Let's bring up the elephant in the room here:

That's a tailwind for $INTC .

Ironically, it could be a relative headwind for $AMD , whose AI narrative is increasingly tied to GPU share gains.

When $NVDA tells you AI needs more CPUs, you should listen.

An NVIDIA executive just told me the GPU-to-CPU ratio will go from 2:1 today to 1:1 “in months" due to agentic AI.

NVIDIA executive is saying 1:1 IN MONTHS.

CPU CPU CPU $NVDA

Both MSCO and JPM raising $ASML EUV ests today, '28 EUV units now at 104 and 105, respectively. Super bullish notes, upping ests and PTs, too. MSCO PT to €1,660 and JPM to €1,900 ($2,200)

JPM: "The Street is Behind the Curve: ‘27/’28 Numbers Need a Rewrite"

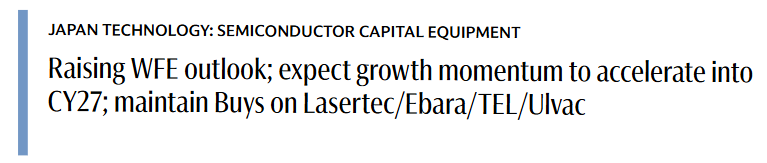

Goldman came away from its Tokyo Electron call with one message:

WFE demand is still getting stronger, not weaker.

The biggest upward revision wasn’t AI GPUs.

It was memory.

TEL’s DRAM and NAND outlook moved materially higher in just three months, reinforcing the “higher-for-longer” memory capex thesis that’s been showing up across multiple reports recently.

If memory makers continue accelerating DRAM/HBM and NAND investments while China logic/foundry demand remains strong, the next estimate revisions may come from the equipment side rather than the chip side.

https://t.co/3isc5b4VYD

Goldman Sachs raising its WFE outlook and expects growth momentum to accelerate into CY27:

The WFE market remains in a strong upcycle, driven by AI-led semiconductor demand and tight supply in advanced nodes. Capex is expanding beyond leading players, with growth expected to accelerate into 2027. Goldman Sachs raises WFE forecasts through CY28 and lifts earnings estimates and price targets across front-end equipment names.

Preferred stock selection focuses on earnings upside vs. consensus. Key highlights include Lasertec, supported by its ACTIS A200HT mask inspection tool, and Tokyo Electron, benefiting from stronger WFE growth and improving profitability.

In the US-listed space, companies with similar positive setup and earnings momentum include $AMAT (Applied Materials), $LRCX (Lam Research), $KLAC (KLA Corp), and $TER (Teradyne), all leveraged to advanced logic, memory, and AI-driven capex cycles.

Goldman doubling down on its upgraded Kioxia thesis after the company’s IR Day.

What’s interesting is that management largely reinforced the exact points Goldman used to upgrade the stock just days ago (see tweet below). Looks like Nakamura did a good job (finally).

(++) Kioxia expects NAND demand to grow ~22% CAGR through CY28

(++) AI inference demand driving NAND growth at ~46% CAGR in datacenters

(++) NAND tightness expected to continue through at least 2H27

(++) LTAs increasingly being used to stabilize margins and reduce cycle volatility

(++) Existing fabs appear sufficient until 2029, limiting the need for aggressive supply additions

(+) Shareholder returns becoming a larger part of the story through dividends and potentially buybacks

Management increasingly frames SSDs as a performance-critical component for AI inference systems, which helps explain why Goldman believes NAND profitability can stay elevated much longer than in prior cycles.

https://t.co/gvV7GGWRoK $MU $005930.KS $000660.KS

Goldman finally upgrades Kioxia https://t.co/gvV7GGWRoK to Buy and nearly doubled its PT from ¥48,000 to ¥93,000 and got materially more bullish on Kioxia and, by extension, the NAND cycle.

Peak profits are now expected to continue rising through FY3/29 instead of peaking materially earlier!

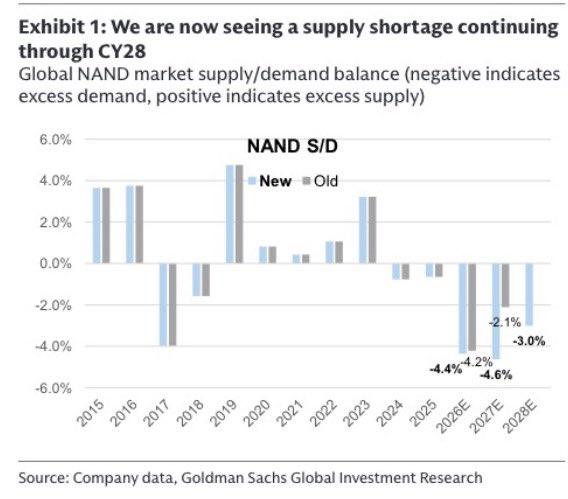

(++) Goldman now expects NAND supply tightness to persist through CY28

(++) Peak profits this cycle seen materially higher and more sustainable than previously assumed

(++) Samsung, SK Hynix and Micron continue prioritizing DRAM/HBM investment, limiting NAND supply growth

(++) DRAM procurement risk for enterprise SSDs appears largely resolved

(++) BiCS 8 transition expected to drive lower costs and stronger margins over time

(+) IR Day, quarterly results and continued NAND price increases seen as potential catalysts

Goldman isn’t arguing NAND has become a structurally different industry. They’re arguing the cycle itself has changed because AI demand is arriving while supply growth remains constrained.

Same cyclical industry, much higher earnings ceiling.

If NAND supply remains constrained because memory makers keep allocating capital toward DRAM/HBM, that should support the broader NAND ecosystem for longer than investors currently expect.

https://t.co/gvV7GGWRoK $MU $005930.KS $000660.KS

Goldman Sachs is actually a bit cautious on Furukawa https://t.co/5mjmaLsmoo near term despite remaining bullish longer term.

The new MMC connector ferrule capacity won’t meaningfully contribute until FY3/29, meaning the stock may need time before the AI optical upside fully shows up in earnings.

(++) New MMC/TMT ferrule plant supports growing demand from next-generation AI datacenter optical architectures

(++) Furukawa continues expanding its higher-margin optical/datacenter product mix

(+) Production capacity expected to increase by more than 1.5x versus current levels

(+) Existing partnerships with Sanwa Technologies and US Conec reinforce ecosystem positioning

(=) Mass production begins around FY3/29, making this more of a medium-term than near-term catalyst

@ReadFuturist@ChipsSaas Not sure about the actual timeline but if you got market access to Germany you can trade the GDRs at least or IBKR started to offer Korean trading access a few weeks ago.

$GNRC announces a global supply agreement with a leading hyperscale data center operator to provide backup power generators. Stock up around 8% in premarket trading so far.

So every new hyperscale data center build requires backup generation, electrical distribution, switchgear, UPS and power management infrastructure.

Names to watch for a potential sympathy move today might be:

$VRT for power & cooling infrastructure

$ETN for electrical distribution & switchgear

$GLW +4% so far today in early premarket trading - not as a new name but as a huge beneficial of the optical interconnect leg.

At Computex 2026, Corning was featured throughout Wiwynn's next-generation "In-Chassis Optical Interconnect" platform alongside Ayar Labs and other photonics players. As AI clusters scale, the bottleneck shifts from compute to connectivity.

Kind of agree here, even though it wasn´t necessarily a surprise quarter, but another step in $CRDO ´s transition from a copperr and connectivity company into a much larger optical infrastructure play.

Goldman Sachs thinks investors are increasingly focused on optical momentum rather than copper displacement. In fact, they still see copper solutions remaining highly relevant while optical becomes a much larger piece of the mix.

(++) Optical revenue outlook raised from $500M to $600M for FY27

(++) ZR optics now expected to be the largest optical revenue contributor (~$400M)

(++) Gross margins continue outperforming expectations despite aggressive growth

(++) EPS estimates raised ~31% following stronger revenue and margin assumptions

(++) PT raised from $170 to $250

(+) Customer diversification improving, with neocloud customers potentially reaching ~20% of revenue over time

(+) DustPhotonics acquisition expanding the optical product portfolio

Another positive datapoint for the broader optical networking theme. If hyperscalers continue scaling AI clusters, the winners likely extend beyond transceivers into DSPs, SiPho, ZR optics and coherent connectivity.

UBS’s first Computex takeaway was about the AI spending cycle continuing to flow especially through the Taiwan supply chain.

Major beneficiaries are some well known names:

(++) Alchip (https://t.co/gZu3o7swvF) sees visibility extending into 2027 as 3nm ASIC programs continue ramping

(++) MediaTek (https://t.co/4Olmlla9DD) increasingly positioning itself at the center of the custom ASIC ecosystem through NVLink Fusion, AI PCs and edge AI

(++) Silicon Motion (https://t.co/oRfAfmRCK9) benefiting from accelerating enterprise SSD and AI storage demand

(++) VPEC (https://t.co/ja950tnnPE) highlighted strong optical demand, pricing power and new laser ramps into 2027

(+) Lotes (https://t.co/TJLmW5Bkpm) continues seeing content gains from next-gen server CPU platforms

(+) Taiwan assemblers, memory names and power suppliers remain key beneficiaries of Rubin and broader AI infrastructure deployments

Custom silicon, optics, storage, packaging, connectors, power delivery and server infrastructure are all participating, with Taiwan remaining one of the biggest beneficiaries of the next leg of AI capex (and sme are alrdy imo).

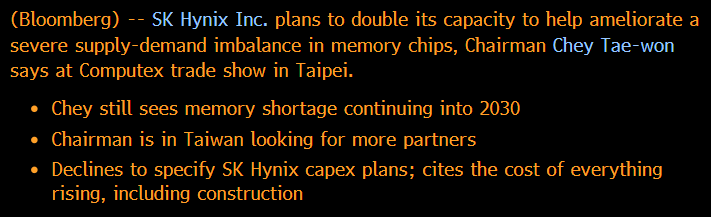

Goldman also just raised the bar for its entire memory thesis again.

The big change isn’t 2026. It’s after - towards 2027-2028.

> Goldman now expects DRAM, NAND and HBM supply/demand to be even tighter in 2027 than 2026

> Undersupply conditions now expected to persist into 2028 across all three memory markets

> AI servers and agentic AI driving much stronger demand visibility than prior cycles

> Limited supply growth due to slower capacity additions and rising HBM wafer allocation

> Long-term agreements increasingly reducing traditional memory cycle volatility

> HBM pricing expected to “catch up” further versus conventional DRAM, driving a larger HBM TAM

> PTs raised for Samsung and SK Hynix; Kioxia upgraded to Buy (see post below)

$MU $005930.KS $000660.KS https://t.co/gvV7GGWRoK

Goldman finally upgrades Kioxia https://t.co/gvV7GGWRoK to Buy and nearly doubled its PT from ¥48,000 to ¥93,000 and got materially more bullish on Kioxia and, by extension, the NAND cycle.

Peak profits are now expected to continue rising through FY3/29 instead of peaking materially earlier!

(++) Goldman now expects NAND supply tightness to persist through CY28

(++) Peak profits this cycle seen materially higher and more sustainable than previously assumed

(++) Samsung, SK Hynix and Micron continue prioritizing DRAM/HBM investment, limiting NAND supply growth

(++) DRAM procurement risk for enterprise SSDs appears largely resolved

(++) BiCS 8 transition expected to drive lower costs and stronger margins over time

(+) IR Day, quarterly results and continued NAND price increases seen as potential catalysts

Goldman isn’t arguing NAND has become a structurally different industry. They’re arguing the cycle itself has changed because AI demand is arriving while supply growth remains constrained.

Same cyclical industry, much higher earnings ceiling.

If NAND supply remains constrained because memory makers keep allocating capital toward DRAM/HBM, that should support the broader NAND ecosystem for longer than investors currently expect.

https://t.co/gvV7GGWRoK $MU $005930.KS $000660.KS

@JeffBro52400644 Goldman‘s highest Rating is Buy (on CL) so I assume they change to Buy for now and will add Kioxia on June 1st to their APAC Conviction Buy List…

Goldman finally upgrades Kioxia https://t.co/gvV7GGWRoK to Buy and nearly doubled its PT from ¥48,000 to ¥93,000 and got materially more bullish on Kioxia and, by extension, the NAND cycle.

Peak profits are now expected to continue rising through FY3/29 instead of peaking materially earlier!

(++) Goldman now expects NAND supply tightness to persist through CY28

(++) Peak profits this cycle seen materially higher and more sustainable than previously assumed

(++) Samsung, SK Hynix and Micron continue prioritizing DRAM/HBM investment, limiting NAND supply growth

(++) DRAM procurement risk for enterprise SSDs appears largely resolved

(++) BiCS 8 transition expected to drive lower costs and stronger margins over time

(+) IR Day, quarterly results and continued NAND price increases seen as potential catalysts

Goldman isn’t arguing NAND has become a structurally different industry. They’re arguing the cycle itself has changed because AI demand is arriving while supply growth remains constrained.

Same cyclical industry, much higher earnings ceiling.

If NAND supply remains constrained because memory makers keep allocating capital toward DRAM/HBM, that should support the broader NAND ecosystem for longer than investors currently expect.

https://t.co/gvV7GGWRoK $MU $005930.KS $000660.KS

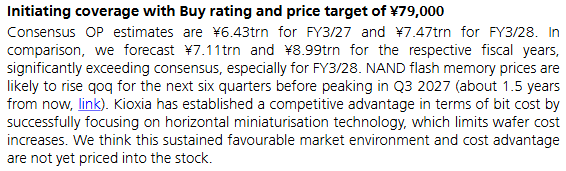

UBS initiating Kioxia with Buy https://t.co/gvV7GGWRoK with a pretty aggressive stance on the NAND cycle.

Their core argument:

The memory upcycle still has a lot more room to run - especially as AI inference increasingly pulls NAND into the AI infrastructure stack.

(++) UBS thinks NAND pricing likely continues rising for another ~6 quarters before peaking

(++) AI inference workloads increasingly driving NAND demand, not just HBM/DRAM

(++) Kioxia seen as having a meaningful cost advantage through horizontal scaling technology

(++) UBS forecasts remain well above consensus, especially into FY3/28

(+) Supply/demand conditions expected to stay tight with bit growth remaining constrained

(+) PT initiated at ¥79,000 with Buy rating

Another sign the Street increasingly sees AI memory demand broadening beyond HBM into the full storage stack as inference/context windows scale.

Come and visit London’s Home of Trophies. 🏆

Book your Stadium Tour at Stamford Bridge now. ⭐️⭐Come and visit London’s Home of Trophies. 🏆

Book your Stadium Tour at Stamford Bridge now. ⭐️⭐Come and visit London’s Home of Trophies. 🏆

Book your Stadium Tour at Stamford Bridge now. ⭐️⭐Come and visit London’s Home of Trophies. 🏆

Book your Stadium Tour at Stamford Bridge now. ⭐️⭐Come and visit London’s Home of Trophies. 🏆

Book your Stadium Tour at Stamford Bridge now. ⭐️⭐Come and visit London’s Home of Trophies. 🏆

Book your Stadium Tour at Stamford Bridge now. ⭐️⭐️