Sigh.

I keep telling retail + Swedish Hedge Funds how important $SIVE is to CPO, but people don’t listen.

Enough retail holders got shaken off, and

now JP Morgan managed to buy up a massive stake in Sivers (purely institutional).

JP Morgan went from .4% ownership last month to 5%+ ownership this month…

$SIVE is my favorite CPO / photonics stock after AAOI.

Partly because it's Swedish and you have entertainment from comedians over there.

Today a new non-technical hedge fund called Protean Funds (likely shorting), went on air.

To said $SIVE CPO applications are imaginary.

Right after $GFS just made $SIVE their reference laser.

(Just for some context to newer readers: Lot of people in Sweden can only look at past 12 month revenue, and don't understand concepts of forward growth)

Also because they don't understand that no CPO application has scaled up yet at all.

So Swedish hedge funds keep going short (with many of their hedge funds like Colosseum / Origo heavily underwater).

But... for the technical readers... from H2 2026 to 2028, it goes from near $0 to $91B TAM in 1 1/2 years. (we're entering H2 now).

Overall TAM hits $141B (which is also 10x+ or so in 1 1/2 years)... and $SIVE has scaled into pluggable market with $JBL + other unnamed pluggable players with that too.

Probably not going to end well for the local Swedish firms, shorting right before the largest inflection points ever hits for $SIVE.

Just a matter of time before volume ramps.

Here's a $SIVE fact that almost nobody is talking about. It's the structural setup behind everything happening with the Nasdaq listing.

Zero US institutional investors currently file 13F, 13D, or 13G forms showing $SIVE ownership.

I mean that literally. Per Fintel's SEC filing database, Sivers Semiconductors has zero US institutional owners on record with the SEC. Not one filed position.

[Source: https://t.co/jEIBHI0rbb]

The one major US institutional holder we know exists, Hudson Bay Capital, which participated in the May 11 raise — holds the position through structures that don't generate SEC 13F disclosure for SIVEF.

Why this matters:

Most US institutions are mandated by their charter to hold US-listed securities only. Some can hold US OTC names like SIVEF. Almost none can directly hold a Stockholm-primary listing.

This creates the structural reality of $SIVE today:

→ Trading is dominated by retail flow

→ Volatility is amplified because there's no institutional anchor

→ Short attacks have outsized impact (no large holder absorbing supply)

→ Index inclusions create disproportionate moves because the institutional layer is missing

Now connect the dots.

When $SIVE completes the Nasdaq NY dual listing, that "0 US institutional filings" becomes a much larger number.

Here's what that actually triggers:

- Every US institution with a photonics, AI infrastructure, or thematic mandate becomes a potential buyer for the first time

- Mutual funds and pension funds that benchmark against US semiconductor indices start adding $SIVE to reduce tracking error

- Inclusion in US-listed sector ETFs (semiconductors, photonics, AI infrastructure) becomes possible

Once a US-listed name has institutional holders, sell-side analysts start coverage to capture business because initiations follow ownership

Each subsequent 13F publicly shows institutions adding $SIVE, which itself becomes a buy signal for other institutions

You're watching a company that hasn't even been introduced to the US institutional buyer pool yet.

The biggest catalyst for $SIVE isn't the GFS deal. Isn't Ayar Labs. Isn't the EU Tech Sovereignty Package.

It's the moment when the answer to "how many US institutions own $SIVE" changes from "zero" to anything else.

$SIVE

Three different ETF issuers have now filed 2X LONG $SIVE products with the SEC. Let me explain why this matters.

The filings:

→ REX Shares T-REX 2X Long SIVE Daily Target ETF (filed May 26)

→ Defiance Daily Target 2X Long SIVEF ETF (filed April 10)

→ Themes ETF Trust Leverage Shares 2X Long Sivers Semiconductors Daily ETF (filed May 26)

Here's what most people don't understand about leveraged ETF launches:

ETF issuers are essentially demand-prediction businesses.

They don't file 2X products for stocks no one will trade. They file them for stocks with explosive expected retail interest — because that's where the trading volume and management fees come from.

When THREE different issuers independently file the SAME 2X LONG product on a Swedish-listed company that doesn't even have a US primary listing yet, you're watching structural demand forecasting in real time.

The pattern recognition is clear. Recent Defiance 2X Long launches include: $IREN, $RKLB, $PLTR, $MSTR, $RGTI, $ASTS, $OSCR, $MP, $LMND.

Every one of those names is a retail momentum monster. $SIVE just got added to that company — except it's earlier in the cycle, before the US listing has even happened.

Two additional details worth noting:

All three products are 2X LONG. There are no matching 2X SHORT $SIVE products being filed. The directional asymmetry tells you exactly which way issuers expect retail demand to flow.

The prospectus language explicitly references "American depositary receipts (ADRs) may be substituted as the Underlying Security." Translation: these products are being structured in anticipation of the Nasdaq NY dual listing and the ADR creation that will accompany it.

What this actually means:

→ Three of the most active leveraged ETF issuers in the US market have positioned ahead of the $SIVE listing

→ They've allocated legal, regulatory, and operational resources for a stock most US retail hasn't even discovered yet

→ When the Nasdaq NY listing hits, these products go live and dramatically amplify the retail flow

→ Every dollar into a 2X LONG ETF requires the issuer to buy 2x that amount in $SIVE shares to maintain exposure

This isn't a passive index inclusion. This is the leveraged demand layer being built BEFORE the stock has even arrived at its primary US venue.

You don't get three 2X LONG ETF filings on a $2-3B Swedish-listed company by accident.

You get them because the demand they're forecasting is real.

$SIVE

Basically this entire $SIVE debacle has been this:

1. Serenity reads between the lines to make educated guess about what’s likely to happen to $SIVE in terms of new partnerships

2. Someone says “nuh uh, it’s not confirmed! This is overpriced! You’re just guessing, it’s not true”

3. Serenity ends up right more often than not. Price already rerating as it’s confirmed.

4. Repeat.

Guys, do I need to remind ya’ll, this is a speculative market, you make a guess and profit from the re-rating. If you don’t want massive profits, feel free to buy after everything is priced in and confirmed.

48 hours of $SIVE catalysts.

Yesterday: $SIVE laser arrays embedded in GlobalFoundries' silicon photonics reference designs.

Today: Ayar Labs — the leading CPO solution provider for AI scale-up — joined NVIDIA's NVLink Fusion ecosystem.

Why this matters for $SIVE:

Ayar Labs' co-packaged optics solution requires high-precision InP DFB lasers as the optical light source. $SIVE is a publicly named partner of Ayar Labs for exactly that role — CPO External Light Sources.

Now stack the supply chain:

$SIVE → Ayar Labs → NVIDIA NVLink Fusion → next-gen AI scale-up architecture

$SIVE → GlobalFoundries silicon photonics platform → entire foundry customer base

Two distinct paths into the heart of AI infrastructure. Both with $SIVE lasers in the stack.

Context on Ayar Labs in case you missed it:

→ $3.75B valuation after March 2026's $500M Series E

→ Strategic investors include NVIDIA, AMD, MediaTek, Alchip

→ TeraPHY optical engine processes 8 terabits/second per unit

→ Described as "the industry's first proven CPO solution for AI scale-up"

This is the company NVIDIA just embedded in NVLink Fusion.

And it's a publicly named $SIVE partner.

Three names did the structural validating in the last 48 hours: NVIDIA. GlobalFoundries. Ayar Labs.

These companies don't pick small suppliers.

They pick standards.

And the standard increasingly has $SIVE inside it.

$SIVE $NVDA $GFS

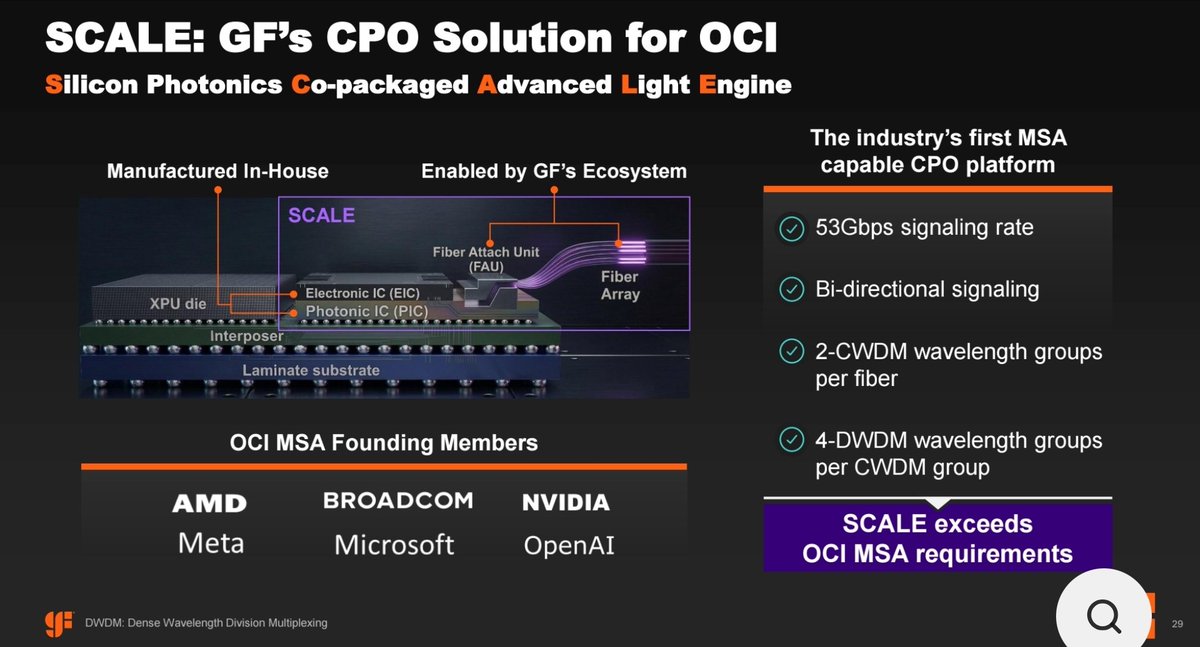

Many people read the Sivers $SIVE/GlobalFoundries $GFS PR and see "AI optics."

I see something more: GF's SCALE platform is explicitly positioned as a CPO solution for OCI (Optical Scale-Up Initiative), whose founding members are: NVIDIA, AMD, Broadcom, Meta, Microsoft, OpenAI

Hennce, Sivers $SIVE just became the first publicly named laser partner integrated into SCALE reference designs. GF CPO solution for OCI. SCALE is the Industry First MSA capable CPO platform.

OCI drives the transition from 800G EMLs to 1.6T/3.2T SiPh + CW laser architectures, this partnership hence is highly strategically important.

Not just a partnership announcement, it is an ecosystem announcement.

"Sivers’ laser arrays will also be available in GF’s Silicon Photonics Co-packaged Advanced Light Engine (SCALE™) platform for next-generation optical sub-assemblies and light engine architectures":

https://t.co/MKT1Lu4evA

"Optical Scale-up Consortium Established to Create an Open Specification for AI Infrastructure Led by Founding Members AMD, Broadcom, Meta, Microsoft, NVIDIA and OpenAI"

https://t.co/9KeYxFJ4b4

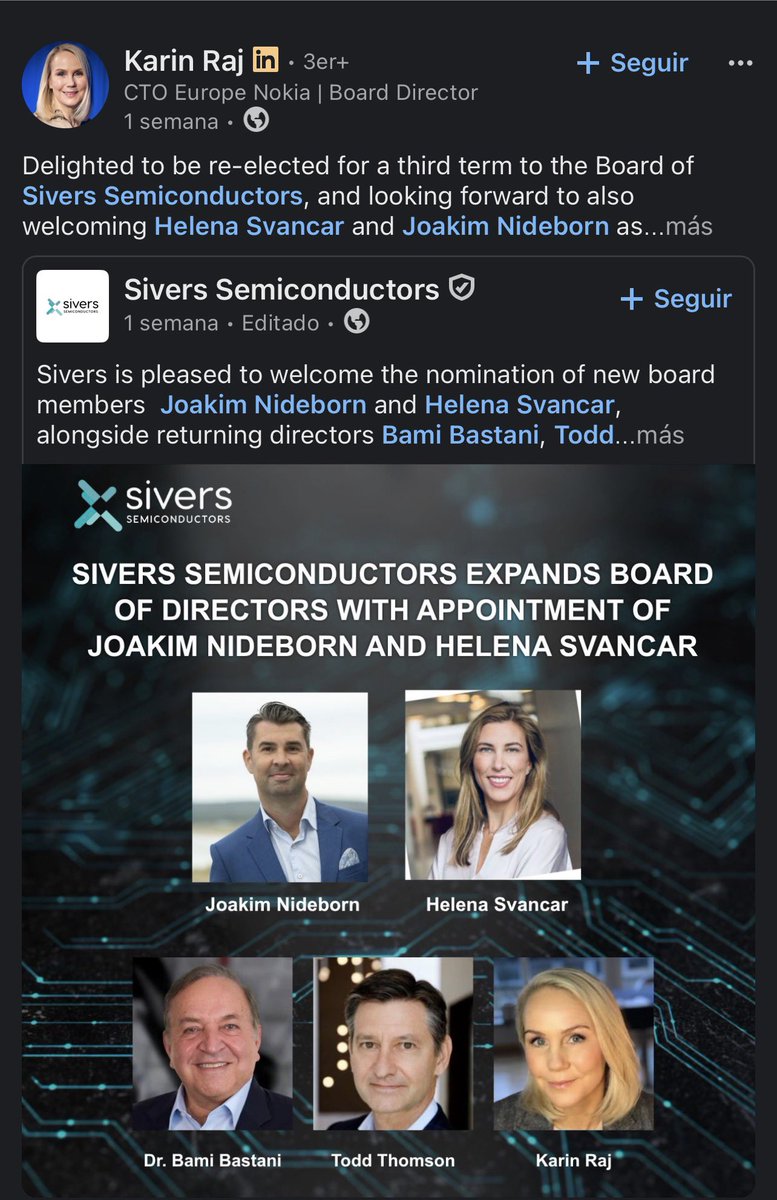

Check your data: Lock-up undertakings:

"In addition, shareholding board members Bami Bastani, Tomas Duffy, Karin Raj and Todd Thomson as well as the Company’s CEO Vickram Vathulya, and CFO Heine Thorsgaard have undertaken not to sell any shares in the Company for a period of 90 days after completion of the Directed Share Issue, subject to customary exceptions."

Note the "completion". That was after the EGM. This means approximately mid August 2026.

Well well well. What do we have here.

Karin Raj, CTO of Nokia Europe, was just re-elected to the Board of Directors of $SIVE Sivers Semiconductors for a third term. Third term. She keeps coming back.

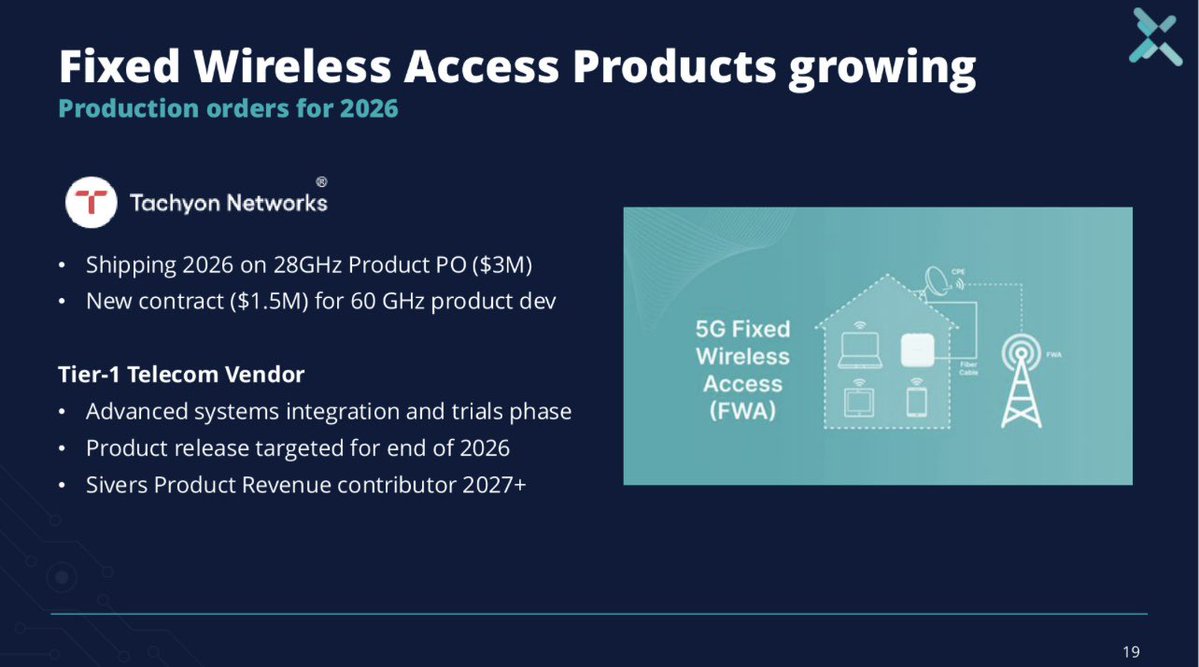

At the same time, look at what Sivers just disclosed in their latest investor presentation.

Fixed Wireless Access products are growing, with two live engagements:

Tachyon Networks -- $3M production order for their 28GHz product shipping in 2026, plus a brand new $1.5M contract for 60GHz product development. Two stacking contracts, two frequency bands, same partner.

A Tier-1 Telecom Vendor

- who’s identity might be impossible to infer - is currently in advanced systems integration and trials phase. Product release targeted for end of 2026. Sivers revenue contribution starting 2027.

A Tier-1 Telecom Vendor.

Now I am not saying anything. I am just saying that the CTO of Nokia Europe sits on the board of a company that just disclosed a Tier-1 Telecom Vendor engagement expanding from 28GHz to 60GHz FWA.

Nokia is the world's largest telecom equipment company. Nokia has a massive 5G Fixed Wireless Access product line. Nokia's European CTO has now chosen to be on this board three times.

You connect the dots.

$SIVE is not just a photonics and InP laser story. The Wireless segment is building its own multi-year revenue line quietly in the background while everyone watches the CPO thesis.

Two segments. Two catalysts. One stock.

Bullish $SIVE.

The massive disconnect between local retail sentiment and international institutional reality regarding Sivers Semiconductors ($SIVE) has officially reached peak absurdity.

As $SIVE undergoes a historic macro re-rating, local bears and casual observers on social media are pushing two desperate narratives:

1. That the management team is running some sort of "scam."

2. That Sivers massive $800M pipeline is just fluffy "sales talk over coffee and business cards."

Let’s look at the actual data, the structural mechanics of the semiconductor industry, and the regulatory realities to see why the smart money is ignoring the noise and locking up the float.

🔮 Part 1: The Anatomy of an $800 Million Qualified Pipeline

During the Q1 2026 presentation, CEO Vickram Vathulya dropped a monumental update on Sivers' qualified opportunity pipeline. The numbers are staggering:

End of 2024: $276 Million USD

End of 2025: $453 Million USD (+64% YoY)

May 2026 (Last 5 months): Just shy of $800 Million USD! (+77% growth in 150 days)

To suggest this $800 Million pipeline is based on "coffee and business cards" shows a fundamental lack of understanding of how deep-tech procurement works.

First, this pipeline spans the 2026–2030 commercial window, tracking the global ramp of AI optical interconnects and next-gen SATCOM networks.

Second, an opportunity does not just "appear" in this funnel. Sivers enforces a strict, multi-stage qualification matrix:

Technical Alignment: The hardware specs must precisely match the client’s architecture.

Commercial Visibility: The customer must provide an active commercial timeline and explicit multi-year volume forecasts.

Physical Validation: The client must be actively evaluating and stress-testing Sivers’ physical silicon in their own labs.

🔬 Part 2: The Silicon Valley Pedigree vs. The "Scam" Narrative

The theory that Sivers' leadership is running a "pump-and-dump" or a "con" falls apart the moment you look at the executive roster and the board.

Sivers' leadership isn't made up of penny-stock promoters. We are looking at an elite group of semiconductor veterans with decades of high-level execution at the absolute titans of the tech world:

- GlobalFoundries

- Lumentum

- Nokia

- NXP Semiconductors

- Maxim Integrated

Are we seriously to believe that world-class executives and PhDs, who spent 25+ years building immaculate reputations in Silicon Valley and global telecom, decided to collectively throw away their careers to run a fake equity story in Stockholm? The premise is ridiculous.

🛡️ Part 3: Sovereign Vetting (The Ultimate Due Diligence)

If you still think Sivers is a mirage, you have to believe that a small design house from Sweden somehow managed to outsmart the most rigorous forensic auditing teams on Earth:

The US Department of Defense: Sivers cleared the extreme technical and security vetting required to secure millions in funding from the NEMC Hub via the US CHIPS Act for advanced electronic warfare.

The European Union: Sivers is heavily integrated into the newly released European Chips Act 2.0 framework as a vital asset for regional digital sovereignty.

The Pentagon and the European Commission do not grant dual-use defense status and millions in taxpayer incentives based on a flashy PowerPoint. They run exhaustive, line-by-line, chip-by-chip physical audits. Sivers passed them all.

💡 The Bottom Line

The Technology has been vetted and funded by sovereign entities (US & EU Chips Acts).

The Scalability is locked in with Tier-1 manufacturing giants like WIN Semiconductors, GlobalFoundries and Jabil (co-developing the 1.6T transceiver).

The Pipeline is rapidly moving into late-stage "design-in" to the tune of almost $ 800M.

The Shareholder Registry is being aggressively overtaken by international investors.

Local retail sentiment is trading on backward-looking historical data and coping with the volatility.

As always do your own due diligence.

@ram_blings Not 1:1 but $LITE gross margins are ~45-48%.

Having 60% gross margins for $SIVE is extreme pricing power.

And that’s on top of exponentially growing revenue pipelines… at the very beginning of the CPO supercycle.

$SIVE is the most compelling CPO/photonics exposure to me.

Addressing the disinformation: I haven’t sold and don’t plan to sell a single share.

I do think this ends up the next $80B+ $LITE one day from ~$2.1B.

And I personally have plans to acquire more ownership + support their M&A prospects.

I believe earnings transcripts will be strongly positive.

As in the part few months we’ve discovered:

> AlChip/Amazon private placements, which is positive for Ayar -> $SIVE implying Trainium 4 design in

> Wiwynn + Ayar CPO scale up

> $JBL 1.6T optical transceiver ramp with Sivers incoming faster than markets expected (with relatively dramatic moat + demand as much as they can produce)

> O-Net scaling up ELS efforts with $SIVE

> $YSS acquisition of $SIVE allspace lead partner, designing Sivers into Space defense primes

> New CHIPS ACT funding for $SIVE

> $POET H2 volume ramp and their new $50m -> $500m order (with $SIVE as light source)

> information discovery around $AAPL using $SIVE lasers for next gen consumer devices

> information discovery around links to Lightelligence (went public $10B+ MC) + Lightmatter as likely customers.

> Celestial volume ramp with $MRVL indicators.

> new customers working on TFLN with $SIVE like Lightium

> $AMD going with $GFS for CPO, and GFS listing sivers as one of two laser suppliers

> Ayar removing $MTSI / $LITE from their website and signaling $SIVE as primary source/sole source

> Ayar raising $500m for volume ramp (intel, Mediatek, Nvidia, amd etc)

> pluggable TAM expansion signaled from 2025 annual report

> Nasdaq listing expected soon

> MSCI small cap index / Nasdaq omx inclusion, making Blackrock, Vanguard and others passive buyers

> M&A signaled from 2025 annual report + 2 new board members that have experience in that area

> $NOK as likely customer from 2025 annual report.

> $LITE getting cw bottlenecked from EML contracts, $SIVE signaling capacity agreements in place with Win, making the a likely bottleneck owner + chokepoint in CPO sector.

All of this market research was done before earnings.

Any results is just confirmation of supply chain mapping done.

I don’t think anyone cares about former quarter revenue since $SIVE is an exceptionally compelling 2027 long, especially H2 onward.

Only thing I’m looking at are:

> TAM expansion of the overall photonics supercycle (eg. optical engine, ELS, pluggables) either from M&A or developments

> volume ramp expectations from existing companies

> Nasdaq listing timelines for more liquidity to support their M&A efforts

> any new customers signaled for CPO/Pluggables