@cloudsweeper99@Ross__Hendricks Yeah I think the difference is that these AI data center investments deal with depreciating assets and it’s difficult to know if you’ll get a return.

@Ross__Hendricks They do like to be able to reinvest at attractive returns on capital so long as it is fairly predictable long term. BNSF and Berkshire Hathaway Energy come to mind

🚨 THE ENTIRE AI BOOM MIGHT BE BUILT ON FAKE REVENUE.

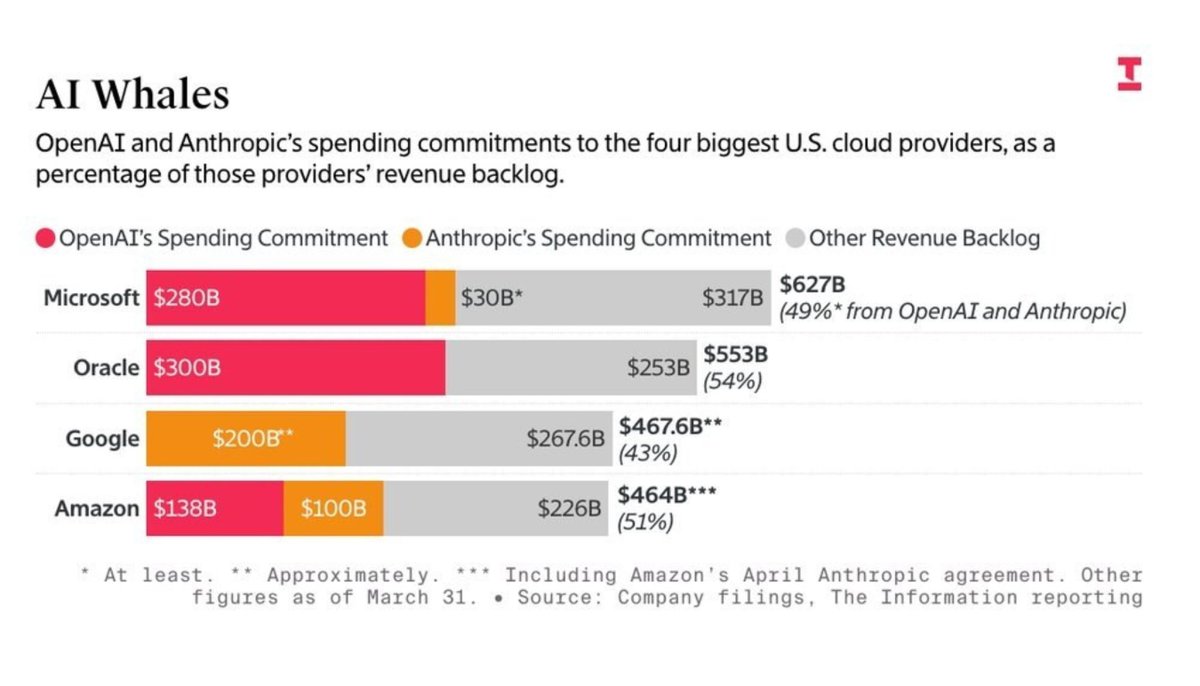

Latest corporate filings show that OpenAI and Anthropic alone make up over half of the entire $2 trillion future cloud backlog held by Microsoft, Oracle, Google, and Amazon.

This massive pipeline is actually being created through a circular accounting trick called a round trip revenue loop.

But how it works ?

A tech giant gives billions of dollars to an AI startup as an "investment". But hidden in the contract is a strict rule forcing the startup to hand that exact same money straight back to the tech giant to rent their computer servers.

Look at the documented case of Microsoft and OpenAI.

When Microsoft invested $13 billion into OpenAI, it didn't just give them cash; it gave them "cloud credits" to use Microsoft servers. OpenAI used those exact credits to train its AI models, and Microsoft then turned around and recorded that server usage as brand new "cloud revenue" from a customer.

The tech giant is literally paying itself with its own money and calling it a sale.

This is why OpenAI’s annual cloud bill has ballooned to over $60 billion, double its actual revenue of $25 billion, kept alive solely by this recycled funding loop.

Anthropic runs the exact same play, spending $2.66 billion on Amazon Web Services in just nine months, which was basically 100% of all the money it earned at the time.

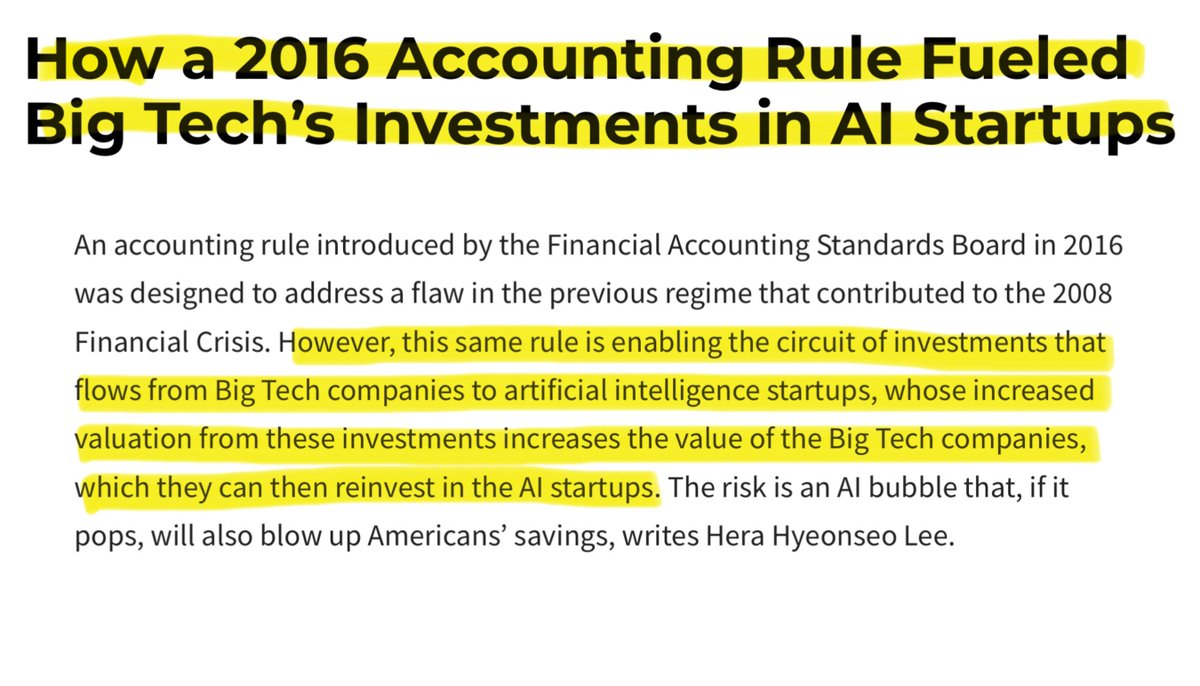

This manufactured demand triggers a second accounting trick where tech giants book massive paper profits. Every time a startup gets a higher value from a new funding round, the tech giant updates the value of its investment on its books and counts that unearned paper gain as direct profit.

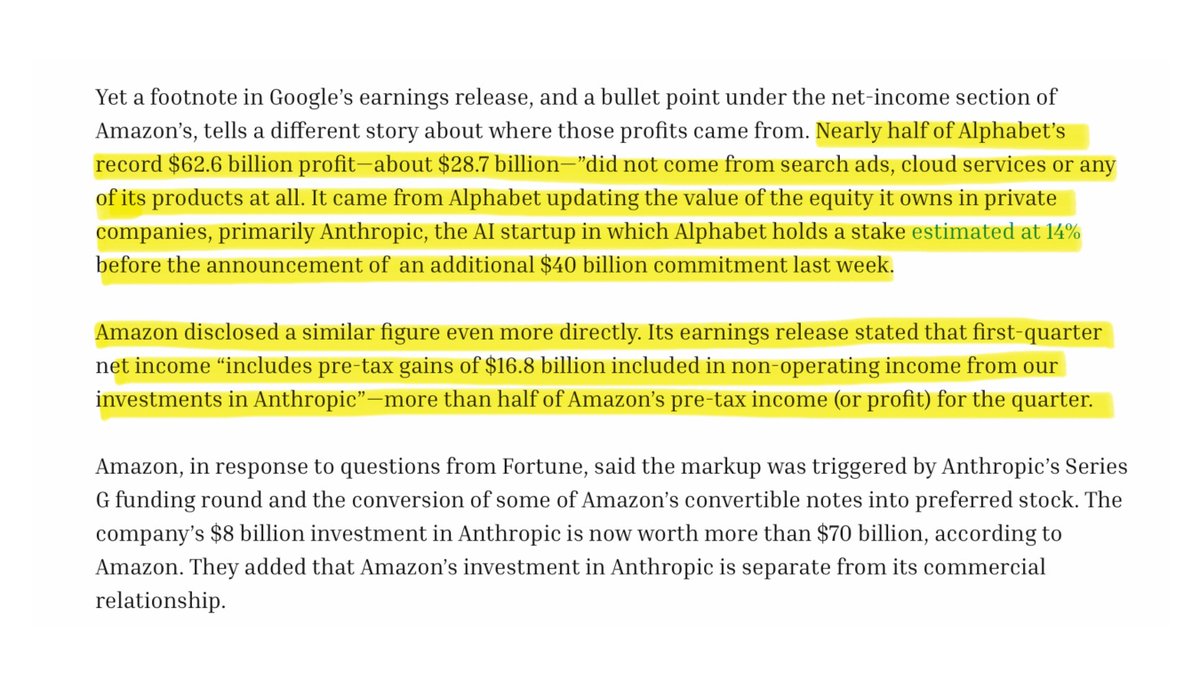

In Q1 2026, Alphabet reported a record $62.6 billion profit, but $28.7 billion nearly half, was just a paper markup on its Anthropic investment. In the same quarter, Amazon reported $30.3 billion in profit, but $16.8 billion of it was just an Anthropic paper gain.

While Amazon reported record profits, its actual free cash flow collapsed 95% to just $1.2 billion because it had to spend $44.2 billion in real cash to build physical data centers.

This has created a massive danger where these giant companies rely heavily on just one or two unstable startups. Microsoft has 49% of its $627 billion future backlog tied to OpenAI, while Oracle has an incredible 54% of its entire $553 billion pipeline relying on OpenAI alone.

This perfectly mirrors the 2001 dot-com crash when Global Crossing and Qwest Communications swapped identical fiber-optic network capacity with each other just to book fake sales.

Qwest had to erase $1.4 billion in fake income, and Global Crossing went completely bankrupt.

The only difference is that the dot-com swaps were illegal, but today's AI loop is fully legal under current accounting rules.

This legal loop inflates tech company stock prices, forcing automatic retirement accounts and index funds to buy even more of these tech stocks. It is a self feeding loop where investments, sales, and stock prices all go up on paper without the AI technology ever making real cash profits.

@JohnRud58360421@KobeissiLetter Feel like I’ve been screaming the same message into a void for awhile. If it wasn’t the market cap weighted index it wouldn’t get past most committees.

Back in the 1960s there was a company called National Video. They made color television picture tubes, and were the first to produce a 23-inch rectangular color TV picture tube. It quickly became the industry standard, and every major TV set producer scrambled to get their hands on National Video’s picture tubes. They literally couldn’t make them fast enough.

The stock went from a low of 15 in 1964 to a peak of 120 in October 1965. The final 70 points came in just the last few months.

Eventually, though, the Motorola’s and Zenith’s of the world produced their own color TV picture tubes. They didn’t need National Video’s any longer.

The stock went from 120 to a low of 40 in 1966, 15 in 1967, and then to zero in 1968 as the company went bankrupt. The poor thing couldn’t even make it to the Go-Go years.

In those days, Mueller and Company produced tick volume charts. National Video’s chart depicted the stock going from Northwest to Southeast in a straight line while the tick volume line went straight up.

The stock was a fundamental short. In those days, short sales could only be executed on an uptick. Which meant the whole world was always offered up an eighth.

Oh, National Video’s ticker symbol? NVD.A.

This story is true, but any resemblance to any other companies is purely coincidental.

@CryptoTice_ Sovereign wealth funds are for countries with large surpluses to avoid an overly strong currency. We have large deficits making this a margin account. Just big government controlling capital for no good reason.

@ByEricPratt This is why I just don’t subscribe to any of it. I’d pay if I could watch what I wanted but sadly they’d rather have me spend my entertainment dollars elsewhere.

@buccocapital@TheStalwart When you pay your staff with stock it becomes an issue if that stock declines significantly. Lots of these have never actually been profitable unless you are willing to believe giving equity doesn’t have a cost. In which case, why should anyone buy it?

@nim_chef I think it’s probably too things. 1.) Customers prioritize speed over everything else. 2.) they couldn’t achieve enough route density.

What do you think?

This is so much better than Instacart. Refrigerated vans, more orders per route, better compensated drivers. Just signed up for the membership! $KR https://t.co/MM0hX12NPW