𝗣𝗼𝗿𝘁𝗳𝗼𝗹𝗶𝗼 𝘂𝗽𝗱𝗮𝘁𝗲 - 𝗠𝗮𝘆 𝟮𝟬𝟮𝟲

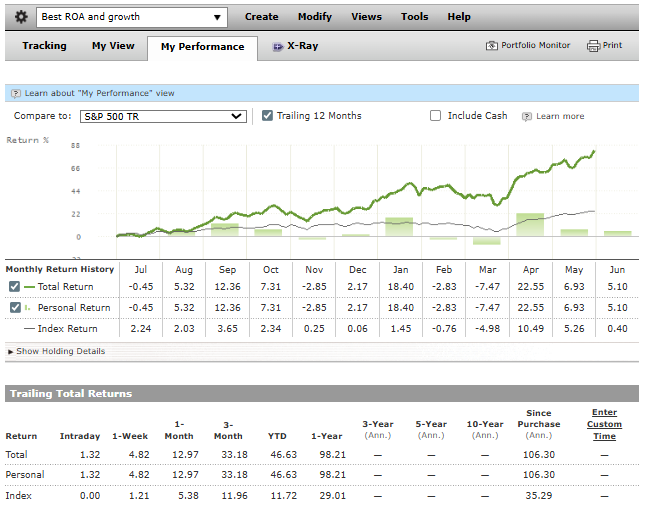

CL April 4.37%

SP500 April 5.26%

CL YTD 3.2%

SP500 YTD 11.3%

𝗧𝗿𝗮𝗻𝘀𝗮𝗰𝘁𝗶𝗼𝗻𝘀

In May, I made a few additions, shifting capital from low-volatility positions to growth stocks with the potential to outperform the index. The AI expansion is ongoing and sustainable, and I want to be part of it. This strategy may increase the volatility of my portfolio, but I see it as an opportunity, not a flaw. My portfolio is stress-tested monthly to ensure any drawdowns remain limited. I also hold significant capital in bonds and low-beta ETFs, ready to be deployed during a meaningful market decline, typically aiming for around 20%.

➖ To satisfy reallocation of capital, EVO, NVO, BIL were partially disposed and EEMV was fully disposed.

➕ Added RZLV (Generative AI / AI Software), SYM (AI Warehouse/Logistics within Robotics & Automation industry), JOBY (eVTOL / urban air mobility), EOSE (Energy storage / battery manufacturing), ASPI (isotopes/nuclear supply chain), Also added BTDR, CLSK, MARA. These 3 Data centers/BTC Miners standout as transitioning to AI/HPC with a hyperscaler deal expected in 2026. They now constitute 10% allocation. Once deal is announced, I expect shares to skyrocket. Diversification between different miners is key in portfolio construction. Market is pricing each of those separately based on 10% probability of a hyperscaler deal. But when combined, this probability rises exponentially.

➕ Added IONQ. My quantum computing bet.

𝗦𝘁𝗿𝗲𝘀𝘀 𝘁𝗲𝘀𝘁

If SP500 collapses by 50%, our portfolio is expected to drop by 27%.

𝗛𝗼𝗹𝗱𝗶𝗻𝗴𝘀 𝗮𝘀 𝗼𝗳 𝟬𝟭/𝟬𝟲/𝟮𝟬𝟮𝟲:

PRAB 12%

BIL 9%

SHY 7%

FTSL 4%

CLSK 4%

BKLN 4%

BTDR 4%

IEI 3%

ADBE 3%

USMV 3%

PNDORA 3%

LQD 3%

SPHD 3%

PYPL 3%

VGT 3%

EVO 3%

NVO 3%

MARA 2%

EOSE 2%

MBIN 2%

WKL 2%

EGBN 2%

Cash 2%

Other 17%

𝗕𝗿𝗲𝗮𝗸𝗱𝗼𝘄𝗻 𝗯𝘆 𝘀𝗲𝗰𝘁𝗼𝗿/𝗮𝘀𝘀𝗲𝘁 𝗰𝗹𝗮𝘀𝘀

Cash and equivalents – 30%

Bonds ETF – 14%

Consumer Cyclical – 10%

Financials – 14%

Technology – 13%

Low volatility ETF – 7%

Industrials – 6%

Healthcare – 4%

Communication Services – 1%

Basic Materials – 1%

CL.

@Q0MT6pFmbVqynsM Сравнить биток с золотом это как сравнивать гоночный болид с range rover. Каждый имеет свои плюсы и минусы. 50% drawdown для высоковолатильног актива это нормально.

Looking at hindsight, in April 2025 I made a huge mistake by not making this portfolio my main one.

I made my homework and at least now I know that this formula works. I am going to deploy full capital into top 10 stocks selected with this formula, but under certain conditions.

That condition is market drawdown >20%.

I don't think we will have to wait long for this.

Stay tuned, I will share everything online.

Still remember my Growth + Wide Moat portfolio I created in April 2025, subs?

Absolutely crashing the index.

The only regret about this portfolio is that it was a demo account.

Seriously, why would someone believe that $GIS is undervalued at 17B MC, when its average annual FCF is just 1.4B?

Don't be surprised that div yield is 8% at the moment, math is simple here.

Still remember my Growth + Wide Moat portfolio I created in April 2025, subs?

Absolutely crashing the index.

The only regret about this portfolio is that it was a demo account.

Market-implied intrinsic value for Sivers Semiconductors AB.

After 20x in just one year, it’s worth examining what expectations are currently embedded into $SIVE stock price.

To do that, I use Mauboussin’s market-implied CAP framework from his recent research paper “Competitive advantage period”.

Key expectations:

* For the first few years of explicit revenue forecast, I am using analyst consensus adjusted for mid-point since company already reported 1 quarter 2026. Afterward, I factor +50% until the end of the explicit period.

* I then calculate the terminal value assuming ROIC equals Cost of Capital after the end of the explicit period, i.e. any growth will not create value.

* Gradual EBITDA Margin expansion from current negative values to mid-double-digit in Year 17.

* WACC @ 9.2%.

* Tax rate 15% - in line with OECD’s Pillar 2 “Global Minimum Tax”

* The input that drives reinvestment is Sales to Capital ratio = 1.75.

At current price, market not only assumes very high returns on incremental capital going forward, but also a meaningful improvement in ROIC on existing capital.

This exercise is not investment advice, but rather an illustration of the key expectations infrastructure embedded into stock price.

You are required to do further financial and strategic analysis to assess whether those expectations are too low, too high, or about right.

AI expansion is currently at risk because of data centre delays.

Equipment (transformers & gas turbines) are genuine hard constraints. Lead times on large power transformers have stretched to 2–4 years in some cases, and gas turbines from GE Vernova, Siemens Energy, and Mitsubishi are essentially sold out well into the late 2020s. These are capital-intensive, low-volume manufacturing businesses that can't simply ramp overnight.

Labour is arguably the binding constraint right now. The passage flags electricians and pipefitters specifically - these are skilled trades that take years to credential, and the US already had a structural shortage before the AI buildout accelerated. The 30% labour cost premium for remote sites compounds this => hyperscale campuses in places like West Texas or rural Virginia struggle to attract and retain workers.

Grid interconnection is the third leg. Even if you have the equipment and the workers, getting a large load connected to the grid can take 3–7 years through the interconnection queue, which is why developers are increasingly pursuing behind-the-meter generation (gas turbines, SMRs in theory) to bypass it entirely. This then loops back to the turbine supply problem.

The compounding effect is what makes this tricky to model for investment purposes. Each constraint reinforces the others: remote sites chosen partly because grid capacity is unavailable there then face worse labour economics, which delays construction timelines, which pushes more demand into an already-strained equipment order book.

For the names I track - $MARA, $CLSK, $BTDR and the like, this is actually a mild competitive moat because they have sites already energised and interconnected. The barrier to replicating existing capacity is rising faster than it might appear on paper.

I am not buying $NBIS or $IREN.

That is too late => you overpay for MW of capacity in a commodity-like business.

Instead, I try to find other asymmetric opportunities. 👇

Such names are definitely riskier.

For sure have a lot to prove.

But still have a chance to become a multibagger from here.

Already have Mara, BTDR and CLSK in my portfolio.

Tomorrow I will add $HIVE.

With huge delays in Data Center construction across the US, industry will have no choice but to notice miners transitioning to AI/HPC.

Diversification between different miners is key in portfolio construction. Market price each of those separately based on 10% probability of a hyperscaler deal. But when combined, this probability rises exponentially.

Do you know why the windshield is so big and the rearview mirror is small?

What's ahead is 100 times more important than what's behind.

If you stare back all the time, you'll crash into a pole.

You do need to look back sometimes, but just to avoid repeating your mistakes.

This applies to investing as well. Markets price the future, not the past.

Press the throttle and drive forward. It's all just beginning.

While everyone is talking AI, there is a tiny industry that can have even greater long-term potential.

Today, I give you $YES.NE CHAR Technologies.

No name with a 38M MC.

Operating within engineered carbon removal => CAGR 50% potential.

Here is why I see potential for exceptional returns

* First facility began commissioning in Q1 2026, reducing project risk.

* Path to $131M annual project revenue and $42M free cash flow across five facilities.

* Long-term contracted revenue, including a 20-year RNG offtake and a 5-year, 62,500-tonne biocarbon agreement.

* Multiple growth vectors: core facilities, EU licensing, and PFAS destruction.

* Strong forecasted margins supported by non-dilutive project financing.

Strategic partnerships and validation

* ArcelorMittal holds a 7.3% stake and signed a biocarbon offtake agreement, validating steel industry demand.

* Elkem signed a 5-year, 62,500-tonne biocarbon offtake and sold its Saguenay facility, expanding into ferrosilicon markets.

* BMI Group is a 9.46% shareholder, providing $18M in project commitments and construction resources.

* Indigenous partnership secures wood waste feedstock, with $ 80M+ in potential revenue.

Project pipeline and financial projections

Five-facility pipeline targets $131M annual revenue and $42M free cash flow to equity => more than entire MC!

* Thorold facility: $28M revenue, $9M free cash flow, 10,000 tonnes biocarbon, 425,000 GJ RNG annually.

* Lake Nipigon: $44M revenue, $14M free cash flow, 15,000 tonnes biocarbon, 750,000 GJ RNG annually.

* Additional projects in Saint-Félicien, Espanola, Saguenay, and Baltimore expand capacity and market reach.