There's a 6-week window where you can buy a house 30% off and the seller thanks you for it

The homeowner wants you to show up. The bank wants you to show up. The law requires the whole thing be published publicly so you can find it

It's called pre-foreclosure, and it's the most misunderstood moment in real estate:

What's happening: a homeowner has missed months of mortgage payments. The bank files a public notice (a "notice of default" or "lis pendens" depending on your state) that starts the foreclosure clock. The owner now has weeks to months before the house gets seized and auctioned

The part nobody explains: the homeowner still owns the house during this window. They can still sell it. And selling is usually the best thing that can happen to them:

If foreclosure completes, they lose the house, lose ALL the equity trapped inside it, and take a credit wound that follows them 7 years

If they sell during the window, they walk away with cash and no foreclosure on their record

Real math: the owner owes $61,000 on a house worth about $130,000. Foreclosure vaporizes their $69,000 of equity. You offer $95,000 with a fast close. The bank collects its $61,000 and goes away. The owner keeps roughly $30,000 they were about to lose completely. You bought a $130,000 house for $95,000. Every person in that story ended up better off than the alternative

The bank prefers this too. Foreclosing costs them tens of thousands in legal fees, and they lose money owning and reselling houses. Banks lend money. They hate holding property

How to find these:

The notices are public record at the county. Many county websites have free searchable lists. Zillow has a pre-foreclosure filter buried in its listing types. Paid tools like PropStream aggregate everything if you want convenience

Then contact the owner with the softest touch you have. A letter: "I saw the notice on your property. If selling fast would help, I can close in 2 weeks and you'd walk away with cash and your credit protected. No pressure either way"

Remember who you're writing to. This is someone in the worst stretch of their life. Job loss, medical bills, divorce. Half your value is speed. The other half is being decent. The investors who treat these families like prey wash out of this business fast and deserve to

Run your normal numbers: fixed-up value times 70%, minus repairs, is your ceiling. If their mortgage balance is too high for the math, walk away and tell them about a short sale (the bank agrees to accept less, slower process, sometimes their best option). Costs you nothing to leave someone with a map

You need speed money here: hard money lenders close in 7-14 days, which is exactly what they're built for

The auctions get all the YouTube videos. The smarter, kinder, less crowded deal happens 6 weeks earlier at a kitchen table, where you're the only buyer who bothered to write a letter

If you want to flip a house but have $0 in the bank, you can get funded for up to $150k with a hard money loan or 0% APR credit cards. I'll keep mapping these windows. Keep an eye out

You do not need 20% down to buy a house

Almost everyone believes you do. It's the single biggest reason people who could already own are still renting, saving toward a number that was never real

Where the myth comes from: put less than 20% down on a normal loan and the bank adds PMI, mortgage insurance, $100 to $250 a month, until you hit 20% equity. That's it. That's the whole penalty. It is not a requirement, it's a fee, and it falls off automatically later

To live in: FHA is 3.5% down. Conventional goes as low as 3%. VA and USDA are 0% down. The real gap is often $9,000 to $11,000 plus closing, not the $60,000 you've been killing yourself to save

But here's what nobody tells you, because it's the actual wealth lever. For an INVESTMENT property, the one that pays you, you don't use those loans at all. You use the funding the bank rejects you for, and it doesn't check your income:

The investor funding stack, exactly how I buy houses with almost none of my own cash:

1. HARD MONEY for the house. An asset-based lender funds 80 to 90% of the purchase and 100% of the renovation. They underwrite the DEAL, not you. No W-2, no tax returns. You need roughly a 660 to 680 score, some cash in the bank, and a deal that makes sense. Kiavi, Lima One, RCN, Easy Street. Pre-qualified in 48 hours

2. 0% CREDIT CARDS for the gap. The only cash left is your down payment plus closing, usually $18,000 to $25,000 on a cheap house. Cover it with 0% APR business cards, Chase Ink, Amex Blue Business, US Bank Triple Cash. $100,000 in 0% limits is normal for a decent profile. You pay zero interest for 12 to 18 months

3. EXIT before the clock runs. Renovate in 4 to 6 weeks, rent it, then refinance into a 30-year DSCR loan. That check pays off the hard money AND the cards before the 0% window closes. You never paid a dollar of interest, and your cash is back for the next one

Run the cost of waiting instead: spend 4 years saving for 20%, and prices climb the whole time, so the number you're chasing keeps running away from you while you pay rent with nothing to show for it

Stop saving toward a number a coworker made up. The money to buy your first investment property is sitting in a credit limit and a lender's account right now, not in a savings account you're slowly starving to build

(I help people build the exact funding stack, 0% credit plus hard money, and walk them into their first flip. It's all in my bio)

Fred Rogers met with a child psychologist every week for 22 years to build his show. She shaped everything: every script, prop, and song. The whole point was to give a child's nervous system time to slow down. In 1984, a single regulatory decision ended all of it.

The psychologist was Dr. Margaret McFarland, who co-founded the Arsenal Family and Children's Center alongside Benjamin Spock and Erik Erikson. She and Rogers understood that the prefrontal cortex in children, the part of the brain that controls impulse, emotion, and attention, takes decades to fully develop. At the start of every episode, Rogers tied his sneakers and changed his sweater while children settled in. Those pauses were intentional, designed to help a child's nervous system shift into a calmer, more focused state.

What ended it had nothing to do with child development science. In 1984, Reagan's FCC chairman Mark Fowler abolished the advertising limits that had protected children's programming from commercial pressure. Toy companies moved within months. Between 1984 and 1985, cartoons tied to toy lines increased by 300%, from a handful of shows to more than 40 animated series. In almost every case, the toy was designed first. The cartoon was built to sell it.

Researchers later put numbers to what parents were already noticing. A 2011 study in Pediatrics from the University of Virginia tested 60 four-year-olds across three groups: one watching SpongeBob, which cuts scene every 11 seconds; one watching a slow PBS show, which cuts scene every 34 seconds; and one drawing. Nine minutes later, all three took tests on attention, impulse control, short-term memory, and problem-solving. The SpongeBob group scored significantly worse across every measure.

In the 1970s, children began watching television around age 4. Research from pediatrician Dimitri Christakis found that by 2009, the average age of first screen exposure had dropped to 4 months, as the content got faster and the audience got younger. Researchers separately found that each additional hour of daily screen time at ages 1 or 3 raised the risk of attention problems at age 7 by 9%.

The longer $TSLA underperforms, the wealthier I become.

On our walk today I was running some numbers.

When I retired in December 2021, $TSLA was trading around $350 and my net worth was $2.65 million. Now $TSLA is at $406 (up just 16%) and my net worth is $4.5 million — that’s +70% after spending roughly $340k along the way.

This didn’t come from the stock ripping. It came from aggressively selling short puts during dips and trimming on strength. We’ve had at least one 40-65% drawdown every single year since 2022.

Who knows what the future holds. It would be nice to finally get some real help from the underlying. Which we eventually will. But I’ve learned how to keep growing my net worth through active management regardless.

The game has been good to me.

Akon reveals to Andrew Schulz just how INSANE his music royalties are, using his hit record “Smack That” as an example and claiming it can generate up to $200,000 per quarter 😳💰👀

He also explains how artists labeled as one-hit wonders can often live comfortably off a single successful song for the rest of their lives 🔥

🚨La identidad de este imitador de Michael Jackson fue un misterio durante años...

Pero ahora que se reveló quién era realmente, este video está explotando otra vez en redes.

Y viendo el moonwalk… es imposible no quedarse mirando. 🔥🕺

X-Fam,

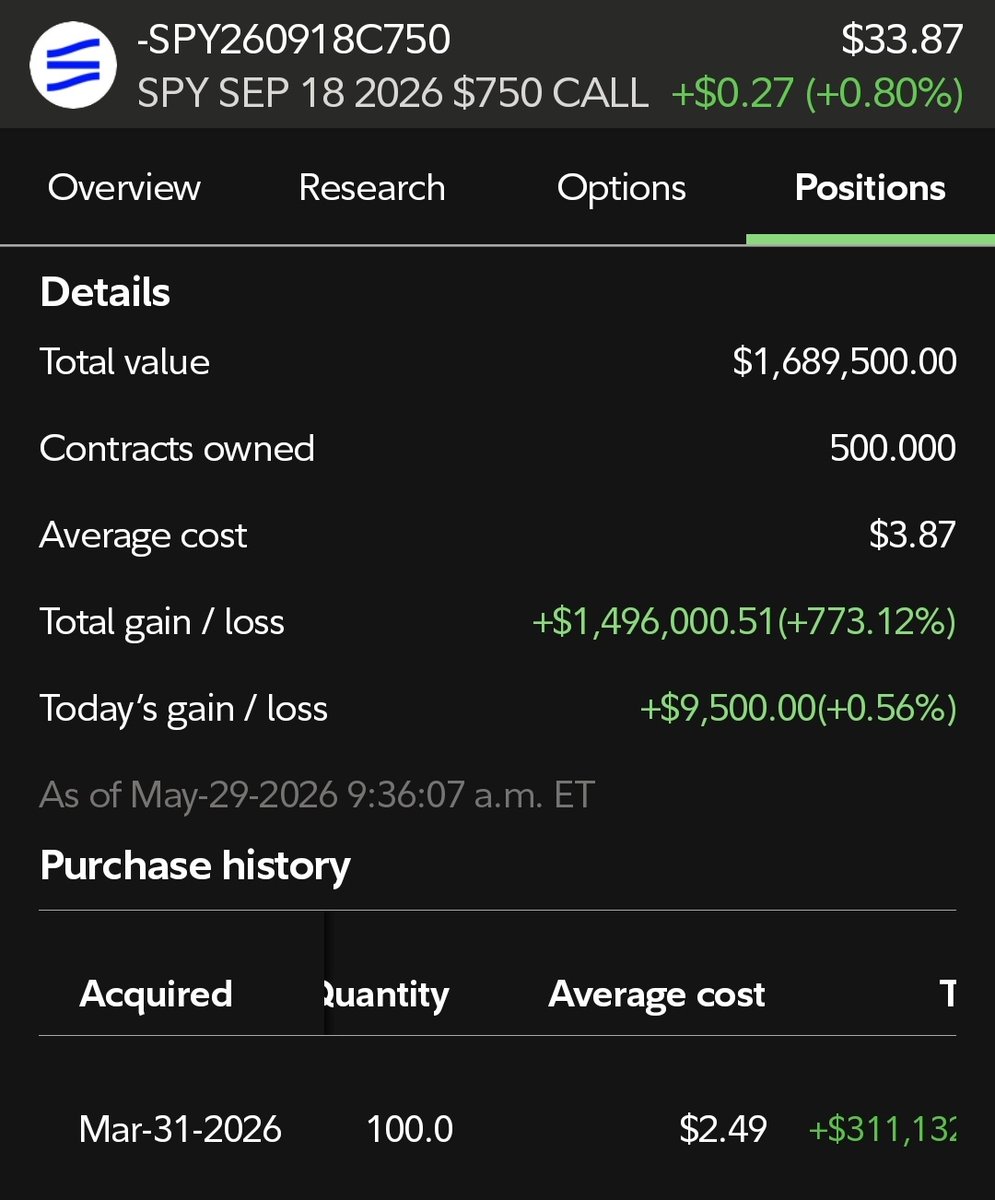

Today I closed my $SPY Sep 2026 $750 LEAP position, taking advantage of End-of-Month window dressing and selling into strength.

This trade started in one of the most uncomfortable environments imaginable. While on spring break with my kids, sitting in a Disneyland hotel room at 6:30 AM, markets were in panic mode and many were calling for significantly lower prices.

Instead of reacting Emotionally, I trusted my process.

Using my Unique Crash LEAP Entry System, I accumulated 500 contracts as fear peaked and sentiment deteriorated.

Today, after 42 trading days, I exited the position on the ask.

• 500 Contracts

• ~$193K Cost Basis

• ~$1.69M Exit Value

• +$1.496M Profit

• +773% Return

• 42 Trading Days

What made this trade special wasn't just the return—it was the power of the Delta Ramp.

At Entry, Delta was approximately 0.11.

At Exit, Delta had expanded to approximately 0.60!!

As price advanced, exposure accelerated dramatically, allowing the position to capture a disproportionate share of the move higher.

The lesson is simple:

Great opportunities are often found when conviction is hardest to maintain.

Now, it's time to reset, Reduce exposure, protect capital, and begin searching for the next high-probability setup for the summer.

Several July structures currently have my attention, and I'll be reviewing flow, positioning, and technicals throughout the weekend.

To do this, I'll download the Options Chain ⛓️ for technical review. (JULY 31ST $760, $770 are early picks, January $800 also).

FYI....

I'm not Bearish either, just using sound money management tactics to reset and search for better Delta Ramp Setups.

Most importantly, thank you to everyone who contributed thoughtful analysis, challenged assumptions, shared data, and helped sharpen the process along the way!

Markets are a team sport. 🫶

On to the next one!

@Norseman1@Banana3Stocks@StockPatternPro@blondebroker1@dannycheng2022@Bluekurtic@ISABELNET_SA@RyanDetrick@salmaogs@Mr_Derivatives@BeardoTrader@chad_ventures@Micro2Macr0@smartertrader@WayneWhaley1136@mark_ungewitter@cantonmeow

@ChizaramNelo@VolatilityVIX nope you are right. they can't take dividends back once they pay you a dividend. they can always take the growth back once the market heads downward

If I put 107k into my TFSA and it grows to $1M , I can sell the growth investment and buy $1M worth of dividend ETFs yielding 4% . That’s 40k/year tax free income. Why aren’t we doing this?