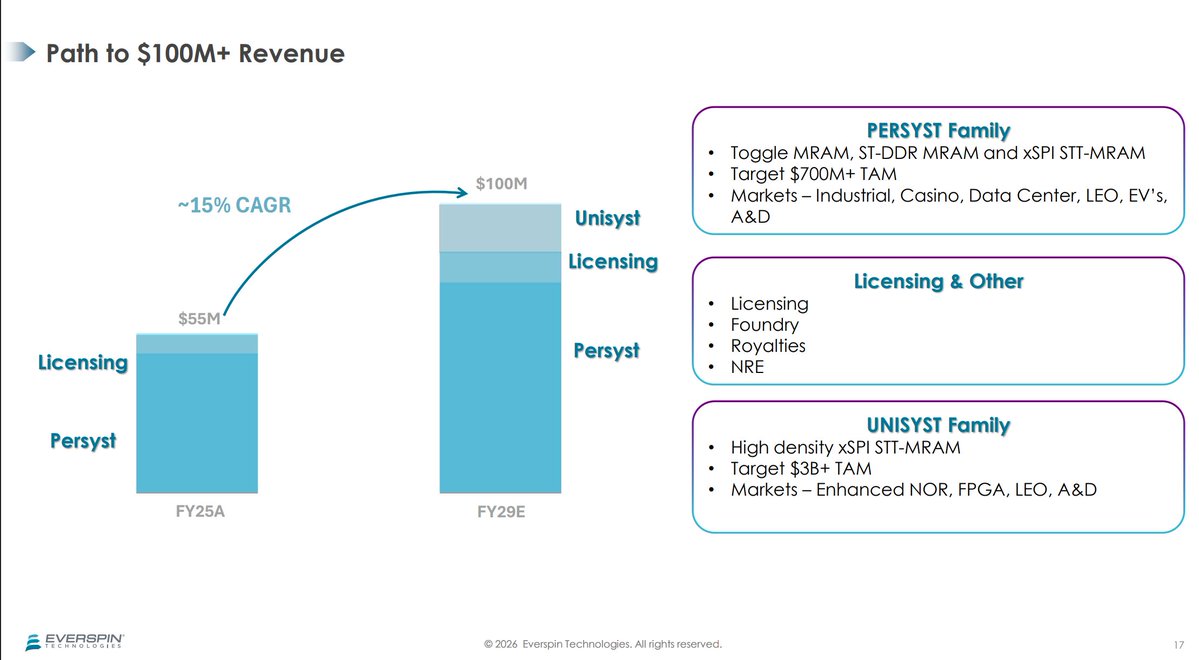

The long-term thesis for 2027 remains the core focus. The defense contract effectively de-risks the balance sheet, but the "mega-growth" catalyst still rests on the UNISYST family sampling in Q4 2026.

Everspin Technologies ($MRAM): A Brief History of "Memory That Doesn’t Forget"

Before we dive into the hard numbers of the upcoming earnings, we need to understand who Everspin is.

This isn’t just another Silicon Valley startup promising a revolution.

They are a pioneer and leader that has spent over 20 years (originating from Freescale/Motorola) building a technology that the world is only just becoming ready for in 2026.

➡️ What do they do?

Everspin is the world pioneer and dominant player in discrete MRAM (Magnetoresistive RAM).

Unlike traditional memory (like the DRAM in your PC or Flash in your phone), MRAM stores data using magnetic states rather than electric charges.

Why is it a "Big Deal" in 2026?

➡️Non-volatility:

Power off?

The data stays.

No batteries or capacitors required.

➡️Speed:

It operates nearly as fast as RAM but is as persistent as a hard drive.

➡️Endurance:

You can write to it billions of times.

Flash memory is a "toy" by comparison.

⬇️

Today, Everspin is evolving from a niche player for industrial meters into a strategic U.S. asset for AI infrastructure and automotive safety.

➡️When Will "Small Steps" Turn Into Massive Scale?

Investors watching Everspin have every right to feel a bit weary.

While the AI sector is growing exponentially, $MRAM has been delivering stable but modest quarterly revenues around $14M–$15M for some time.

This is a classic case of a company with "great tech" stuck in a long design-in cycle.

Here is the brutal and realistic assessment: When will we actually see the money on the table?

1⃣The "Design Win" Trap and the Real Revenue Timeline

Everspin boasts hundreds of design wins (238 in 2025 alone).

In the semiconductor industry, the journey from a "win" to "mass production" typically takes 18–24 months.

Realistic Outlook: Most AI Edge and Automotive projects contracted in 2024 will only start generating massive, recurring orders in H2 2026 and throughout 2027.

The Inflection Point: The landmark Microchip ($MCHP) agreement signed on April 8, 2026, is an operational breakthrough.

However, it's vital to note the timeline: while the first Toggle MRAM products from this deal may hit the market in late 2027, the higher-margin STT-MRAM production is expected closer to 2028.

Until then, expect steady growth rather than a vertical spike.

Until then, expect steady but slow growth.

2⃣ "Hard Truth": What Needs to Happen for the Stock to Soar?

The market is waiting for Everspin to break the $20M quarterly revenue barrier.

This is the level where operational leverage starts to work its magic: with gross margins exceeding 50%, every additional dollar of revenue flows almost entirely to the net profit line.

Watch the production ramp of the 256Mb STT-MRAM.

Qualification is expected to wrap up in July 2026, the Q4 2026 report could be the first real "revenue surprise."

3⃣The Competitive Landscape: MRAM vs. the Giants

While Everspin is the king of discrete (standalone) MRAM, they aren't playing in a vacuum.

To understand the risk, we must look at the "Hidden Giants":

➡️The eMRAM Threat:

Companies like TSMC and Samsung are increasingly integrating embedded MRAM (eMRAM) directly into their logic chips (at 22nm and 5nm nodes).

This means for simple tasks, designers don't need a separate Everspin chip.

➡️The "Discrete" Moat:

Everspin’s defense lies in high-density, high-reliability standalone modules (like the new 256Mb).

Unlike the giants who focus on mass-market consumer tech, Everspin owns the "Industrial & Aerospace" niche.

Their modules meet the AEC-Q100 Grade 1 standards, providing capacities and extreme-temperature resilience that embedded solutions from giants often cannot match.

➡️Operational Comparison:

While $MRAM is a "pure-play," investors often compare its growth to the Philadelphia Semiconductor Index (SOX).

For $MRAM to break out of its current valuation, it must prove that its growth rate can decouple from the general slow-moving industrial sector and align with the high-velocity AI infrastructure market.

4⃣Is Everspin a Takeover Target?

The structure of the 10-year Microchip deal suggests deep integration.

In the tech world, such partnerships are often a prelude to a full acquisition.

For Microchip, buying Everspin would be a logical step to dominate the non-volatile memory market for the Aerospace & Defense sectors.

➡️Verdict:

If you’re looking for a stock that will show +50% revenue tomorrow morning, you’ll be disappointed.

Everspin and Magnachip are games of patience.

Tonight’s results (11:00 PM CET) will likely be "stable," but the key will be management’s commentary on the Microchip wafer ramp-up speed.

➡️My strategy for “future” companies like Everspin:

Accumulate on dips, but aim for 2027. That is when "tomorrow's technology" finally shows up in the Excel sheets as today's profits.

It's not financial advice. DYOR.