Finally hit my first $1 million, been in and out of markets since 2018, last 12 months have been my most consistent and profitable. Started fresh with $50k in September 2024 in $MTM after a few rough years with no returns. Now to not give it back!

$NVU $4DX $ATX #ASX

Server-grade DDR5 memory costs $27 to $37 per GB today, and prices have risen 300 to 400% since mid-2025. For AI workloads that are consuming memory faster than fabs can produce it, that is a significant infrastructure cost challenge.

Marvell Structera CXL devices address this through a purpose-built hardware block that compresses data at full memory bandwidth as it is written to DRAM and decompresses it on read, completely transparent to the host CPU. The result is that the host sees more memory than physically exists on the device, at ratios that can reach 2:1 or higher on real-world data types.

Director of Product Marketing Arifur Rahman details how the technology works and what it means for the economics of CXL memory pools: https://t.co/KlPv37vcY9

Terrible hold so far, but lots of potential to meet all the criteria for a contract with US gov and a relatively small comparative market cap $PUSA

Manufacturing scale is already proven, units are cheap, US army already has familiarity with their systems too

Powerus Launches Guardian-1 Interceptors to Defeat Low-Cost, One-Way Attack Drones

• Powerus recently announced a proposed merger with Aureus Greenway Holdings Inc. (Nasdaq:AGH), positioning Powerus to become publicly traded upon completion.

• Guardian-1 is designed as a cost-effective, high-speed counter-drone interceptor targeting hostile one-way attack drones, such as the Shahed-136, seen in modern conflicts.

• The Guardian-1 platform was tested during large-scale battlefield exercises at the National Training Center by U.S. servicemembers.

• The Guardian-1 platform is available to U.S. government customers and approved allies.

WEST PALM BEACH, FL / ACCESS Newswire / March 18, 2026 / Autonomous Power Corporation, doing business as Powerus, a company co-founded by former U.S. Army Special Operations veterans that builds and scales autonomous drone systems for military and commercial use in high-risk environments, today introduced the "Guardian-1 Interceptor," a low-cost, high-speed counter-drone interceptor platform built to defeat hostile unmanned aerial threats at scale. The system recently completed flight demonstrations alongside war-game exercises at the National Training Center, validating its performance in the hands of U.S. Servicemembers.

Guardian-1 is built to deliver major cost advantages to traditional drone defenses, as it is designed for high-volume production, and rapid capacity expansion. The system's availability is designed to speed up U.S. defense responses, which have traditionally favored larger, slow-to-develop weapons systems that require extensive training and planning.

Existing interceptors have proven untenably expensive for countering low-cost, unmanned systems. The "missile math" problem, first encountered in the Ukraine-Russia conflict, and now the Middle East, demonstrates that it's too costly to down a $30,000 drone with a $1 million interceptor. Powerus's focus on high adaptability led to the introduction of the Guardian platform to defeat threats posed by one-way attack drones and loitering munitions, including systems, such as the Shahed-136 and comparable long-range strike drones.

Link below for the news:

https://t.co/6WZmDEOtVs

@powerus_usa@AureusGreenway@DominariSec

#Powerus #Guardian1 #Drone #DefenseTech #AutonomousSystem #AGH #DominariSecurities #Dominari

$TRT doubling isn’t random, it’s the market finally waking up to what burn-in actually means in AI.

They just printed real growth and landed a meaningful order tied to next-gen AI GPUs likely $AMD and that’s the key shift. Reliability is becoming a bottleneck, not an afterthought.

Everyone is chasing compute and optics but if these chips fail at scale, the whole stack breaks.

That’s why $TRT and even $AEHR start to matter more as this cycle matures.

It’s not hype. It’s the part of the stack nobody pays attention to… until it’s mission-critical.

Researching $HAWK HawkEye 360

Space/Defense/Sensing

Just filed S-1. IPO likely early May.

Last private valuation ~$2B.

Net income positive (rare in Space sector, let alone prior to IPO).

🔹Only commercial company operating a large-scale (30+ sat) constellation of RF signals intelligence satellites. Detecting, geolocating, and analyzing hidden radio signals that traditional imagery satellites can’t see.

🔹2025 revenue of $117.7M (74% YoY growth and triple 2022 levels), with net income flipping positive at $2.7M and Adjusted EBITDA hitting $24.8M. Seems to be turning the corner from heavy R&D spend to high-margin scaling.

🔹Contract backlog exploded to $302.7M (6x YoY). Recent events will probably push this higher. Multi-year revenue predictability under a recurring, subscription-like model. Pretty rare for the Space sector.

🔹61% of revenue already from pretty big U.S. defense/intelligence customers, with international revenue recently increasing to 39% and climbing fast. Rising defense budgets, electronic warfare, GPS jamming, and maritime threats (South China Sea, Red Sea, etc.) are structural demand drivers that are likely to persist.

Biggest Customers:

▫️National Reconnaissance Office (NRO) – #1 customer

▫️National Geospatial-Intelligence Agency (NGA)

▫️U.S. Space Force

▫️U.S. Navy (significant recurring contracts)

DYOR, I am still doing mine but giving you guys an early heads up.

"Rumors that SpaceX will buy GlobalStar were the buzz at SatShow 2026 last week."

https://t.co/YuUnHqkpoE

“I think everyone’s convinced that there will be a sale of Globalstar,” @TMFAssociates , founder of the satellite research firm TMF Associates, told @malleven33

$4DX

One of a few of my bigger fumbles recently.. This one hurts the most …. and this was only half the position that was sold on this date, well done to holders!

Plenty of value long term next to $PME

#ASX

Modern warfare has a math problem.

$30K drone vs $4M interceptor

That model doesn’t scale.

How do you defend at volume without breaking the bank?

#DefenseTech#Autonomy

Started a position in $HIMS, seeing a lot of demand for these grey market peptides (BPC, CJC and Tesamorelin etc)

$HIMS should be a huge beneficiary to this trend, particularly if FDA goes ahead with “un-greying” them

$AGH - Aureus Greenway, owning two public golf country clubs in Florida

🔹Announces Reverse Merger bringing the drone company Powerus to the public market

🔹Creating a New American Manufacturing Drone and Defense Company $PUSA

🔹KCGI committed $50 million to purchase Powerus common stock by April 6, 2026

🔹Merger approved by both boards and a majority of each company’s stockholders

🔹Powerus subsidiaries include heavy-lift UAS with 500lb+ payload capability

🔹Low float near 15M shares

👇 5% / $4.98

#Photonics trade really taking off overseas. Not much to pick from on the ASX but $BLG $BLG.ax starting to get some interest . (Held)

Recent deal with Toptica and a US defence extension

$SHMD I took a position in Schmid, a German AI chips pick and shovel play.

The AI hardware revolution is creating an immediate necessity for Glass Core Substrates as organic materials hit physical limits on heat dissipation and interconnect density. Intel has confirmed glass substrates enable 10x denser interconnects compared to organic substrates, while Intel, Samsung, and AMD are all actively developing this technology for next-generation AI chips with 100+ billion transistors. This represents a fundamental architectural shift required to extend Moore's Law into the 2030s, making adoption a structural inevitability for high-performance computing.

Schmid is positioning itself as essential infrastructure for this transition. The company's InfinityLine technology suite provides the wet-process equipment needed for manufacturing, addressing the core technical challenge of creating defect-free Through Glass Vias (TGVs) at scale. Through its January 2025 partnership with TRUMPF, Schmid's chemical etching processes enable the precision required for high-volume production. The company claims to operate "the sole supplier for full TGV lab with all process steps necessary to turn a bare glass substrate into an Advanced IC Package," positioning it at the critical tooling layer as major chipmakers race to deploy this technology.

The investment setup crystallized with January 2026's $30 million financing and explicit 2026 guidance. Management projects revenue exceeding €100 million in fiscal 2026 with adjusted EBITDA margins above 12%, representing substantial growth from 2024's ~€61 million revenue base. This is backed by a €53+ million machinery order backlog as of mid-November 2025, recent equipment orders from leading Asian advanced packaging manufacturers, and the first InfinityLine C+ installation at a major Japanese customer in December 2025.

The opportunity spans the $31 billion advanced IC substrate market projected by Yole Group for 2030. This market includes the physical platforms on which semiconductor chips are mounted and interconnected, driven by AI and HPC demand. Schmid's InfinityLine equipment performs the critical wet-chemical processes (etching, developing, plating, cleaning) required to manufacture these substrates across multiple technologies: next-generation glass cores, traditional advanced organic substrates using semi-additive processes (mSAP/SAP), and large-format panel-level packaging solutions. While glass specifically represents a fast-growing $586 million segment (15.7% CAGR), the buildout serves as a technology-leading wedge for broader equipment sales across all substrate types. As an equipment provider rather than a capital-intensive substrate manufacturer, Schmid can potentially generate strong returns as the industry deploys capacity simultaneously.

The company must regain SEC filing compliance, with the 2024 Form 20-F expected in February 2026 to address current Nasdaq delisting notices. At approximately $400 million market cap, this presents a classic high-risk, high-reward setup and it's still relatively cheap. If management executes on guidance while expanding market share across the substrate equipment ecosystem, the current valuation implies dramatic upside potential. The downside involves execution challenges, but the upside case offers multibagger potential if the company navigates the next 12-24 months successfully.

Key catalysts: (1) Order announcements across glass and traditional substrates, (2) Q1 2026 results demonstrating revenue and margin trajectory, (3) Major customer wins as Intel, Samsung, and others accelerate deployment, (4) Strategic partnerships expanding ecosystem position, (5) Successful Form 20-F filing restoring Nasdaq compliance.

The asymmetry derives from a market cap disconnected from the scale of opportunity and Schmid's position as infrastructure provider for what multiple industry leaders have validated as the next substrate architecture.

Thanks to @pennycheck for drawing my attention to this company!

$LASR been watching this one since $50, watching the tech in action and seeing the economics of it makes this a very interesting play

Looking to enter tonight

BREAKING:

🇮🇱 Israel used its laser air defense system against rockets launched from Lebanon.

The “Laser Dome” (Or Eitan) laser system successfully intercepted rockets from Lebanon.

A new era of defense.

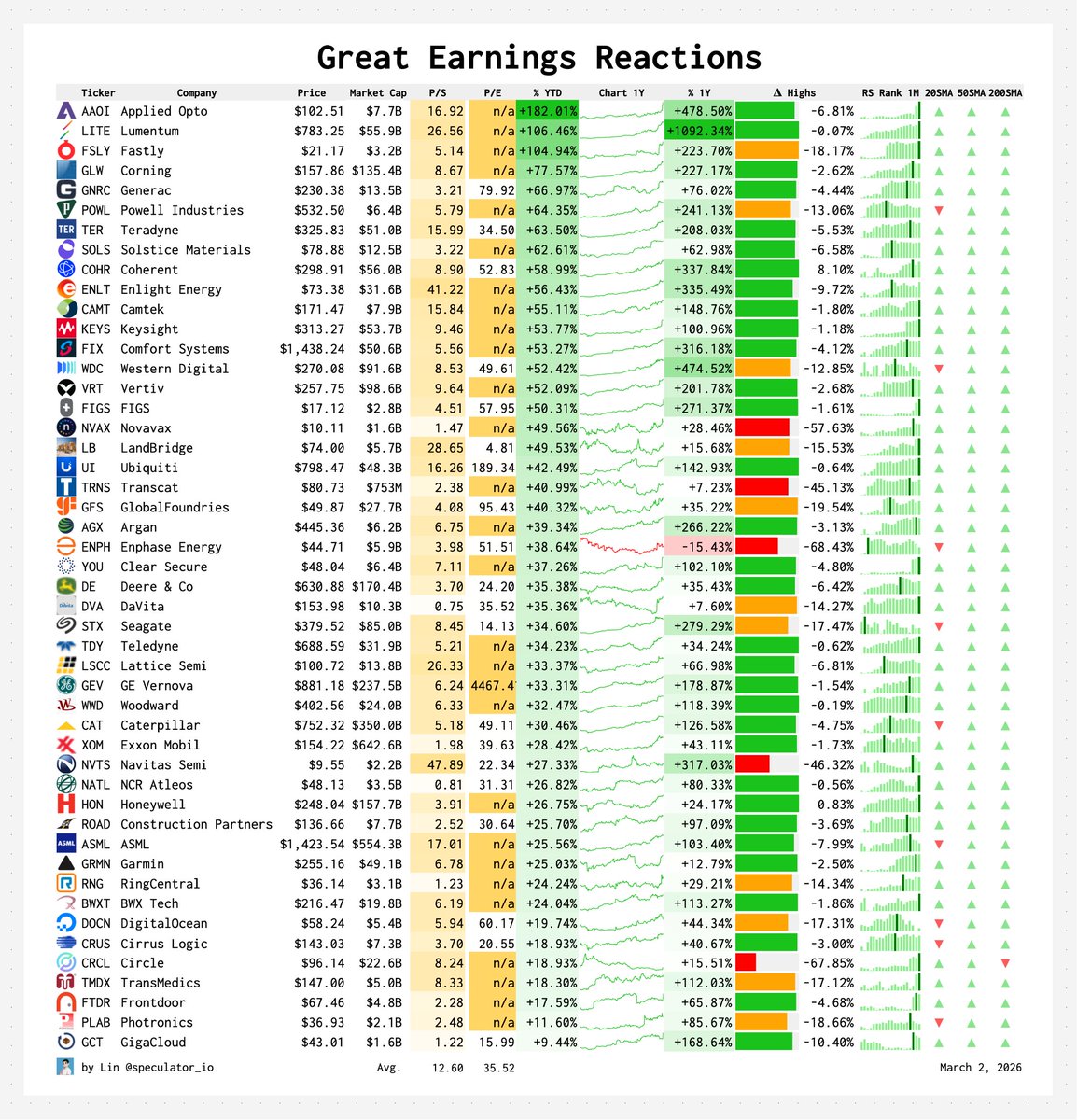

One of the best ways to find the next big winner is to track how stocks react to earnings.

So, here are some of the best earnings right now:

$AAOI Applied Optoelectronics +182.01%

$LITE Lumentum +106.46%

$FSLY Fastly +104.94%

$GLW Corning +77.57%

$POWL Powell Industries +64.35%

$TER Teradyne +63.50%

$SOLS Solstice Materials +62.61%

$COHR Coherent +58.99%

$ENLT Enlight Energy +56.43%

$CAMT Camtek +55.11%

$KEYS Keysight +53.77%

$FIX Comfort Systems +53.27%

$WDC Western Digital +52.42%

$VRT Vertiv +52.09%

When companies surprises to the upside, the market is repricing the company. Everyone raises their price tragets. Funds that were underweight now need to buy and push the stock price higher.

Sometimes it is just a one hit wonder and the move fades after a few days.

But in other cases, it turns into a lasting catalyst, especially if the earnings confirm that growth is accelerating and the company is starting to emerge as one of the next potential leaders.

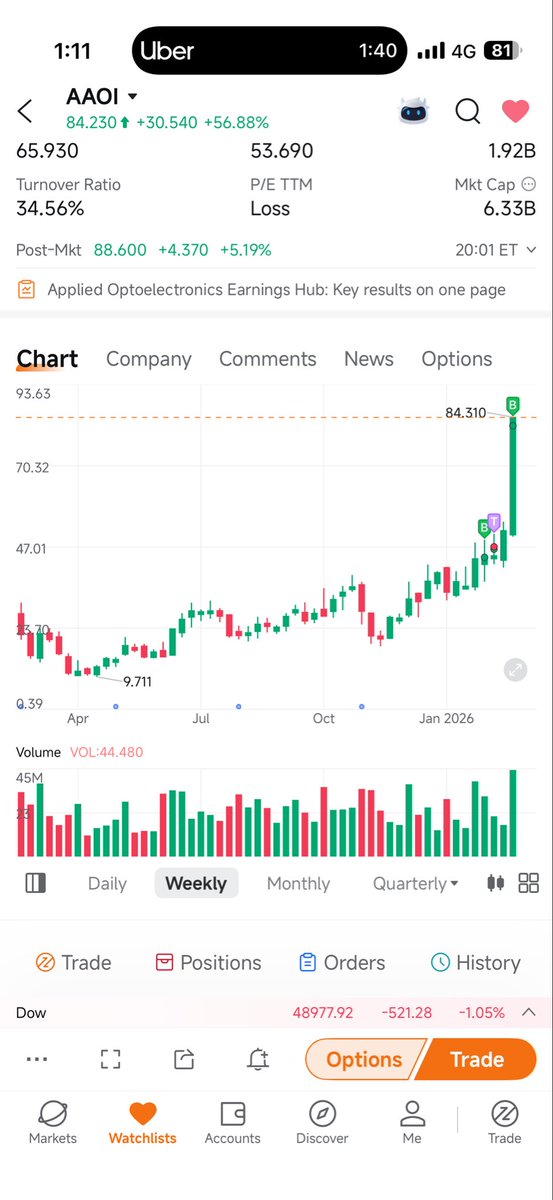

$AAOI

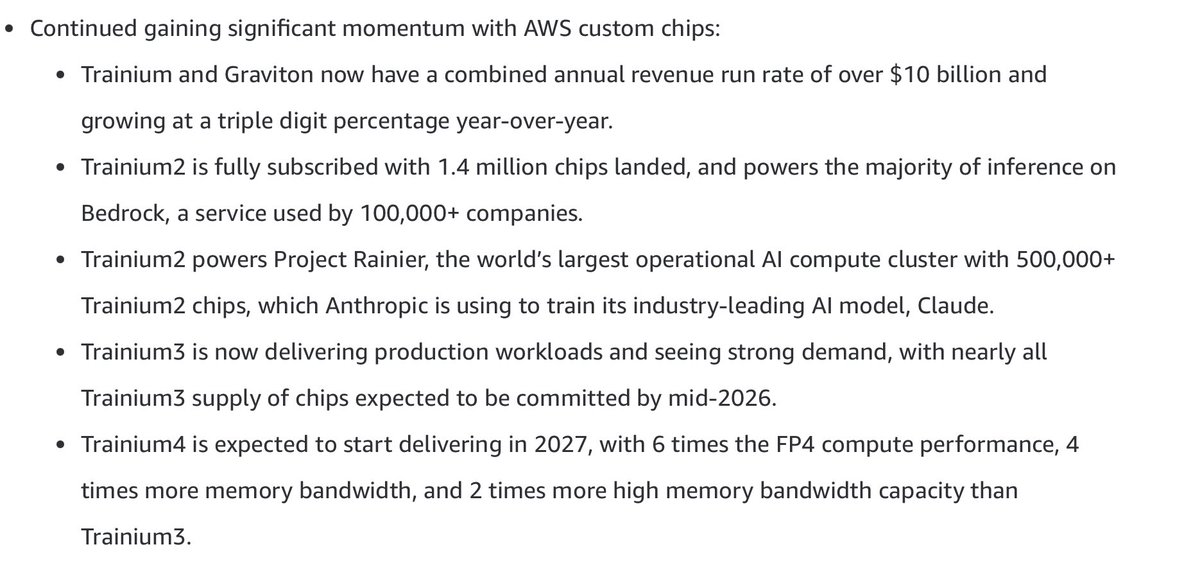

$AMZN trainium chip deployments at massive scale can only bode well for $AAOI. The ceo/founder mentioned customers in discussions to invest $200-300m into their new texas fab so they can lock in transceiver supply. With amazon capex coming in way higher than expectations, the need for this transceiver supply is higher than ever.

Dont forget, all the demand for Anthropic is the main driver behind this.

$AAOI is the best proxy for upside from Anthropic. Name one better, Ill wait.