I don't post often on X, but when I do it's usually to share my latest Substack research.

I find nuanced investment analysis deserves more than 280 characters.

Deep dives on company fundamentals: https://t.co/d8iohygrhB

A Disney employee had 460,000 conversations with Claude in 9 days.

One every 1.7 seconds.

This is what AI “adoption” looks like.

https://t.co/3l8KNAZaem

$FOUR is down 15% today and 33% since we tossed it in the "Too Hard" basket.

A lot of die-hards came for my throat when I made this call. At Bearstone, we don’t do feelings. We stay analytical, cold-blooded, and willing to follow the data where others follow the herd.

“We have three baskets for investing: yes, no, and too hard to understand.”

— Charlie Munger

Which basket does $FOUR belong in?

Shift4: Valuation and Personal Opinion:

https://t.co/hnXuLCKSUl

$OXY is moving into a dominant, first-mover position in Direct Air Capture (DAC).

CEO Vicki Hollub projects the carbon capture industry could eventually reach $3-5 Trillion. While DAC isn’t economical yet, $OXY is leveraging "Digital Twin" tech via their @AWS partnership to crush the cost curve.

You’re looking at a setup similar to the early days of Tesla - but with a massive difference:

Unlike early Tesla, you’re buying a stable, cash-flowing business with a 10% earnings yield attached to the "lottery ticket."

For a deep-dive analysis (5k words), read here:

https://t.co/CuHek9tgvI

What if a 1% improvement in technology unlocked billions of barrels of oil without buying a single new acre? 🛢️

Most investors hate oil because of the "Wildcatter’s Dilemma." But the gap between SEC-mandated "Proved Reserves" and actual "Oil-in-Place" is where opportunity lives. My deep dive into the 16.5B BOE prize at Occidental $OXY:

https://t.co/9hCNSQDL8A

In this post, we discuss United’s $UNH PBM business and question whether its positioning is as comfortable as it appears from the outside.

https://t.co/qDXzoEwzNg

In this article, we track the evolution of OptumInsight and the mechanics of the machine through the lens of Behavioral Health. We also break down the competitive and regulatory landscape currently unfolding around it.

In my next post, I’ll provide my final thoughts and valuation on United $UNH.

https://t.co/PwVcbLcI4Y

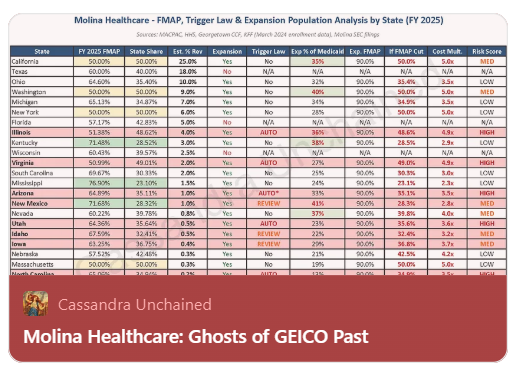

Molina Healthcare: Ghosts of GEICO Past

"In 1974, however, GEICO started selling auto insurance to the public. With almost no actuarial experience, GEICO’s pricing was a guess and turned out to be too low. A frustratingly common problem in the insurance industry. This poorly informed underwriting dove-tailed with the high inflation environment and a new law forcing GEICO to take on high-risk drivers. The perfect storm sank GEICO in 1975 and into 1976, and ultimately provided the opportunity for Buffett’s Berkshire Hathaway to swoop in.

Buffett likes to say he bought GEICO three times – in 1951 as a student, in 1976 with Berkshire Hathaway, and 1996 when Berkshire Hathaway fully acquired GEICO. The whole saga is a testament to good analysis and patience.

With that, here in 2025, I present Molina Healthcare."

$MOH

https://t.co/3JISZZlxCh

H&R Block $HRB reports earnings today with the stock near 52-week lows. Here’s a look at why it’s trading down and what I think:

https://t.co/akkaFK0Zyq

Williams‑Sonoma $WSM is live.

This one is a single deep dive on why Williams‑Sonoma is, operationally, one of the best - if not the best - furniture retailers in the business today. I walk through how their data and omnichannel distribution actually work in practice, and why that shows up in their margins.

I’ll probably come back to this name over time to add more work or look at the stock’s history, but for now this is a standalone piece.

Next week, there’s a little surprise coming on Tuesday. On Thursday, we’re circling back to another fintech name: Wise.

Looking forward to hearing what you think, and as always, hope you enjoy the read.

Williams‑Sonoma: Data and Design https://t.co/2rthC5OBTf

The last part of my Constellation Brands series went out yesterday. In it, I examine whether the recent downturn is structural or cyclical and then lay out a base case range of what STZ could be worth in a decade. I hope you enjoy reading it.

https://t.co/I20CGVLkg5

I bought Williams-Sonoma $WSM about two years ago. Its financials were incredible, there was very little downside to the investment, and I'm a big fan of Pottery Barn, so I pulled the trigger. It has nearly tripled since. Interestingly I didn't see any major investors buying it or hear anyone talking about it.

I think this stock will periodically trade down in housing cycles. So we're going to analyze it so everyone is prepared for the next dip.

The first article drops on my Substack on Thursday. Looking forward to discussing it with you all.

New post.

The Payments Giants: FEE FI FOUR Umm…

The attraction for most investors is that the payments business at scale intuitively is a moneymaker. A toll bridge on all the payments happening in some section of the world or economy, with the toll so small no one that pays it worries about it. This should work as long as the toll bridge can keep other bridges from being built in that particular section.

The difference between one toll bridge and two on any one section of river is night and day. So, most try to dominate some part of the river, but barriers to entry are not what they once were. Irreverent newcomers have installed ferries all over the place without putting the time and capital into a bridge.

When a mature business loses its pre-eminent position, it must buy things to grow. Or, sell to another buying things to grow.

https://t.co/H9ybTEyUM8

This article is primarily focused on analyzing the unit economics of each hectoliter of beer brewing capacity at Constellation Brands $STZ. It outlines the methodology in detail and presents my base-case assumptions for maintenance capex. However, I encourage investors to adjust the numbers based on whether they prefer a more conservative or optimistic outlook. I hope you enjoy the read!

https://t.co/FvcLPPlxXg

“We have three baskets for investing: yes, no, and too hard to understand.”

— Charlie Munger

Which basket does $FOUR belong in?

Shift4: Valuation and Personal Opinion:

https://t.co/hnXuLCKSUl

PayPal’s $PYPL unbranded and branded segments have a symbiotic relationship.

If one falls, the other weakens.

They’re both under attack.

https://t.co/TWX2CyVYbU