Dad | Vet Sniper | Ex-GM & HoB (FCA) | BSc Hons Economics/Data Science/CS Python Applied Quant Student | TA • EW • Crypto/TradFi/DeFi | Be Your Own Bank | NFA

Navigating the Chaos Corridor

Bitcoin’s Power-Law Ascent and the Symmetrical Fracture of Fiat Reality

The Chaos Corridor is a statistically bounded monetary ecosystem, a tunnel within which Bitcoin’s price evolves under persistent power-law dynamics. It is not merely a curve or trend; it is the envelope of energy accumulation, compression, and release within a system constrained by supply, adoption, and network security:

P(t) ~ A * t^n

Across multiple estimation techniques ordinary least squares (n ≈ 5.69), median quantile regression (n ≈ 5.82), and pairwise delta analysis (n ≈ 5.74) the exponent converges near 5.7, reflecting sustained super-linear adoption. This spine is structural, directional, and persistent, indifferent to volatility, drawdowns, or euphoric spikes. It is the mathematical heartbeat of Bitcoin, underpinned by hashpower, settlement finality, issuance constraints, and network adoption metrics.

Quantile regression wraps the spine, forming the corridor:

- Lower quantiles (3–25%): compression zones, deep accumulation, latent energy.

- Upper quantiles (85–99%): rapid dispersion zones, where stored energy is released via singularity-like repricings.

- Median quantile: dynamic fair value, corridor center of mass.

What appears chaotic is energy redistribution, not disorder. Volatility clusters as adoption, liquidity, and sentiment arrive asynchronously. Current price levels (~$91,000) lie within lower-quantile compression, historically a prelude to expansion, with supports between $65,000–$80,000 representing where energy has historically condensed.

Singularity Events and Log-Periodic Scaling

Resolution occurs through singularity-like events bubble formations with log-periodic acceleration, where adoption and liquidity overcome the system’s ability to distribute smoothly.

Quantitative support includes:

LPPL / Money or Debt data: λ ≈ 2.07; fundamental modes observed in BTC/Gold residuals (2011, 2013, 2017, projected 2027).

Harmonics: explain secondary oscillations, aligning with larger residuals (2021 first harmonic).

Predictive fidelity: log-periodic fits outperform 4-year cycles in RMS error, reflecting endogenous network-driven dynamics.

Each singularity reinforces the spine, redistributing price at a higher altitude rather than collapsing. Current projections: upper-quantile expansions $110,000–$130,000+, mid-2027 crest near $195,000, and historical overshoot potential $300,000–$350,000 before further redistribution.

Symmetry: Bitcoin Adoption vs Fiat Debasement

The corridor is inherently symmetric: Bitcoin adoption is matched by persistent structural decay of fiat.

- Since Nixon Shock (1971), U.S. M2 expanded from ~$710B → >$22.3T (~31×, 6.6% annualized), silently eroding purchasing power (~2.6% annual drag).

- Inflationary drag & Cantillon effect: Productivity grew ~80% (1947–2009), while real wages rose ~8%; asset holders captured disproportionate gains.

- Debt accumulation: Federal debt >$38T, interest >$1T/year; austerity triggers recessionary feedback; debasement is the equilibrium, not a policy choice.

- Silent Depression: Real income plateaued post-2001 China Shock; purchasing power down ~50% since 1975; wages lag GDP by ~66% since 2000; corporate profits doubled (5→11% GDP).

Societal consequences: deaths of despair ~2.7×, drug/alcohol fatalities 5×/4.6×, suicides at Great Depression highs, birth rates down 20–30%. Generational assets diverge sharply — Boomers far outpace Millennials/Gen Z.

Macro signals: liquidity expansions, M2 uptrends, commodity curls, dovish interventions — provide temporary relief but reflect systemic fragility.

This is zero-sum, not asymmetric: each validation of digital scarcity corresponds to further fiat debasement, erosion of trust, and generational imbalance.

The Digital Stack and Structural Migration

Stablecoins: $260–$307B market cap, $23–33T annual volume, anchor reserves in Treasuries, suppress yields, facilitate refinancing, migrate value to programmable infrastructure, amplifying symmetry.

Regulatory clarity (GENIUS Act, CLARITY Act): reduces friction for institutional flows, accelerates adoption. Unlocking fresh tier/layers of capital.

De-dollarization: manifests as fragmentation — local currencies for spending, USD for liquidity, Bitcoin for long-term reserve integrity.

Sovereign allocations: >$120B by late 2025, projected toward $300B in 2026 — risk-managed adoption of digital scarcity.

The Chaos Corridor as a Conservation Law

Inside the corridor:

- Bitcoin oscillates, accumulates, releases energy, adhering to the power-law spine.

- Singularities redistribute energy predictably, not chaotically.

- Legacy fiat erodes continuously via debasement, debt accumulation, generational inequity as the cost of system persistence.

Volatility is the cost of truth - appreciation is inseparable from decay in legacy paradigm. The power law ensures long-term structural integrity, while the corridor contains chaos and redistributes energy.

The Chaos Corridor is the price-level signature of the digital monetary transformation bounded, directional, mathematically indifferent to legacy. It is bullish for digital scarcity, devastating for fiat fragility, and inevitable.

Inspired by -

@moneyordebt@infraa_@jameslavish

Note on the data source: the original chart used data whose terms restrict redistribution on third-party sites. On June 16, 2026 I switched the data source to Coin Metrics Community Data (CC BY-NC 4.0), so the chart now runs entirely on free, openly-licensed data. The power-law model and methodology are unchanged. Free, non-commercial use is welcome — please just keep the source/license credit visible.

https://t.co/cfl6sLkL1q

The link is the same as before, so you don't need to change anything.

DKG v10's mainnet rollout is underway, introducing a robust, conviction-based staking system.

15M TRAC is already committed at launch via the new Publisher Conviction mechanism — and our own @DrevZiga breaks down how to use the staking dashboard.

For ethereum:0xaa7a9ca87d3694b5755f213b5d04094b8d0f0a6f holders:

→ Delegate to nodes and boost your staking factor up to 6x

→ Stake migrates to v10 nodes on @Gnosis and @Base

→ Migrating delegators receive ≈2 epochs of lock credit

As security audits clear, we'll continue toward mainnet deployment of @origin_trail v10.

Protecting the sovereign context infrastructure for trusted AI — together!

$WTI $USO $USOIL

Geopolitical de-escalation removes the war premium, a but it does nothing to fix the structural arithmetic deficit.

Look past the paper noise.

The cleanest physical signals remain loud and clear: steep backwardation and aggressive storage draws.With global operational slack sitting at zero, China’s re-entry is the highest-conviction swing factor on the board. The paper-to-physical spread is coiled for violent upside

https://t.co/MiBpTz0zJ3

Good morning with good news: Global energy storage additions skyrocket 41% to 158 GW/459 GWh in 2026!

Annual additions double 2026 level by 2032 & exceed 1000 GWh by 2033.

Global solar capacity rises to ~6.5 TW in 2030 from 2.9 TW in 2025.

https://t.co/4w6E8g9Ui2

🚢Claims about Hormuz reopening are exactly why we built this:

If ships start moving through the Strait with AIS transponders on, you’ll see it in the index — updated every 30 minutes alongside Suez, Bab al-Mandeb and Panama.

🗣️"Southeast Asia is set to account for 20% of the growth in the world’s energy demand over the next decade, second only to India"

More from IEA's @fbirol on what’s needed to ensure secure & affordable energy supplies in the region as demand rises 👉 https://t.co/ARQ2bCFnGX

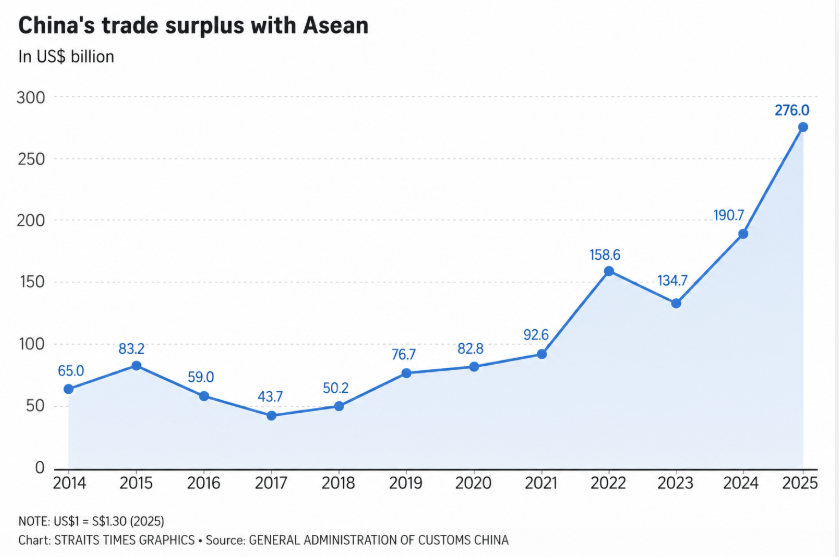

China is pursuing an ultra-expansionist policy of total economic domination in the Asia-Pacific, the region that will become the centre of global trade.

China runs a $276bn trade surplus with ASEAN, while India has a $99bn trade deficit with China. Over the years, both deficits have only continued to grow.

China is taking over regional markets and creating structural dependence in key sectors by massively subsidising its companies to undercut and destroy national industries.

The objective is that in 20 years, when India and Indonesia become two of the four world’s largest economies, and Vietnam, the Philippines and Malaysia become multi-trillion-dollar economies, their industries will already be structurally dependent on China.

A country that depends on China for goods, inputs, technology and industrial capacity cannot have an independent foreign policy. That is China's goal.

Asia home to around 60% of the global population and projected to generate around 50–52% of global GDP by 2050 will become economically monopolised by China.

The only way to avoid this is through an aggressive commercial foreign policy. Europe needs to coordinated trade agreements, investment, supply-chain alternatives and market access policies to reduce Asia-Pacific dependence on China’s trade balances.

NEW: US and Iranian sources have expressed diverging interpretations of some key aspects of the recent US-Iran agreement. The full text of the agreement has not yet been published, which makes it difficult to ascertain which interpretations of the agreement are accurate.

Other Key Takeaways:

Iran’s interpretation of the agreement’s provisions about the Strait of Hormuz would constitute a significant strategic victory for Iran if its interpretation became the recognized reality. Iranian statements indicate that the regime defines an “open” strait as one that remains under Iranian management, which conflicts with US and global commercial interests.

The reopening of the Strait of Hormuz depends on the risk calculus of shipping companies and captains. Continued Iranian threats against commercial shipping may have a negative impact on the willingness of companies and captains to resume transiting through the strait. Iran’s mine-laying activities and threats to mine the strait are also a key component of this effort.

Hezbollah has signaled that it will adhere to the Lebanon ceasefire outlined in the US-Iran agreement and suggested that the group views the agreement as a precursor for Israel’s withdrawal from Lebanon.

Israeli officials have stated that the IDF will continue to operate in Lebanon to degrade Hezbollah. Hezbollah and Iran could make their implementation of the US-Iran agreement contingent upon the cessation of Israeli operations against Hezbollah in order to push Israel to halt these operations.

The global commodity index has retraced to early‑March levels: geopolitical risk premia are being priced out and markets are pivoting from supply‑shock anxiety to an ‘abundant supply’ mindset.

via Bloomberg

Central banking operates as a legalized monopoly that would make John D. Rockefeller green with envy. When you grant one institution exclusive control over the money supply, you create the most powerful cartel in human history. The Federal Reserve doesn't compete for customers; it simply prints their purchasing power away.

Free banking systems operated successfully across multiple countries and time periods before governments monopolized money creation. Scotland from 1716 to 1845 experienced remarkable monetary stability under competitive note issuance. Canadian banks weathered the 1930s depression far better than their American counterparts, partly due to fewer regulatory restrictions. These were real markets serving real people.

Competition forces private banks to maintain reserves and honor their commitments. Your local bank can't just conjure money from thin air without consequences. Other banks will demand redemption in specie, creating natural market discipline. When Chase issues too many notes relative to its reserves, Wells Fargo will present those notes for payment. This clearing process keeps everyone honest.

Central banks face no such constraints. The Fed creates trillions of dollars without backing, because who exactly will demand redemption? Congress? The Treasury? They're all part of the same wealth extraction scheme. When private banks fail, depositors lose money and investors learn painful lessons. When central banks fail, taxpayers absorb the losses while bureaucrats collect pensions.

You live under a monetary system where twelve unelected officials determine interest rates for 330 million Americans. They meet eight times per year in marble halls, adjusting the price of money like Soviet planners setting wheat quotas. Every boom and bust cycle flows from this central planning apparatus that free market thinkers recognized as fundamentally unsustainable over a century ago.

Your savings account loses value by design, not accident.

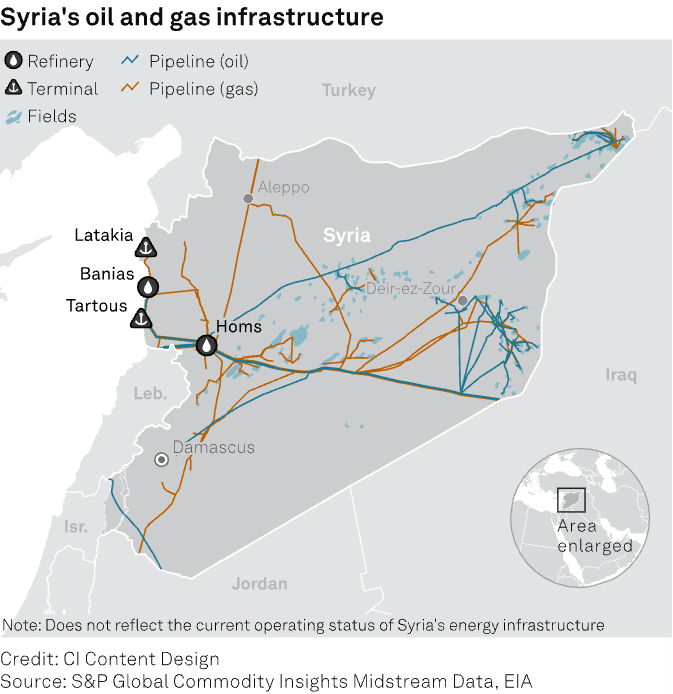

🇸🇾Syria was a war zone for 13 years.

This week, ConocoPhillips is signing a deal to drill there.

That sentence would have been unthinkable 18 months ago.

Then Assad fell in late 2024.

New government.

US sanctions eased and suddenly the energy majors started circling one of the most underleveraged hydrocarbon basins in the Middle East.

ConocoPhillips and Novaterra Energy will develop existing Syrian gas fields and explore for new ones alongside state-owned Syrian Petroleum Company.

They're not alone... TotalEnergies and QatarEnergy already signed for offshore Block 3 near Latakia in May.

Syria has gas, it's close to Europe and it just got a new government that's actively courting Western energy investment.

The Middle East energy map is being redrawn in real time.

The question is who gets there first.

ConocoPhillips just answered that question.

ConocoPhillips is set to sign the first major U.S. energy contract with Syria’s new government this week. Onshore gas field development and exploration with the Syrian Petroleum Company (partner Novaterra). This follows the May 2026 offshore Block 3 technical deal alongside TotalEnergies and QatarEnergy.

The timing is critical.

Assad fell December 2024.

Abu Mohammad al-Jolani took power January 2025.

Trump terminated most U.S. sanctions July 2025.

MoU signed November 2025.

Deals accelerating now in mid-2026.

This is not random corporate expansion. It is de-escalation and normalization executed through capital contracts.

Follow the Money Lens

MIC/FIC/TIC complexes are exchanging contracts: U.S. energy majors (COP) + European (Total) + GCC state energy (QatarEnergy) + local partners. These deals de-risk the Levant, reduce Russian/Chinese leverage in the Eastern Mediterranean, and lock in Western-aligned supply chains.

Rebuild under new alignment: Gas production ramp (target +4-5 million m^3/day) directly powers Syria’s grid while signaling that the new Damascus administration is open for business.

Sanctions relief + diplomatic engagement (Sharaa’s White House and Gulf visits) created the legal and political runway.

Middle East as the new capital marketplace: Post-normalization Syria is becoming an entry point for large-scale capital. BlackRock and major asset managers, alongside GCC sovereign wealth funds (Saudi PIF, Qatar Investment Authority, Mubadala, etc.), are positioning for energy, infrastructure, and reconstruction flows. The Levant offers high-upside, de-risked assets once sanctions and conflict overhangs clear.

Why this moment matters:

AI-driven electricity demand is exploding. Hyperscalers need firm baseload power that only natural gas can deliver at scale in the near term. COP’s move secures new low-cost reserves while helping stabilize regional grids, indirectly supporting global LNG flexibility and U.S. supply chain security.

The Dragon-Bear axis (Russia-China influence via old Syrian networks) is being displaced by pragmatic Western + GCC capital deployment. Energy contracts are the leading edge of normalization. They create mutual economic interests faster than diplomacy alone.

This is classic follow the money. When MIC/FIC/TIC players start signing production-sharing and exploration deals in a former war zone within 18 months of regime change and sanctions relief, it marks a structural shift — not a one-off transaction.

🇸🇾Syria was a war zone for 13 years.

This week, ConocoPhillips is signing a deal to drill there.

That sentence would have been unthinkable 18 months ago.

Then Assad fell in late 2024.

New government.

US sanctions eased and suddenly the energy majors started circling one of the most underleveraged hydrocarbon basins in the Middle East.

ConocoPhillips and Novaterra Energy will develop existing Syrian gas fields and explore for new ones alongside state-owned Syrian Petroleum Company.

They're not alone... TotalEnergies and QatarEnergy already signed for offshore Block 3 near Latakia in May.

Syria has gas, it's close to Europe and it just got a new government that's actively courting Western energy investment.

The Middle East energy map is being redrawn in real time.

The question is who gets there first.

ConocoPhillips just answered that question.

ADNOC just sold 30 million barrels of crude in 2 weeks.

India, China, Japan, South Korea every major Asian refiner in one fire sale.

Let me tell you what's really happening here.

During the Hormuz war, ADNOC kept exporting but secretly.

Transponders switched off.

Ship to ship transfers in the dark.

Cargoes slipping through the strait hoping Iranian drones weren't watching.

That crude piled up, at Fujairah storage (Zirku Island) Floating on tankers waiting for a safe window.

Now with the ceasefire MoU the window opened.

And ADNOC moved fast selling before the official agreement was even inked.

The buyers jumped:

→ India's IOC and BPCL: 6 million barrels

→ China's Unipec: 6-8 million barrels

→ South Korea's SK Energy: 7 million barrels

→ Japan's Eneos: 3 million barrels

→ Vitol and traders: another 6 million+

All priced at parity or tiny premiums.

Not the crisis prices you'd expect.

This is the stored-up supply that was waiting behind Hormuz coming to market all at once.

It's real.

And it will pressure spot prices short-term.

But 30 million barrels is about 3 days of pre war Hormuz traffic.

The structural deficit doesn't disappear in a fire sale.

Long-term US Treasuries vs gold are collapsing.

- 2014: Global central banks stopped buying US Treasuries on a net basis

- 2014-2026: Long-term US Treasuries vs gold are down 85%

- 2025: Gold surpassed Treasuries as the top reserve asset

In a world where trust is evaporating, gold is becoming the preferred reserve asset.

🇨🇳China's gasoline demand just fell more than 20% in a single year.

EVs are now 60%+ of all new car sales in China.

Traditional gasoline car sales collapsed by a 1/3.

People are taking public transit more.

Goldman Sachs projects Chinese gasoline demand falls another 5–6% in 2026.

The world's biggest oil importer is becoming structurally less dependent on gasoline.

But gasoline isn't the whole story.

China doesn't just burn oil in cars.

It uses crude for petrochemicals, aviation, shipping, industrial production, and power generation.

And here's what that chart doesn't show...

China is using less gasoline because it's replacing it while using crude for it's industry.

Gasoline peaks,but total crude demand from China is still growing, just in different forms.