Albrecht Law is seeking a litigation attorney licensed in Delaware to join our Litigation Division for a remote position.

Our Litigation practice, headed by @RitterLawyer, has been busy with high-stakes commercial cases and is now hiring a Delaware-licensed lawer.

If you are a buyer in an asset deal and the seller negotiated a gross up - please don’t take a seller’s gross up calc at face value. Call me to review it for you. I just reviewed a seller gross up calc and it was wrong - I saved my client $57k of cash at closing.

@elialbrecht@Albrecht_Law

Albrecht Law Client Alert. Tax Implications from One Big Beautiful Bill Act (H.R. 1)

The One Big Beautiful Bill Act (H.R. 1) was passed by the House and Senate and is set to be signed into law by the President. Here are some of the relevant tax implications for businesses from @JoshuaASiegel, Chair of Transactional Tax at @Albrecht_Law

Albrecht Law Client Alert. Tax Implications from One Big Beautiful Bill Act (H.R. 1) passed by the House and Senate and is set to be signed into law by the President. Here are some of the relevant tax implications for businesses from @JoshuaASiegel, Chair of Transactional Tax.

New tax cuts just passed!

100% bonus depreciation is back and is permanent!

Immediate expensing for R&D activity is back!

And much more!

Please reach out to discuss in more detail

@Albrecht_Law

M&A Monday - How Does an Independent Sponsor Make Money? (Part III of III)

Part III - Carried Interest

This M&A Monday post is Part III and will cover the third way an Independent Sponsor makes money, Carried Interest. This is the IS’ most significant upside and the most complex of the three buckets.

In Part I, we covered the first way an Independent Sponsor gets paid, the Transaction Fee. In Part II, we covered the Management Fee, and in Part III, we cover the most lucrative (and complex) part of the economics, the Carried Interest. This part also has the most variation. This post will be a high-level summary.

Traditionally, in a PE-style/Indy Sponsor acquisition, 100% of the equity of the business is allocated to those who put in real money. For example, with a $30M Purchase Price + transaction costs ($20M Senior Debt / $10M), 100% of the acquisition is owned by the $10M. $1M investment gets 10%.

In that case, where is the IS’ interest, ownership, and upside?

Of course, they get a management fee (see Part I), and they can roll in their Transaction Fee (see Part II), but no ownership.

Enter, Carried Interest.

Carried Interest is an economic share of the profits that acts like equity ownership. The Sponsor slots into the waterfall and has the right to economic profit after the Investors (called Preferred Investors because they have preference over others).

In the simplest form, after Investors receive their investment back plus a certain return on their investment (MOIC, IRR, or annual interest), then, the IS starts to receive 15%/20% of all profits.

Straight Waterfall vs. Variable Waterfall

Traditionally, and most of the time, Indy Sponsors have a variable waterfall, whereby they get escalating percentages of carry the more investors make - in other words, every return Hurdle, the IS gets higher percentage carry. (i.e., 15% until investors get 1.5x MOIC, 20% for a 2x MOIC, 25% for 2.5x MOIC – the numbers are all negotiable and vary). Usually, there is a catch-up included for the Sponsor.

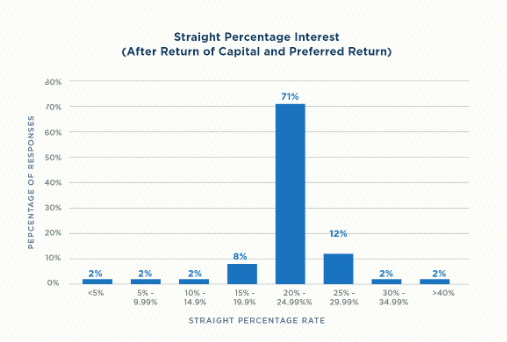

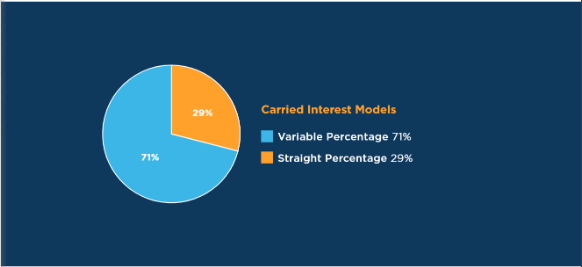

The 2024 IS Survey says 71% are variable and 29% are straight. In my experience, this is moderately overstated.

What is Market for a variable waterfall?

More traditional IS will start at around 10%/15% for the first Hurdle of about 1.5x MOIC or 10% IRR. Second hurdle gets the IS 20% carry if the Investor gets 2x MOIC or 15% IRR. For those with a third hurdle, it is often 25% to the IS for achieving returns of 2.5x MOIC or 20% IRR plus. A catch-up for the IS is common.

Straight Waterfall

In a minority of Indy Sponsor deals, there is a straight waterfall. For example, Investors get their money back plus 10% annual interest, and thereafter, all profit is split 80%/20% (often, with a catch-up).

While the straight waterfall is simpler, the variable waterfall is supposed to incentivize the IS to shoot for a higher exit and reward the IS in a “home run” scenario.

What is market for straight waterfall?

In traditional IS deals, the straight waterfall tends to be around 20% - 30% carry to the IS after a return for investors of their investment plus a preferred return percentage. The 2024 Indy Sponsor Survey reflected this.

However, increasingly, I am seeing higher splits. I have done 3 deals this past year where, once investors received their money back plus their percentage return, all profits were split 50/50 and 60/40 (the IS received 60). This is more common on deals where the leverage is higher, the seller holds a large promissory note and/or rollover, and the equity funds come from outside the traditional IS community. Additionally, the first return hurdle for the investor tends to be higher (i.e., 15%+ annual return)

Finally, there is a structure where lenders are putting in all of the debt and if needed, the equity (uni-tranche). While the lender usually requests warrants and the IS usually has to roll their fee into equity (see Part II), this results in the IS owning practically all of the acquisition without putting almost any of their own money in the deal. I have closed several of these deals and I will break down one of these deals in a future post.

Final note - be very careful how you structure this from a tax perspective. Your carried interest should be treated as capital gains, but we often see this messed up.

The carried interest part of the IS’ economics is the most important and the most complex. There are tons of other factors to consider, including, and importantly, tax treatment.

In the next post, I will do a deeper dive into how to finance an Indy Sponsor deal and then I will break down the structure of a recently closed Indy Sponsor deal.

Until @RitterLawyer launched the Litigation Department at @Albrecht_Law, I never realized that getting a Litigator involved early can save a TON of money. This is especially true post-M&A transaction.

M&A Monday - Independent Sponsor Economics – How does an Independent Sponsor make money? (Part II of III)

Part II - The Management Fee

In Part I, we covered the first way an Independent Sponsor gets paid, the Transaction Fee. In Part II, we cover (ii) the Management Fee, and (iii) Carry.

Once an acquisition by the Independent Sponsor is closed, the Management Fee begins to be paid to the Sponsor. This is a fee paid by the newly acquired operating company (OpCo) to an entity affiliated with the IS’ principals. This fee is in consideration of the IS overseeing the portfolio company, but does not include professional services provided (i.e., CFO services).

The Management Fee tends to be 5.5% of trailing 12-month EBITDA, with a floor depending on deal size, and paid quarterly (I prefer monthly). This is what the IS uses to keep their lights on.

This is done pursuant to a separate Management Agreement or Advisory Agreement.

Lenders and Investors negotiate the following points.

A. The percentage of EBITDA paid as the Management Fee. 5%-6% of EBITDA has become standard. While lenders/investors may try to negotiate this, few end up outside of 5%-6%. The fee is ordinarily paid quarterly, but I encourage clients to have it paid monthly (this is not usually controversial). The Management Fee will be frozen and (usually) accrued if subordinated by the lender (see below).

B. Trailing EBIDTA. Often, I try to get the Management Fee paid on pro-forma budgeted EBITDA. To be honest, I rarely win this point for obvious reasons.

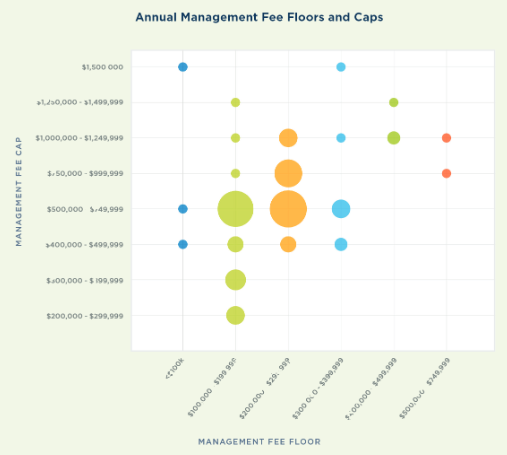

C. Floors and Ceilings. The IS will want a Management Fee floor (even if the business declines the IS will receive a certain amount of management fee) and Lender/Investor may argue against this. On a $2m-$4m business, the floor is usually $250k/$300k. The Lender/Investors may want a ceiling. For example, even if 5% of EBITDA exceeds $750k, the Management Fee is capped at $750k. I argue against a cap because it misaligns incentives for IS to grow the business. If the IS can grow the business so much to hit the ceiling, that should make everyone happy. I often see floors, but almost never agree to caps. I win this point on most deals.

D. Management Fee Subordination. The Lender will have a Management Fee Subordination Agreement to freeze the Management Fee from being paid to the IS in the event the business is not doing well and trips their covenants. The trigger and whether the fees accrue are heavily negotiated. I argue for the Management Fee to be accrued and paid out when the business is back out of default. The Lender will want the fee to be lost if frozen. Lots of options and compromises exist here. This agreement must be closely scrutinized and negotiated.

A few additional points.

1. The mechanics of the Management Fee are included in a Management Fee Agreement or Advisory Agreement. This agreement is an agreement between the OpCo and the Sponsor and includes a lot more provisions, including term, indemnification, and dispute resolution.

2. The IS should use the same ManagementCo entity for all of their platform acquisitions (i.e., the same entity receives management fees from multiple platforms) because eventually, a stake in this entity can be sold to a private equity group (or taken public). This is called a GP Stakes Acquisition and while more common in real estate and PE, can be done with an IS seeking liquidity or an exit.

3. On rare occasions, the investors/lenders are also paid a management fee. While this is rare, this is a tool that can be used if particularly in need of capital.

4. Finally, the Management Fee usually cannot be changed without lender and investor's consent. This is because the loan documents prohibit it, and the operating agreement/shareholder agreement usually prohibits the IS from engaging in affiliated agreements without the majority of investors’ consent (sometimes a different threshold). The lender’s negotiations should take place in the Management Fee Subordination Agreement because the Management Fee Agreement cannot be changed even after the lender is paid off. Lenders like to negotiate both documents, it should be resisted.

Part III will cover the third way an Independent Sponsor makes money, Carried Interest. This is the IS’ biggest upside and the most complex of the three buckets.

*A note on the data. I am using data from MW Independent Sponsor survey. For reasons I can discuss, this data is heavily skewed to be lender and investor-friendly. I tend to get much better terms for my clients than the data in this survey.

Business Marriage Prenuptials: Practicable Optimism

Starting a new partnership. Investing in a new deal. Inking a new joint venture.

Ever wondered how many business relationships end in divorce?

A “fun” fact for you: It’s higher than first-time marriages.

According to many sources, between 50% and 70%+ end badly. Only 40% to 50% of first-time marriages end in divorce.

Among even those that stay together, many live under dysfunction — materially affecting growth, profit, and headspace. They eventually stagnate or suffer a silent death. All because of poor legal structures or counsel when a dispute arises.

Nothing ventured; nothing gained. I eat, sleep, and breathe it too. Get it.

But think *very* carefully through what may go wrong, including how the business and business relationships may (and likely will) change over time.

Not just the downside scenario. That’s obviously critical. Think through how your business relationship(s) and governing document(s) may crack when your venture exceeds all expectations. I’ve seen character chameleon when millions of dollars are suddenly in play.

And be focused — very focused — on how the governing state law and your operating agreement (or governing documents) account for various outcomes. Including potential litigation.

“I’m an optimist, but I’m an optimist who carries a raincoat,” Harold Wilson. So I can think of at least a dozen critical clauses I’d present and consider papering in your business marriage.

I’ve drafted these clauses. I’ve tested many in litigation. Not plain vanilla business disputes. The legal equivalent of business Vietnams (posts for another day).

I recently spoke to a litigator (former big law equity partner) who’s view overlapped with mine: If the litigator or M&A attorney has never seen or been through a business war, they have no business drafting or advising you — by themselves — on your governing documents.

Because “it ain’t what you don't know that gets you into trouble. It’s what you know for sure that just ain’t so." Mark Twain (and The Big Short, Paramount Pictures 2015).

An Example: The (Aptly Named) Shotgun Clause

An example of a clause your deal attorney probably didn’t raise for you to consider: A shotgun clause. Something I hope you don’t need.

I usually present a shotgun clause (or something like it) as an option for clients, especially for real estate deals or joint ventures. These clauses can be drafted in various forms.

An example: A provision permitting one partner to buy out the other for a set price. Sometimes a 2x multiple of a third-party expert’s valuation of the business or deal. This type of clause, and others like it, create an escape valve for the business when faced with problematic partners or non-overlapping visions for the future.

Prevention Is the Best Cure

If you don’t consider or incorporate these dozen or so critical clauses to protect against business and relationship volatility over time, you are, statistically speaking, likely to regret and pay (more) for it later.

Then you’ll have to hire someone like me to clean up a mess. A lot like a surgeon, I hope you never need me. If you do, I’m highly skilled at, among other things, un-morass-ing a morass. And turning an ugly mess into a net NPV positive situation.

Chaos and crises can often beget opportunity. But, it’s still risky to play for a huge win at the edge of oblivion.

So if you need me, I hope we’ve already spoken. That either I, or one my partners, already helped box in whatever issue is now in play.

If you haven’t, you should consider reaching out to me (or someone else great) as soon as practicable.

Particularly when you see any extreme outcome on the horizon, whether storms or treasure; whether litigation or deal structuring.

Because I can tell you — as a lawyer, self-reflective person, and former private equity founder and CEO — an ounce of prevention is worth a pound of cure.

I totally disagree with the idea that Lenders/Investors asking for the transaction fees of Independent Sponsors to be rolled are hypocritical and rude.

One of the basic problems with the IS model is the lack of alignment. If a due diligence item comes up at the last minute, there is huge incentive to over look the issue and just close the deal. If the Company starts to under perform, there is very little incentive to work hard to recover the situation.

Rolling the transaction fee into the deal is a basic way to achieve more alignment. That is why it happens in over 50% of deals. I don't think all of those people are hypocritical and rude.

And FWIW, while you are negotiating for the IS not to role their fee in, you are demanding that the seller role into the deal for alignment.

And paying the bills is generally what the management fee is for....

Now I am sure many investors will listen to the situation and try to make a structure work. But alignment is important. My investors make me and my partners invest in our own funds for just this reason!

@Albrecht_Law is excited to welcome our first, 1L Summer Associate, Aidan Powers.

Aidan Powers is a rising 2L at Georgetown Law with a background in business and real estate. He earned dual degrees in Operations Management & Business Analytics and Information Systems at the Robert H. Smith School of Business at the University of Maryland, along with a minor in Real Estate Development.

As a Summer Associate, Aidan will shadow the M&A, Tax, and Litigation teams and get a behind-the-scenes view of what goes into an acquisition or business litigation matter.

Welcome Aidan to Albrecht Law.

Independent Sponsor Economics – How Does An Independent Sponsor Make Money? (Part I of III)

An Independent Sponsor (i.e., fundless sponsor) is a private equity buyer without a permanent fund – meaning they raise debt and equity for each investment.

These are complex transactions that involve significant expertise from an M&A lawyer to navigate (see (https://t.co/wWb5BkDLRv), for a breakdown of the structuring of this type of deal). Today’s post focuses on how an IS’ makes money, what the market is, what is negotiable, and where I see these terms landing on my deals.

One note, I will use data from MW Independent Sponsor Survey (2023) because it is the only data, however, I find that the sponsors I represent are getting much better terms than this survey. I have my theory as to why, but across the board, MW’s data is not sponsor-friendly.

Typically, an IS has three streams of economics, (i) Transaction Fees, (ii) Management Fees, and (iii) Carry.

(i) Transaction Fees. This is a fee resulting from the IS acquiring the platform target, each add-on acquisition, and refinancings/new capitalizations. (This is also called, Acquisition Fee or Diligence Fee.)

The market for Transaction Fees is around 2.5% for the initial transaction and 2.5%-3% for add-ons and financings.

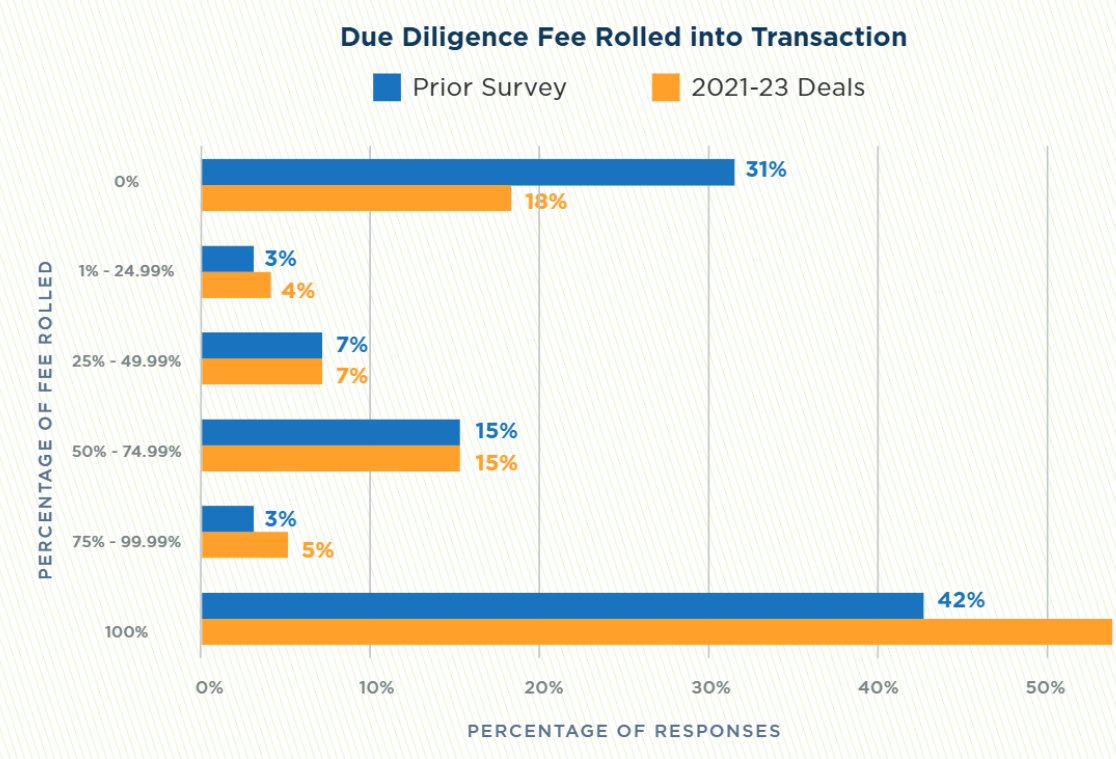

Often, an IS will be compelled to “roll” in their Transaction Fee for the initial platform acquisition. This means they do not take the transaction fee in cash at closing, rather they roll it in as the IS’ contribution to the deal. This is in exchange for preferred equity, profits interests, or on rare occasions, the Sponsor’s carry (i.e., nothing).

When IS is forced to roll the transaction fee I push hard for this to come in as preferred equity alongside other equity investors. One step down, the Transaction Fee is exchanged for profits interests, which sits below investors in the waterfall. Finally, and rarely, it is rolled into the deal in exchange for the Sponsor’s Carried Interest (see Part III).

Sometimes, part of the transaction fee is rolled and some is taken in cash. For add-ons, it is almost always taken in cash. MW survey says half of deals roll 100% of the Transaction Fee – this is not true in my deals. Only 25% of deals are forced to roll 100% of the Transaction Fee into equity, but of course, this is because I am fighting for my clients.

These points are heavily negotiated by lenders and professional investors. They want the acquisition fee to be lower, rolled, and rolled into nothing or profits interests.

I vigorously negotiate this with lenders and investors. I have been on calls with lenders and investors where I describe the 13 months the IS’ was working on this deal. These are people who risked everything to leave their jobs, max out credit cards, destroy relationships, are tortured by dead deals, and when they finally get to closing, they need the acquisition fee to pay off debts, and put money in the bank to prepare for the next bruising battle. Frankly, no one deserves the Transaction Fee more than them.

Comes along the lender two months before closing (who by the way has no problem taking their own fees at closing and every turn) and says, oh, don’t be greedy, roll in your fee - you should have skin in the game. The IS is practically bleeding out from one of the hardest acquisition structures in the world and the lender says, Where is your skin in the game?

Nonsense.

Sponsors should take a fee and feed their families. Lenders/Investors asking for fees to be rolled are hypocritical and rude. The IS is sufficiently motivated to grow the business to get the management fee and upside of the Carried Interest. I am happy to share who the lenders are who are totally fine with Transaction Fees and those who try to squeeze sponsors just because they can.

In Part II, I will do a deep dive into Management Fees and in Part III, Carried Interest.

Congratulations to our client on closing a Consumer Packaged Good acquisition. For this deal, we structured a convertible seller note, which will give the seller a stake in the buyer and drive them to continue to support the business.

In today's deal market, buyers and sellers alike are faced with a critical question:

Who is the best M&A lawyer to represent me in my transaction?

With many lawyers flocking to the practice, the decision has become even more difficult for buyers and sellers. So Albrecht Law sat down to draft what really sets us apart from the competition — then we realized, Chambers already did it for us.

https://t.co/ksZo4XEglU

@Albrecht_Law@elialbrecht@RitterLawyer

It's awesome to serve cool people like @elialbrecht and @KurtisHanni through @Meow. We're grateful for these words!

Meow is a financial technology company, not a bank. This statement only applies to Meow Technologies and not advisory services.

I remember my first call with this Independent Sponsor - he had an unconventional background for a Sponsor, but I saw right away he had two critical skills, (1) an uncanny ability to connect with people and gain trust through being genuine and honest, and (2) the ability to address challenges with creative solutions.

I remember I told him, don't worry, I'll walk you through everything else.

Since then, we have grown together. We gathered an incredible team around him - other people who are also talented in unique ways.

Yesterday, we closed another platform acquisition for this Indy Sponsor team.

Watching and participating in the group's success has been deeply gratifying and rewarding. I am very grateful to our incredible team, @JoshuaASiegel, Anthony Desiderio (incredible M&A lawyer working alongside me on every deal), and Marina Pittano Jones (M&A paralegal, who is an essential part of our team) - each dedicated themselves to helping this client succeed.

We did not need @RitterLawyer for Litigation, but we know he is ready and waiting if we need him.

M&A Monday – Structure and Financing an Independent Sponsor Deal

This M&A Monday, we are discussing the structure and financing of an Independent Sponsor deal (called, Fundless Sponsor, or my favorite, Indy Sponsor). Indy Sponsors usually take down deals between $2m-$10m EBITDA, with some outliers. The IS can be extremely flexible, creative, and is often favored by founder-sellers. I lovingly refer to Indy Sponsors as Cashless Sponsors – they have everything except money. As such, we have developed a special legal engagement for Indy Sponsors.

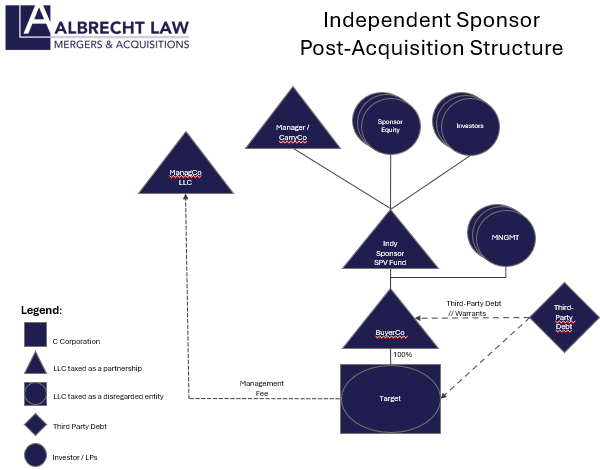

Structure -

Each deal is structured with its own mini-fund. In its simplest form, the Indy Sponsor forms an SPV, that SPV takes in funds from outside investors and buys the target through a BuyerCo (see chart). (If seeking QSBS, this is different.)

Financing –

Any Indy Sponsor deal finances an acquisition through, (i) debt, (ii) contingent purchase price tools, and (iii) equity from investors or lender.

Because most deals are over $2m EBITDA, the purchase price is often 5x-8x EBITDA.

(i) Debt. A combination of senior debt (50%-60% of PP), sometimes Mezz debt (10%-20%), and Seller financing (10%-20%). This debt often comes from SBIC lenders who make both debt and equity investments into the deal. On a minority of occasions, a lender will do a unitranche – a combo of Senior, Mezz, and Equity (sometimes in partnership with other lenders) to provide all the needed capital for the deal. Lenders will often take warrants (a right to equity at a future date).

There are some fantastic lenders in this market and some sharks – stay away from the sharks. Consider asking your lawyer (me) for recommendations or engaging a capital broker.

(ii) Contingent Purchase Price tools. The more a Sponsor can push to after closing the better. This includes, promissory note, rollover, earnout, holdback, consulting agreement, and bonuses. This usually makes up 15%-30% of the purchase price.

(iii) Equity. Usually about 10%-20% of the PP comes from equity. I have done several deals where $0 of sponsor equity was used, but this requires a great deal of creativity. The Indy Sponsor usually raises from friends, family, and investors to cover this portion. Sometimes Lenders provide equity, but most want to see the sponsor bring equity. Sometimes equity investors fund a portion of the costs incurred between LOI and Closing.

Indy Sponsor Economics -

How does the Indy Sponsor get paid? 3 ways (i) Transaction Fees, (ii) Management Fees, and (iii) Carry.

(i) Transaction Fees. The Sponsor gets a transaction fee of 2%-3% of the purchase price of the deal to compensate the sponsor for closing the deal. Some lenders require the Sponsor to not take these fees out at closing, but roll them into the deal (I hate this – I’ll tell you why in another post). The Sponsor also gets fees if they execute an add-on, refinancing, or sale.

(ii) Management Fees. The acquired target pays management fees to the Sponsor. This is usually 5.5% of EBITDA, with a floor (ceiling is less popular). The floor is usually around $250k depending on deal size.

(iii) Carry. Because the Indy Sponsor usually does not invest equity, they do not own any percentage of the Fund – the investors do. However, the Sponsor has a right to Carry – a percentage of the profits from a sale after Investors have received their money back + a hurdle (negotiated return). These waterfalls can get very complex, but the usually (1) investors get money back, (2) preferred return/MOIC hurdle, (3) Sponsor catch up of up to the initial carry (usually, 20%), lastly, (4) a percentage to investors, and a percentage to Sponsor. (Often, there are more hurdles and Sponsor has a higher upside).

Sponsor Post-Closing Role

After closing a deal, a Sponsor is supposed to be moderately hands-off, however, most of the good Indy Sponsors are very hands-on – spending time on location and driving improvements.

We are hosting a webinar on private equity (PE) funds.

Sign-up link is in the comments 👇

The teams at TIL and Abrecht Law will cover the following:

✅ A clear breakdown of how private equity funds are structured ✅ The typical lifespan of a PE fund — and how it ends ✅ What’s new in fund formation: 506(c) and open-end PE ✅ How to structure your LOI and win deals ✅ Optimizing tax structure (to save everyone money) ✅ Market trends in lower-middle-market PE

This session is perfect for: Fund managers, business owners, lawyers, LPs, and anyone navigating the fund formation or M&A space.

Details: 📅 Date: April 23, 2025 ⏰ Time: 9:00am PT | 12:00pm ET 📍 Location: See below in the comments

@elialbrecht@JoshuaASiegel@investing_law@Chris_Schuering