Alaska'nın yüksek zirvelerini gözlemleyen görevliler, zirvede hiç beklemedikleri bir manzara ile karşılaştı. Zirvede, yalnız başına manzaranın keyfini çıkaran devasa bir boz ayı görüldü.

"The top 1 percent of American households, which have a minimum net worth of $11.1 million, now collectively own about $25.6 trillion worth of stocks and mutual funds, the same amount as the remaining 99% of the country," per the Federal Reserve

STRATEGY CEO PHONG LE REVEALED:

THEY HAVE 72 YEARS OF BITCOIN RESERVES ENOUGH TO LAST UNTIL 2100 🤯

“WE’RE CREATING A BULLETPROOF BALANCE SHEET FOR THE NEXT 65–100 YEARS.”

THIS IS WILD 🚀

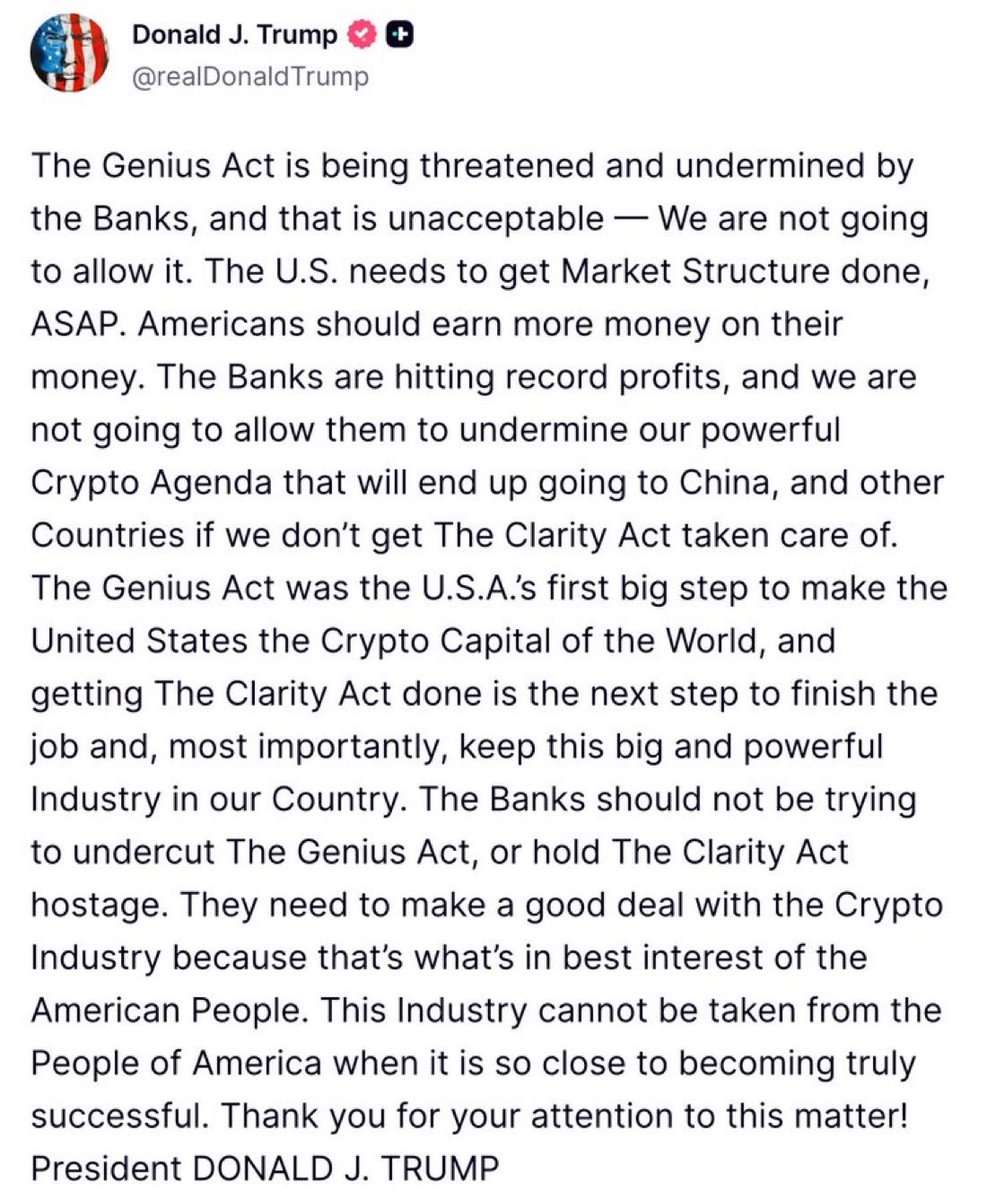

🚨 STABLECOIN YIELD DEBATE HEATS UP IN SENATE HEARING

Banks argue that stablecoin interest could drain deposits from credit unions and traditional banks.

At the Senate Banking hearing, NCUA Chair KYLE HAUPTMAN pushed back.

🔹 Stablecoins aren’t inherently a threat

🔹 Credit unions can participate in the ecosystem

🔹 Innovation shouldn’t be blocked to protect incumbents

One of the key fights in the stablecoin CLARITY Act debate is whether digital dollars can offer yield.

Banks want restrictions.

Crypto wants open competition.

$ETH $BTC

Let me make this very clear: Big Banks (think JPMorgan Chase, Bank of America, Wells Fargo, etc.) are lobbying overtime to block Americans from getting higher yields on their savings—while trying to block any rewards or perks from being given to customers.

These banks, and others, pay rock-bottom rates on standard savings (often 0.01%–0.05% APY), even as the Fed pays them 4% or more. This massive spread fuels record profits, with almost none passed back to their customers / everyday depositors.

Today, the banks are desperately targeting crypto/stablecoins, where platforms plan to offer 4–5%+ yields or rewards. The ABA and other lobbyists are spending millions trying to ban or restrict those yields via bills like the Clarity Act, crying “fairness” and using words like "stability"—when it's really about protecting their low-rate monopoly and preventing deposit flight. This is anti-retail, anti-consumer, and straight-up anti-American.

Next time you see a big bank dropping billions on a shiny new Midtown Manhattan HQ, you know exactly where that money comes from: the non-existent interest rate they “pay” you!

Fortunately, the big banks are losing this fight as customers wake up to the games…

@worldlibertyfi

BREAKING: 🇺🇸 THE FEDERAL RESERVE JUST OFFICIALLY APPROVED A BITCOIN AND CRYPTO EXCHANGE TO ACCESS THEIR PAYMENTS SYSTEM

THIS IS ABSOLUTELY WILD

IT CHANGES EVERYTHING

HERE WE GO 🚀

The “Big Banks”—the very institutions that have held a monopoly and screwed their customers for years, offering near-zero yields on retail Money Market Accounts while crushing low-balance accounts with exorbitant fees—are now doing everything they can to block the Crypto industry from offering real benefits, perks, and rewards on their platforms.

They are the greatest hypocrites and are in mass panic given they know they are losing the digital finance race! @worldlibertyfi

Unrealized gains tax for Gen-Z:

You buy a Pokémon card for $50.

Someone offers you $500 for it. You say no. You love that card. You're keeping it.

The government says: "Cool, but that card is worth $500 now. You owe us $100 in taxes."

You: "…I didn't sell it."

Government: "Don't care. Pay up."

You don't have $100 lying around. So you're forced to sell the card you love just to pay a tax on money you never received.

Next month? That card drops back to $50.

Your card is gone. Your money is gone. And the government shrugs.

That's a wealth tax on unrealized gains. They don't pay you back the tax...

Now picture this.

Your mom calls you crying. She has to sell the house she raised you in. Not because she can't afford it. She's lived there 30 years. It's paid off.

But some website says it's worth more now and the government says she owes $15,000 she doesn't have.

So she sells your childhood home. The kitchen where she made you breakfast. The doorframe where she marked your height every birthday.

Gone.

To pay a tax on money that was never real.

Now picture the opposite.

Your dad put everything into his small business. For 20 years he built it from nothing. One year the business is "valued" at $2 million on paper. He owes a massive tax bill. He empties his savings. Sells his truck. Borrows money. Pays it.

Next year the market crashes. His business is worth $200,000.

He lost everything to pay a tax on a number that doesn't exist anymore.

Does the government give him his money back?

No.

Does the government give him his truck back?

No.

Does the government care?

No.

They sold this idea as "taxing billionaires." But billionaires have armies of lawyers, offshore accounts, and trusts. They'll be fine.

You know who won't be fine? Your mom. Your dad. Your neighbor with a small business. The farmer down the road who's had the same land for four generations and now has to sell it because dirt got expensive.

You're not taxing wealth. You're taxing people for owning things.

It's like getting a parking ticket for a car you might drive somewhere someday.

They want you to own nothing and be happy. To fund the fraud, waste and abuse of the welfare state they created.

There is enough money. More tax isn't needed. It's all a lie. But you've been gaslit into believing this is a rich vs poor debate.

I hope you understand what's at stake.