Market overreaction of the year? 🚨

$INTU fell 20% in a single day following Q3 results, driven by 17% workforce restructuring noise and low-end DIY tax headwinds.

But look beneath the hood and a different story emerges. We just added 3% to our position.

Here is why 👇

$ADSK Q1 FY27 Earnings are out, and at first glance, the numbers look stellar!

But with the stock slipping in after-hours, here is what’s really going on under the hood.

The Highlights:

• Revenue: $1.93B (Up 18% YoY).

• Profitability: Non-GAAP EPS hit $2.99.

• Cash Machine: Free Cash Flow surged 58% to $876M.

• Outlook: Full-year FY27 guidance was raised.

So why the drop? A few things the market is digesting:

• Headline vs. Normalized Growth: The 18% billings growth looks incredible, but FY27 constant currency growth, when adjusted for their new transaction model, is projected at a much cooler 8-9%. The new model is inflating the current headline numbers.

• Massive Acquisition: $ADSK announced a $3.6B all-cash deal for MaintainX. While highly strategic for their AI and operations lifecycle, large cash outlays often bring short-term integration jitters.

Overall, Autodesk is executing well, but Wall Street is likely repricing for the restructuring and acquisition risks.

https://t.co/zEiV6nTkrU is our go-to platform when we need granular information to analyze a company. Quick and easy access to KPIs.

They run a special discount of 25% so if you want to grab this, here’s our affiliate link:

https://t.co/IxDEt0dFYb

The numbers out of Big Tech this quarter are absolutely staggering.

Inside the StockOpine News:

🔥 $META: A $145B CapEx shock (despite 41% margins)

☁️ $MSFT: AI revenue surges 123% + a massive $627B backlog

🛒 $AMZN: Custom silicon hits a $20B run rate & a $17B Anthropic windfall

🧠 $GOOGL: Cloud rockets 63% as Gemini processes 16B tokens/min

Dive into it 👇

PayPal just dropped a new 8-K and it’s raising some serious red flags. 🚩

Yet another major leadership shakeup.

Two EVPs are out: Diego Scotti (Consumer Group) and Michelle Gill (Small Business). Scotti’s exit is especially notable as he was the executive driving Venmo’s growth and monetization, and he led the launch of PayPal Everywhere and PayPal Ads.

$PYPL is shifting to a new 3-unit operating model, but they are leaving critical growth engines like Venmo to interim leads.

How many executive restructurings does it take before we start questioning the stability of this turnaround story?

$POOL increased the company’s share repurchase program to $600 million.

That’s about 7.5% of its market cap. Meanwhile the company it’s trading near its 52-week lows.

You read this - what’s your next action??

$AMZN

“AWS is growing 28% (our fastest growth in 15 quarters) on a very large base, our chips business topped a $20 billion revenue run rate (growing triple digits year-over-year), Advertising grew to over $70 billion in TTM revenue, and unit growth in our Stores reached 15% (the highest since the tail end of covid lockdowns)”

Just published our earnings review of $POOL’s Q1’26 results.

Management held firm on a low-single-digit full-year revenue outlook despite the 6% Y/Y growth and Q1 beat.

We believe management is sandbagging guidance, setting a highly achievable bar for the core summer months.

After a tough three years of post-pandemic normalization and negative growth, we see clear signs of $POOL returning to growth:

- Q1 '26: Back to +6% growth. This is the first meaningful acceleration after nearly 12 quarters of declines or flatness.

- New Construction: The industry seems to have hit bottom at 58K pools built in 2025, a level similar to 2011.

- Chemicals: Chemical deflation appears to have stopped being a headwind as of Q1 '26.

The pool industry finally seems to be returning to growth after a three-year cycle.

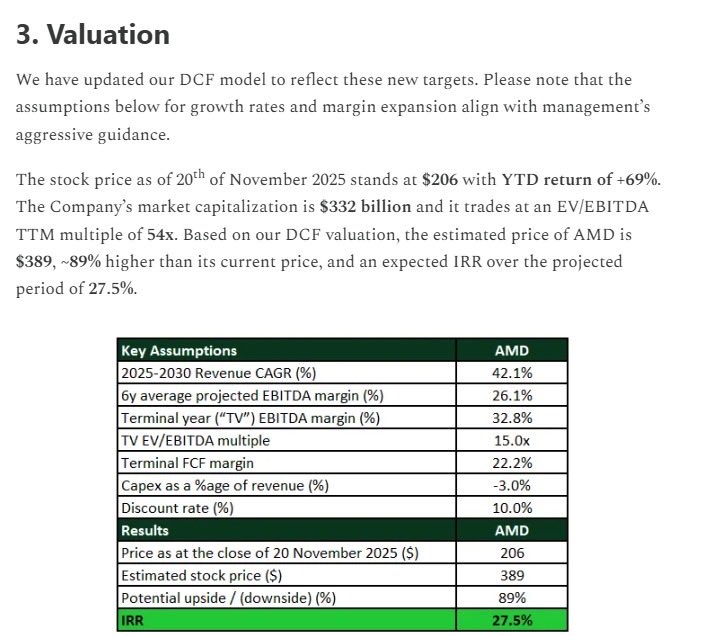

After $AMD Financial Analyst Day in November, we revised our valuation. With the stock at $206, we set a "long shot" target of $389, levels we’re now approaching.

Prophecy? Maybe. Just doing the work? Partly. To be honest, it’s often a matter of luck, but it is incredibly self-satisfying to see those distant valuation targets actually hit the tape.

If you’re into investing, this is actually worth checking out.

The valuation bot gives you really quick access to valuing a company, and there are plenty of examples so you can see how it works in practice. Plus, @EdmundSimms is doing a great job with the valuations, the performance has been strong and seems to be outperforming the S&P 500.

For what you get, the cost is pretty minimal.

If you want to try it, you’ll get 25% off your first purchase using our referral link below 👇

$TRIP

We broke all of this down (with full valuation + downside scenarios) in the deep dive.

It’s usually behind the paywall — but it’s open right now:

https://t.co/dbrxF7GEic

Most investors think $IDXX Laboratories is “just a vet diagnostics company.”

We just opened our full IDEXX deep dive (usually Premium):

Here’s the real moat 🧵