Goldman finally upgrades Kioxia https://t.co/gvV7GGWRoK to Buy and nearly doubled its PT from ¥48,000 to ¥93,000 and got materially more bullish on Kioxia and, by extension, the NAND cycle.

Peak profits are now expected to continue rising through FY3/29 instead of peaking materially earlier!

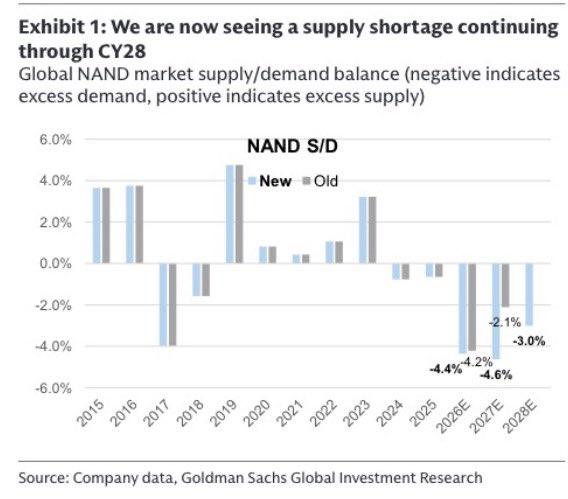

(++) Goldman now expects NAND supply tightness to persist through CY28

(++) Peak profits this cycle seen materially higher and more sustainable than previously assumed

(++) Samsung, SK Hynix and Micron continue prioritizing DRAM/HBM investment, limiting NAND supply growth

(++) DRAM procurement risk for enterprise SSDs appears largely resolved

(++) BiCS 8 transition expected to drive lower costs and stronger margins over time

(+) IR Day, quarterly results and continued NAND price increases seen as potential catalysts

Goldman isn’t arguing NAND has become a structurally different industry. They’re arguing the cycle itself has changed because AI demand is arriving while supply growth remains constrained.

Same cyclical industry, much higher earnings ceiling.

If NAND supply remains constrained because memory makers keep allocating capital toward DRAM/HBM, that should support the broader NAND ecosystem for longer than investors currently expect.

https://t.co/gvV7GGWRoK $MU $005930.KS $000660.KS