It started with a phone call.

In late 2022, a Navy officer called Bryon Hargis (SpaceX's government sales director) — basically begging for a new entrant in the missile market.

Hargis didn't just pass the message along.

He, a SpaceX salesman, and a finance manager started working nights and weekends — then left SpaceX that November to build hypersonic missiles themselves.

The early grind was brutal. More than 50 investors and banks rejected them in their first five months. Some lumped the company in with alcohol and guns as a "vice."

They kept going — and applied the SpaceX playbook to weapons:

→ A clean-sheet hypersonic taken to 25+ flight tests in 2.5 years.

→ A $350 million round (led by Altimeter and Lightspeed), valuing Castelion at $2.8 billion.

→ A manufacturing approach built to produce thousands of missiles a year, not dozens.

What stays with me is why Hargis says he's doing it:

"I have two young kids — I don't want them to have to experience a war in their lifetime. This is how I'm giving back to them."

That's the part most coverage misses. The thesis behind a lot of this new defense-tech wave isn't bravado — it's deterrence. Build enough capability fast enough that the conflict never starts.

The lesson for founders: "50 no's, including people who call you a vice" is not a failure story. With the right conviction and the right moment, it's the first chapter.

Crusoe stock is up 682% in the past two years.

What started as a bitcoin miner burning natural gas nobody wanted has become one of the most valuable AI infrastructure companies in the world.

Now it's a builder behind OpenAI's Stargate — at an implied $30B valuation.

The unlock: While every AI cloud fought over the same power grid, Crusoe ran GPUs on stranded gas — the kind oil wells flare off as waste.

Years of cheap power, remote GPU experience — already built — right as the 2023 GPU shortage hit.

So when AI compute exploded, they didn't have to learn the hard part. They just pointed it at AI.

Revenue reportedly went ~$152M (2023) → ~$500M (2025E). Bookings up ~5x.

Crusoe had to decide if they were a bitcoin miner or an AI infrastructure company.

They chose the latter and havent looked back since.

Amazon and Anthropic reportedly just renegotiated part of their deal.

Starting next year, Amazon will pay for Claude based on the number of tokens used — not the amount of compute time.

And now Amazon is looking to OpenAI and its own Nova models to help bring those AI costs down.

The founder of Anduril and the CTO of Palantir backed the same nuclear startup.

Last week it hit criticality — a live, self sustaining reactor it built in just 9 months.

The company is Valar Atomics.

They build nuclear reactors small enough to load onto a military cargo plane and designed to power things like army bases and AI data centers.

The thesis behind Valar:

AI's real bottleneck is no longer chips — it's power.

Valars plan is to build 'gigasites' clusters of thousands of small reactors used to feed data centers directly, instead of relying on the grid.

Funding so far: $19M seed → $130M Series A → ~$450M, reportedly at a $2B valuation.

The same names building America's defense stack are now funding the power to run it.

🚨 Breaking 🚨 OpenAI just designed its own AI chip.

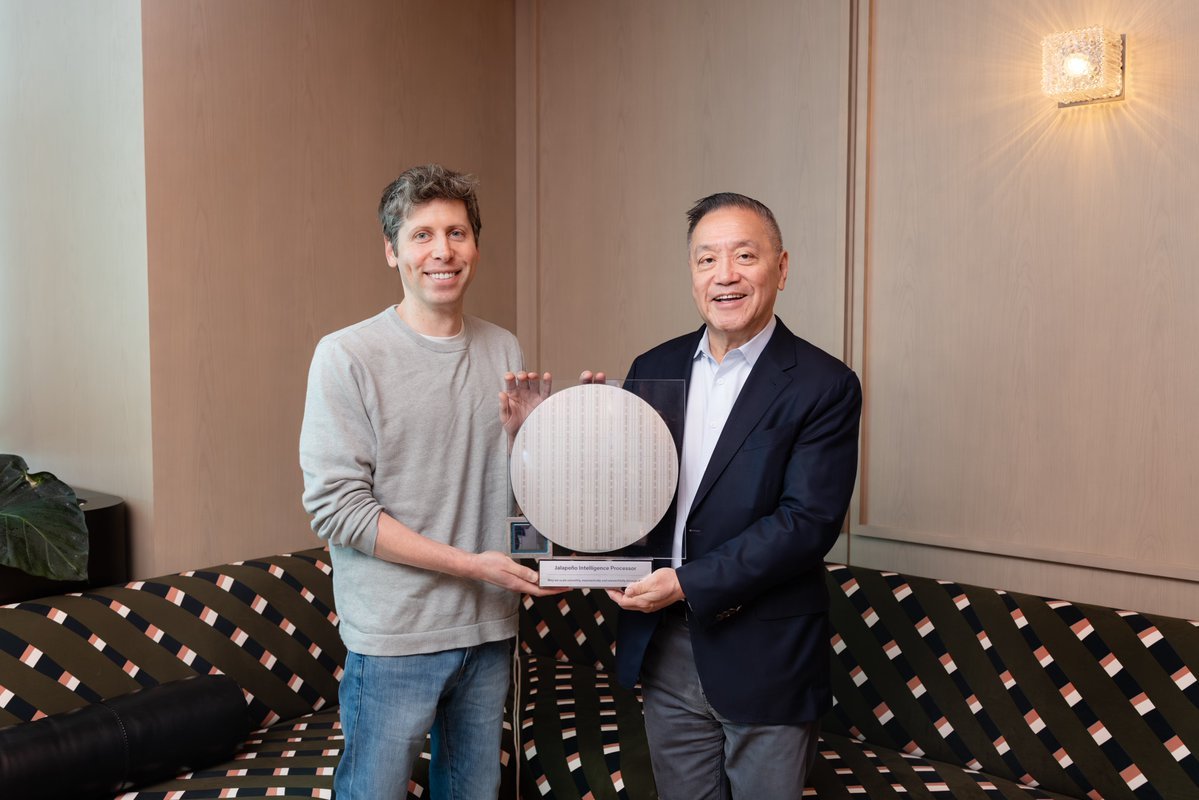

It's called Jalapeño — built from the ground up by OpenAI, brought to production with Broadcom ($AVGO), and purpose-built for LLM inference: the workloads behind ChatGPT, Codex, the API, and whatever agentic products come next.

Three things make this matter for anyone watching OpenAI's path to public markets:

1. The full stack play. OpenAI now spans products → models → infrastructure.

They're no longer just renting compute — they're designing the silicon underneath it. That's the Apple playbook, applied to AI.

2. The unit economics. Reportedly, custom inference silicon could cut OpenAI's inference costs meaningfully (Bloomberg has floated ~50%). For a company widely reported to be laying groundwork for a 2026 IPO, a credible path to cheaper compute is exactly the story public markets want to hear.

3. The Nvidia question. This isn't OpenAI beating the H100 in a benchmark. It's the largest AI buyer signaling it wants leverage over its own hardware bill. Google has TPUs. Amazon has Trainium. Meta has MTIA. Microsoft has Maia. Now OpenAI has Jalapeño — and Broadcom is the workshop building all of it.

Reportedly co-developed from design to tape-out in nine months. Initial deployment targeted for late 2026, scaling through 2029.

Microsoft is restarting Three Mile Island — the most infamous nuclear plant in America — for one reason: to power its AI.

That's how intense the data center race has gotten.

AI needs enormous, around the clock power, and wind and solar can't deliver it on demand.

So in a single year, Big Tech signed more than 10 gigawatts of new nuclear deals — Microsoft, Amazon, Google, Meta — all racing to lock up the only clean power source that runs 24/7.

That scramble is quietly opening one of the most interesting setups in energy investing.

I asked Aaron Dillon where the money is actually moving, what companies are leading the charge, and what technologies he's keeping an eye on.

Full conversation on YouTube 👇

Educational content, not investment advice.

PRE-IPO STOCK MARKET UPDATE - JUN 17, 2026 | Enterprises are moving to AI LLM open architecture solutions; Large language models vs world models and how to pick some winners; Exponential vs linear growth in technology will yield incredible investment opportunities

Click to watch = https://t.co/g56NhfRE0V

An AI price war is now reshaping the economics of the entire sector, and the pressure is coming from the cost side rather than the demand side. OpenAI has been optimizing to maximize token spend, but a wave of inference optimization across both software and hardware is forcing frontier labs to bring per-token prices down or cede share. Open-source models are the lever, with the strongest options today coming out of China (DeepSeek, Kimi K2.5) and US application companies increasingly willing to route everyday workloads to them. Several AI application CEOs now expect to run almost entirely on open source within one to two years, reserving frontier closed-source models for only the most complex tasks where they can cost roughly 50 times more per token. A new category of model routers, exemplified by Factory AI, is emerging to match each query to the cheapest and best-suited model, turning model selection itself into a margin lever. At least one US open-source contender is already carrying a $25 billion valuation, Reflection AI. The takeaway is that the next super cycle is an optimization cycle, and value is migrating toward whoever compresses inference cost without sacrificing output quality.

Jeff Bezos has stepped directly into the frontier-model race with Project Prometheus, which raised $12 billion at a $41 billion valuation to build what it calls artificial general engineers. The structure is notable for how much institutional capital has lined up behind a company that has not yet shipped a product. The thesis is that AI can be pointed at engineering itself, designing and then stress-testing systems such as rocket engines inside virtual environments before anything is physically built. That ambition places Prometheus squarely in the world-model camp, where simulated environments substitute for expensive real-world iteration. A $41 billion pre-product valuation is aggressive on any conventional basis, and it signals that investors are underwriting the category rather than current revenue. We would treat the raise as a marker of how much capital is now willing to chase applied AI at the engineering layer, and as confirmation that compute-rich incumbents intend to compete on their own terms.

Decart released a new world model that goes after the single biggest bottleneck in generative AI, video generation. One large provider was spending roughly $15 million a day to output clips that still took a long time generate, far from instant. Decart lifted a video-generation model off its original setup and onto an AWS Trainium chip, increasing inference output by 8 times while cutting cost by 2 times. AI world models extend well beyond entertainment into self-driving (Tesla), humanoid robotics (1x and Figure AI), and industrial/manufacturing. These AI models are becoming core infrastructure, and the companies that optimize the hardware-to-model fit will capture a disproportionate share of the value.

Robotics scaling now looks exponential rather than linear. Once a humanoid robot learns a task, that skill can be copied across an entire fleet, and one Figure AI robot has already run a single task for three days straight without stopping. The next unlock is robots building other robots, which turns factory output into a compounding curve while a fleet-wide data flywheel, much like Tesla's cars, makes every unit more capable over time. The near-term applications are concrete, spanning factory logistics, household tasks, and elder care, where a home robot could let aging parents stay in their own homes one to three years longer at a lower expense vs a human at-home care nurse. The investment framing is that robotics is 12 to 18 months away from a 6 to 9 month window in which it has its ChatGPT moment, after which valuations could re-rate sharply, with a 5 to 10 times move possible before the shift becomes obvious. We would position at the beginning of that window, with particular attention to humanoid platforms, their proprietary world models, and the AI infrastructure layer that all of this runs on. Note that this is a high-conviction, long-duration thesis, and the timeline carries real execution and capital risk that argues for sizing exposure accordingly.

In 2011, a Navy SEAL lost teammates all because they were clearing a building they couldn't see into.

His answer to that night is now worth $12.7B

Meet Shield AI 🇺🇸

After 7 years of service, Founder Brandon Tseng believed losses like this were preventable.

So in 2015, he and his brother built software to make aircraft fly themselves.

They called it Hivemind — a software that enables drones and jets to navigate with no GPS, no remote pilot, and no signal to jam.

It's been flying in real combat since 2018, and they're now rolling out X-BAT: an autonomous jet that needs no pilot and no runway.

The numbers:

→ $2B raised in March at a $12.7B valuation

→ More than double its price a year earlier

→ Projecting $540M+ in revenue in 2026

The real story is who's writing the checks. Blackstone and JPMorgan used to leave defense to Lockheed and Boeing.

Now they're backing a founder who lived the problem — and built the fix.

@MilkRoadAI@GavinSBaker Gavins right.

The companies that have secured the most gigawatts coming online in 2026 and 2027 are positioned for very strong years ahead.

Everyone in AI is racing to build bigger models.

A 2 year old startup just raised $300M betting that's the wrong race.

Decart builds AI that generates a drivable 3D world in real time from a text prompt — Toyota wants to crash-test self driving cars inside it.

Decart's world models are: Cheaper, open to any developer, and have 100,000+ people already building on it.

Nvidia, Radical Ventures, Toyota, and Nintendo's founding family are all in. ~$4B valuation.