$MCCK shareholder letter is pretty good. They own physical gold because they don’t trust the government’s ability to overspend and foresee hyperinflation. Also hidden in here is the potential for returning capital via Dutch tender offer.

$UTGN growing BV fast (10% in 1 quarter) because of the appreciation of their oil & gas investments.

Q2 will be even better. The SoH is still closed, so perhaps further beyond as well.

Surprised the share price hasn't gone up more. A lot more upside to this one, IMO.

1/ Southern Realty Co. $SRLY is an interesting little company with 18,000 net acres of mineral rights in California's Central Valley.

It's got a $1.8MM market cap with cash + securities at $1.25MM, of mostly common stocks and treasuries.

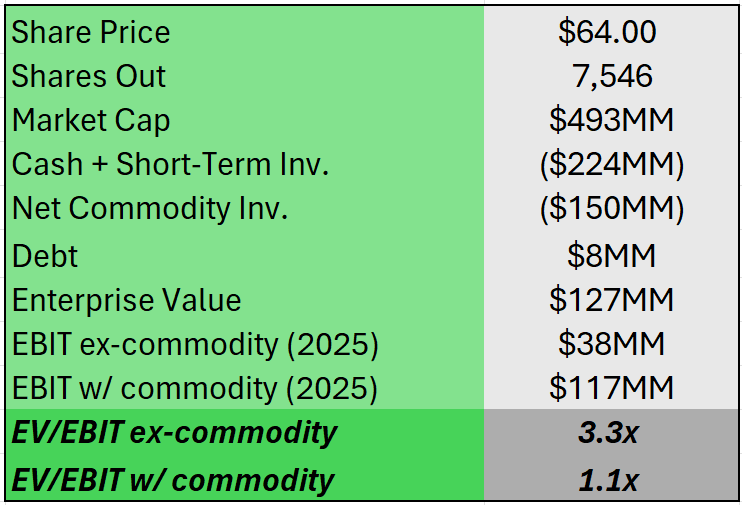

Mestek $MCCK is still wildly cheap after the 2025 annual report.

Looks like they sold off a big portion of their commodities from Q3.

Cash is up from $28MM in 2024 to $194MM today.

Here’s the updated valuation.

In investing it’s important not just the price to meet value but to remember this value can move up or down or stay same. If value moves down, you’re essentially screwed. If it stays same, it’s good but not great. When they say it’s okay to pay up for a good business, what they mean is you can pay up for one which is growing its value over time so while it’s expensive compared to today’s value, it’s cheap compared to value ten years down the lane. I seldom see good discussions on how company is creating or destroying value but a lot more on price differential vs value.

I hear people say a lot that Benjamin Graham is outdated, but this couldn’t be further from the truth.

His writing is academic, which is off-putting to some, but we really don’t have anyone else (to my knowledge) that lays out the questions regarding investing as he does.

He lays the whole thought process bare, considers opposing arguments. So much so that you aren’t sure at times what he really thinks.

I like looking at companies under $5MM.

In this niche, it’s trite by now to say that institutional investors can’t touch businesses of this size, but another fun part of these stocks is how little information there is.

I think it goes without saying that most retail traders aren’t going to look very hard at the financial statements, many hold these companies because they consistently pay a dividend.

But if you can dig, call management, and see what you can find from other channels, which only takes a little bit more work, you can really get yourself a big informational advantage.

4/ The company has been very generous with dividends and has paid out $1.3MM since 2020.

The real trouble with the stock is determining whether they can continue to get deals, as there is very limited information.

At any rate, it's worth watching.

3/ In 2020/2021 they received ~$1.2MM for oil & gas surface rights. In 2023, they received ~$900k due to two solar surface rights waivers.

There was essentially no revenue in 2022 and 2024, and 2025 was a modest $67,000 for the sale of excess water rights.