AW#33 RFS: On-Chain Banking

The phrase "the future of finance is borderless" has been thrown around for a decade. But we are finally moving past speculation and into infrastructure. We believe the future of banking will be programmable, transparent, and natively on-chain.

It's not just about trading crypto; but modernizing the global financial infrastructure—from asset tokenization, decentralized clearing, and settlement, to borderless cross-border payments.

Building this layer of the digital economy requires massive stamina, localized regulatory intelligence, and deep institutional trust.

How AppWorks Backs On-Chain Builders

On-chain banking wins on real-world adoption. You need to plug into the real world. Here is how we bridge that gap for you:

Real-World Web2 & Web3 Bridges: Through our deep network of corporate partners, we connect Web3 startups with regional financial institutions, telecom operators, custodians, and exchanges to run compliant, real-world Proof of Concepts (PoCs).

The Web3 Legacy (and Present): You are joining one of Asia's largest Web3 ecosystems, featuring 152+ active teams and 313 founders. Our alumni and portfolio networks include Web3 titans like @pendle_fi (AW#20), @StraitsX (MAS-licensed stablecoin infrastructure, AW#21), @sanctumso, and @SignalPlus_Web3.

Regulatory & Scaling Navigation: Compliance is the ultimate boss fight in FinTech. Benefit from hands-on mentorship by compliance advisors, Web3 pioneers, and traditional finance veterans across 9 distinct Asian markets.

Capital Access: With a total fund size of $386M, our investment team is close by to guide you navigate the full fundraising stacks across different instruments when the time is right.

And the utmost principal: the accelerator is 100% free with zero equity, tokens, or fees taken.

If you are a founder moving the world’s value on-chain, AppWorks is your strategic launchpad to navigate and dominate the Asian market.

📅 First Round Application Deadline: June 21, 2026

📍 Apply here: https://t.co/5Ho1nIKBWo

Are you building the future of on-chain banking, or know a team that is? Let's talk in the comments or tag them below! 👇

It was a privilege to be part of the Solana Network State Demo Day in KL, we are amazed by Malaysia’s builder density!

Sincere thanks to @SuperteamMY and @jelawangcapital for hosting.

What AppWorks does for founders:

- Equity-free, fee-free 3-month accelerator

- 2,000+ founder peers

- Warm BD pipeline into Asia TradFi

- $380M in capital to support founders in scaling

AppWorks Accelerator #33 applications are open now → https://t.co/kS7aslXNG6

Solana Network State Spring 2026 Demo Day is here 🔥

Presented by @AppWorks × @jelawangcapital

Pitch to investors, builders, and ecosystem partners in the room.

Happy to partner with Jelawang Capital + Superteam Malaysia on this.

Malaysia's crypto community has had some of the strongest momentum in the region, excited to see what this batch ships!

Five weeks of building. One afternoon to show what you made.

Solana Network State Spring 2026 Demo Day to showcase your work to investors, builders, and ecosystem partners.

Presented by @AppWorks × @jelawangcapital

📍 Kuala Lumpur

Details below 👇

In 1907 J.P. Morgan organized a private bank rescue, and the Fed was founded 6 years later.

Last month Stani organized DeFi United to rescue Aave. Is DeFi about to get its own central bank?

On @aave now, two groups of users are sitting on opposite sides of the same pool:

- wstETH holders are running a looping strategy — deposit wstETH as collateral, borrow ETH, swap the ETH back into more wstETH, repeat. A leveraged bet on staking yield.

- aWETH holders are the simple lenders — they just deposited ETH into Aave and hold aWETH as the receipt, expecting to redeem 1:1 anytime.

Now both sides are trapped:

- aWETH holders can't withdraw their ETH — the loopers borrowed all of it. Utilization is at 100%, the pool is empty.

- wstETH loopers are bleeding, because borrow rates have spiked past 30%, flipping their ~3% staking yield into deeply negative carry. And they can't unwind cleanly either — repaying Aave requires ETH, but they only hold wstETH. Dumping billions of wstETH into DEX pools would crack the peg and trigger a liquidation cascade.

This is where @0xfluid 's wstETH ↔ aWETH redemption channel comes in. Instead of forcing both sides to clear through the open market, Fluid lets them settle directly against each other: aWETH holders exit into wstETH (solving their liquidity problem), and loopers' collateral offsets the matching ETH debt (solving their negative carry). Both pressures release at the same time — without touching DEX liquidity, without breaking the peg.

This is the kind of move that justifies why DeFi still works. When one window closes, composability opens another. Real composability.

At AppWorks, we believe the next wave of DeFi lending maturity won't come from better yield strategies.

It will come from better collateral underwriting. Operational risk is still the most underpriced risk in the space.

Some thoughts as a crypto VC:

1. This Q1 number (5 pre-seed deals) needs a big asterisk. People don't want to announce it now, they hold the news for better timing. So the directional read is probably right, but the drop-off looks more dramatic than it actually is.

2. That said, the underlying trend is real and for a few reasons worth unpacking. Secondary has been rough post Q4 '25, and secondary is historically the leading indicator for primary, and crypto just makes this more extreme, as in crypto, the fundraising announcement itself is a GTM tool to make your way toward TGE.

But that playbook has died. So now teams are just sitting on the news, waiting for better conditions to amplify it.

3. Also from what I've heard, a lot of funds have genuinely slowed primary and rotated toward liquid. The logic being: liquid deals come with lighter vesting and even at high valuations, the risk/reward is more legible and markable. Hard to argue against that when primary deals are still priced as if a token premium exists.

4. The longer-tail issue is we're still unwinding the 2021-2022 hangover. A lot of GPs raised mega funds and still haven't found enough quality targets to deploy — which is part of why projects over the last 1.5 years raised way more than they needed at jacked valuations. This is now still correcting, slowly and painfully.

5. My bet is still that market will eventually settle around the 3 things in crypto with real PMF:

Bitcoin, payment rails, and speculation infrastructure.

Everything else is going to have a tough time justifying the ask.

Our team @cebillhsu has analyzed the current Pre-IPO market for Anthropic.

During our research, we discussed several Pre-IPO tokenization channel, but we found that the current transaction costs are simply too high to own Anthropic

If any team is currently working on a solution to liquidity for pre-IPO equity, please feel free to contact us.

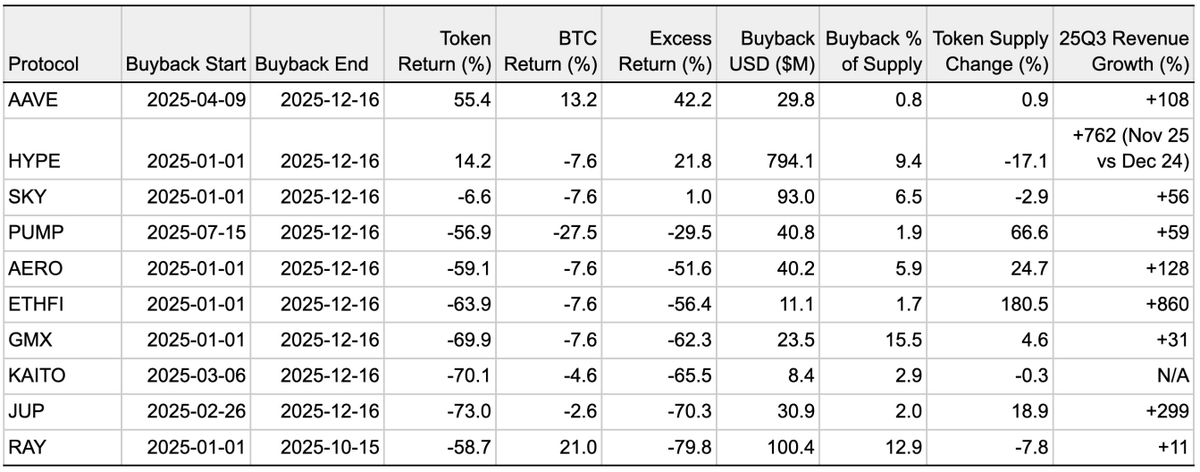

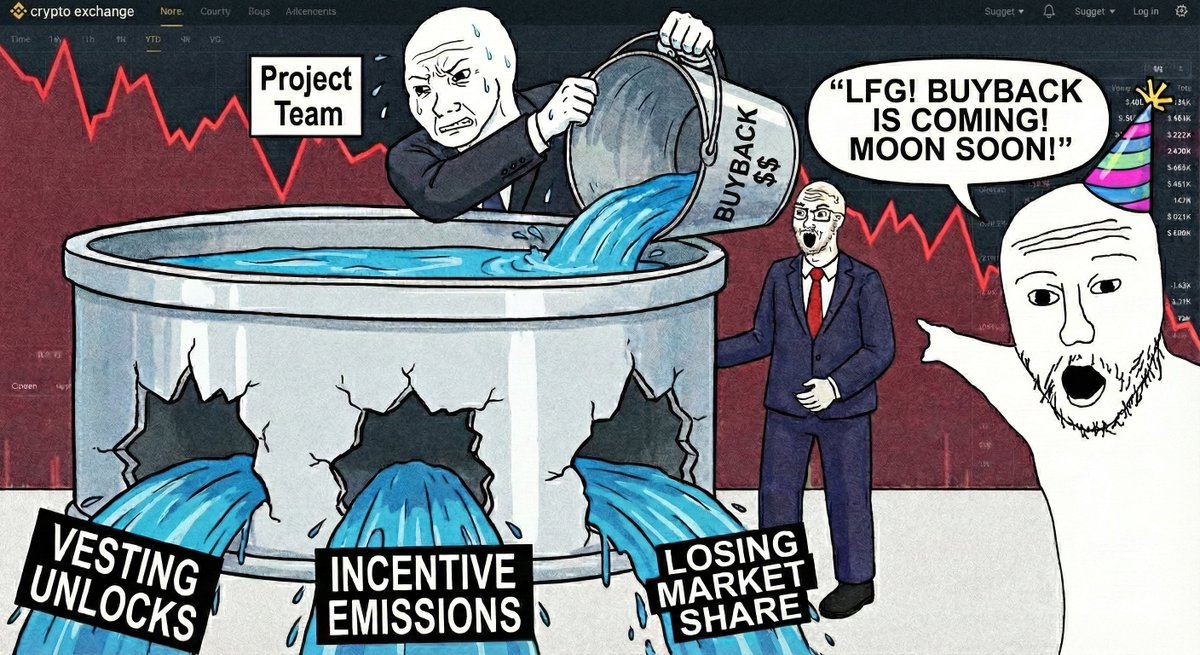

Do Token Buybacks Really Lift Token Prices?

This analysis aims to answer the question:

"Do token buyback explain token price performance (excess return vs BTC) in a consistent, repeatable way?"

TL;DR: Buybacks help, but they don’t “save” tokens

- Only 3/10 tokens beat BTC during their buyback windows (AAVE / HYPE / SKY). Big buyback headlines still often underperform.

- Net supply matters more than buyback spend: buybacks must actually reduce/flatten circulating supply; otherwise issuance, vesting, and emissions overwhelm the effect.

- The repeatable pattern: buybacks + flat/declining supply + improving fundamentals/competitive outlook → positive excess return. Miss any one, and excess return is hard—even with large buybacks

Result

This analysis focuses on 2025 (YTD) buyback amount, and uses excess return vs BTC as the price-performance metric, to assess whether there is any stable correlation/explanatory framework between buybacks and excess return. Also the analysis incorporated the broader context of net supply dynamics and fundamentals/competitive landscape, to avoid over-attributing price moves to buybacks alone.

Key Finding

1) Token returns are driven by many factors; buybacks can matter, but alone they have limited explanatory power

Even with high buyback % of supply, outcomes differ materially (e.g., strong outperformance like HYPE vs significant underperformance like GMX and RAY). In these 10 cases, only 3 tokens have positive excess return (AAVE / HYPE / SKY).

2) Net supply dynamics are more important than buyback.

Supply is affected not only by buybacks (repurchase/burn), but also by vesting, issuance, airdrop unlocks, incentive emissions, and any mechanism that increases circulating supply. Practically, what matters is the net effect: “buyback reduction” minus “new circulating supply added” over the same period.

3) Competition and business performance (revenue/TVL growth) can materially change the marginal impact of buybacks.

When core business growth is strong and supply is relatively clean, buybacks are more likely to be priced as long-term value return; when supply inflates rapidly or competition deteriorates, the buyback effect is often offset by supply or fundamentals.

4) Quick conclusion: Buyback + no additional supply + improving business & outlook → all three are necessary for excess return

From this 2025 YTD sample, the tokens with positive excess return (AAVE, HYPE) share a common pattern: (1) meaningful buybacks, (2) supply that is flat or declining (not inflating), and (3) business fundamentals that are stable-to-improving. When any one of these three conditions is missing, excess return becomes difficult to achieve—even if buybacks are large in absolute terms. SKY also has positive excess return, but its business fundamentals are not improving, resulting in only modest token performance.

- Missing buybacks or supply discipline: tokens like PUMP, AERO, ETHFI, and JUP all have buybacks, but supply still rises materially, overwhelming the buyback effect.

- Missing business momentum: tokens like GMX and RAY have buybacks and even some supply reduction, but face deteriorating competitive position or revenue decline, making it hard for buybacks to drive sustained outperformance.

Closing Thoughts

More broadly, 2025 may be remembered as the year crypto started learning capital allocation discipline.

Looking into 2026, the more interesting question is whether leading protocols can turn buybacks from a narrative into a predictable capital return policy—with clear rules, transparency, and credibility over time. Policy credibility comes from rules + repetition: either tie buybacks to FCF, or tie them to valuation—then execute through cycles.

Our principal Ching Tseng (@chingtsengtw) shared a piece about on chain governance recently.

Tokens are digital shares. Holders should focus on value appreciation and effective governance, while users engage with products without needing to own tokens.

The convergence of TradFi and crypto is here. Governance as code is the future.

What do you think—ready to treat tokens as shares?

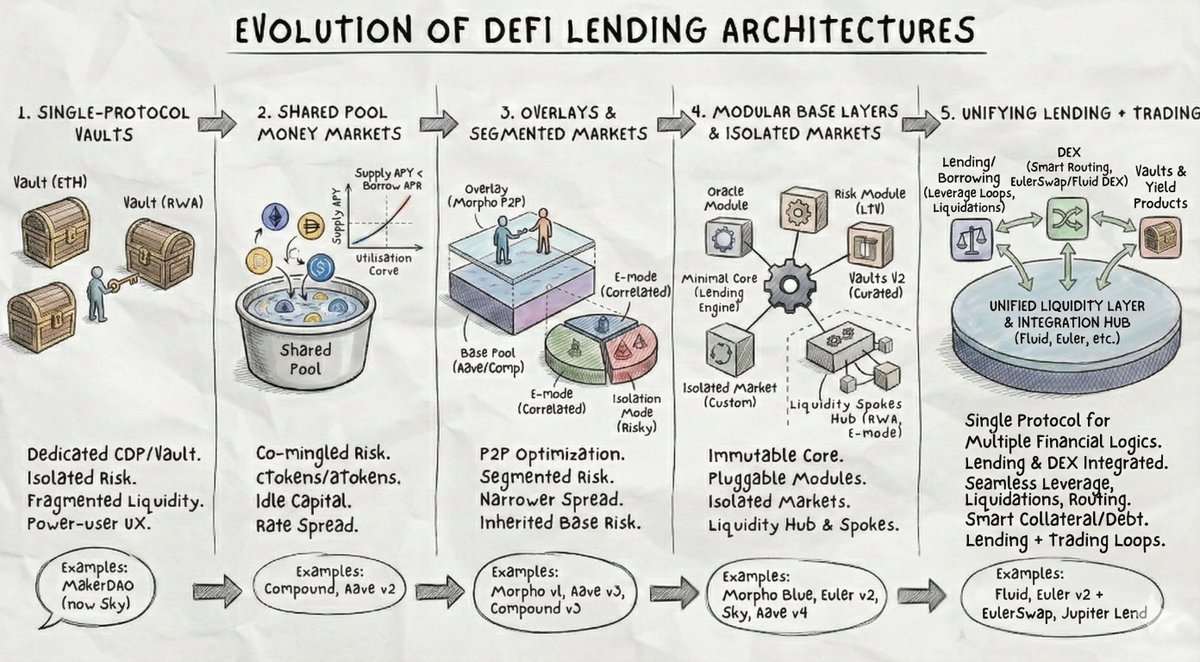

DeFi Lending Market Revisit 2025

The category is evolving into a multi-purpose liquidity hub, and the clearest way to see it is the architecture shift from Gen 1 to Gen 5.

Gen 1: Single-protocol vaults (@SkyEcosystem )

Separate vault per collateral type. Strong isolation, but liquidity is fragmented. It’s closer to onchain credit lines than a general money market.

Gen 2: Shared pool money markets (@compoundfinance , @aave v2)

Many assets in one pool, and deposits are “tokenized” into transferable receipt tokens (aTokens/cTokens). That deposit token can be reused across DeFi (as collateral, in vaults/strategies, etc.), which is why composability is high and TVL can scale fast. But risk is co-mingled and a lot of capital stays idle.

Because one bad asset can threaten the entire pool, a pooled model typically needs a wider supply/borrow spread and more conservative LTV parameters to absorb tail risk. That increases idle capital and lowers the protocol’s capital efficiency.

Gen 3: Optimization overlays and segmented markets (@Morpho v1, Aave v3)

Morpho v1 started as a P2P matching layer on top of Aave/Compound: match lenders and borrowers directly, and fall back to the underlying pool when no match exists. This narrows the supply/borrow spread by reducing the “pool buffer” wedge and idle liquidity.

In parallel, Aave v3 improved segmentation: Isolation Mode quarantines new/risky assets, while E-mode groups highly correlated, lower-risk collateral/borrow pairs so the system can safely allow higher LTV and better capital efficiency inside that bucket.

Gen 4: Modular base layers and isolated markets (Morpho Blue, @eulerfinance v2, Aave v4)

Minimal lending engines with risk modules unbundled. This reduces contagion and makes market creation more permissionless.

Morpho Blue and Euler v2 both split the world into Markets and Vaults: Markets are the primitive lending engine; Vaults sit on top and allocate deposits across markets via curators who set risk budgets and allocations.

Gen 5: Lending and DEX integration (@0xfluid Lending + DEX, Euler v2 + EulerSwap)

The big idea is to merge lending and trading loops so leverage, liquidations, and routing can feed directly into the lending market.

Fluid goes further with a shared liquidity layer: assets live in one base layer and lending, DEX, and vaults become applications on top, so liquidity doesn’t need to “move across protocols.”

Euler emphasizes the lending x DEX coupling via Euler v2 plus EulerSwap, but the DEX liquidity itself can still come from separate LP sources, so the key point is integration rather than a single shared liquidity pool.

The trajectory really is single‑asset vaults → pooled markets → overlays / segmented markets → modular base layers → shared liquidity layers + specialized sub‑protocols. Euler v2 and Fluid are the “latest generation” that not only modularize risk, but also natively unify lending and trading so that leverage, liquidations, FX and structured products are all downstream of one credit engine.

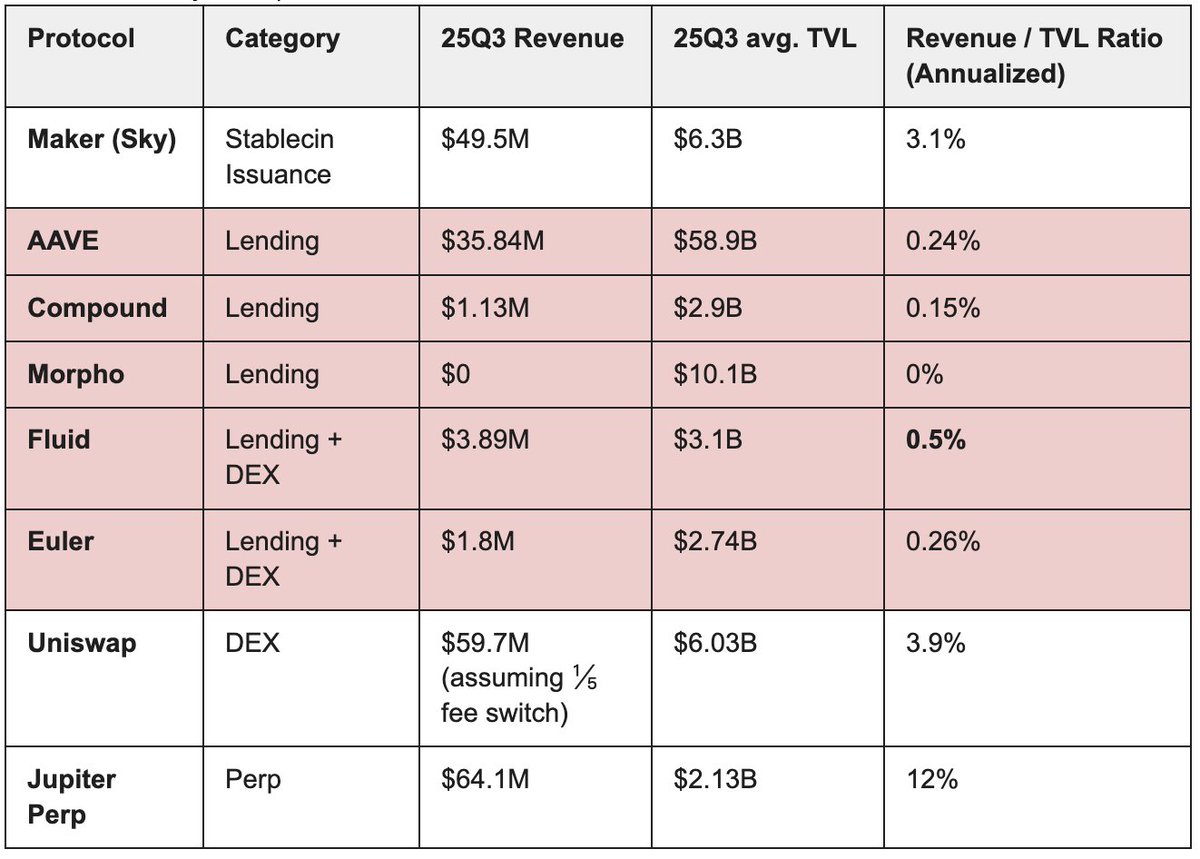

Why this matters: capital efficiency.

Whoever generates the most revenue per dollar of TVL tends to win.

Revenue over TVL (annualized, 25Q3):

Why some names look much higher on the same chart:

Maker (Sky): stablecoin issuance and balance-sheet style revenue, not a straight lending money market, so the TVL denominator isn’t apples-to-apples.

Uniswap: revenue is trading fees (sometimes modeled with a fee switch take rate), so strong orderflow can drive a higher revenue-to-liquidity ratio.

Jupiter Perp: perp revenue tracks notional volume more than TVL; margin needs can be small while volumes are huge, so the ratio can look extreme.

Why Fluid stands out structurally (Revenue / TVL = 0.5%, highest among lending competitors) :

Smart Collateral and Smart Debt mean collateral (and even debt) can be productive as DEX liquidity.

One capital base can earn two streams: lending yield and trading fees.

Its liquidation engine is designed around tick-based liquidations with an integrated DEX, enabling very high LTV with very low liquidation penalties (per its design claims).

This is where the market is heading: liquidity layers, not just lending pools.

This is the beginning. I’ll go deeper on Fluid’s design in future posts.

Stay tuned. Stay Fluid.

AppWorks #31 Demo Day Recap|Web3 Track

We had 28 teams on stage this round, and the Web3 track ended up pointing to a pretty clear through-line.

Everything’s moving on-chain. Not in a hypey way, more in a “this is probably what financial infrastructure looks like in a few years” way.

Our four Web3 teams captured that shift pretty neatly:

@hataglobal (MY): a regulated exchange anchoring Malaysia’s crypto market.

@Juic3Labs (TW): battery assets as RWA.

@SingularDAO (HK): tokenized pre-IPO equity with actual distribution paths.

@Auki (HK): a crypto-powered data layer for robots.

---

For next batch, we’re looking for teams building across this entire on-chain banking stack.

If you’re working on anything along these lines:

- stablecoin payments or wallets (consumer or B2B)

- crypto / virtual cards

- cross-border payout systems

- treasury or liquidity management

- expense automation, AR/AP (on-chain or hybrid)

- RWA issuance or secondary markets

- custody, MPC, permissioning

- regtech, KYB/KYC, risk

- liquidity infra, on/off-ramps, market-making primitives

Applications for AppWorks Accelerator #32 are open. Join the largest founder community in GSEA. 👉 Apply here: https://t.co/wLFjegwstC