펌) 변호사님 말씀

“사람 인생 그렇게 쉽게 안 망한다.”

변호사로서 수많은 의뢰인들의 삶을 지켜보고 있는데, 의외로 사람 쉽게 안망합니다. 심지어 전과가 생겨도, 다시 일어서서 사업하시고 더 대성하시는 분들 많습니다.

하물며 그냥 인간적인 갈등이나 다른 직장으로 이직하는 거, 잠시 백수 생활하시는거, 다른 업계로 넘어가시는 거, 자영업 하시는 거 다 괜찮습니다. 장담합니다. 초반에 빚 너무 져가면서 사업만 안하시면 됩니다.

특히 인간관계나 집단에서 가스라이팅 당하거나 혼자 스스로 가스라이팅 해서 '이거 아니면 안된다' '여기서 꼭 버텨야 된다' 이런거 하지 마십시오.

적당히 항의하고 감정표현하세요. 항의하는 부하 직원 때려죽인 상사는 못봤지만, 당해주는 부하 직원 죽을 때 까지 괴롭히는 상사는 자주 봤습니다.

지들이 뭐 힘이 있어서 이직 막는거 그런거 안됩니다. 세상 넓고 일자리 많습니다. 혹여 임금 좀 낮춰가도 안죽습니다.

스스로 헤쳐나오기 힘들면 감정적으로는 정신과 의사한테 의지하시고, 법률적으로는 변호사한테 의지하세요

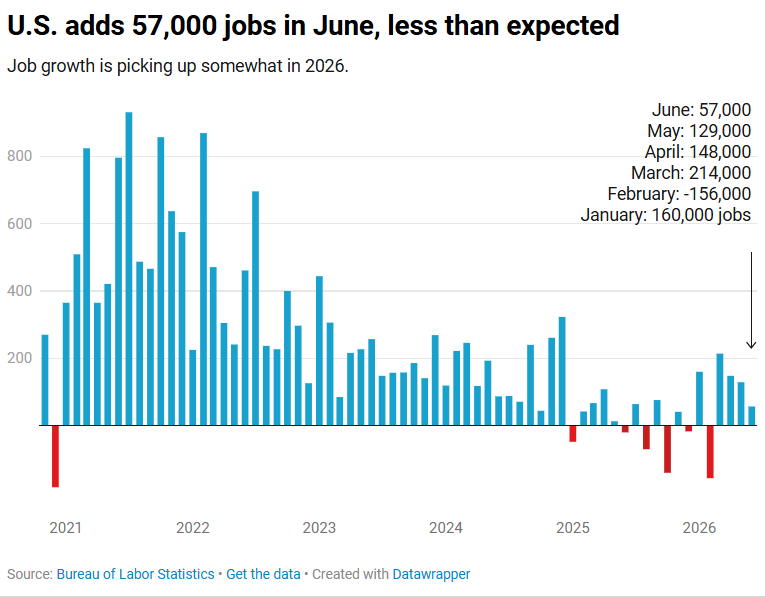

JUST IN: A disappointing jobs report. The US economy added 57,000 jobs in June (below expectations of 115k). Hospitality jobs decline by -61k. Plus, April and May were revised lower by -74,000.

The unemployment rate fell to 4.2% --> the lowest in a year, but mainly due to a big drop in people job hunting.

The bad news = Wages aren’t keeping up with inflation. Wage gains were 3.5% in the past year, which is below ~4% inflation.

Investors are increasingly seeking downside protection:

Open interest in Volatility index, $VIX, call options relative to put options is up to ~3.1, the highest since July 2025.

This is also the 2nd-highest level since February 2025, before a market correction started.

Put differently, traders are positioning for higher volatility at roughly a 3-to-1 ratio versus lower volatility.

Furthermore, the spread between the $VIX and the S&P 500's 20-day realized volatility is down to around zero, the 2nd-lowest in at least 2 years.

This suggests protection against a future market selloff remains historically cheap.

Investors are bracing for more market volatility.

🚨THIS IS SCARY:

The S&P 500 Shiller PE (CAPE) ratio has hit 42.7x, the 2nd-highest EVER.

By comparison, the long-term average is 17.4x.

This metric divides the S&P 500's price by its average inflation-adjusted earnings over the last 10 years, making it one of the most reliable long-term valuation tools available to investors.

The ratio is now approaching its Dot Com Bubble all-time high of 44.2x.

In the past, whenever the S&P 500 reached valuations this expensive, the 10-year annualized return was NEGATIVE.

Is anyone paying attention to this?

Job openings for January were revised up, but the three-month moving average continues to gently grind lower through February

There were 0.9 vacancies for every worker counted as unemployed in February, near the low for the current business cycle.

📉 PE 대형 4사 주가 고점 대비 -36% 급락했는데, S&P 500은 고점 대비 -3%에 불과함

• 블랙스톤 $BX, KKR $KKR, 아폴로 $APO, 칼라일 $CG 균등가중 바스켓 기준 총수익률이 고점에서 36% 빠짐

• 같은 기간 S&P 500은 사상 최고치 대비 겨우 3% 하락한 수준에 머물러 있음

• 2017년 이후 이 PE 바스켓은 조정 때마다 -25%, -35%, -36%, -19% 등 S&P 500보다 훨씬 깊게 빠지는 패턴을 반복해옴

• 이번 -36% 낙폭은 2020년 코로나 급락(-36%)과 동일한 수준이고, 역대 최대급임

• 특이한 건 S&P 500이 거의 고점권인데도 PE주만 이 정도로 무너졌다는 점임

• 지수가 버티는 건 시가총액 상위 소수 종목의 쏠림 효과가 실제 시장 내부의 체력 저하를 가리고 있기 때문이라는 시각도 있음

S&P 500과의 괴리가 이 정도로 벌어진 건 이례적임.

수면 아래에서는 이미 스트레스가 쌓이고 있고, 크레딧 시장과 딜 플로우 위축이 계속되면 결국 지수도 현실과 조정을 맞춰야 하는 국면이 올 수 있음.

🚨Private credit market cracks are rising at an alarming pace:

The median listed BDC is trading at ~0.8x its net asset value (NAV), the lowest since 2020.

This means the market is pricing these funds at a ~20% discount to what they claim their loans are worth.

This comes as NAV writedowns, large outflows, asset sales, dividend cuts, and redemption gates hit the sector.

By comparison, in the 2008 Financial Crisis, this ratio collapsed to ~0.35x.

The private credit sector is flashing red.

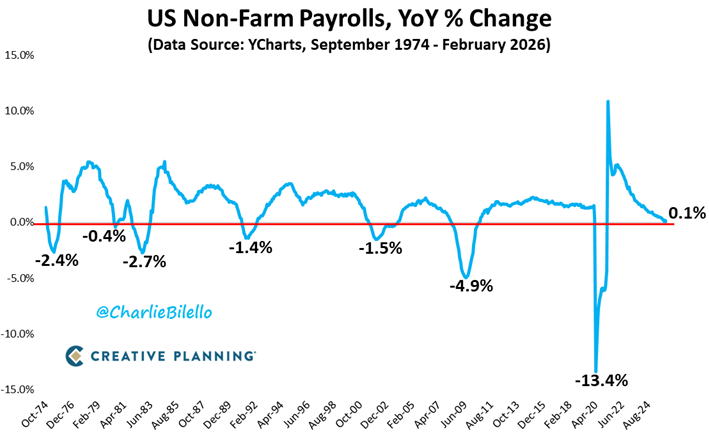

The total # of jobs in the US increased by just 0.1% over the past year. In the last 50 years, this same slowdown in the labor market has ONLY occurred during recessions (1974/1980/1981/1991/2001/2008/2020).

Is this time different?