@myapdx Feels like a live demonstration of the other discussion.

Even if only a handful of companies remain as frontiers, each new release raises the bar for everyone else. The innovation cycle just keeps accelerating.

Ohh, truthfully yes. In terms of number of frontier competitors, I agree it'll likely be only a handful that can stomach the cost, just as you pointed out.

I was thinking more about competition as an engine for innovation than competition in terms of market structure. Even if only few remain at the frontier, each breakthrough will force the others to learn, adapt or iterate, which accelerates the progress pace.

As a geologist, I'd also add one more ingredient:

Materials.

More AI requires more compute. More compute requires more energy. More energy infrastructure requires more copper, rare earths, lithium, nickel and steel. All finite resources

Abundance starts with what we can actually build.

Intelligence and energy are necessary, but they aren't sufficient.

Abundance also depends on incentives, institutions and distribution.

History is full of technological breakthroughs that increased wealth without benefiting everyone equally.

The question isn't just can we create abundance, but how it's shared.

Whether or not this is intentional, it is already highlighting a trade-off.

Closed models optimize control and rapid iteration.

While open models optimizes for resilence and user autonomy.

I suspect the long term winner won't be which is smarter or better today, but whichever ecosystem compounds its users trust faster

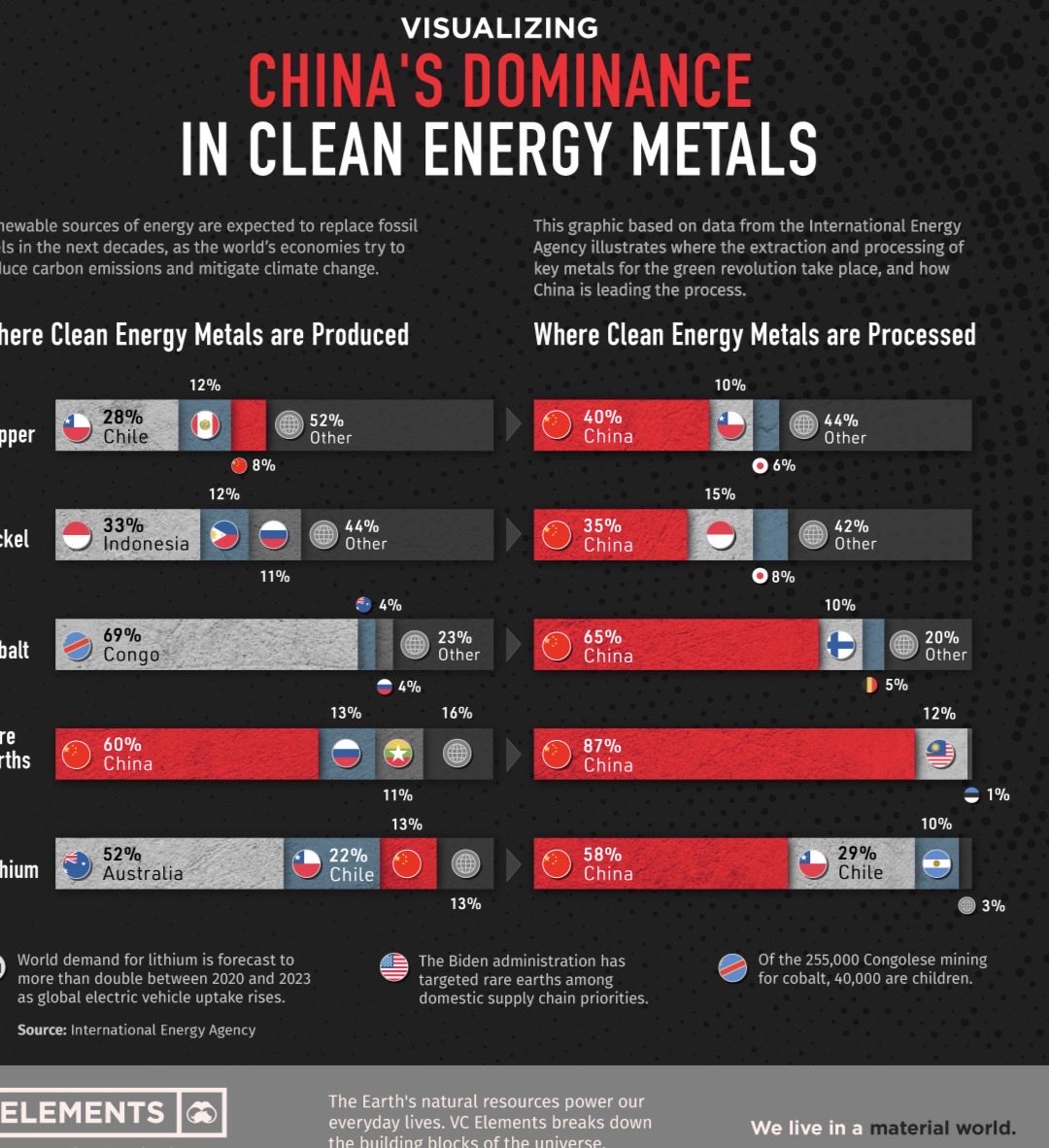

I think critical minerals will define the next decade.

AI is already on everyone's radar but only a few are talking about the rocks that make AI possible.

Data centers need power.

Power grids need copper.

Robots need rare earth elements.

EVs need lithium, nickel and graphite.

Advanced chips depend on highly specialized mineral supply chains.

The future of intelligence isn't built on code alone. It relies on geology.

The conversation around critical minerals isn't just about mining. It's about who controls the physical foundation of tomorrow's technologies.

Software may be eating the world.

But the Earth still supplies the ingredients.

The next technological revolution won't just be written by software engineers.

It will also be mined, refined and powered.

That's why I think every discussion about AI should eventually becomes a discussion about energy, geology and, inevitably, strategy.

Two Themes We’re Betting Big On 3/4

Critical minerals: where supply chains are starting to matter again

The second theme where we’ve been allocating capital is critical minerals and strategic supply chains.

For years, the market optimized almost exclusively for the lowest-cost producer.

Today, the world is slowly realizing that security of supply can matter just as much as cost.

China has built dominant positions across many commodity supply chains—not only in mining, but also in refining, processing and downstream manufacturing.

That worked extremely well in a globalized world. But in a more fragmented geopolitical environment, we believe many Western supply chains are simply too fragile.

We’ve already seen how powerful these setups can become.

$MP (MP Materials) was one of the best examples: one of the few Western rare earth companies attempting to build an integrated supply chain from mining through refining to permanent magnet production.

More recently, we’ve seen a similar dynamic in tungsten, where Chinese export restrictions helped expose how concentrated global supply really is.

Our exposure there has been $EQR.AX (EQ Resources), which we believe is becoming one of the most important tungsten producers in the Western Hemisphere.

But the broader point is not only rare earths or tungsten.The same logic applies across multiple commodity markets.

One area we’re particularly focused on right now is copper.

Unlike tungsten, our copper thesis is less about a single export restriction and more about long-term supply/demand.

AI infrastructure, data centers, grid upgrades, robotics, EVs, renewable energy and electrification all require significantly more copper.

At the same time, many large high-grade deposits are being depleted, new projects often have lower ore grades, higher capex requirements and longer permitting timelines, and the sector has been underinvested for years. That creates a very attractive setup.

What makes the opportunity in miners even more interesting is valuation.

Across smaller commodity producers, we still find companies trading at free cash flow yields that can approach 40–50% under current commodity prices.

That is extremely rare in most parts of the market. Small producers are often ignored, under-covered and too illiquid for large institutions. But for us, that’s exactly where opportunities can appear.

One account I read regularly in this space is @GPs_capital_, who does excellent work on small commodity producers across different geographies and metals.

One example we currently like is $ORV.TO (Orvana Minerals).

It gives exposure to both gold and copper, trades at what we believe is a very low valuation relative to current cash generation, and has several potential catalysts ahead.

GP Capital has written very detailed work on the company, and we found the setup compelling as well.

In our view, companies like Orvana are a good example of why we still spend time in small-cap mining despite the sector being difficult.

When sentiment is poor, the market often prices these businesses as if current cash flow is temporary or irrelevant. But if management executes and commodity prices remain supportive, the upside can be substantial.

The bigger picture is simple:

The world needs more strategic materials. But supply is increasingly difficult, expensive and geopolitically sensitive.

That combination creates opportunities in small producers with real assets, current or near-term cash flow and exposure to commodities where supply chains are structurally tight.

We don’t think every mining company deserves a high valuation. Most don’t.

But selected small producers in the right commodity, right jurisdiction and right set up still offer some of the most asymmetric opportunities we see today.

Times and times again , I treated AI like a simple software.

But this month reminded me that governments are starting to treat it like strategic infrastructure.

Whether the original restrictions were primarily about security, leverage, or both is almost beside the point.

The bigger lesson is this:

The nations that control frontier AI may increasingly influence who gets access to the tools that shape economies, research, and innovation.

We've spent decades talking about sanctions on oil, chips, and trade.

It's worth asking whether access to frontier intelligence has become form of geopolitical leverage.

This isn't about who wins the AI race but about who is privy to such infrastructure

It's about what the world looks like when intelligence itself becomes an export-controlled resource.

Cloude ai şirketi tüm internetin güvenlik zaafiyetlerini çözebilen mythos sürümünü kapattıktan sonra piyasaya bunu sürdüler.

Fable bile mythos versiyonunun %5 i bile değildir.

Dünya 1-2 sene sonra çok korkunç yere evrilecek web2 neredeyse bitme noktasına adım adım gidiyoruz.