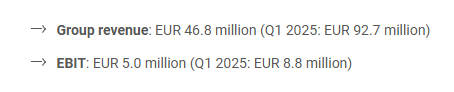

M1 Kliniken $M12.DE publishes Q1 figures.

If someone not very well informed saw first pic would think is a disaster.

Turns out market isn't very smart, M1 sold a big part of the company and the remaining business (beauty clinics) is doing really well. Pic #2

-7% today....😌

Repasando esta semana una vieja conocida tras ver video de @HolyFinance :

Groupe Guillin $ALGIL

Sigue siendo buen negocio, con "propietario", balance muy sólido y a valoración atractiva.

🧠A c/p sufrirá por aumento crudo pero cuando ajusten precios volverán a márgenes altos.

Repasando esta semana una vieja conocida tras ver video de @HolyFinance :

Groupe Guillin $ALGIL

Sigue siendo buen negocio, con "propietario", balance muy sólido y a valoración atractiva.

🧠A c/p sufrirá por aumento crudo pero cuando ajusten precios volverán a márgenes altos.

Uff 😮💨 buenísimo el documental de @RafaelNadal en Netflix. Me lo he terminado del tirón.

Rafa es un símbolo de ambición, sacrificio y superación pero no sabía que había ido tan al límite🔝

Imposible no emocionarse, el mejor deportista español de la historia. Que suerte tuvimos

Time to reveal my last portfolio incorporation:

Northern Oil & Gas $NOG

Market Cap: 2,3B$

What made this company interesting for me was its NON-OPERATOR business model. What does this mean?

Short thread 🧵👇

I'm working on a thesis about an oil & gas company from 🇺🇸. I haven't finished it yet, but today market is offering it to me cheaper than when the Iran conflict began.

Mr. Market’s logic🎰🧠

It's only a matter of time before SECURE $SES.TO is gone...so I'm using some cash

Financially, it’s a value-generating machine. Free from massive fixed assets, they convert crude prices into FCF.

Why hasn't the stock perform as expected despite high oil & gas prices? Production was highly hedged (77% oil, 62% gas) at lower prices, causing derivative losses.

$93M1 MPH Health Care AG released their AR25 & show an increase in their $M12 holdings by 1.6% - they now hold 66.3% of the M1 Kliniken shares & trade at a ±50% discount (!!!) to that holding, despite the recent run-up.

The Character Group $CCT.L

Dos insiders comprando acciones a 276p.

Pequeñas compras de apenas £4.500 y £9.200 pero aumentando sus posiciones al fin y al cabo.

El primero tiene un 5,66% de la empresa y el otro +11%.

ℹ️Guidance $CCT.L para FY:

▫️Ventas planas

▫️Márgenes EBITDA mejorados al ~31% actual

▫️Mejora de posición caja

📢Y lo mejor:

▫️Anuncia que EBIT superará significativamente las previsiones actuales del mercado

🫠 Los resultados anuales de Shinnihon (1879.T)...📸

EPS: 260¥

Cotizando a 2285¥ con un un market cap. de 134M¥ y EV de apenas 40M¥

Encima suben el dividendo (me da un poco igual) a 67¥ y presentan un guidance bastante prometedor🙃

Quizás me precipité al vender, habrá que ...👀

Me ha costado decidirme, pero después de +6 años (desde inicio de posición) decido vender Shinnihon (1879.T) a 1986¥ principalmente para hacer liquidez.

Rentabilidad acumulada: 133%

Liquidez al 17% para ampliar alguna que otra posición y mirando nuevas candidatas🧐

Digital Bros🎮 $DIB.MI Q3 2026:

Weak Q3 but good 9M

Results impacted by the asset impairment of 10,7M€ for the cancellation of game Directorate.

Best position ever

Guidance for FY:

Revenue increase with better cost efficiency resulting in positive EBIT

Back to (low) net debt

ℹ️Guidance $CCT.L para FY:

▫️Ventas planas

▫️Márgenes EBITDA mejorados al ~31% actual

▫️Mejora de posición caja

📢Y lo mejor:

▫️Anuncia que EBIT superará significativamente las previsiones actuales del mercado

The Character Group $CCT.L H1:

✔️Aumento y mejora margen EBITDA (£4,2M y 31,7% respecto £3,7M y 29,3% en 2025) a pesar de reducción de ventas (-9%)👈

✔️EPS: 11,06p (+29%)

✔️Caja: £13,9M

✔️Deuda: ~£0

✔️Programa recompra completado al 18%

@CFAs4CFPs Haha so true! That was going to be my next comment.

MPH increasing its dividend from 6M€ to potentially 14,5M€ from its M1 stake was missed by the market😅