⏲️ Every delayed vessel creates a chain reaction.

🧠 Inventory planning. Terminal operations. Inland transport. Customer commitments. The challenge isn't just knowing where a vessel is today - it's understanding where it will be tomorrow.

🔮 Alphaliner Predict helps shipping and logistics professionals move from visibility to foresight by delivering daily forecasts for:

🔸ETA (Estimated Time of Arrival)

🔸ETB (Estimated Time of Berthing)

🔸ETD (Estimated Time of Departure)

🛰️ Powered by decades of actual sailing schedule data and advanced statistical modelling, Alphaliner Predict provides a forward-looking view of container vessel movements across global services.

Why does it matter?

✔️ Improve inventory and production planning

✔️ Anticipate the impact of port congestion and delays

✔️ Make faster, data-driven operational decisions

✔️ Deliver more reliable information to customers

✅ In a market where disruptions can quickly ripple across the supply chain, predictability becomes a competitive advantage.

💡 Discover how Alphaliner Predict can help your team stay one step ahead:

https://t.co/axrSc1TKI7

📢 MSC and Maersk market share gap keeps widening!

🗓️ The two leading container carriers displayed notably different market share trends in the month of May.

🏆 Following the explosive growth in its fleet seen from 2020 onwards, Mediterranean Shipping Company (MSC) last month hit a new record in terms of market share, operating 21.5% of total global container capacity.

ℹ️ No carrier has ever previously achieved such a quota, with the only other carrier to come close, Maersk, achieving 19.3% of the market in 2018.

🚀 Geneva-based MSC continues to eat into the market share of other lines, and it was the only top-10 carrier to reach a high in its market share this year. The world’s largest container carrier has effectively doubled its market share since 2010.

📉 At the other end of the scale, A.P. Moller-Maersk has adopted a very different strategy, and May saw the carrier languish at its lowest market share in twenty years. Tonnage operated by the group represented just 13.7% of the total container fleet, the lowest point since the Danish group bought P&O Nedlloyd in 2005.

♻️ Maersk’s deliberate decision to cap its fleet at 4.1–4.3 Mteu from early 2024, combined with the relentless growth in the overall container fleet, has condemned the company to a falling market share. The Danish carrier said that is would prioritise decarbonised fleet replacement and integrated logistics to achieve its strategic and financial objectives.

🌐 Elsewhere in the top-10, CMA CGM maintained a firm market share, holding 12.5% of the global fleet, only marginally down from the carrier’s peak of 12.9% in 2023.

✅ Read the full story and subscribe for the latest news in Liner shipping at https://t.co/GZTVLJGip1.

📢 Far East - Europe and Africa absorb most of fleet growth!

📉 The effect of the military conflict in the Middle East on shipping is clearly visible in the global container fleet deployment per trade. Vessel capacity deployed in services to the Middle East and India is down 7.6% year-on-year.

🔄 For the other trades, we see a continuation of the trends of the previous years. The largest trade, Far East - Europe, continues to grow strongly. Capacity deployed in African services saw a spectacular 25.3% increase year-on-year. Latin America also continues to be an important growth region for liner shipping.

🗓️ The capacity of the global container fleet increased 5.7% during the past twelve months to 33.9 Mteu. Between May 2025 and May 2026 another 1.84 Mteu of new teu slots were added to the fleet.

📊 A very large part of the new capacity was absorbed by the Far East – Europe trade. An extra 667,400 teu slots were deployed on this route, representing 36% of all the newly added fleet capacity. Overall vessel capacity was up 8.5% year-on-year.

📈 After an already impressive 11.7% increase between May 2024 and 2025, some carriers were still short of tonnage to staff all Far East – Europe loops which are deviating around the Cape of Good Hope due to the Red Sea crisis.

🔍 With 25% of the global fleet now trading there, it is by far the largest shipping lane for the liner fleet. Three years ago, the percentage stood at 20.8%. It might further increase as long as carriers cannot sail through the Strait of Hormuz.

✅ Read the full story and subscribe for the latest news in Liner shipping at https://t.co/GZTVLJGip1.

📢 Route trends lead to range of Q1 operating margins for lines!

🗓️ The average operating margin for the leading container carriers reached 5.2% in the first quarter of 2026, practically unchanged on the previous three months, but the result disguised a wide variety of individual performances by the lines.

📊 While the average ratio of EBIT return on carriers’ revenues remained in positive territory, and only marginally lower than the previous quarter’s 5.3% average, the gap between well and poorly performing lines grew more clearly in the period, forming two distinct groups.

📉 As in the previous quarter, three carriers declared operating losses: ZIM, Maersk and Hapag-Lloyd reported EBIT of -USD 5 M, -USD 174 M and -USD 192 M on shipping activities for the period.

ℹ️ This produced negative operating margins ranging from –0.4% (essentially a break-even result) to –3.6%. It was Maersk’s second consecutive quarter of operating losses for its Ocean division.

💲The lines, which operate above average capacity on the Transatlantic, suffered from shrinking export volumes out of Europe, which impacted both volumes and prices.

🔍 Also at the low end of the range, Yang Ming and ONE returned to profit in Q1 after slumping to a deficit in the fourth quarter of 2025.

✅ Read the full story and subscribe for the latest news in Liner shipping at https://t.co/GZTVLJGip1.

❓How much time is your team spending reacting to schedule changes instead of anticipating them?

🧠 Alphaliner Predict helps you stay proactive by giving you real-time visibility into containership fleet port calls, including accurate ETA, ETB & ETD insights across global liner services.

🛰️ Powered by decades of container shipping history and live operational signals, Alphaliner Predict API enables you to:

🔸 Automate schedule intelligence

🔸 Anticipate disruption before it hits operations

🔸 Reduce manual intervention and reactive firefighting

🔸 Scale predictability across networks and customers

📊 From terminals and ports to logistics providers and shippers, better predictability means stronger supply chain performance.

👉 Learn more and book your demo at https://t.co/axrSc1UixF 🔮

📢 Mirna Haddadin, Sinem Sen, Mael Pape-Léostic and Johnny Dewan from Signal were on the ground at TOC Europe in Hamburg this week.

🌍 It was a great event filled with meaningful catch-ups and conversations with clients throughout - exactly the kind of connection that makes these gatherings worthwhile.

💭 Thank you to everyone who stopped by to connect!

#TOCEurope #ContainerShipping

📢 European carriers control most of Europe-ECSA & WCSA trades!

🌍 The trades between Europe and the two coasts of South America are largely controlled by four European carriers. MSC, Maersk, CMA CGM and Hapag-Lloyd together operate 93.3% of all capacity, based on April figures.

💪 COSCO SHIPPING and Ocean Network Express (ONE) are the only Asian carriers trading between Europe and the East and West Coasts of South America, with a joint market share of 6.2%. This leaves only 0.5% for two niche carriers.

ℹ️ A total of 99 container ships were trading between Europe and ECSA & WCSA in April, representing a total capacity of 710,530 teu or 2.1% of the total cellular container fleet.

🚢 The Europe – ECSA trade was host to 49 ships with a total capacity of 369,573 teu. This was slightly larger than the Europe – WCSA trade with 50 ships totalling 340,957 teu. The average size of the ships trading to the East Coast is 7,542 teu. This compares to 6,819 teu for the West Coast.

🥇 MSC is now the market leader on both routes. Its market share by capacity deployed between Europe and ECSA stands at 34.8%. The Geneva-based carrier increased its capacity 4.1% year-on-year.

📉 This was enough to take over the number one position from Maersk. The Danish shipping line reduced its capacity by 13.0% y-o-y by shifting a series of 10,589 teu ‘Cap San-class’ ships to the Asia – Latin America trade in a swap with ‘L-class’ ships of 8,850 teu, which are now deployed in the Europe – ECSA ‘Samba’ service.

🔄 Despite this vessel swap, Maersk still has a strong market position with a 31.9% share.

✅ Read the full story and subscribe for the latest news in Liner shipping at https://t.co/GZTVLJGip1.

📈 Struggling to keep pace with constant changes in the container shipping market? Between fleet developments, vessel movements, and shifting trade patterns, fragmented data can slow down critical decisions.

🔍 With Alphaliner, you get a reliable, real-time view of the global liner industry - transforming complex market data into actionable intelligence.

🚢 Track fleets, monitor services, analyze orderbooks, and stay on top of market developments through one trusted platform used across the shipping industry.

⚡ Replace manual research and disconnected sources with faster insights, smarter planning, and greater confidence in your strategic decisions.

👉 Discover how Alphaliner helps industry professionals stay ahead in a fast-moving market at https://t.co/4VtfqCDoQL

📢 The global container supply chain community is gathering in Hamburg - and we'll be there!

🌍 Next week, TOC Europe will bring together the world's leading minds in port and terminal operations for three days of breakthrough technologies, forward-thinking strategies, and connections that matter. With 4,500+ attendees, 100 thought-leading speakers, and 900 port & terminal executives from over 100 countries - this is where the future of the industry takes shape.

🤝 Our Sinem Sen and Mirna Haddadin will be on the ground, connecting with senior decision-makers from across ports, terminals, and maritime logistics, and exploring the partnerships and opportunities that drive businesses forward.

📍 If you're heading to Hamburg, reach out to Sinem or Mirna - they'd love to connect in person!

#TOCEurope

📢 MSC has almost half of the North Europe - Med market!

🚢 MSC controls nearly half of all cellular capacity deployed in the North Europe - Mediterranean trades which as per 1 May stands at 360,517 teu.

📈 The Geneva-based carrier has by far the highest market share of all carriers in the North Europe - Med service segment. It reaches 45.5%, more than double that of its overall 21.6% global market share, placing it well ahead of all competing operators.

🌍 Alphaliner has identified only ten carriers offering regular liner services between North Europe and the Mediterranean.

💪 Seven of these are established Main Line Operators (MSC, CMA CGM, Maersk, COSCO Shipping Lines, ONE, ZIM and Hapag-Lloyd), collectively accounting for 97.3% of the total North Europe - Med capacity.

📊 This leaves a combined share of just 2.7% for the three regional carriers Tailwind Shipping Lines, Borchard Lines and Akkon Lines.

✅ Read the full story and subscribe for the latest news in Liner shipping at https://t.co/GZTVLJGip1.

⏪ Looking back at last month's breaking news, container shipping developments showed a market adjusting on multiple fronts: from fleet ownership to operating speeds.

📰 Based on Alphaliner’s Weekly Newsletter:

🔸 Far East–Oceania capacity surged by 12%, outpacing global fleet growth

🔸 MSC Mediterranean Shipping Company and CMA CGM led the expansion, reshaping rankings on the route

🔸 The decline of Non-Operating Owners slowed, but carriers continued absorbing tonnage

🔸 Regional carriers outperformed global lines, driven by strong intra-Asia demand

🔸 Rising bunker prices pushed fleet speeds to their lowest levels in over two years

📌 The takeaway: growth continues, but it’s becoming more selective, more regional, and more cost-driven.

📝 We’ve summed up the major container shipping developments we reported throughout April in our latest blog.

👉 Read our recap here: https://t.co/m54tYZ4rp3

⏪ Looking back at April, container shipping data revealed just how abnormal current market conditions were.

🔎 Based on Alphaliner insights:

🔸 Container ship transits through Hormuz remained extremely limited, even after the ceasefire

🔸 Several vessels were attacked or seized, marking a clear escalation in risk

🔸 International liner participation became sporadic and highly selective

🔸 Global fleet capacity expanded beyond 34 Mteu, with MSC exceeding 7.3 Mteu

🔸 The market remained fully employed, but partly because capacity was effectively trapped or diverted

📝 We’ve broken this down in our latest data-driven article recapping the main container ship trends observed throughout April.

💡 Read our full blog: https://t.co/5ElvpRfkUo

📢 Chinese-built slow-steamer container ships: from domestic workhorses to charter market stars?

📅 Over the past decade, the Chinese coastal and domestic trades have absorbed numerous container ship newbuildings designed specifically for this growing sector of the liner market. Most of these vessels share features that adapt them to the specific requirements of the trade.

🛳️ The Chinese domestic lines favour very compact ships with a high deadweight, small engines, modest reefer intakes, and slow sailing speeds that rarely exceed 15 knots. Typically, these ships are built without gear and their lashing bridge arrangements are minimal to non-existent.

ℹ️ The ship design reflects the nature of the cargo and the routes, with fairly high average container weights, a low percentage of reefer containers, and relatively short steaming distances between the Chinese main ports.

🔎 One might describe these ships as 'low tech' vessels with specifications that make them resemble open-hatch bulk carriers without cranes.

🏗️ While some of this tonnage was produced by first-tier yards such as Yangzijiang or Jinling, many vessels originate from lesser-known producers of the second or third tier that primarily build tonnage for compatriot owners in China.

✅ Read the full story and subscribe for the latest news in Liner shipping at https://t.co/GZTVLJGip1.

⚠️ Container planning changes between schedule releases.

🔀 Transit times move. Capacity shifts. Service patterns evolve week by week, sometimes before the impact is visible in rates, lead times or customer commitments. Published schedules only tell part of the story.

👨💻 Alphaliner’s APIs help turn live vessel and service data into practical benchmarks for day-to-day decisions:

🔸️ Transit Time API: Track actual transit time performance by lane and service. Compare routings, monitor consistency and identify where schedules are starting to drift.

🔸️ Capacity Watch API: Follow deployed capacity week on week. Spot service changes, vessel deployment shifts and forward capacity signals before they affect planning assumptions.

🧠 Together, they bring real-time container ship intelligence directly into your planning, commercial and operational workflows.

✅ Less guesswork. Better benchmarks. Faster and more accurate decisions.

👀 Want to see how this maps to your key loops and trade lanes?

💡 Book your demo with our team today:

https://t.co/pEbq5DK6X3

✨Last week, we had the pleasure of being represented by Sinem Sen and Mirna Haddadin at the three-day Mediterranean Ports and Logistics 2026 event in Porto.

📝 Alongside the conference programme, their busy agenda included customer visits, prospect meetings and supplier discussions across the port and logistics community, including port authorities, terminal operators and freight forwarders.

🎉 A particular highlight cherished by Sinem and Mirna was the reception dinner hosted by YILPORT Holding Inc., which brought together familiar faces from across the port and logistics community.

🙌 Thank you to everyone who took the time to meet with our colleagues in Porto. We look forward to continuing the discussions.

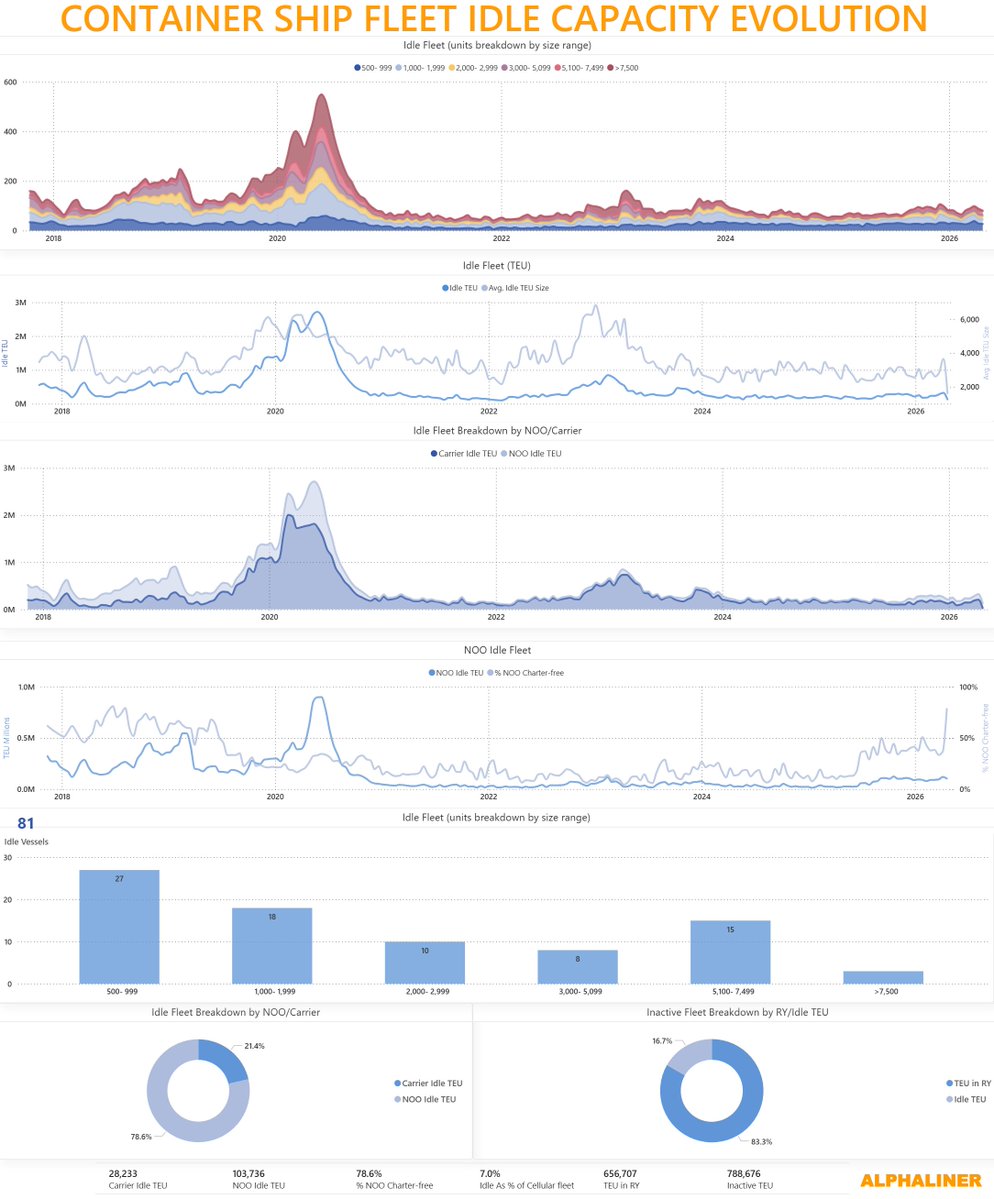

📰 Gulf Conflict: Uncertainty keeps tonnage supply tight!

📅 Nine weeks after the start of military action in the Middle East Gulf, commercial idling of container tonnage remains low.

ℹ️ The idle vessel fleet briefly touched the 1% capacity mark for the first time in more than two years, but has since slipped back to 0.7%. At this level, the liner sector remains in “full employment”, with no signs of “structural” idling.

🔎 This does not mean the market is unaffected. Most carriers have had to adjust their networks in some way, and the operational impact of these changes continues to absorb vessel capacity. Diverted sailings, rescheduled loops, vessel detours and delays all add to effective tonnage demand.

✅ Alphaliner does not count every vessel stuck in or affected by the Middle East situation as “commercially idle”. This distinction matters.

🛳️ At least 58 container ships, representing around 310,000 teu, have diverted or sheltered due to the conflict. With widespread AIS transponder deactivation in the region, the actual figure could be higher. These vessels are not available for normal revenue service, which means this “forced inactivity” is draining supply even if it does not appear in the commercial idle fleet.

📊 As per our latest count, Alphaliner tallied 81 ships of 235,705 teu as commercially idle.

📉 Capacity tied up in drydock also declined moderately over the past fortnight, falling by almost 150,000 teu to 141 units of 656,707 teu. Combined, the idle and “in yard” fleet accounted for 2.7% of the global fleet.

👨💻 With Alphaliner’s AXSInsights module, you can monitor container ships in active service, commercially idle, or in shipyards and repair docks.

💡 Find out more and request a demo at https://t.co/dl6n9fFyga. 👈

📣 Carriers react to bunker price increase: One fleet, two speeds!

📅 Between Q4 2025 and Q2 2026 (to 14 April), the average speed of the container vessel fleet dropped by 2.3%, from 15.58 to 15.22 knots, with the move concentrated entirely after 28 February.

📊 On 14 April, Alphaliner recorded an average of 15.18 knots, the lowest reading since March 2023.

📈 Directly driving this deceleration, bunker prices moved sharply in the opposite direction, reaching all-time highs of $1,201 per tonne for VLSFO on 13 March and USD 2,018 per tonne for LSMGO on 3 April both in Singapore.

🔍 The Gulf crisis’ impact on speeds however is not homogenous across all trades.

🌐 North-South trades slowed the most. Far East - South America and Far East - ANZ both lost 3.6% over the period.

🚢 Long sea-passages make speed cuts even more valuable and these services usually carry enough slack to absorb slower steaming without breaking schedule frequency. The Transpacific and Transatlantic also clearly reacted to fuel price increases: Far East - East Coast of North America reduced speed by 2.2%, Far East – West Coast North America by 1.8%, and the North Atlantic by 1.5%.

✅ Read the full story and subscribe for the latest news in Liner shipping at https://t.co/GZTVLJGip1.

📊 Are you making carrier decisions based on rate cards and gut feel - or actual performance data?

🌐 Transit times and capacity swing week to week. Without real-time benchmarks on existing services, you aren't planning - you're guessing. And while you guess, your competitors optimize.

🧭 Here are two game changer tools:

🔹 Transit Time API - Monitor lane and service-level transit time performance. Benchmark your service against competitors objectively. See which operators consistently deliver on their schedule. Spot weak loops before they cascade.

🔹 Capacity Watch API - Track deployed capacity patterns week on week. Identify early service shifts, anticipate capacity changes before they impact your rates and lead times, and see weeks ahead with predictive schedule visibility.

💡 Together, they give your team the fact-based clarity to plan with confidence, reduce costly last-minute expediting, and negotiate carrier contracts from a position of strength.

⏱️ Worth 20 minutes to see how this maps to your key loops and trade lanes?

👉 Book your demo with the Alphaliner team today at https://t.co/KkyVKJwCyQ

📢 The Xinde Marine Forum Singapore 2026 brought together the industry to navigate disruption and set a new course, and our team - Keston Chia, Chavmaine Aw, Saranya Sivakumar, and Rinaldi Gumulya were proud to be part of it!

🎙️ Rinaldi had the privilege of moderating a panel discussion that brought together a well-balanced mix of voices - carriers, shipowners, and macro-level thinkers - each offering a distinct perspective on the challenges shaping container shipping today.

⚓ The conversation touched on what matters most right now: ongoing disruptions, massive orderbooks, shifting trade flows, and fragmenting regulatory frameworks - and how the interplay of all these forces is defining the new balance for the sector.

💡 Events like this are a reminder of why bringing together different parts of the industry in one room matters. The insights that emerge from those conversations are exactly what help us serve our clients better in a rapidly changing maritime landscape.

🤝 Thank you to the Xinde Marine Forum team for a world-class event.

📢 All three non-Iranian container ships attempting to transit the Strait of Hormuz yesterday reportedly came under attack, with two confirmed seized.

1️⃣ EPAMINONDAS (7,200 TEU, Technomar-owned, on @MSCCargo charter) was hit by gunfire and rocket-propelled grenades while transiting eastbound, sustaining bridge damage before being seized by the IRGC. AIS signals place the vessel currently stationary between Qeshm, Larak, and Hormuz islands.

2️⃣ MSC FRANCESCA (11,200 TEU, MSC-owned) was intercepted eastbound, reportedly damaged and subsequently detained. Its last AIS position showed it stopped off the Iranian coast on the east side of the Strait.

3️⃣ A third vessel, EUPHORIA (UAE-owned), was also reported fired upon during transit but continued its voyage and is now offshore Fujairah east of the Strait.

⚠️ The incidents mark a major escalation for container shipping, with liner traffic now directly exposed to the coercive risks. Yet the attacks also cap a broader pattern visible in container traffic through Hormuz over the past month and a half.

🛰️ Alphaliner AIS-derived data has recorded 54 container ship crossings across 53 days since 1 March. Half of them involved Iranian-flagged or Iranian-owned vessels operating on domestic and state-linked routes. The remaining 27 were non-Iranian.

🔎 Persistent Iran-linked and regional feeder traffic has continued, while participation by international liner operators has become sporadic and increasingly vulnerable.

🕵️ Among non-Iranian crossings, the overwhelming majority involved small feeder and regional tonnage, rather than sustained participation by the mainline container trades.

📝 Meaningful deepsea liner participation has been limited to a handful of notable exceptions:

🔸 1 March: @Maersk recorded the last conventional mainline transit before widespread withdrawal with the ASTRID MAERSK.

🔸 30 March: two large @COSCOSHIPPING vessels (CSCL INDIAN OCEAN and CSCL ARCTIC OCEAN) transited outbound the Persian (Arabian) Gulf.

🔸 2 April: CMA CGM KRIBI (@cmacgm-owned) recorded a single isolated crossing, not repeated.

🔸 21 April: TEMA EXPRESS, owned by @HapagLloydAG reappeared after a month-long AIS blackout on the east side of the Strait.

🔸 22 April: the first significant non-Iranian capacity attempt outside the apparent exemption framework in three weeks ended with all three vessels attacked.

ℹ️ A notable share of non-Iranian feeder crossings has also involved opaque ownership structures, suggesting parallel regional networks may have helped sustain residual corridor activity despite disruption.