"to house all of finance."

That's the goal @HyperliquidX’s founder laid out to the @WSJ.

$HYPE up 100%+ this past year. ~$16B market cap.

Access $HYPE staking exposure with $HYPG.

https://t.co/Kl3dRispwY

Imagine a world where retail traders operate at the same efficiency as institutional desks

where you don’t need 50 analysts to have the same edge

Introducing TrueNorth, the world’s first agentic brokerage

built on @HyperliquidX 🧵

A DeFi protocol just force Coinbase and Circle to share their profits.

And those profits now automatically buy $HYPE. 🤯

Here's something that's never happened before in financial history 👇

A decentralized exchange negotiated a deal where two of the world's biggest financial companies hand over most of their income — directly to the protocol.

Not a rumor. This is live. Let me explain. 💰

First — the scale nobody is talking about:

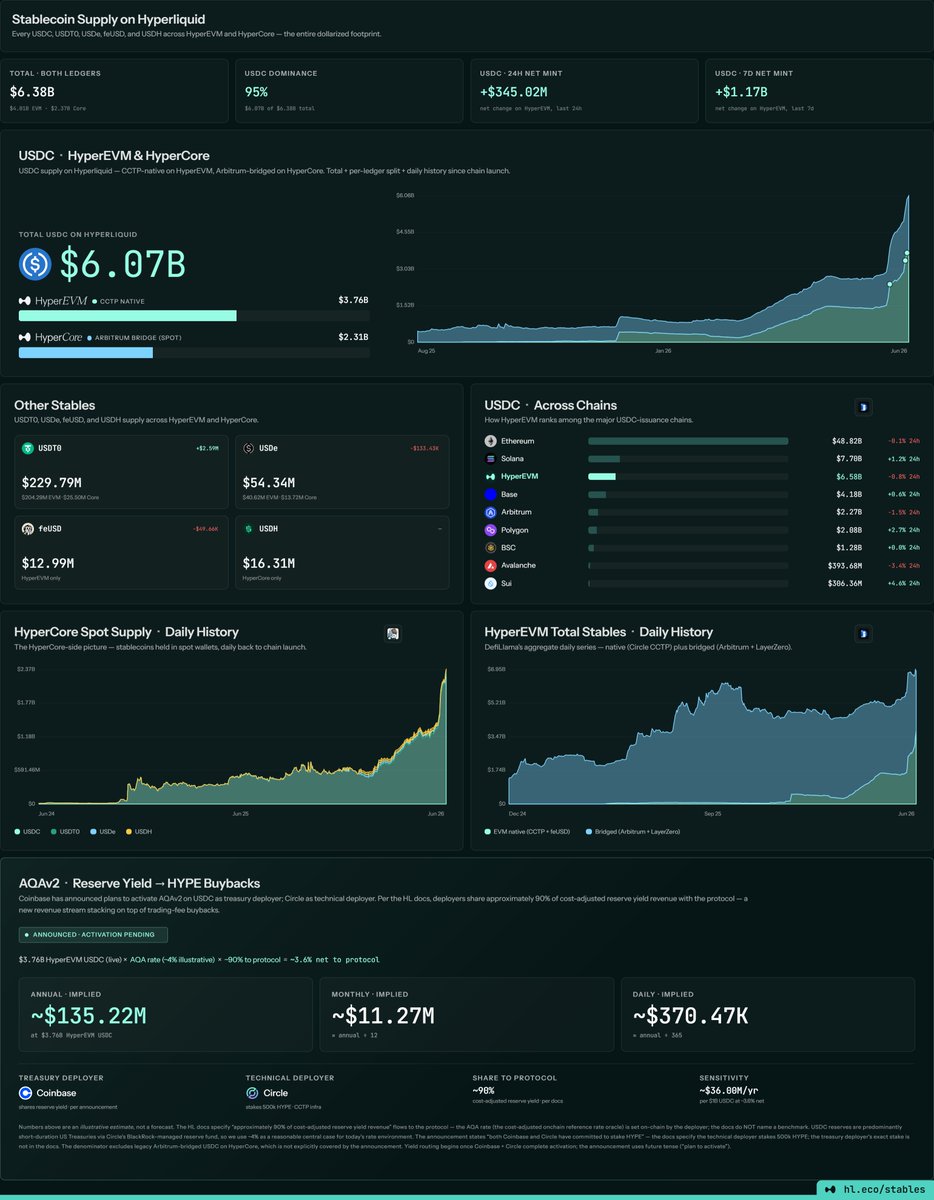

Hyperliquid now holds $6.90 BILLION in stablecoins.

To put that in perspective:

🥇 Ethereum: $48.82B USDC

🥈 Solana: $7.70B USDC

🥉 HyperEVM: $6.58B USDC ← Hyperliquid

4️⃣ Base: $4.18B

5️⃣ Arbitrum: $2.27B

6️⃣ Polygon: $2.08B

7️⃣ BSC: $1.28B

A DEX built 3 years ago is the #3 USDC chain on Earth. 🌍

And money is pouring in FAST:

📊 Last 24 hours: +$346 million new stablecoins minted

📊 Last 7 days: +$1.17 billion net inflow

That's not a trickle. That's a flood. 🌊

Now here's the deal that changes everything:

For years, this $6.9B sitting in Hyperliquid was generating massive yield.

How? Simple: US Treasury interest rates.

$6.9B × ~4%/year = $276 million/year in interest income

The problem?

That yield historically flowed to Circle and Coinbase — not to Hyperliquid or its users. The protocol supplied the users, the liquidity, and the trading activity that made the stablecoin useful — but kept none of the income.

Hyperliquid decided that needed to change. 🔧

The AQAv2 deal — explained simply:

Think of it like owning a shopping mall.

Before: Tenants (Circle, Coinbase) kept all the rent money.

After AQAv2: The mall owner (Hyperliquid) now keeps ~90% of the rent. 🏢

Under the new arrangement, Coinbase serves as USDC treasury deployer and shares the vast majority of reserve income with the Hyperliquid protocol.

Compass Point analysts estimate the deal removes roughly $60-80 million in annual EBITDA from Coinbase and Circle combined.

Where does that money go?

➡️~90% of all USDC reserve yield → Hyperliquid protocol➡️ Protocol uses it to buy $HYPE from the open market➡️ Automatically. Every day. On top of the $800M/year in trading fees.

Implied additional yield revenue:

💵 ~$135M/year (illustrative at ~4% rate — estimate, not guaranteed)💵 ~$11.27M/month💵 ~$370K/day

⚠️ Activation still pending — yield routing begins after Coinbase + Circle complete technical setup

The skin-in-the-game signal:

Circle committed to stake 500,000 HYPE tokens as part of the deal. Coinbase also increased its staked HYPE position.

The companies providing the stablecoin infrastructure are now forced to be aligned with $HYPE.

If HYPE goes up → they profit. If HYPE goes down → they lose. 🎯

The total revenue picture for $HYPE:

💰 Trading fees (existing): ~$800M/year💰 Stablecoin yield (new, AQAv2): ~$135M/year (illustrative)

Combined: ~$935M/year in protocol revenue — and this is BEFORE US market access opens.

The precedent this sets:

Compass Point warns that other DeFi protocols may now demand similar revenue-sharing terms from Circle and Coinbase — creating pressure across the entire stablecoin industry.

Hyperliquid didn't just negotiate a deal for itself.

It changed the rules for every protocol. Forever. 📜

⚠️Not financial advice. Always DYOR.

Hyperliquid traders playfully end almost every post with the word “Hyperliquid,” regardless of the topic. Many adopt the platform’s mascot, a smiling, green-jacketed cat named “Hypurr,” as their social-media avatars.